Michigan has long been synonymous with high car insurance rates, a reputation rooted in its unique no-fault system and the historically unlimited Personal Injury Protection (PIP) medical benefits. For residents and those considering a move to the Great Lakes State, understanding the intricacies of Michigan’s auto insurance market is not just a matter of curiosity, but a critical component of personal financial planning. The question isn’t merely about a dollar figure; it’s about navigating a complex landscape shaped by legislation, individual risk factors, and evolving market dynamics. This comprehensive guide will delve into the elements that determine car insurance costs in Michigan, offer insights into recent reforms, and provide actionable strategies for managing your premiums effectively.

Understanding Michigan’s Unique Auto Insurance Landscape

Michigan’s car insurance system has historically stood apart from almost every other state, primarily due to its no-fault structure and a unique approach to medical coverage for accident victims. This distinct framework has profoundly influenced premium costs, often placing Michigan at the top of national rankings for most expensive car insurance.

No-Fault Insurance Explained

Michigan operates under a “no-fault” auto insurance system. In a no-fault state, if you are involved in a car accident, your own insurance company pays for your medical expenses, lost wages, and other related costs, regardless of who was at fault for the accident. This system aims to streamline the claims process and reduce litigation by ensuring that injured parties receive immediate benefits without having to prove fault. While seemingly straightforward, Michigan’s no-fault system historically included an extraordinary component that significantly drove up costs: unlimited lifetime medical benefits through Personal Injury Protection (PIP).

The Impact of Unlimited PIP Coverage (and Recent Reforms)

Prior to July 2, 2020, every auto insurance policy sold in Michigan automatically included unlimited lifetime medical coverage for accident-related injuries through PIP. This meant that if you were severely injured in a car accident, your auto insurance policy would cover all reasonable and necessary medical expenses for the rest of your life, without limits. While this provided an unparalleled safety net for accident victims, it also made Michigan’s auto insurance premiums exceptionally high. The financial burden of funding these unlimited benefits, managed through the Michigan Catastrophic Claims Association (MCCA) assessment on every policy, was passed directly to policyholders.

The exorbitant costs led to widespread calls for reform, culminating in the historic 2020 legislative changes. These reforms introduced choices for PIP medical coverage, moving away from the mandatory unlimited option. This shift fundamentally altered the financial landscape of car insurance in Michigan, offering policyholders the ability to select lower PIP coverage limits and, theoretically, achieve significant premium reductions.

