Navigating the world of personal and business finance often leads to a common need: a loan. Whether you’re looking to consolidate debt, finance a major purchase, buy a home, or expand a business, securing capital can be a critical step. Chase Bank, as one of the largest financial institutions in the United States, is a prominent player in the lending landscape, offering a wide array of loan products to meet diverse financial needs. Understanding how to approach Chase for a loan, what they offer, and what they look for in an applicant is essential for a smooth and successful application process.

This guide will demystify getting a loan from Chase Bank, outlining their various offerings, the key factors that influence their lending decisions, and a step-by-step approach to navigate the application process. With the right preparation and understanding, you can significantly enhance your chances of securing the financing you need.

Understanding Chase Bank’s Loan Offerings

Chase Bank provides a comprehensive suite of loan products tailored for individuals and businesses. Each loan type serves a specific purpose and comes with its own set of terms, eligibility criteria, and application nuances. Identifying the right loan for your particular need is the first crucial step.

Personal Loans: Eligibility and Use Cases

Chase Bank does not explicitly offer traditional, unsecured personal loans in the same way some other lenders do. Instead, they primarily focus on secured lending or specific financing options that often leverage existing relationships or assets. For individuals seeking flexible financing without collateral, Chase often directs customers towards products like credit cards with competitive APRs or lines of credit if they have sufficient equity (e.g., a HELOC).

However, it’s important to clarify what “personal loan” might mean in broader terms, as it often refers to an unsecured installment loan used for various personal expenses. If you’re looking for flexible funds, Chase’s secured options or lines of credit are generally their primary offerings.

- What are they? Unsecured personal loans are typically installment loans with fixed interest rates and repayment schedules, used for a variety of purposes without requiring collateral. Chase’s alternatives might include leveraging home equity or utilizing credit card options.

- Typical eligibility requirements: Generally, lenders look for a strong credit score (typically 670+ for prime rates), a stable income, and a manageable debt-to-income (DTI) ratio.

- Common uses: Debt consolidation, home improvements (though a HELOC might be more appropriate from Chase), medical emergencies, or funding major purchases.

Home Loans: Mortgages and HELOCs

Chase is a major player in the mortgage market, offering a robust selection of home financing options for buyers and existing homeowners.

- Mortgages: Whether you’re a first-time homebuyer or looking to refinance, Chase provides various mortgage types, including:

- Fixed-Rate Mortgages: Offer predictable monthly payments over the life of the loan (e.g., 15-year, 30-year).

- Adjustable-Rate Mortgages (ARMs): Feature an initial fixed-rate period, after which the rate can fluctuate based on market indices.

- Jumbo Loans: For loan amounts exceeding conforming loan limits, suitable for high-value properties.

- Government-Backed Loans: While Chase may not directly originate all government-backed loans (like FHA or VA), they can guide you through options or work with partners.

- Home Equity Line of Credit (HELOCs): A HELOC allows you to borrow against the equity you’ve built in your home. It functions like a credit card, providing a revolving line of credit that you can draw from as needed, up to a certain limit. Interest is only paid on the amount borrowed.

- Specific requirements for home loans: These typically include a down payment (which can vary significantly), a good credit score, proof of stable income, a low DTI, and a property appraisal.

Auto Loans: Financing Your Vehicle

If you’re in the market for a new or used car, Chase offers competitive auto loan solutions.

- New vs. Used car loans: Chase provides financing for both new and used vehicles, often with different interest rates and loan terms.

- Application process specifics for auto loans: You can apply directly through Chase, or often through a dealership that partners with Chase. The vehicle itself serves as collateral for the loan.

- Considerations: Factors like the vehicle’s age, mileage, your down payment, and any trade-in value will influence the loan amount and terms.

Small Business Loans: Fueling Entrepreneurship

Chase understands the unique financial needs of businesses, from startups to established enterprises.

- Types:

- Term Loans: A lump sum of capital repaid over a fixed period with regular installments.

- Business Lines of Credit: Flexible, revolving credit that businesses can draw upon as needed, ideal for managing cash flow or short-term operational expenses.

- SBA Loans (Small Business Administration): Chase is a leading lender for SBA-guaranteed loans (e.g., SBA 7(a) loans), which are excellent for businesses that might not qualify for traditional loans due to risk factors, but require favorable terms and government backing.

