Navigating the complexities of Social Security retirement benefits can be a daunting task, especially when trying to understand the financial landscape of early claiming. For many, turning 62 marks the earliest opportunity to begin receiving Social Security payments, a decision often driven by a mix of immediate financial need, health considerations, or a desire to exit the workforce. However, claiming benefits at this age comes with significant implications, primarily a permanent reduction in monthly payments compared to waiting until your Full Retirement Age (FRA). The question then naturally arises: is there a floor to this reduction? What exactly constitutes the “minimum” Social Security payment one might receive at age 62? This comprehensive guide aims to demystify this critical aspect of retirement planning, exploring the various factors that influence benefit amounts, the concept of a special minimum benefit, and strategic considerations for those contemplating early claiming.

Understanding your potential Social Security income is paramount for robust retirement planning. It’s not just about what you could receive, but what the absolute baseline might be, particularly if your work history has been sporadic or low-earning. The Social Security Administration (SSA) operates on a system designed to provide a safety net, but the amount each individual receives is highly personalized, based on a meticulous calculation of their earnings record over decades. While the idea of a fixed “minimum” payment is appealing for simplicity, the reality is nuanced, involving a combination of individual work history, specific rules for early claiming, and a lesser-known provision for a special minimum benefit designed for long-term, low-wage workers. As we delve into these details, it will become clear that while a universal minimum might not exist in the conventional sense, understanding the lowest possible payouts requires a look at both the standard benefit reduction and the special provisions aimed at poverty prevention.

Understanding Social Security Retirement Benefits

Before we can address the concept of a minimum payment, it’s crucial to grasp the foundational principles of how Social Security retirement benefits are determined and when they can be claimed. This understanding forms the bedrock upon which all subsequent calculations and considerations are built.

The Basics of Social Security

Social Security is a social insurance program in the United States, providing benefits for retirees, disabled workers, and their survivors. It’s funded primarily through payroll taxes (FICA taxes) paid by workers and employers. When you work and pay Social Security taxes, you earn “credits.” In 2024, you earn one credit for each $1,730 of earnings, up to a maximum of four credits per year. Most people need 40 credits (10 years of work) to be eligible for retirement benefits. These credits ensure you qualify for benefits, but the amount you receive depends on your earnings history.

Eligibility Requirements for Retirement Benefits

The earliest age an individual can start receiving Social Security retirement benefits is 62. To be eligible, you must have accrued at least 40 work credits. While age 62 grants eligibility, it does not mean you receive your full benefit amount. This distinction is critical for understanding the “minimum” payment at this age. Claiming at 62 initiates a permanent reduction in your monthly benefit, a trade-off for receiving payments over a longer period.