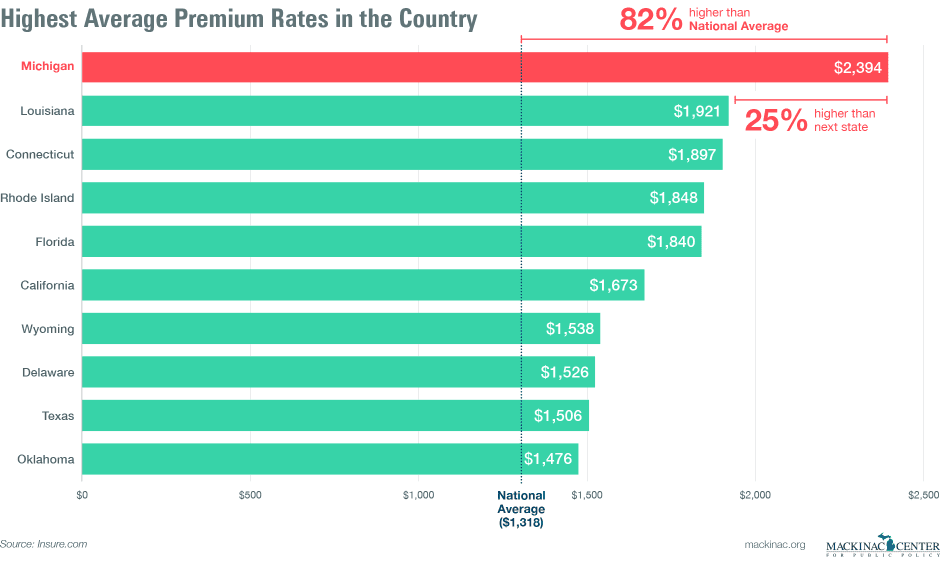

Why Michigan Was Historically the Most Expensive State

Michigan’s distinction as having the highest car insurance rates in the nation stemmed directly from the combination of its no-fault system and the mandatory unlimited PIP medical benefits. The MCCA, which covered medical claims exceeding a certain threshold (historically around $580,000, adjusted annually), assessed a fee on every auto insurance policy to fund these catastrophic claims. This assessment, combined with the general cost of managing a system with such extensive benefits, translated into significantly higher base premiums compared to states with lower or no-fault PIP requirements. The reforms aimed to address this fundamental cost driver, but the legacy of the old system continues to influence perceptions and, to some extent, current market realities.

Key Factors Influencing Your Michigan Car Insurance Premium

While Michigan’s unique insurance laws set a baseline, numerous individual factors contribute to the final premium you pay. Understanding these variables is crucial for both estimating costs and identifying opportunities for savings. Insurers assess a multitude of data points to determine your risk profile and, consequently, your rate.

Driver-Specific Variables (Age, Driving Record, Credit Score)

- Age and Experience: Younger, less experienced drivers (especially teenagers and those in their early twenties) typically face higher premiums due to their statistically higher accident rates. As drivers mature and gain more experience without incidents, rates tend to decrease.

- Driving Record: This is arguably one of the most significant factors. Accidents, traffic violations (speeding tickets, DUIs), and claims history directly correlate with increased risk and higher premiums. A clean driving record is your best asset for lower rates.