- Commercial Real Estate Loans: For purchasing or refinancing commercial properties.

- Business-specific requirements: Beyond personal credit, Chase will scrutinize your business plan, financial statements (profit and loss, balance sheets), cash flow projections, time in business, and industry experience. Often, a personal guarantee from the business owner is required.

Key Factors Chase Bank Considers for Loan Approval

Regardless of the type of loan you seek, Chase, like any prudent lender, evaluates several critical factors to assess your creditworthiness and ability to repay. Understanding these elements can help you prepare a stronger application.

Your Credit Score and Credit History

This is often the first and most impactful criterion. Your credit score, particularly your FICO score, is a numerical representation of your credit risk.

- Importance of FICO score: A higher score indicates a lower risk to lenders, often leading to better interest rates and more favorable terms. Scores generally range from 300-850, with anything above 700 considered good to excellent.

- Factors affecting credit score:

- Payment History (35%): Timely payments are crucial. Missed or late payments significantly hurt your score.

- Amounts Owed (30%): How much debt you carry relative to your credit limits (credit utilization) is key. Keeping utilization below 30% is advisable.

- Length of Credit History (15%): Longer credit histories generally demonstrate more experience managing credit.

- New Credit (10%): Opening too many new accounts in a short period can negatively impact your score.

- Credit Mix (10%): Having a healthy mix of different credit types (e.g., credit cards, installment loans) can be beneficial.

- Tips for improving credit before applying: Review your credit report for errors, pay down high-interest debt, make all payments on time, and avoid opening new credit accounts just before applying for a major loan.

Income and Employment Stability

Lenders need assurance that you have a steady and sufficient income to cover your loan payments.

- Demonstrating ability to repay: Chase will ask for proof of income to verify your financial capacity.

- W-2s, pay stubs, tax returns: These are standard documents for salaried employees.

- Self-employment considerations: If you’re self-employed or own a business, you’ll typically need to provide several years of tax returns, profit and loss statements, and bank statements to demonstrate consistent income.

Debt-to-Income (DTI) Ratio

Your DTI ratio is a crucial metric that helps Chase determine how much of your monthly gross income goes towards paying debts.

- What it is and why it matters: Calculated by dividing your total monthly debt payments by your gross monthly income, DTI indicates your ability to take on additional debt. A high DTI suggests you might be overextended.

- Ideal DTI for lenders: Most lenders prefer a DTI ratio of 36% or lower, though some might go up to 43% for certain loan types, especially mortgages.

- How to calculate and improve DTI: Add up all your monthly debt payments (credit card minimums, car loans, student loans, existing mortgage/rent) and divide by your gross monthly income. To improve it, focus on paying down existing debts or increasing your income.

Collateral (for Secured Loans)

For secured loans, an asset is pledged to the lender to guarantee the loan.

- When it’s required: Mortgages use your home as collateral, auto loans use the vehicle, and some business loans might require real estate, equipment, or inventory as collateral. HELOCs are also secured by your home equity.

- How it reduces lender risk: If you default on the loan, Chase can seize the collateral to recover their losses, making secured loans less risky for the bank and often resulting in lower interest rates for the borrower.