Full Retirement Age (FRA) Explained

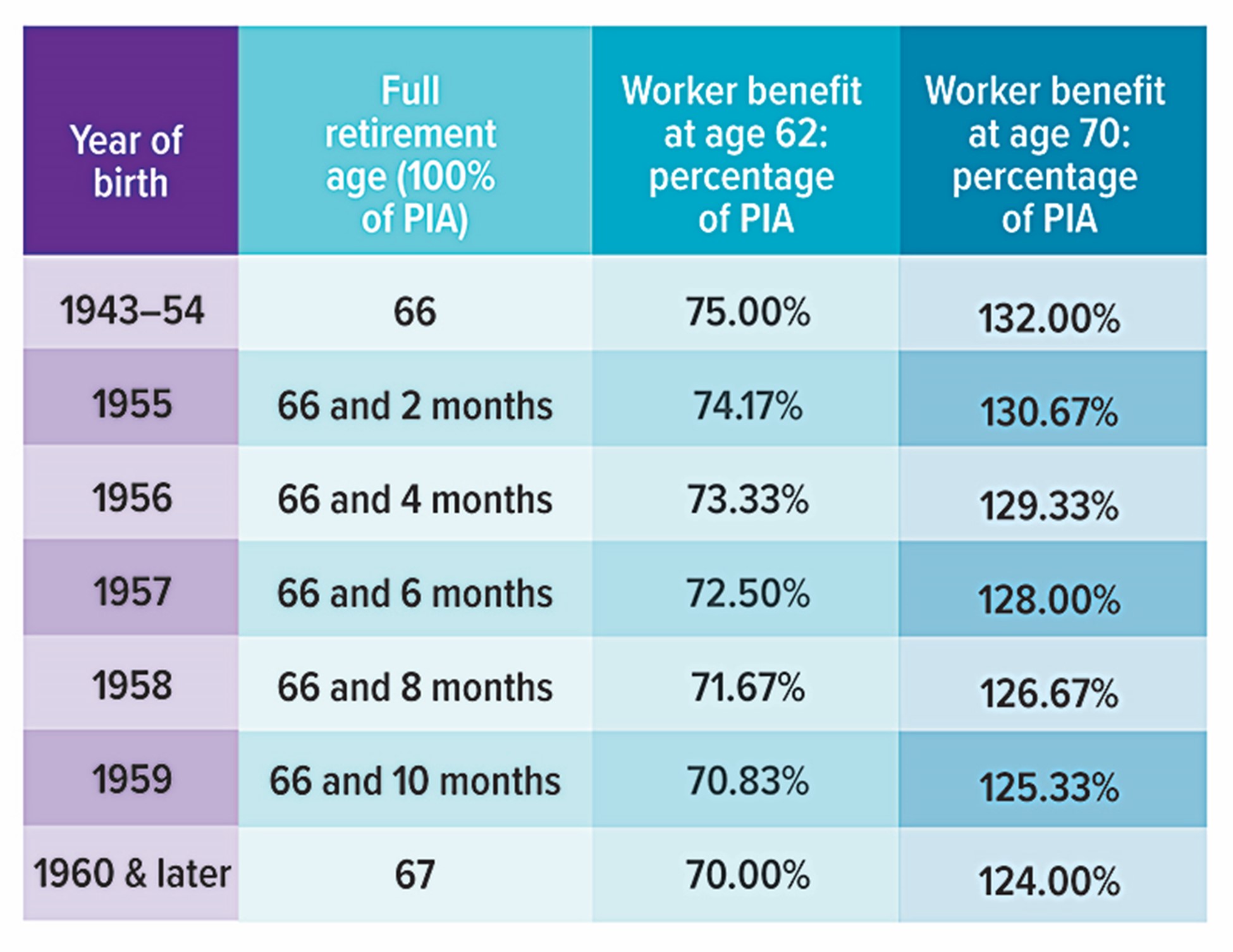

Your Full Retirement Age (FRA) is the age at which you are entitled to receive 100% of your primary insurance amount (PIA). The FRA depends on your birth year. For those born in 1943 through 1954, FRA is 66. It gradually increases by a few months for those born between 1955 and 1959, reaching 67 for anyone born in 1960 or later. Understanding your FRA is vital because it serves as the benchmark for calculating early or delayed retirement benefits. Any claim before your FRA results in a reduction, and any claim after (up to age 70) results in an increase.

The Impact of Claiming Benefits at Age 62

The decision to claim Social Security at age 62 is perhaps the most significant choice you can make regarding your retirement income, as it locks in a permanently reduced benefit amount. This reduction is not arbitrary but calculated based on a specific formula.

The Reduction for Early Claiming

When you claim Social Security benefits before your Full Retirement Age (FRA), your monthly payment is permanently reduced. The reduction is applied for each month you claim before your FRA. For someone with an FRA of 67, claiming at age 62 results in a benefit reduction of approximately 30%. For instance, if your FRA is 67 and your monthly benefit at that age would be $1,500, claiming at 62 would reduce it to around $1,050. This percentage reduction is applied to your Primary Insurance Amount (PIA), which is the benefit you would receive if you started benefits at your FRA.