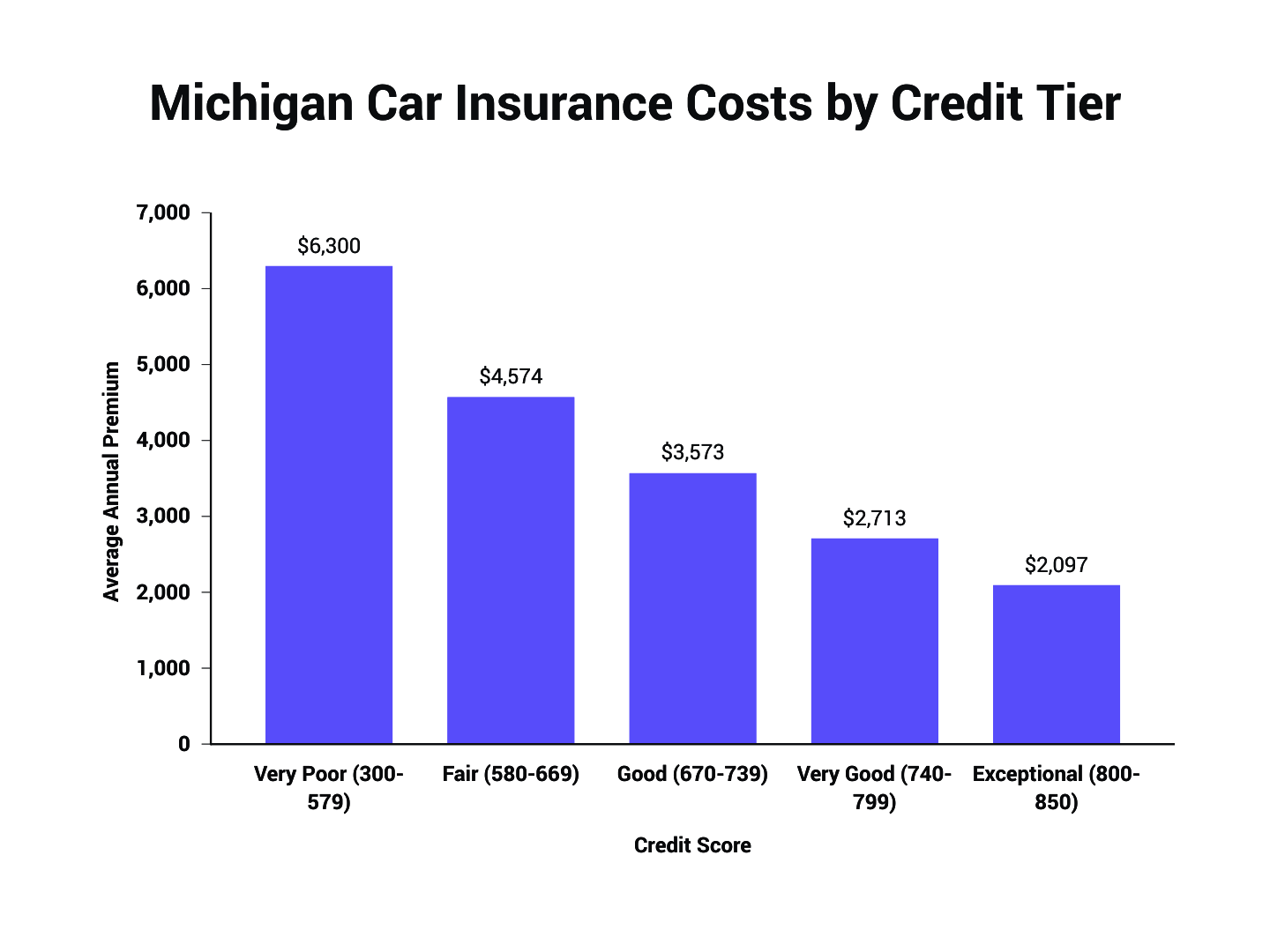

- Credit Score: In Michigan, like many other states, insurers often use a credit-based insurance score as a predictor of future claims. Individuals with higher credit scores generally pay less for insurance, as they are statistically less likely to file claims.

- Marital Status: Married individuals often receive slightly lower rates than single drivers, as they are statistically perceived as more stable and less prone to risky driving behaviors.

Vehicle-Specific Variables (Make, Model, Age, Safety Features)

- Make, Model, and Year: The type of car you drive significantly impacts your premium. Sports cars and luxury vehicles are typically more expensive to insure due to higher repair costs, greater likelihood of theft, and higher performance capabilities. Older, less valuable cars might have lower collision/comprehensive rates but could still be expensive if they lack modern safety features.

- Safety Features: Vehicles equipped with advanced safety features (e.g., anti-lock brakes, airbags, adaptive cruise control, lane departure warning systems) are often eligible for discounts because they reduce the risk of accidents or mitigate injury severity.

- Theft Risk: Vehicles that are popular targets for theft will generally have higher comprehensive coverage costs. Insurers track theft rates by vehicle model.

Geographic Location Within Michigan

Even within Michigan, where you live can have a substantial impact on your insurance rates. Urban areas, particularly those with higher population density, higher rates of accidents, or increased vehicle theft, typically have higher premiums than rural or suburban areas. For instance, residents of Detroit generally pay more than those in Traverse City, reflecting differences in traffic congestion, crime rates, and historical claims data.

Coverage Choices and Deductibles

Your policy’s structure plays a direct role in its cost:

- PIP (Personal Injury Protection): Post-2020 reforms, you now have choices for your PIP medical coverage, ranging from unlimited (the historical default) down to $50,000 or even an opt-out for those with qualified health coverage. Lowering your PIP limit will significantly reduce your premium.

- Bodily Injury Liability: This covers injuries you cause to others. Higher limits provide greater protection but increase your premium.

- Property Damage Liability: Covers damage you cause to another person’s property. Higher limits mean higher costs.

- Collision Coverage: Pays for damage to your own car from an accident, regardless of fault. It’s often optional if your car is paid off.

- Comprehensive Coverage: Pays for damage to your car from non-collision events like theft, vandalism, fire, or weather. Also often optional.

- Deductibles: The amount you pay out-of-pocket before your insurance kicks in for collision and comprehensive claims. Choosing a higher deductible (e.g., $1,000 instead of $500) will lower your premium, but means you pay more if you have a claim.

Navigating the 2020 Michigan Auto Insurance Reforms

The Michigan auto insurance reforms, effective July 2, 2020, represent the most significant overhaul of the state’s auto insurance laws in decades. These changes were primarily aimed at reducing Michigan’s notoriously high auto insurance premiums by introducing more choice and competition into the market.