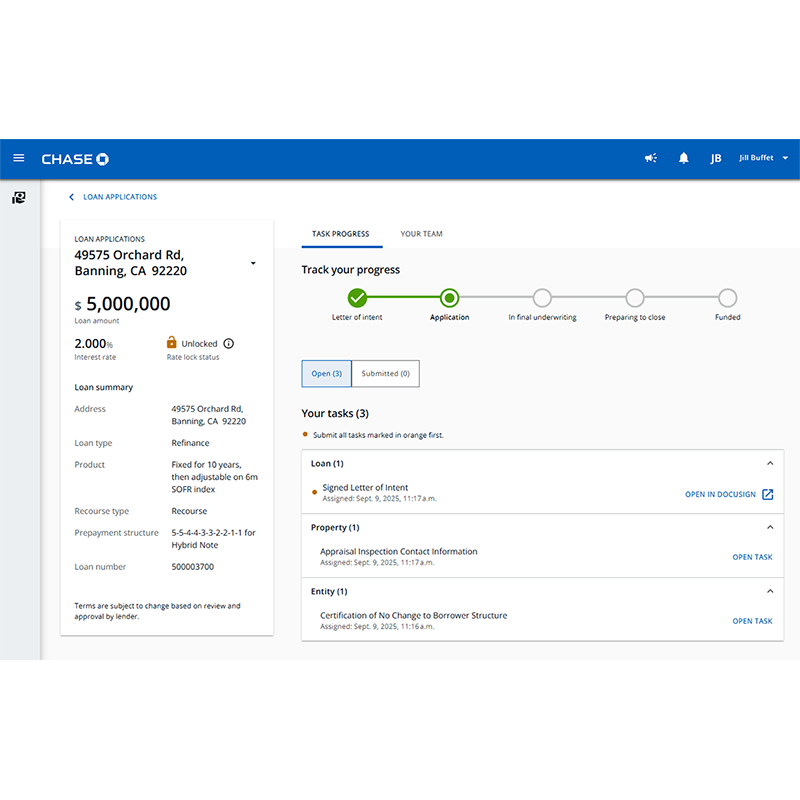

Navigating the Chase Bank Loan Application Process

Once you’ve identified the right loan product and assessed your financial readiness, the next step is to engage with Chase Bank through their application process.

Pre-Qualification vs. Full Application

Understanding the difference can save you time and protect your credit score.

- Benefits of pre-qualification: Many lenders, including Chase for certain products, offer pre-qualification. This involves a “soft” credit inquiry that doesn’t affect your credit score and provides an estimate of what you might qualify for, without committing you to a full application. It’s a good way to gauge your eligibility.

- What a full application entails: A full application requires a more comprehensive review of your finances, including a “hard” credit inquiry (which can temporarily lower your score by a few points), and a detailed submission of all required documentation.

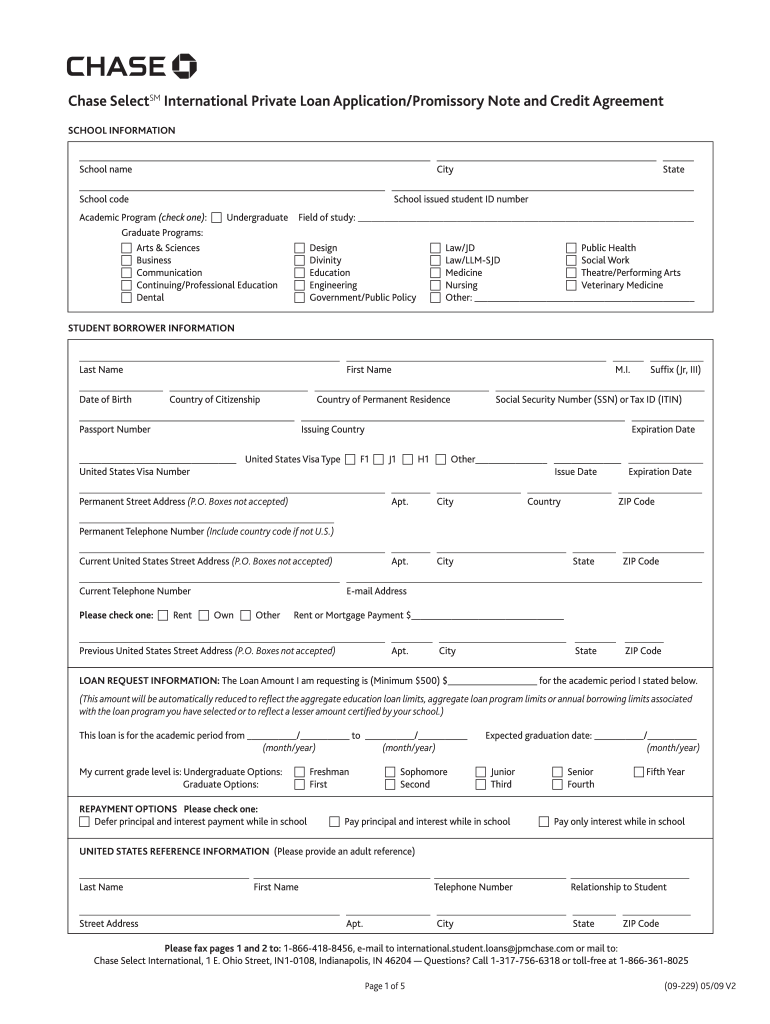

Required Documentation

Gathering your documents in advance can significantly expedite the process.

