Securing car insurance is far more than a mere transactional task; it’s a fundamental pillar of responsible personal finance and asset protection. For many, a vehicle represents a significant investment and a crucial tool for daily life, from commuting to work to managing family responsibilities. Without adequate insurance, this vital asset, and your financial well-being, remain perilously exposed to a myriad of risks, from minor fender-benders to catastrophic accidents and even theft. This guide delves into the financial intricacies of acquiring car insurance, offering a comprehensive roadmap for navigating the marketplace, optimizing coverage, and ultimately safeguarding your monetary future.

Understanding Car Insurance: A Financial Necessity

Car insurance is a legally mandated financial product designed to protect you from the financial consequences of vehicle-related incidents. It acts as a critical safety net, mitigating the potentially devastating costs associated with accidents, damage, or theft. From a financial perspective, understanding its purpose and various components is the first step towards making informed decisions that protect your wealth.

Why Car Insurance Matters

The importance of car insurance transcends mere compliance with legal requirements; it is an essential component of sound personal financial planning.

- Legal Requirements: In almost every state and country, carrying a minimum level of car insurance is a legal prerequisite for operating a vehicle. Driving without it can lead to severe penalties, including hefty fines, license suspension, vehicle impoundment, and even jail time. These penalties not only represent direct financial costs but can also create long-term financial disadvantages, such as increased future insurance premiums due to a tainted driving record. Adhering to these laws is not just about avoiding punishment; it’s about being a responsible participant in the financial ecosystem of road users.

- Financial Protection: Accidents happen, and when they do, the costs can escalate rapidly. Car insurance shields you from these potentially ruinous expenses. Imagine being at fault in an accident that causes significant damage to another vehicle or, worse, leads to serious injuries for others. Without liability insurance, you would be personally responsible for all repair costs, medical bills, legal fees, and potential lost wages for the injured parties. This could amount to hundreds of thousands or even millions of dollars, leading to bankruptcy, asset forfeiture, and long-term financial distress. Even if you are not at fault, specific coverages can protect your own vehicle and physical well-being.

- Peace of Mind: Beyond the tangible financial benefits, car insurance offers invaluable peace of mind. Knowing that you are financially protected against unforeseen circumstances allows you to drive with confidence, reducing anxiety about potential financial setbacks. This psychological benefit, while not quantifiable in monetary terms, contributes significantly to overall well-being and allows you to focus your financial energy on growth and investment rather than constant worry about potential liabilities.

Key Types of Coverage

Car insurance isn’t a single product but a bundle of distinct coverages, each addressing specific financial risks. Understanding these components is crucial for assembling a policy that adequately meets your needs without overpaying.

- Liability Coverage: This is the cornerstone of any car insurance policy and is almost universally required by law. It consists of two main parts:

- Bodily Injury Liability: Pays for medical expenses, lost wages, and pain and suffering for anyone you injure in an accident where you are at fault. This protects your assets from lawsuits arising from injuries.

- Property Damage Liability: Pays for damage to another person’s property (their car, fence, building, etc.) that you cause in an accident. This protects you from the financial burden of repairing or replacing someone else’s assets.

- Collision Coverage: This coverage pays for damage to your vehicle resulting from a collision with another car or object, regardless of who is at fault. It’s especially important for newer or more valuable vehicles where repair or replacement costs can be substantial. When you finance or lease a car, collision coverage is almost always required by the lender to protect their financial interest in the vehicle.

- Comprehensive Coverage: Often paired with collision, comprehensive coverage protects your vehicle from non-collision-related incidents. This includes damage from fire, theft, vandalism, falling objects (like tree branches), natural disasters (hail, floods), and animal collisions. Like collision, it’s typically required by lenders for financed or leased vehicles.

- Uninsured/Underinsured Motorist (UM/UIM) Coverage: This crucial coverage protects you financially if you are involved in an accident with a driver who either has no insurance (uninsured) or insufficient insurance (underinsured) to cover your damages and medical expenses. Given the prevalence of uninsured drivers, this coverage acts as a vital financial safeguard, ensuring you don’t bear the burden of another driver’s irresponsibility.

- Medical Payments (MedPay) / Personal Injury Protection (PIP): These coverages pay for medical expenses (and sometimes lost wages, rehabilitation, or funeral expenses) for you and your passengers, regardless of who is at fault for an accident. PIP is more extensive and is mandatory in “no-fault” states, where your own insurance company pays for your medical expenses up to a certain limit, regardless of fault. These coverages are critical for protecting your personal finances from immediate medical costs following an accident.

