In an increasingly digital world, the way we manage and transfer money has evolved dramatically. Gone are the days when a cash-only approach or physical checks dominated person-to-person payments. Today, financial tools like Venmo have revolutionized personal finance, offering an unparalleled level of convenience and speed for sending and receiving money. Whether you’re splitting a dinner bill, contributing to a group gift, or paying a friend back for tickets, Venmo has become an indispensable part of everyday financial interactions. This guide delves into the specifics of how to effectively use Venmo to pay someone, ensuring your financial transactions are not only smooth but also secure and well-managed within your broader personal finance strategy. Understanding its functionality, security features, and financial implications is key to leveraging this powerful tool for efficient money management.

Understanding Venmo’s Financial Ecosystem

Venmo is more than just a payment app; it’s a vital component in the modern personal finance landscape, streamlining how individuals handle everyday monetary exchanges. To truly master paying someone on Venmo, it’s essential to first grasp its foundational role as a financial tool and how it integrates with your existing monetary infrastructure.

Venmo’s Role in Personal Finance Management

At its core, Venmo simplifies numerous aspects of personal finance that were once cumbersome. It transforms the act of splitting expenses with friends, family, or even roommates from an awkward calculation into a seamless digital transaction. Think about shared groceries, utility bills, a group vacation, or simply spotting a friend for lunch – Venmo eliminates the need for exact change, IOUs, or bank transfers that can take days to clear. It acts as an immediate financial intermediary, ensuring that funds can be exchanged almost instantly, fostering greater financial flexibility and reducing friction in social and domestic financial arrangements. For many, it has become the de facto method for managing informal financial agreements, making it a critical financial tool for everyday life.

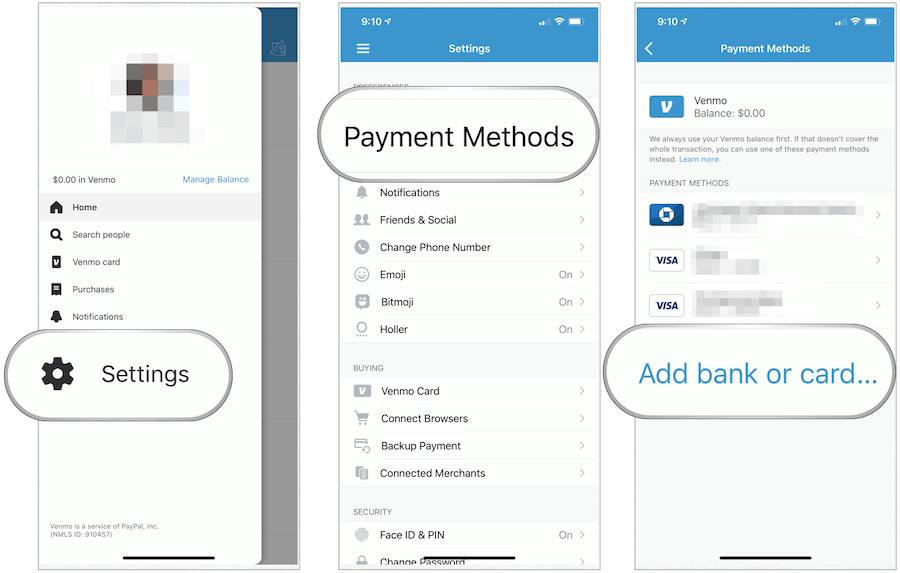

Linking Your Funds: Banks, Debit, and Credit

The operational backbone of Venmo’s financial utility lies in its ability to connect directly with your traditional financial accounts. To send money, you must link a funding source: typically a bank account, a debit card, or a credit card. Linking a bank account allows for direct transfers both into and out of Venmo, usually without a fee for standard transfers. Debit cards also offer a fee-free option for sending money, drawing directly from your bank balance. However, using a credit card to send money to another Venmo user incurs a 3% transaction fee, a crucial financial consideration for users looking to avoid unnecessary costs. Understanding these distinctions is vital for making financially savvy decisions about how you fund your Venmo payments, ensuring you choose the most cost-effective method for each transaction.

Security Measures for Financial Transactions

The ease of digital payments naturally raises questions about financial security. Venmo employs robust security measures to protect users’ monetary transactions and personal financial information. This includes data encryption to safeguard your sensitive details, fraud detection algorithms that monitor unusual activity, and multi-factor authentication options like PINs or biometric logins (fingerprint/face ID). However, ultimate financial security also rests with the user. Best practices include using strong, unique passwords, enabling multi-factor authentication, being cautious of unsolicited payment requests, and regularly reviewing your transaction history. Recognizing that you are dealing with real money, it’s imperative to treat your Venmo account with the same diligence you would your traditional bank account, adhering to security guidelines to prevent potential financial loss.