The Shift to Choice in PIP Medical Coverage

The most impactful change was the elimination of the mandatory unlimited PIP medical coverage. Instead, Michigan drivers can now choose from several levels of PIP medical coverage:

- Unlimited: Retaining the historical, robust coverage.

- $500,000

- $250,000

- $50,000 (if you have Medicaid)

- Opt-out (if you have qualified health coverage that covers auto accident injuries or Medicare)

This newfound flexibility allows individuals to tailor their coverage to their financial situation and existing health insurance plans, providing a direct pathway to lower premiums for many.

Impact on Premiums: Expectations vs. Reality

The promise of the reforms was an average reduction in PIP premiums of 10% for unlimited coverage, 20% for $500,000, 35% for $250,000, and 45% for $50,000. For those who opted out, the PIP portion of their premium would be eliminated entirely. While many drivers have indeed seen significant savings, particularly those who chose lower PIP limits or opted out, the overall impact on total premiums has been more nuanced. Factors like rising repair costs, inflation, and continued increases in claims frequency have tempered some of the anticipated statewide reductions. Furthermore, the mandatory MCCA assessment, which was a large component of the unlimited PIP cost, was eliminated for those choosing lower PIP limits, but continues for those who select unlimited PIP coverage (albeit at a reduced rate for a transitional period).

Understanding Your New Coverage Options

It is crucial for Michigan drivers to fully understand their choices and the implications of each. While opting for lower PIP limits can save money, it also transfers more risk to the individual. Before selecting a lower PIP option or opting out, carefully review your health insurance policy to ensure it adequately covers auto accident injuries, has reasonable deductibles, and does not have exclusions for motor vehicle accidents. Consulting with a trusted insurance agent or financial advisor is highly recommended to ensure you make an informed decision that aligns with your overall financial and healthcare safety net.

Strategies to Lower Your Car Insurance Costs in Michigan

Given the inherent costs of car insurance in Michigan, proactive strategies are essential for minimizing your financial outlay without compromising necessary protection. By understanding how insurers price policies and leveraging available options, you can significantly reduce your premiums.

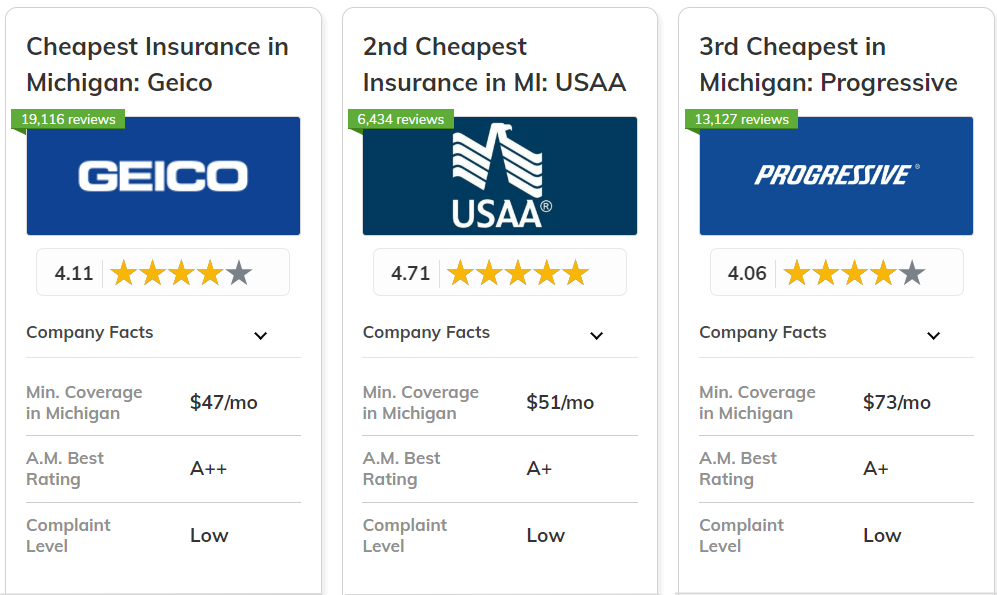

Shopping Around and Comparing Quotes

This is perhaps the most effective strategy. Car insurance rates can vary dramatically between different providers for the exact same coverage. Each insurer uses its own proprietary algorithms and risk assessment models. Therefore, getting quotes from at least three to five different companies, including large national carriers and smaller regional ones, is paramount. Websites and independent agents can help you compare options efficiently. Make it a practice to re-shop your insurance every year or two, or whenever a significant life event occurs (e.g., getting married, moving, buying a new car).