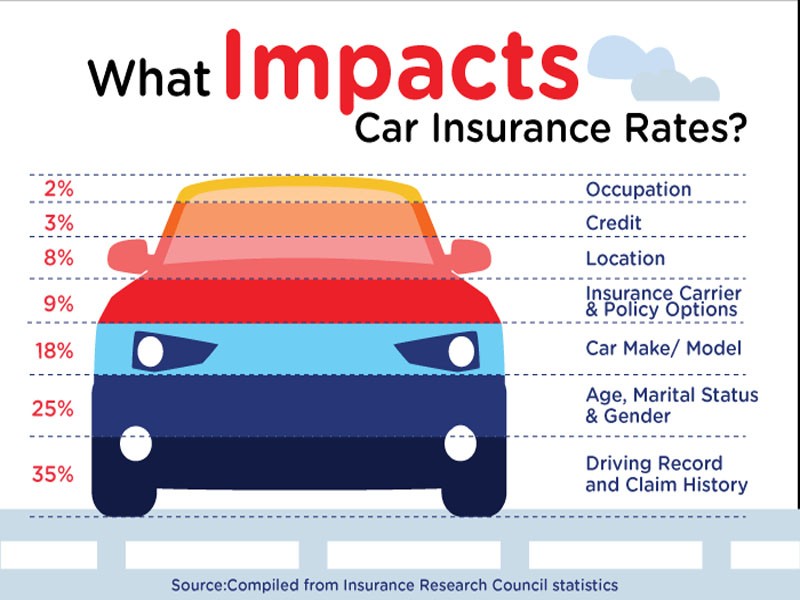

Factors Influencing Premiums

Car insurance premiums are meticulously calculated based on a complex interplay of risk factors. Understanding these can help you anticipate costs and identify areas for potential savings.

- Driver Profile: Your age, gender, marital status, and driving record (accidents, traffic violations) significantly impact premiums. Younger, less experienced drivers, and those with a history of infractions, typically face higher rates due to their statistically higher risk profiles.

- Vehicle Type: The make, model, year, safety features, and even the color of your car can influence rates. Expensive-to-repair luxury cars, high-performance sports cars, and models frequently targeted by thieves often incur higher premiums. Vehicles with advanced safety features may qualify for discounts.

- Location: Where you live and park your car plays a substantial role. Urban areas with higher traffic density, crime rates, and greater likelihood of accidents or theft generally have higher premiums than rural areas. Even your specific zip code can influence rates.

- Driving History: A clean driving record is your best financial asset when it comes to car insurance. Accidents and moving violations signal higher risk to insurers, leading to increased premiums for several years. Conversely, a long history of safe driving often qualifies you for significant discounts.

- Credit Score: In many states, insurers use a credit-based insurance score (which is related to, but not identical to, your regular credit score) as a predictive tool for risk. Statistically, individuals with higher credit scores tend to file fewer claims. Maintaining good credit can therefore lead to lower insurance costs.

Navigating the Car Insurance Marketplace

The car insurance marketplace is vast and competitive, offering a multitude of choices from national giants to regional specialists. Effectively navigating this landscape requires strategic research and a clear understanding of your personal financial situation and coverage needs.

Researching Reputable Providers

Choosing the right insurance company is as important as selecting the right coverage. You want a financially stable company that offers competitive rates and excellent customer service, especially when it comes to handling claims.

- Financial Stability Ratings: Consult independent rating agencies such as A.M. Best, Standard & Poor’s, or Moody’s. A strong financial rating indicates the company’s ability to meet its financial obligations, including paying out claims, even in adverse economic conditions. This ensures your policy is a reliable financial safeguard.

- Customer Reviews and Satisfaction Scores: While financial stability is key, equally important is the company’s track record in customer service. Websites like J.D. Power, Consumer Reports, and the National Association of Insurance Commissioners (NAIC) provide valuable insights into customer satisfaction regarding claims processing, communication, and overall experience. Look for companies with a reputation for transparent communication and efficient claims handling.

- Policy Offerings and Flexibility: Assess whether the insurer offers the specific coverages and deductibles you need. Some companies specialize in certain niches (e.g., high-risk drivers, classic cars), while others offer a broader range of products and bundling options (e.g., home and auto) that can lead to significant financial savings.

Gathering Necessary Information

Before seeking quotes, prepare all relevant information. Having this data readily available streamlines the process and ensures accurate premium estimates.

- Personal Details: This includes your full name, date of birth, marital status, occupation, and current address. Your driving history (accidents, violations, claims) for all drivers to be insured is paramount.

- Vehicle Information: Provide the make, model, year, Vehicle Identification Number (VIN), odometer reading, and details on any anti-theft devices or safety features installed. If the vehicle is financed or leased, you’ll need the lienholder’s information.

