In the fast-paced world of modern finance, the speed and reliability of money transfers are paramount, whether for personal transactions or critical business operations. Among the various methods available, wire transfers stand out for their efficiency and security, making them a preferred choice for sending significant sums of money domestically and internationally. For customers of major financial institutions like Chase, understanding the typical timelines for these transfers is crucial for effective financial planning and execution.

This article delves into the specifics of how long a wire transfer takes when initiated through Chase, exploring the factors that influence these timelines, the distinctions between domestic and international transfers, and best practices for ensuring a smooth and timely transaction. As an essential financial tool, mastering the nuances of wire transfers can empower individuals and businesses to manage their funds with greater confidence and precision.

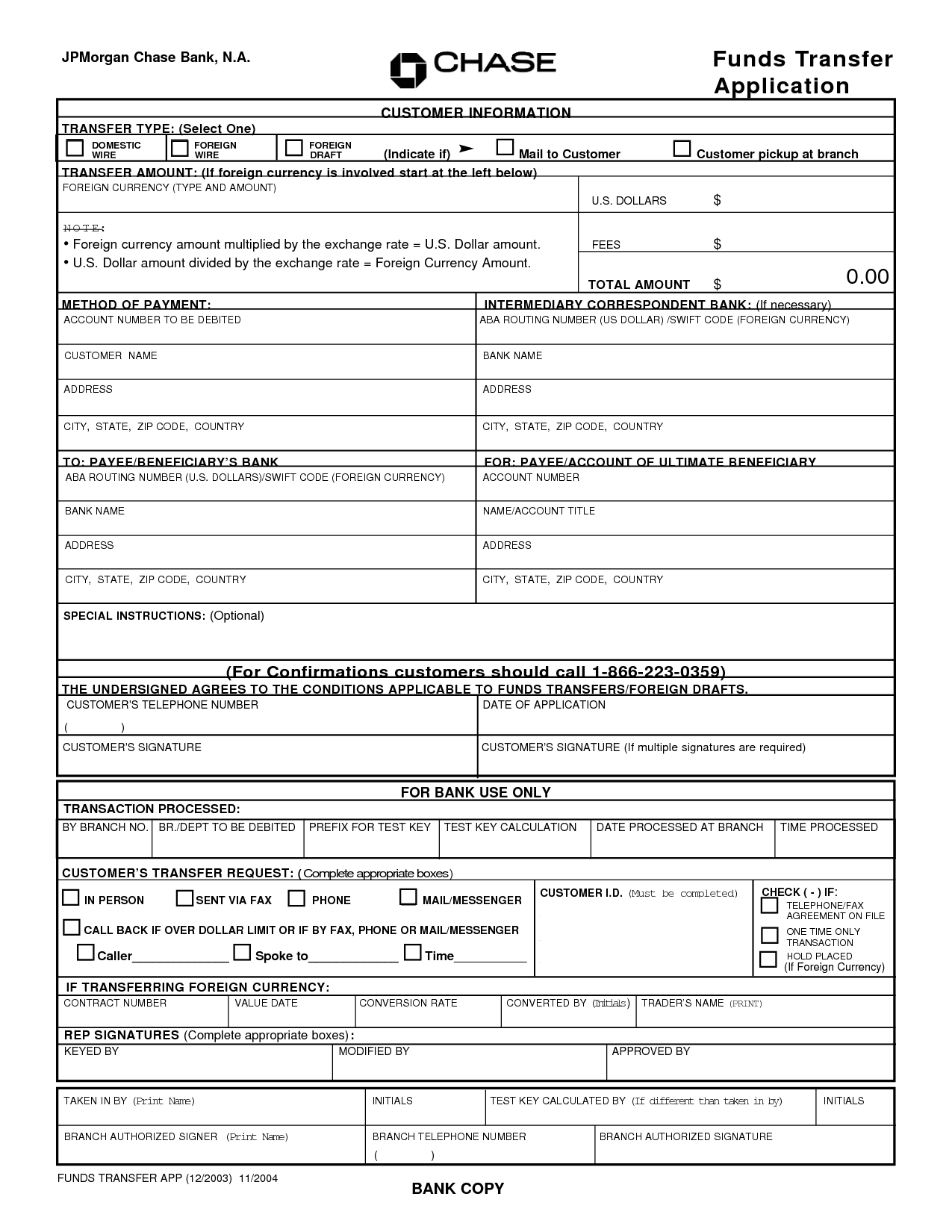

![]()

Demystifying Wire Transfers: An Essential Financial Instrument

Before diving into the specifics of Chase’s timelines, it’s important to grasp the fundamental nature of wire transfers and why they remain a cornerstone of financial transactions. Unlike other payment methods, wire transfers move money directly from one bank account to another, often utilizing specialized electronic networks designed for speed and security.