How Your Primary Insurance Amount (PIA) is Calculated

Your Primary Insurance Amount (PIA) is the full monthly benefit you’re entitled to at your FRA. The SSA calculates your PIA based on your Average Indexed Monthly Earnings (AIME). This involves taking your 35 highest-earning years, adjusting them for inflation (indexing) to reflect wage levels at the time you turn 60, and then averaging them. If you have fewer than 35 years of earnings, zero-earning years are factored into the average, which can significantly lower your AIME and thus your PIA. The AIME is then run through a progressive formula with “bend points” that provide a higher replacement rate for lower earners. This progressive formula is designed to ensure that those with lower lifetime earnings receive a proportionally higher benefit relative to their contributions than high earners.

The Earnings Limit for Early Claimers

Another critical factor for those claiming benefits at age 62 is the Social Security earnings limit. If you claim benefits before your FRA and continue to work, your benefits may be temporarily withheld if your earnings exceed a certain threshold. In 2024, if you are under your FRA for the entire year, the SSA deducts $1 from your benefits for every $2 you earn above $22,320. In the year you reach your FRA, the limit is higher ($59,520 in 2024), and the deduction is $1 for every $3 earned above the limit, until the month you reach FRA. Once you reach your FRA, the earnings limit no longer applies, and you can earn any amount without your Social Security benefits being reduced. Any benefits withheld due to the earnings limit are not lost forever; they are used to recalculate your benefit at your FRA, potentially leading to a slightly higher monthly payment.

Is There a True “Minimum” Social Security Payment?

While there isn’t a universally fixed “minimum” payment for all claimants at age 62, the Social Security Administration does have a provision known as the Special Minimum Benefit, designed to help long-term, low-wage workers. This is the closest concept to a defined minimum.

The Special Minimum Benefit

The Special Minimum Benefit is a provision within the Social Security program intended to provide a basic level of protection for individuals who have worked for many years under covered employment but at very low wages. It ensures that individuals with a substantial work history, despite low earnings, receive a benefit amount that exceeds what they might otherwise qualify for under the standard PIA calculation. This benefit is less common today than in the past because regular benefits, even for low earners, often exceed the special minimum benefit due to wage indexing and benefit formula adjustments. However, it’s still a critical safety net for a specific demographic.

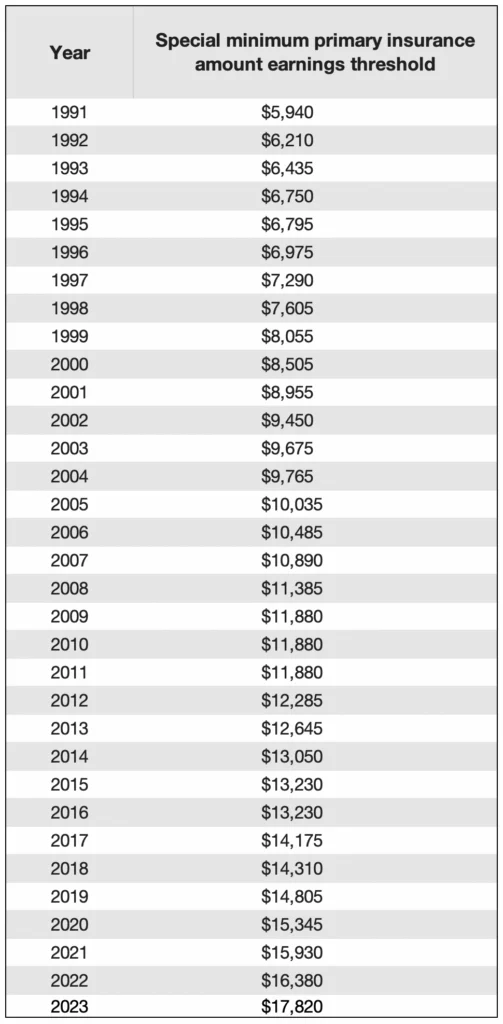

Who Qualifies for the Special Minimum Benefit?

To qualify for the Special Minimum Benefit, an individual must have a certain number of “years of coverage” (YOCs). A year of coverage is a year in which your earnings reached a specified threshold. This threshold is typically based on a certain percentage of the national average wage index. The more YOCs you have, the higher your special minimum benefit. For example, in 2024, if you have 30 or more YOCs, you would receive the maximum special minimum benefit. The amount decreases with fewer YOCs, down to a minimum of 11 YOCs to qualify for any special minimum benefit. It’s important to note that these YOCs are distinct from the 40 credits required for basic eligibility; YOCs relate specifically to earnings levels within those years.