- Driving Record for All Drivers: Be prepared to provide driver’s license numbers and dates of birth for anyone who will be driving the car, especially those living in your household. A complete and accurate driving history is critical for receiving precise quotes.

The Quote Process: Online, Agent, or Broker

There are several avenues for obtaining quotes, each with its own advantages.

- Comparison Websites: These online platforms allow you to input your information once and receive multiple quotes from various insurers simultaneously. They are excellent for quickly comparing prices, but always double-check the coverage details to ensure you’re comparing apples to apples. They may not include all insurers, especially smaller, regional ones.

- Independent Agents: An independent agent works with several different insurance companies. They can shop around on your behalf, providing you with a range of options and expert advice tailored to your financial needs. Their goal is to find the best policy and price for you, as they are not tied to a single insurer. This can be particularly beneficial for complex situations or specific coverage requirements.

- Captive Agents: These agents work exclusively for one insurance company (e.g., State Farm, Allstate). They have in-depth knowledge of their company’s products and can often offer personalized service. While they can’t compare rates across different companies, they might be able to find unique discounts or bundled packages within their own insurer’s offerings.

Optimizing Your Policy for Cost-Effectiveness and Coverage

Once you understand the basics, the next financial step is to strategically optimize your policy. This involves finding the sweet spot between adequate coverage and manageable premiums, ensuring you get the most financial value for your money.

Smart Strategies for Lowering Premiums

There are numerous ways to reduce your insurance costs without compromising essential protection.

- Bundling Policies: Many insurers offer significant discounts when you purchase multiple policies (e.g., auto, home, renter’s, life) from them. This “multi-policy discount” can often be one of the largest savings opportunities. From a financial planning perspective, consolidating your insurance needs with one provider can also simplify administration.

- Discounts, Discounts, Discounts: Actively inquire about all available discounts. Common examples include:

- Good Driver Discount: For maintaining a clean driving record for a certain number of years.

- Good Student Discount: For young drivers who maintain a high GPA.

- Anti-Theft Device Discount: For vehicles equipped with alarms, immobilizers, or tracking systems.

- Safety Features Discount: For cars with advanced safety features like anti-lock brakes, airbags, and automatic emergency braking.

- Low Mileage Discount: For drivers who don’t drive frequently.

- Defensive Driving Course Discount: For completing an approved defensive driving course.

- Multi-Car Discount: For insuring more than one vehicle with the same company.

- Pay-in-Full Discount: For paying your annual premium upfront rather than in installments.

- Higher Deductibles: Your deductible is the amount you pay out-of-pocket before your insurance coverage kicks in for a claim. Choosing a higher deductible (e.g., $1,000 instead of $500) will lower your premium. However, ensure you have sufficient liquid savings in your emergency fund to comfortably cover this higher deductible should an accident occur. It’s a risk-reward calculation: lower monthly payments now versus a larger out-of-pocket expense later.

- Vehicle Safety Features: Cars equipped with advanced safety technologies like automatic emergency braking, lane-keeping assist, and blind-spot monitoring may qualify for lower premiums due to their potential to reduce the likelihood or severity of accidents. When purchasing a new vehicle, consider the long-term insurance implications of its safety ratings and features.

- Review Coverage on Older Cars: For older vehicles with low market value, reconsider if comprehensive and collision coverage are still financially prudent. If the annual cost of these coverages approaches or exceeds 10% of the car’s actual cash value, it might be more economical to drop them and self-insure against physical damage, saving the premium for potential future repairs or replacement.

Customizing Your Coverage

Your financial situation, risk tolerance, and the value of your assets should dictate your coverage choices.

- Balancing Risk vs. Cost: Don’t automatically opt for the cheapest policy if it means inadequate protection. Conversely, don’t over-insure. Assess your personal risk profile: do you have significant assets to protect from lawsuits (requiring higher liability limits)? Do you live in an area prone to theft or natural disasters (necessitating strong comprehensive coverage)? Find the balance that secures your finances without unnecessary expenditure.

- Understanding Deductibles and Limits: Clearly understand the implications of your chosen deductibles and coverage limits. Higher liability limits offer greater financial protection but come with higher premiums. A lower deductible means less out-of-pocket for claims but a higher premium. Tailor these to your comfort level with risk and your financial capacity to absorb immediate costs.

The Importance of Annual Reviews

The insurance market, like your life, is not static. Regular reviews are critical for maintaining optimal financial efficiency.

- Market Changes: Insurance rates can fluctuate significantly from year to year due to various factors, including regional accident rates, natural disaster frequency, and changes in repair costs. Reviewing your policy annually (or at least every few years) allows you to shop around and ensure you’re still getting the most competitive rates.