The Mechanics of a Wire Transfer

At its core, a wire transfer is an electronic funds transfer service that allows individuals and businesses to send money quickly and securely across banks, even those in different countries. When you initiate a wire transfer, your bank (the originating bank) sends a message through a secure network, such as the Fedwire system in the U.S. or the SWIFT network for international transfers, to the recipient’s bank. This message contains instructions for the recipient’s bank to credit a specific amount of money to the designated account. The actual funds are typically settled between the banks through their respective reserve accounts. This direct, bank-to-bank nature is what distinguishes wire transfers from other payment methods like ACH transfers, which operate on a batch-processing system and typically take longer.

Why Choose a Wire Transfer?

Wire transfers are often chosen for specific scenarios due to their unique advantages:

- Speed: They are generally one of the fastest ways to send money between bank accounts, often completing within hours for domestic transfers.

- Security: Due to the direct bank-to-bank communication and stringent verification processes, wire transfers are highly secure. They are less susceptible to fraud once initiated, though sender vigilance is still key to prevent initial scams.

- Irrevocability: Once a wire transfer is sent and processed, it is extremely difficult, if not impossible, to reverse. This characteristic, while requiring careful execution, offers a high degree of certainty for recipients that funds will be received as intended.

- Large Amounts: Wire transfers are ideal for sending substantial sums of money, such as down payments for real estate, business payments, or large personal gifts, where other methods might have lower limits or higher processing times.

Wire Transfers vs. Other Payment Methods

It’s helpful to differentiate wire transfers from other common payment methods:

- ACH Transfers (Automated Clearing House): These are electronic transfers processed in batches, commonly used for payroll, direct deposits, and bill payments. While often free or low-cost, ACH transfers typically take 1-3 business days to clear.

- Credit/Debit Card Payments: Instantaneous for transactions, but primarily for purchases rather than direct bank-to-bank transfers of large sums.

- P2P Payment Apps (e.g., Zelle, Venmo): Designed for quick, smaller personal transfers. While some offer instant transfers, they often have daily/weekly limits and may not be suitable for very large sums or international transfers to traditional bank accounts.

- Checks: A traditional method, but notoriously slow, requiring physical delivery and several days for funds to clear.

Given their blend of speed, security, and suitability for large transactions, wire transfers remain an indispensable tool in both personal and business finance, making their processing times a critical piece of information.

Chase Wire Transfers: Navigating Domestic and International Timelines

When you initiate a wire transfer through Chase, the expected timeline hinges significantly on whether the transfer is domestic or international, as well as the time of day it is initiated. Chase, like other major banks, operates within specific cut-off times that dictate when a transfer will be processed on the same business day versus the next.

Domestic Wires: Expectation vs. Reality

For domestic wire transfers within the United States, Chase typically processes transfers quite rapidly.

- Standard Processing: If a domestic wire transfer is initiated and confirmed before Chase’s daily cut-off time (which is generally 4:00 PM ET for most online and branch-initiated wires), it often reaches the recipient’s bank account on the same business day.

- Post Cut-off: If the transfer is initiated after the cut-off time, or on a weekend or banking holiday, it will usually be processed on the next business day. The funds would then typically arrive at the recipient bank on that next business day.

- Recipient Bank’s Role: While Chase will send the funds quickly, the exact time the money becomes available to the recipient can also depend on the receiving bank’s processing procedures and its own cut-off times. Most banks credit incoming wires almost immediately upon receipt, but some may hold funds for a short period depending on their internal policies or specific account types.