Bundling Policies

Many insurance companies offer discounts if you purchase multiple policies from them, such as combining your auto insurance with your home, renters, or life insurance. These “multi-policy” or “bundling” discounts can often lead to substantial savings, sometimes 10-25% or more on your total insurance spend. It’s a win-win: you consolidate your insurance needs and reduce your overall costs.

Maximizing Discounts (Good Driver, Multi-Car, Telematics)

Insurers offer a wide array of discounts that drivers often overlook. Ask your agent about every discount you might qualify for:

- Good Driver/Accident-Free Discount: For maintaining a clean driving record over a certain period.

- Multi-Car Discount: If you insure multiple vehicles with the same company.

- Telematics/Usage-Based Insurance: Programs that monitor your driving habits (speed, braking, mileage) via an app or device and offer discounts for safe driving.

- Good Student Discount: For young drivers who maintain a certain GPA.

- Defensive Driving Course Discount: Completing an approved safety course.

- Anti-Theft Device Discount: For cars equipped with alarms or tracking systems.

- Payment Discounts: For paying in full, setting up auto-pay, or choosing paperless billing.

Adjusting Deductibles and Coverage Limits

As discussed, your deductibles and coverage limits directly impact your premium.

- Increase Deductibles: Opting for a higher deductible (e.g., $1,000 instead of $250 or $500) on your collision and comprehensive coverage can significantly lower your premium. Just ensure you have enough savings to cover the deductible should you need to file a claim.

- Review PIP Limits: Post-2020 reforms, carefully reconsider your PIP medical coverage limits based on your health insurance and financial comfort with risk.

- Drop Unnecessary Coverage: If you have an older, low-value car, you might consider dropping collision and/or comprehensive coverage, as the cost of the premium might outweigh the potential payout in an accident. Always perform a cost-benefit analysis.

Improving Your Credit Score

Since credit-based insurance scores are a factor in Michigan, improving your overall credit health can lead to lower insurance premiums over time. Pay bills on time, reduce debt, and monitor your credit report for errors. This financial discipline not only benefits your insurance rates but also your broader financial well-being.

The Long-Term Financial Planning for Auto Insurance

Car insurance isn’t a one-time purchase; it’s an ongoing financial commitment. Treating it as such, and integrating it into your long-term financial planning, ensures you remain adequately protected without overspending.

Budgeting for Annual Premiums

Incorporate your auto insurance premiums into your annual budget. Whether you pay monthly, semi-annually, or annually, knowing this fixed cost helps you manage your cash flow. Consider setting aside funds regularly if you prefer to pay a larger sum upfront to potentially receive a discount. For families, factor in potential increases as young drivers are added to policies.

Regular Policy Reviews

Don’t just set it and forget it. Review your auto insurance policy at least once a year, or whenever significant life changes occur. Did you get married? Buy a new car? Move to a new neighborhood? Have a child go off to college? Each of these events can affect your rates and coverage needs. A regular review ensures your coverage remains appropriate and that you’re taking advantage of all possible discounts. It’s also an excellent opportunity to re-shop for quotes.

The Importance of Adequate Coverage

While saving money is a priority, never compromise on adequate coverage. Being underinsured can lead to devastating financial consequences in the event of a serious accident, potentially wiping out savings or future earnings. Ensure your liability limits are robust enough to protect your assets, especially in a no-fault state where you might still be sued for serious injuries. Understand what your chosen PIP limit truly means for your medical expenses. The goal is to find a balance between affordability and comprehensive financial protection, ensuring peace of mind on Michigan’s roads.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.