Calculating the Special Minimum Benefit (Historical Context & Current Relevance)

The Special Minimum Benefit is calculated based on the number of years of coverage (YOCs) an individual has. For example, in 2024, the maximum special minimum benefit for someone with 30 or more YOCs was around $1,033 per month. This amount is indexed annually for inflation. If an individual’s PIA, calculated through the standard method, is lower than their special minimum benefit, they would receive the special minimum benefit. Conversely, if their standard PIA is higher, they receive the standard PIA. This provision ensures that even individuals with very low career earnings but a long history of work receive a more substantial benefit than they might otherwise. However, due to significant increases in the average wage index over time and the progressive nature of the standard PIA formula, most low-wage workers today find that their standard PIA calculation results in a higher benefit than the special minimum benefit, making this provision less frequently applied than in decades past. Therefore, for most people claiming at 62, the “minimum” payment will be their standard PIA, reduced by approximately 30% for early claiming, rather than the special minimum benefit.

Factors Influencing Your Social Security Benefit Amount

Beyond the basics of eligibility and early claiming reductions, several key factors directly impact the size of your Social Security payment, whether at age 62 or later. Understanding these influences is crucial for estimating your potential benefits.

Lifetime Earnings Record

The most significant factor determining your Social Security benefit is your lifetime earnings record. The SSA considers your 35 highest-earning years, adjusted for inflation (indexed), to calculate your Average Indexed Monthly Earnings (AIME). The higher your AIME, the higher your Primary Insurance Amount (PIA) will be. Conversely, if you have years with low or no earnings within those 35 years, these will depress your average, leading to a lower PIA. This underscores the importance of consistent employment and earning as much as possible throughout your career to maximize your Social Security benefits.

Number of Years Worked

While 40 credits (10 years of work) are required for eligibility, having more than 10 years of work is highly beneficial, especially having 35 years or more. As mentioned, the SSA uses your 35 highest-earning years. If you’ve worked fewer than 35 years, zero-earnings years will be included in the calculation of your AIME, which will inevitably lower your average and, consequently, your benefit amount. Therefore, working at least 35 years at meaningful income levels is key to optimizing your Social Security benefit.

Spousal and Survivor Benefits Considerations

Social Security isn’t just for individual workers; it also provides benefits for spouses, divorced spouses, and survivors.

- Spousal Benefits: If your spouse claims benefits, you might be eligible for a spousal benefit if it’s higher than your own benefit. A spousal benefit can be up to 50% of your spouse’s full retirement age benefit. You can claim a spousal benefit as early as age 62, but it will also be reduced for early claiming.

- Divorced Spousal Benefits: You may be eligible for benefits based on your ex-spouse’s earnings record if the marriage lasted at least 10 years, you are currently unmarried, and you are 62 or older. Your ex-spouse does not need to be collecting benefits for you to apply, but they must be at least 62.

- Survivor Benefits: If your spouse passes away, you or other family members (children, dependent parents) may be eligible for survivor benefits. A widow(er) can claim survivor benefits as early as age 60 (or age 50 if disabled) and receive 100% of the deceased spouse’s benefit if claiming at their own FRA. If claiming early, the benefit is reduced.

These benefits can significantly impact the total household income in retirement and should be considered when planning your claiming strategy, especially for those with lower individual earnings records.

Cost-of-Living Adjustments (COLAs)

Social Security benefits are subject to annual Cost-of-Living Adjustments (COLAs). These adjustments are designed to help benefits keep pace with inflation. Each year, the Social Security Administration announces a COLA, which increases the monthly benefit amount for all beneficiaries. While COLAs don’t directly determine your initial “minimum” payment at age 62, they ensure that the purchasing power of your benefits is maintained over time, which is an important aspect of long-term financial stability in retirement.

Strategic Considerations for Claiming Social Security Early

Deciding when to claim Social Security is one of the most significant financial decisions you’ll make in retirement. While age 62 offers the earliest opportunity, it comes with permanent implications. A thoughtful strategy, rather than a default decision, is paramount.