In most ideal scenarios, a domestic wire transfer sent through Chase will be completed within a few hours on the same business day, assuming all information is correct and it’s sent before the daily deadline.

International Wires: The Global Network Effect

International wire transfers are inherently more complex and thus typically take longer than domestic transfers. This is due to several factors, including multiple banking systems involved, different time zones, currency conversions, and rigorous international regulations.

- Standard Processing: For international wire transfers, Chase generally advises customers to expect the funds to arrive within 1 to 5 business days.

- Influencing Factors: The exact timing within this range can vary widely based on:

- The destination country: Transfers to countries with well-established banking systems and strong relationships with U.S. banks may be faster. Remote locations or countries with less developed financial infrastructure could take longer.

- The recipient bank’s efficiency: Just as with domestic transfers, the efficiency of the receiving international bank plays a role.

- Currency conversion: If currency conversion is involved, it can add a small amount of processing time.

- Intermediary banks: International wires often pass through one or more intermediary banks before reaching the final destination. Each intermediary bank adds a step to the process, which can introduce minor delays and potentially additional fees.

Understanding Chase’s Daily Cut-off Times

Chase’s cut-off times are critical for determining when your wire transfer will be processed. These times apply to both domestic and international transfers.

- General Cut-off: For most wire transfers, the typical cut-off time is 4:00 PM Eastern Time (ET) on a business day.

- Variations:

- Online Banking: Wires initiated through Chase Online may have slightly different or stricter cut-off times compared to those initiated in a branch or over the phone. It’s always best to check the specific cut-off displayed within the online platform.

- Branch/Phone: While the general cut-off applies, some branches might have slightly earlier internal cut-offs for processing to ensure they meet the bank’s system deadline.

- Business Accounts: Chase Business customers might have slightly different cut-off times or options for late processing, depending on their account type and service agreements.

To ensure your wire transfer is processed on the same day, it is highly recommended to initiate it well before the published cut-off time, allowing for any potential delays in data entry or verification.

Unpacking the Variables: What Dictates Wire Transfer Speed?

While Chase aims for efficiency, several external and internal factors can influence how quickly a wire transfer reaches its destination. Understanding these variables can help set realistic expectations and avoid unnecessary frustration.

The Role of Intermediary Banks

As mentioned, international wire transfers, and sometimes even complex domestic ones, may not travel directly from your Chase account to the recipient’s bank. Instead, they might pass through one or more “intermediary banks” or “correspondent banks.” These banks facilitate the transfer between institutions that don’t have direct relationships. Each intermediary bank acts as a transit point, adding a step to the process. While typically efficient, each step can introduce a minor delay, especially if the intermediary bank is in a different time zone or has its own processing cut-offs. This is a primary reason why international wires take longer.

Regulatory Compliance and Anti-Money Laundering (AML) Checks

Financial institutions, including Chase, are bound by strict regulatory requirements, such as the Bank Secrecy Act (BSA) and various Anti-Money Laundering (AML) and Counter-Terrorist Financing (CTF) laws. Large transactions, or those involving certain countries or entities, may trigger enhanced scrutiny.

- Verification: Banks must verify the identity of senders and recipients and ensure the legitimacy of the transaction. This process helps prevent fraud, money laundering, and terrorist financing.

- Sanctions Screening: Transfers are screened against international sanctions lists (e.g., OFAC in the U.S.). If a name or entity on the transfer matches an entry on a sanctions list, the transfer will be held for further investigation, which can cause significant delays or even lead to the funds being frozen.

- Documentation: In some cases, Chase or an intermediary bank might request additional documentation or clarification about the purpose of the transfer, especially for unusually large sums or transactions involving high-risk jurisdictions. Responding promptly to such requests is crucial to prevent delays.

The Impact of Banking Hours and Holidays

![]()

Wire transfers are processed during banking business hours. This means:

- Weekends and Holidays: Transfers initiated on weekends or bank holidays will not begin processing until the next business day. This applies to both the originating bank (Chase) and the receiving bank. If the receiving bank is in a different country, their local holidays must also be considered.

- Time Zones: For international transfers, time zone differences are a significant factor. A wire sent at 3:00 PM ET from the U.S. might be received in Europe already after their banking hours, meaning it won’t be processed until their next business day. This effectively adds a day to the transfer time.