- Identification: Government-issued ID (driver’s license, passport) and Social Security Number.

- Proof of income: Recent pay stubs (1-2 months), W-2 forms (last two years), and federal tax returns (last two years). For self-employed individuals, business tax returns, profit and loss statements, and bank statements.

- Bank statements, asset information: Statements from your checking, savings, and investment accounts to verify liquid assets.

- Business financials (if applicable): For business loans, be prepared to submit a detailed business plan, balance sheets, cash flow statements, and possibly accounts receivable/payable aging reports.

Online, In-Branch, or Phone Application

Chase offers multiple channels for loan applications, allowing you to choose the most convenient method.

- Online: Many loan applications can be started or completed entirely online through Chase’s secure website or mobile app. This offers convenience and speed.

- In-Branch: Visiting a Chase branch allows you to speak directly with a loan officer, ask questions, and receive personalized guidance. This can be beneficial for complex loans or if you prefer face-to-face interaction.

- Phone: You can also typically apply or discuss options over the phone with a Chase representative.

- Chase’s digital tools: For pre-qualification and tracking your application status, Chase’s online platforms are generally robust and user-friendly.

What Happens After You Apply?

The period after submitting your application involves several steps:

- Underwriting process: Chase’s underwriters will thoroughly review all your submitted documents, verify information, and assess the risk associated with lending to you. This can involve requesting additional information.

- Approval, denial, or request for more information: You will receive a decision. If approved, you’ll get the loan terms. If denied, Chase is required to provide reasons for the denial. Sometimes, more information is requested to make a final decision.

- Loan closing and funding: If approved, you’ll review and sign the final loan documents (closing). Once signed, the funds will be disbursed to you or directly to the seller/creditor, depending on the loan type.

Tips for a Successful Loan Application at Chase

Securing a loan requires more than just meeting the minimum requirements; strategic preparation and proactive engagement can make a significant difference.

Prepare Your Finances in Advance

Proactive steps taken months before applying can greatly improve your standing.

- Review credit report: Obtain free copies of your credit report from AnnualCreditReport.com and dispute any errors.

- Build savings: Having a healthy savings account demonstrates financial responsibility and provides a buffer.

- Reduce debt: Pay down existing high-interest debt to lower your DTI ratio and improve your credit utilization.

Understand Loan Terms and Conditions

Don’t just look at the interest rate. Read the fine print carefully before committing.

- Interest rates: Understand whether it’s fixed or variable, and what the Annual Percentage Rate (APR) truly is.

- Fees: Be aware of any origination fees, application fees, prepayment penalties, or late payment charges.

- Repayment schedule: Know your monthly payment amount, the total number of payments, and the loan term.

Don’t Be Afraid to Ask Questions

Chase has dedicated loan specialists for various products. Utilize their expertise.

- Clarify anything you don’t understand about the loan product, the application process, or the terms.

- Inquire about ways to improve your application or explore alternative options.

Consider All Your Options

While Chase offers a broad range of products, it’s wise to compare.

- Compare rates: Don’t hesitate to get quotes from other lenders to ensure you’re getting the best possible terms.

- Explore different loan types: Sometimes, a different loan structure (e.g., a HELOC instead of an unsecured personal loan for home improvements) might be more suitable.

- Think about co-signers if necessary: If your credit profile isn’t strong enough, a creditworthy co-signer might help you qualify or secure better terms, but understand the implications for the co-signer.

Conclusion

Getting a loan from Chase Bank is a structured process that rewards preparation, financial prudence, and clear communication. By understanding the specific loan products available, recognizing the key factors Chase considers for approval (credit score, income, DTI, and collateral), and meticulously navigating the application process, you can significantly increase your likelihood of success.

Whether you’re aiming to purchase your dream home, secure a new vehicle, or inject vital capital into your business, Chase Bank offers robust financial solutions. Approaching the process with knowledge and diligence will empower you to make informed decisions and secure the financing that best fits your financial journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.