Closing a bank account might seem like a straightforward task, but in the intricate world of personal finance, it often involves a methodical process to avoid unexpected fees, credit score impacts, or logistical headaches. Whether you’re consolidating your finances, moving to a new bank, or simply no longer satisfied with your current services, understanding the proper steps to close your Citi account is crucial. This guide provides a professional, insightful, and engaging roadmap to navigate the process, ensuring a smooth transition and protecting your financial well-being. By meticulously preparing and executing each step, you can close your Citi checking, savings, or credit card account with confidence and clarity, sidestepping common pitfalls and securing your financial future.

Preparing for Account Closure: Essential Pre-closure Steps

Before initiating the formal closure of any Citi account, thorough preparation is paramount. Hasty decisions can lead to complications, such as missed payments, overdrafts, or adverse effects on your credit history. Taking the time to organize your financial affairs ensures a clean break and protects your financial standing. This preparatory phase is where most potential issues can be identified and proactively addressed, laying the groundwork for a hassle-free closure.

Reviewing Your Account Activity and Balances

The first critical step involves a detailed review of all activities associated with your Citi account. Access your online banking portal or recent statements to identify all pending transactions, such as outstanding checks, direct debits, or recurring payments scheduled to clear. Ensure that all checks you’ve written have been cashed by the recipients and that no recurring payments are outstanding. For credit card accounts, ascertain your current balance and any interest accrued. For checking and savings accounts, confirm your available balance and any minimum balance requirements that might trigger fees if not maintained until closure. It’s also wise to download or print several months’ worth of statements for your records, as access might be restricted post-closure. This meticulous review helps prevent any surprises or fees that could arise from uncleared items after you’ve initiated the closure process.

Updating Direct Deposits and Automatic Payments

One of the most crucial elements of account closure is rerouting your financial flows. Any direct deposits, such as your salary, social security benefits, or tax refunds, must be redirected to your new bank account before closing your Citi account. Similarly, all automatic payments and recurring bill pay setups linked to your Citi account need to be updated. This includes utilities, mortgage or rent payments, loan repayments, insurance premiums, streaming subscriptions, and any other automated deductions. Failing to update these can result in missed payments, late fees, service interruptions, and potential damage to your credit score. Make a comprehensive list of all such transactions, contact each service provider, and provide them with your new account details well in advance. Consider running both accounts concurrently for a short period to ensure all new arrangements are fully operational before finalizing the closure of your Citi account.

Transferring Funds and Settling Debts

Once all direct deposits and automatic payments have been rerouted, you’ll need to transfer any remaining funds from your Citi checking or savings account to your new bank. Several methods are available for this, including an electronic ACH transfer, a wire transfer (though often associated with fees), or requesting a cashier’s check or bank draft for the full balance. For Citi credit card accounts, it is imperative to pay off the entire outstanding balance, including any pending interest, before requesting closure. Carrying a balance on a card you intend to close can complicate the process and potentially incur additional charges. If you have any linked investment accounts through Citi, consider whether you wish to transfer these assets to another brokerage or liquidate them, understanding any potential tax implications or transfer fees involved. Thoroughly settling all debts and ensuring a zero balance on accounts designated for closure is a non-negotiable step to a clean financial break.

The Official Closure Process: Navigating Citi’s Procedures

With your accounts prepared and all financial flows redirected, you are ready to formally initiate the closure process with Citi. The exact steps can vary slightly depending on the type of account you hold, but generally involve direct communication with the bank through specific channels. Understanding these procedures is key to ensuring your request is processed efficiently and accurately, preventing any lingering ties or unexpected re-openings.

Identifying Account Types and Specific Requirements

Citi offers a diverse range of financial products, and each may have slightly different closure protocols. For standard checking and savings accounts, the primary requirement is often a zero balance and confirmation that all direct debits and credits have been successfully rerouted. Citi credit card accounts, once the balance is paid in full, can typically be closed by a phone request. However, be prepared for agents to try and retain your business with offers, which is a standard practice. Investment accounts linked to Citi, such as those through Citigroup Global Markets Inc., usually require either the transfer of assets to another brokerage or their liquidation, which might involve specific forms and regulatory considerations. Loan accounts, including personal loans or mortgages through Citi, cannot typically be “closed” in the same manner as a deposit account; they must be paid off entirely, at which point the account obligation is fulfilled and ceases to exist. Knowing the specifics for each of your Citi products will streamline your interaction with their customer service.