Precision in Details: Avoiding Delays

One of the most common reasons for wire transfer delays or outright rejections is incorrect or incomplete information.

- Account Details: Even a single incorrect digit in the recipient’s account number or routing number (for domestic) / SWIFT/BIC code (for international) can cause a transfer to be delayed, returned, or sent to the wrong account.

- Recipient Name: The recipient’s name on the wire transfer must exactly match the name on their bank account. Discrepancies can lead to holds or rejections.

- Bank Information: Accurate name and address of the recipient’s bank are also vital.

- Purpose of Payment (for international wires): Some countries or banks require a clear and specific purpose of payment for international transfers. Lack of this information can cause delays at the receiving end.

Double-checking all details meticulously before confirming a wire transfer is perhaps the most critical step a sender can take to ensure timely delivery.

Executing a Seamless Chase Wire Transfer: A Step-by-Step Guide

Successfully initiating a wire transfer with Chase involves more than just knowing the timelines; it requires careful preparation and adherence to best practices. Whether you’re sending money online, in a branch, or over the phone, understanding the process ensures efficiency.

Gathering Essential Information

Before you begin, have all necessary details for the recipient and their bank readily available. This information is critical for avoiding delays and ensuring the funds reach the correct destination.

For Domestic Wire Transfers:

- Recipient’s Full Name and Address: Must match their bank records.

- Recipient’s Account Number: The exact account number where funds should be deposited.

- Recipient’s Bank Name and Address: The full legal name and physical address of their bank.

- Recipient’s Bank Routing Number (ABA Number): A 9-digit code identifying the bank within the U.S. banking system.

For International Wire Transfers:

- Recipient’s Full Name and Address: As it appears on their bank account.

- Recipient’s Account Number/IBAN: The exact account number. For many international accounts, an International Bank Account Number (IBAN) is required.

- Recipient’s Bank Name and Address: Full legal name and physical address of the bank.

- SWIFT/BIC Code: A Bank Identifier Code (BIC) is an international standard for identifying banks globally. Also known as SWIFT code, it typically has 8 or 11 characters.

- Purpose of Payment: A brief, clear description of why you are sending the money (e.g., “Family Support,” “Invoice Payment,” “Property Purchase”). This is often required for international compliance.

- Intermediary Bank Information (if applicable): Sometimes, the recipient’s bank will provide specific instructions for an intermediary bank to ensure the fastest transfer.

Choosing Your Method: Online, Branch, or Phone

Chase provides multiple channels for initiating wire transfers, each with its own conveniences and potential limitations.

- Chase Online Banking/Mobile App: For many personal and business customers, initiating a wire transfer online is the most convenient option. You can typically set up domestic and international wires directly from your computer or mobile device.

- Pros: Available 24/7 (though processing is during business hours), self-service, ability to save recipient information for future transfers.

- Cons: Often has lower daily limits than in-branch transfers, requires strong cybersecurity practices, and may have a slightly earlier cut-off time.

- In-Branch Visit: Visiting a Chase branch allows you to complete the transfer with the assistance of a bank representative.

- Pros: Ideal for first-time wire transfers, complex international transfers, or very large sums that exceed online limits. A representative can guide you through the process and verify details.

- Cons: Requires physical presence during banking hours, potentially longer wait times.

- Phone Banking: For some Chase customers, especially business clients or those with specific account types, it might be possible to initiate a wire transfer over the phone with a customer service representative.

- Pros: Convenience of doing it from anywhere without needing to visit a branch.

- Cons: May involve security verification steps, potentially longer wait times to connect with a representative.

Always confirm the specific requirements and limits for your chosen method directly with Chase.

Understanding Chase’s Wire Transfer Fees

Wire transfers, while fast and secure, typically incur fees. Chase’s fees can vary based on the type of transfer (domestic vs. international) and whether it’s incoming or outgoing.

- Outgoing Domestic Wire: Typically costs around $25.

- Outgoing International Wire: Generally costs between $40-$50.

- Incoming Domestic Wire: Often free for the recipient, but some banks may charge a small fee. Chase typically does not charge for incoming domestic wires.