- Personal Circumstances: Life changes such as marriage, moving to a new address, adding a teenage driver, buying a new car, or improving your credit score can all impact your insurance needs and eligibility for discounts. Proactively updating your insurer about these changes can either lead to savings or ensure your coverage remains adequate.

- Policy Adjustments: Over time, your financial priorities may shift. Perhaps your emergency fund has grown, allowing you to comfortably take on a higher deductible for a lower premium. Or maybe you’ve paid off your car, making collision and comprehensive coverage optional rather than mandatory. Annual reviews are the perfect opportunity to make these strategic adjustments.

Finalizing Your Policy and Beyond

The process doesn’t end once you’ve chosen a policy. Careful review, understanding payment terms, and knowing what to do in the event of a claim are all critical financial steps.

Reviewing the Policy Document

Before making any payment, meticulously read your entire policy document. This dense legal contract outlines the precise terms of your financial protection.

- Understanding Terms and Conditions: Pay close attention to definitions, coverage limits, deductibles, and any specific endorsements or exclusions. Ensure the policy accurately reflects the coverages you discussed and intended to purchase.

- Exclusions: Be aware of what your policy does not cover. Common exclusions might include intentional damage, racing, or using your personal vehicle for commercial purposes without specific commercial coverage. Understanding these helps manage financial expectations in a claim situation.

Payment Options and Grace Periods

Insurers offer various payment schedules, each with financial implications.

- Monthly, Quarterly, Annually: Paying your premium annually in full often comes with a discount, making it the most cost-effective option if you have the liquidity. Monthly or quarterly payments offer flexibility but might incur small processing fees.

- Auto-Pay: Setting up automatic payments ensures you don’t miss a payment, which could lead to a lapse in coverage and potentially higher future premiums or penalties.

- Grace Periods: Understand your insurer’s grace period for late payments. While it offers a small window of flexibility, it’s always best to pay on time to avoid lapses in coverage, which create significant financial risk.

What to Do After an Accident

Knowing the correct steps after an accident is crucial for efficient claims processing and protecting your financial interests.

- Reporting Claims Promptly: Notify your insurance company as soon as safely possible after an accident, even if you don’t plan to file a claim immediately. Delays can complicate the process and potentially jeopardize your coverage.

- Documentation: Collect as much evidence as possible at the scene: photos of damage, contact information of other parties and witnesses, police report numbers, and details of the incident. This documentation is invaluable for supporting your claim and accurately assessing financial damages.

- Communication with Insurer: Cooperate fully with your insurer and provide all requested information. Be honest and factual. They will guide you through the claims process, which is designed to restore your financial position after an insured event.

Common Pitfalls and How to Avoid Them

Even with careful planning, some common mistakes can lead to financial repercussions. Being aware of these pitfalls can save you money and headaches in the long run.

Underinsuring Your Vehicle

One of the most dangerous financial mistakes is choosing the bare minimum coverage to save money upfront.

- Risks of Insufficient Coverage: State minimum liability limits are often inadequate to cover serious accidents, leaving your personal assets vulnerable to lawsuits. If you cause a severe accident and your liability limits are exhausted, you are personally responsible for the remaining damages. This could mean your savings, investments, and even future earnings are at risk, leading to severe financial distress. Always assess your net worth and choose liability limits that adequately protect your assets.

Overpaying for Unnecessary Coverage

Conversely, paying for coverage you don’t genuinely need can be a drain on your finances.

- Evaluating Needs: Regularly review your policy to ensure it aligns with your current situation. For instance, if you have an older car with minimal market value, the cost of collision and comprehensive coverage might outweigh the potential payout after a deductible. Similarly, if your health insurance provides excellent accident coverage, you might be able to reduce your MedPay/PIP limits. Be financially strategic and cut what is genuinely redundant.

Neglecting Policy Updates

Failing to update your insurance policy after significant life changes or ignoring annual review opportunities can lead to both inadequate coverage and missed savings.

- Impact on Claims and Premiums: If you move to a new area with higher risk but don’t update your address, your insurer might deny a claim or charge a higher premium retroactively. Conversely, if you get married or improve your driving record, you could be missing out on valuable discounts. Proactive communication with your insurer ensures your policy remains optimized financially and in terms of protection.

Getting insurance on a car is a critical financial decision that impacts your wallet, your assets, and your peace of mind. By thoroughly understanding the types of coverage, strategically shopping for the best rates, and regularly reviewing your policy, you can ensure you’re adequately protected without overspending. This financial diligence transforms car insurance from a mere obligation into a powerful tool for safeguarding your personal wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.