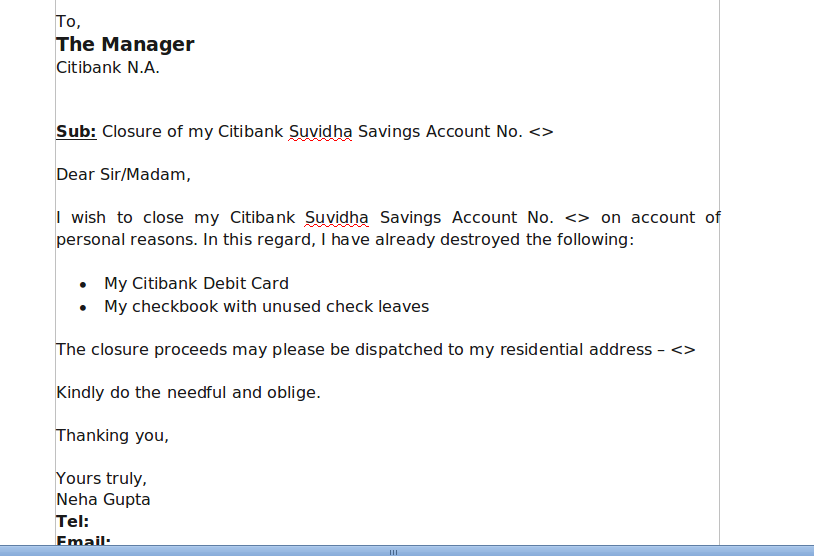

Contacting Citi: Channels and Documentation

Citi provides several channels through which you can request account closure, each suited to different preferences and complexities. The most common and often quickest method for checking and savings accounts is a direct phone call to Citi’s customer service. Be prepared to provide your account number, personal identification details (like your Social Security Number and date of birth), and possibly answer security questions. For credit cards, a phone call is also the standard. Some individuals prefer visiting a Citi branch in person, especially for complex situations, joint accounts, or if they desire a physical receipt or immediate confirmation. This also allows for any remaining cash to be withdrawn directly. While less common for everyday accounts, a formal written request mailed to Citi’s corporate address might be necessary for certain specialized accounts or if you require a documented paper trail of your closure request. Always inquire about any specific forms or documentation Citi might require to process your request, such as a signed letter for joint account closures.

Confirming Closure and Record Keeping

After submitting your request to close your Citi account, the process isn’t complete until you receive official confirmation from the bank. This confirmation is vital proof that the account has been successfully terminated and you no longer hold any obligations or ties to it. Typically, Citi will send a written confirmation letter via mail or an email notification, stating the effective date of closure and confirming a zero balance. It is imperative to wait for this official notice before considering the account fully closed. If you don’t receive confirmation within a reasonable timeframe (usually 10-15 business days), follow up with Citi customer service. Once received, store this confirmation alongside your other financial records for several years. This documentation serves as an important safeguard in case any disputes or discrepancies arise in the future, providing concrete evidence of your successful account closure and protecting you from potential issues.

Potential Pitfalls and Considerations When Closing Accounts

While closing a bank account is a necessary financial maneuver for many, it’s essential to be aware of potential complications that can arise. Ignoring these considerations could lead to unexpected financial setbacks, ranging from damaged credit scores to unforeseen fees. A proactive approach to understanding these pitfalls ensures that your account closure truly represents a clean and beneficial financial transition.

Impact on Credit Score (Especially for Credit Cards)

Closing a credit card, particularly an older one, can have a nuanced and sometimes negative impact on your credit score. Your credit score is influenced by several factors, including your credit utilization ratio (the amount of credit you’re using versus the total available credit) and the length of your credit history. Closing an account reduces your total available credit, which can increase your utilization ratio if your balances on other cards remain the same, potentially lowering your score. Furthermore, older accounts contribute positively to the average age of your credit history. Closing your oldest credit card can shorten this average, which might also negatively affect your score. Before closing a credit card, especially one with a long history and no annual fee, carefully weigh the potential impact on your credit score against your reasons for closure. It’s generally advisable to keep older, unused credit cards open if they don’t incur fees, to maintain a strong credit profile.