The Step-by-Step Financial Transaction: Sending Money

Sending money on Venmo is designed to be intuitive, yet understanding each step ensures accuracy and financial safety. This section breaks down the process, guiding you through initiating, detailing, and completing a payment with precision.

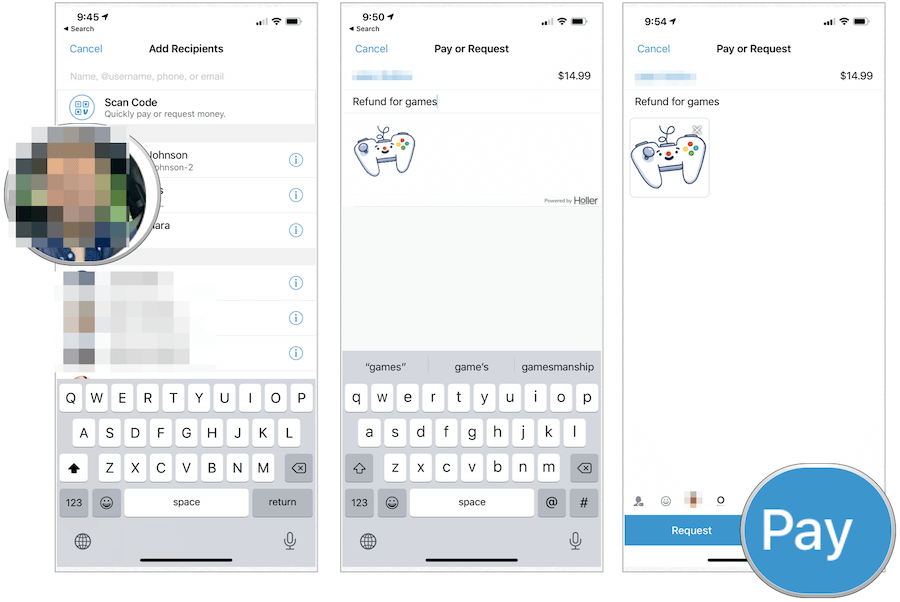

Initiating a Payment: Finding Your Recipient

The first crucial step in making a financial transaction on Venmo is accurately identifying your recipient. Venmo offers several methods to do this, all designed to ensure your money goes to the correct individual. You can search for a user by their unique Venmo username, which often starts with an “@” symbol. Alternatively, you can use their phone number or email address, provided these are linked to their Venmo account. For in-person payments, particularly useful when splitting bills at a restaurant, you can also scan a recipient’s QR code directly from their Venmo profile. Double-checking the recipient’s profile picture and username before proceeding is a vital financial safeguard, preventing funds from being accidentally sent to the wrong person, a mistake that can be challenging to rectify.

Entering the Financial Details: Amount and Purpose

Once you’ve selected your recipient, the next step involves specifying the financial details of the transaction. You’ll enter the exact amount of money you wish to send. Accuracy here is paramount, as Venmo transactions are generally immediate and irreversible once confirmed. Below the amount, you’ll find a field to add a note or description for your payment. While often treated casually, this field serves an important financial purpose. It acts as a digital memo, clarifying the reason for the payment (e.g., “Dinner,” “Rent,” “Concert Tickets”). For personal financial tracking or in cases of dispute, a clear and concise note provides valuable context and a record of the transaction’s purpose, aiding in personal financial accountability.

Selecting Your Funding Source

With the recipient and amount confirmed, you then select how you wish to fund the payment. Your options typically include your Venmo balance (if you have funds available), a linked bank account, a linked debit card, or a linked credit card. As highlighted earlier, this choice carries financial implications: payments funded by a linked bank account or debit card are usually free. However, if you opt to use a credit card, Venmo applies a 3% fee to the sender, which will be clearly displayed before you confirm the transaction. This choice can significantly impact the total cost of your financial transaction, so it’s wise to always consider the most financially advantageous funding method for your specific needs.

Confirming and Completing the Payment

The final stage of the financial transaction involves a comprehensive review and confirmation. Before you tap the “Pay” button, Venmo presents a summary of the transaction: the recipient, the amount, the funding source, and any applicable fees. This is your last opportunity to verify all details are correct. Pay close attention to the recipient’s name and the numerical amount. Once you tap “Pay,” the funds are typically transferred instantly. This immediacy is a key benefit of Venmo but also underscores the importance of pre-payment verification. After confirming, you’ll receive a digital receipt, and the transaction will appear in your Venmo feed (depending on your privacy settings) and in your personal transaction history, providing a record for your financial reconciliation.

Beyond Basic Payments: Advanced Financial Utility

Venmo’s utility extends beyond simple person-to-person payments, offering features that further streamline complex financial interactions and broaden its scope as a versatile financial tool.