- Incoming International Wire: Chase may charge a fee for incoming international wires, often around $15.

- Intermediary Bank Fees: For international transfers, intermediary banks may also deduct their own fees from the transferred amount, meaning the recipient might receive slightly less than the amount sent.

It’s essential to factor these fees into your financial planning. Always confirm the current fee schedule with Chase before initiating a transfer.

Monitoring Your Transaction

After sending a wire transfer, you can often monitor its status, especially if initiated online.

- Confirmation Numbers: Chase will provide a confirmation number or tracking ID for your wire transfer. Keep this number handy.

- Online Tracking: For transfers initiated online, you can usually check the status within your Chase Online account or mobile app.

- Customer Service: If you have concerns about a delayed transfer, you can contact Chase’s customer service with your confirmation number for an update.

While wire transfers are generally reliable, monitoring provides peace of mind and allows for quick action if an issue arises.

Addressing Potential Roadblocks and Ensuring Security

Even with meticulous planning, issues can sometimes arise. Knowing how to troubleshoot and protect yourself is as crucial as understanding the initial process.

When a Wire Transfer Isn’t Instant: What to Do

If your domestic wire transfer hasn’t arrived by the end of the same business day, or your international transfer is taking longer than the 1-5 business days initially advised, here are steps you can take:

- Verify Information: Double-check the confirmation details against the information you provided. A simple typo is often the culprit.

- Contact Recipient: Ask the recipient to check their bank account and contact their bank. Their bank might have received the funds but is holding them for verification or due to an internal processing delay. They should inquire about the status using the sending bank’s name, the amount, and the date sent.

- Contact Chase: If the recipient’s bank has no record, contact Chase customer service with your wire transfer confirmation number. They can trace the wire through the Fedwire or SWIFT network to determine where it might be held up. Be prepared to provide all transaction details.

- Allow Time for International Wires: Remember that international wires have a broader window (up to 5 business days, sometimes more for very complex routes or remote locations). Patience is sometimes necessary before escalating.

Correcting Errors and Recalling Funds

Wire transfers are generally considered irreversible. However, in specific circumstances, it might be possible to correct an error or recall funds.

- Correcting Errors: If you realize you’ve made a minor error (e.g., a wrong digit in the account number) immediately after sending, contact Chase as soon as possible. If the wire has not yet been fully processed and sent from Chase’s system, they might be able to intercept and correct it.

- Recalling Funds: If the funds have already been sent and credited to an incorrect account, recalling them is extremely difficult and often depends on the cooperation of the receiving bank and the account holder. Chase can initiate a recall request, but there’s no guarantee of success. Funds sent to the wrong recipient due to sender error are often unrecoverable. This underscores the absolute necessity of verifying all details before confirming the transfer.

Protecting Yourself from Wire Transfer Fraud

The irrevocability of wire transfers makes them a prime target for fraudsters. Protect yourself by adhering to these security guidelines:

- Verify Recipient Independently: Always verify the recipient’s bank details and identity through a separate, trusted communication channel (e.g., a phone call to a known number, not an email address that sent you the wire instructions). Never rely solely on email instructions, as email accounts can be compromised.

- Beware of Urgency and Pressure: Fraudsters often create a sense of urgency, pressuring you to send money immediately without time for verification.

- Too Good to Be True: Be highly suspicious of unsolicited requests for money, offers that seem too good to be true (e.g., lottery winnings, inheritance, online romance scams), or requests to send money to someone you’ve only met online and never in person.

- Understand the “Why”: Always understand the legitimate purpose of the transfer. If you’re unsure, or if the reason seems dubious, do not send the money.

- Never Wire to Unfamiliar Parties: Avoid wiring money to individuals or businesses you don’t know or haven’t thoroughly vetted, especially for online purchases from unknown sellers.

- Educate Yourself: Stay informed about common wire fraud schemes by checking resources from the FTC, FBI, and your bank.

By understanding the mechanics, timelines, influencing factors, and crucial security measures associated with wire transfers, Chase customers can navigate these essential financial transactions with confidence, ensuring their money reaches its intended destination securely and efficiently. Always remember that due diligence on the sender’s part is the strongest defense against delays and fraud.