Fees and Penalties

Although less common with long-standing accounts, some Citi accounts may have specific fees or penalties associated with early closure. For example, some checking or savings accounts might levy a fee if closed within a certain period (e.g., 90 or 180 days) of opening. Additionally, if your account falls below a required minimum balance before you successfully transfer all funds and close it, you might incur minimum balance fees. It’s crucial to clarify any potential closure-related fees directly with Citi customer service before proceeding. Furthermore, ensure all automatic transactions have ceased to prevent overdrafts or other fees from unforeseen deductions attempting to clear after the account’s intended closure. Thoroughly reviewing your account terms and conditions or speaking with a representative can help you preempt these charges.

Managing Joint Accounts and Authorized Users

The closure of joint accounts and accounts with authorized users introduces an additional layer of complexity. For joint checking or savings accounts, Citi typically requires the consent of all account holders to initiate closure. This often means all parties must be present in a branch or provide written, notarized consent. Ensure all joint account holders are in agreement and understand the implications before proceeding. For credit cards, closing the primary account will also result in the cancellation of all authorized user cards linked to it. While authorized users don’t directly own the account, its closure can still impact their credit history if it was one of their older or higher credit limit accounts. Open communication with all individuals affected by the closure of a shared or linked account is vital to avoid misunderstandings and ensure a smooth process for everyone involved.

Post-Closure Best Practices: Ensuring a Clean Break

The final step in closing your Citi account isn’t merely receiving confirmation; it involves proactive measures to ensure the closure is complete, accurate, and doesn’t leave any lingering digital or physical traces. These post-closure best practices are crucial for maintaining financial integrity and peace of mind, reinforcing a clean break from your former banking relationship.

Monitoring Your Credit Report

Following the closure of any account, particularly credit cards, it is highly advisable to monitor your credit report. Access your free annual credit reports from the three major bureaus (Equifax, Experian, and TransUnion) approximately one to two months after receiving your closure confirmation from Citi. Verify that the closed account is accurately reported as “closed by grantor” or “closed by consumer” with a zero balance. Also, check for any unexpected activity or errors that might indicate an issue with the closure process or even identity theft. Timely identification and dispute of any inaccuracies are crucial for maintaining a healthy credit score and ensuring your financial records are pristine. This vigilance provides an essential layer of security and confirms that Citi has correctly updated your financial standing with the credit bureaus.

Securely Disposing of Old Cards and Checks

Once your Citi account is officially closed and you have received confirmation, it’s time to securely dispose of all physical artifacts associated with that account. This includes cutting up your debit or credit cards into multiple pieces, ensuring the chip and magnetic strip are completely destroyed, and shredding any unused checks. Simply tossing these items into the trash can expose you to identity theft risks, as fraudsters can piece together information to access your financial details. Similarly, shred any old statements or documents related to the closed account that you no longer need for tax purposes or record-keeping, taking care to protect any personally identifiable information. Secure disposal is a critical, often overlooked, step in protecting your identity and ensuring a complete and clean separation from your closed account.

Updating Financial Aggregators and Apps

In today’s digital age, many individuals use financial aggregation tools and budgeting apps (such as Mint, YNAB, Personal Capital, or other banking apps) to manage their money across multiple institutions. After closing your Citi account, remember to remove or delink it from all such platforms. Failing to do so can lead to error messages, irrelevant data populating your financial dashboards, or potentially even security vulnerabilities if the app continues to attempt to connect to a non-existent account. Access the settings within each financial app you use and actively remove the closed Citi account. This not only cleans up your digital financial landscape but also ensures that your budgeting and financial tracking remain accurate and current, reflecting your updated financial structure.

Closing a Citi account, while seemingly a minor financial administrative task, requires a structured and deliberate approach. From meticulous preparation and diligent execution of the closure process to vigilant post-closure monitoring, each step plays a vital role in ensuring a seamless transition. By following this comprehensive guide, you can confidently navigate the complexities, avoid common pitfalls, and safeguard your financial health. Embracing patience and thoroughness throughout this process will lead to a clean break, offering greater financial clarity and setting you up for future success in managing your money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.