Requesting Money and Splitting Bills

Just as easily as you can send money, Venmo allows you to request it, a feature incredibly beneficial for managing shared expenses and informal financial debts. If you’ve covered the cost for a group outing or paid for a shared subscription, you can send a payment request to individual friends for their portion. The “Split a Bill” function takes this a step further, allowing you to enter a total amount and divide it evenly (or unevenly) among multiple contacts, then send individual requests. This drastically simplifies the often-tedious process of collecting money from multiple parties, making Venmo an invaluable aid for budgeting and maintaining fairness in group financial situations. It centralizes the collection process, ensuring timely reimbursement and clarity on who owes what.

Business Payments and QR Codes

While predominantly known for P2P transactions, Venmo has expanded its financial utility to include payments to approved businesses. Many small businesses, merchants, and service providers now accept Venmo as a payment method, especially through QR codes. This allows users to pay for goods and services directly from their Venmo balance or linked funding source, often with fewer fees than traditional credit card processing for the merchant, and a convenient option for the consumer. When encountering a Venmo QR code at a vendor, simply scan it with your app, enter the amount, and complete the transaction. This integration broadens Venmo’s reach, positioning it not just as a tool for personal finance but also for everyday commercial exchanges, blending seamlessly into the local economy.

Managing Your Venmo Balance and Transfers

After receiving money, funds reside in your Venmo balance. You have two primary options for managing this balance: you can keep the money in your Venmo account for future payments or transfer it out to your linked bank account. Standard transfers to a bank account are typically free but can take 1-3 business days to process. For those who need immediate access to their funds, Venmo offers an “Instant Transfer” option, which moves money to your linked debit card or bank account, usually within minutes, for a small fee (typically 1.75% of the transferred amount, with a minimum of $0.25 and a maximum of $25.00). Understanding these options and their associated financial costs is crucial for effective liquidity management, allowing you to choose between convenience and cost-efficiency based on your immediate financial needs.

Maximizing Venmo for Prudent Personal Finance

Leveraging Venmo effectively goes beyond simply knowing how to send money; it involves integrating it wisely into your overall personal finance strategy. Prudent use ensures both convenience and financial security.

Best Practices for Secure Transactions

Financial security on Venmo is a shared responsibility. While Venmo implements robust safeguards, user vigilance is paramount. Always confirm the recipient’s identity and verify the amount before hitting “Pay.” Be wary of unsolicited payment requests or messages from unknown individuals, as these could be phishing attempts or scams designed to compromise your financial data. Link only trusted bank accounts and cards. Regularly review your transaction history for any unauthorized activity and enable all available security features, such as multi-factor authentication and PIN protection. Treating Venmo with the same caution as your primary bank account is essential to protect your money from fraud and ensure your personal finance remains secure.

Tracking Your Financial Activity

Venmo maintains a comprehensive history of all your transactions, which is a powerful tool for personal financial tracking. By regularly reviewing your activity feed, you can monitor your spending, confirm payments, and track reimbursements. This historical data can be invaluable for budgeting, helping you understand where your money is going, especially for informal expenses that might otherwise slip through the cracks. It provides a clear digital ledger of your smaller, everyday financial movements, allowing for better accountability and more informed financial decision-making when it comes to managing discretionary funds.

Understanding Fees and Financial Implications

While Venmo offers many free services, it’s critical to be aware of the instances where fees apply, as these can impact your personal finances. The most common fees include the 3% charge for sending money via a linked credit card and the 1.75% fee for instant transfers to your bank account. Other less frequent fees might apply for specific business transactions. Being conscious of these costs allows you to make financially intelligent choices, opting for fee-free methods whenever possible or consciously accepting a fee for the sake of convenience when necessary. Integrating these potential costs into your budgeting ensures there are no unwelcome surprises.

Venmo as Part of a Broader Financial Strategy

Venmo’s unparalleled convenience makes it an excellent tool for specific aspects of personal finance, particularly for peer-to-peer payments and managing shared expenses. However, it’s generally not designed to replace traditional banking services for large-scale financial planning, saving, or investing. It serves best as a complementary financial tool. Integrate Venmo by using it for its strengths – quick, social payments – while relying on traditional banks and dedicated financial planning tools for long-term savings, bill payments, and substantial investments. By understanding its specific role, you can leverage Venmo to enhance your daily financial fluidity without compromising your overarching financial health and stability.

In conclusion, paying someone on Venmo is a straightforward process that has significantly simplified personal financial transactions. By understanding its operational mechanics, embracing its security features, and being mindful of its financial implications, users can maximize Venmo’s utility as a powerful tool in their personal finance arsenal. From splitting bills to instant transfers, Venmo empowers individuals to manage their money with unprecedented ease and efficiency, making it an indispensable part of modern digital financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.