Financial Needs vs. Long-Term Impact

The most common reason people claim Social Security at age 62 is immediate financial need. They may have lost a job, experienced health issues, or simply cannot afford to continue working. While early claiming provides much-needed income, it’s crucial to weigh this immediate relief against the long-term impact of permanently reduced benefits. A 30% reduction can amount to tens or even hundreds of thousands of dollars over a typical retirement lifespan. It’s essential to project your future expenses and alternative income sources to understand if an early claim is truly necessary or if other short-term solutions (e.g., drawing from savings, part-time work) could preserve a higher Social Security benefit.

Health Status and Life Expectancy

Your personal health and estimated life expectancy play a significant role in the claiming decision. If you have a family history of longevity and are in good health, delaying benefits to receive a higher monthly payment might be a wise choice, as you’re likely to collect that higher amount for a longer period. Conversely, if you have significant health issues or a shorter life expectancy, claiming early might be advantageous, ensuring you collect benefits for as long as possible. This is a highly personal calculation, often involving a “break-even point” analysis to determine when the cumulative benefits from early claiming would equal or surpass the cumulative benefits from delayed claiming.

Coordinating with Other Retirement Income Sources

Social Security should rarely be your sole source of retirement income. It’s designed to replace only a portion of pre-retirement earnings. Therefore, your decision to claim early should be coordinated with other retirement assets, such as 401(k)s, IRAs, pensions, and personal savings. For instance, some individuals choose to draw down their investment portfolios in their early 60s to allow their Social Security benefits to grow by delaying their claim. Others might claim Social Security early to allow their investments more time to grow, or to bridge the gap until another pension or retirement fund becomes available. A holistic view of all your income streams is essential for making an informed decision.

The Break-Even Point Analysis

The concept of a “break-even point” is a useful tool when deciding when to claim Social Security. This analysis estimates the age at which the cumulative total of your higher, delayed benefits would surpass the cumulative total of your reduced, early benefits. For example, if you claim at 62, you receive more money earlier. If you wait until 67, you receive less money initially but a higher monthly amount. The break-even point is typically somewhere in your late 70s or early 80s. If you expect to live past this age, delaying benefits usually results in a higher total lifetime payout. However, this analysis is based on averages and does not account for individual health, spending habits, or unforeseen circumstances, making it a guideline rather than a definitive answer.

Tools and Resources for Planning Your Social Security

Making an informed decision about Social Security benefits requires access to accurate information and personalized estimates. Fortunately, the Social Security Administration provides a wealth of resources to help you plan effectively.

The Social Security Administration’s Online Account

One of the most valuable resources is your personal “my Social Security” online account. Creating an account allows you to:

- View your complete earnings record.

- See estimates of your future benefits at different claiming ages (62, your FRA, and 70).

- Review your Social Security Statement.

- Manage your benefits once you start receiving them.

This account is an indispensable tool for understanding your personalized benefit estimates, which are far more accurate than generic calculations, as they are based on your actual earnings history.

Benefit Calculators and Estimators

Beyond your personal online account, the SSA website offers various benefit calculators and estimators. These tools can help you:

- Estimate your benefits under different scenarios (e.g., if you stop working early, if your earnings change).

- Calculate potential spousal or survivor benefits.

- Understand the impact of the earnings limit.

Third-party financial planning websites and software also offer Social Security calculators, often providing more detailed “what-if” scenarios and comparisons, though it’s always wise to cross-reference with official SSA information.

Seeking Professional Financial Advice

While online tools provide excellent starting points, Social Security claiming strategies can be highly complex, especially for couples, those with varied work histories, or individuals with significant other assets. Consulting with a qualified financial advisor who specializes in retirement planning can be invaluable. A professional can help you:

- Analyze your entire financial picture, not just Social Security.

- Develop a customized claiming strategy that aligns with your specific goals, health status, and other income sources.

- Understand intricate rules regarding spousal, divorced spousal, and survivor benefits.

- Minimize taxes on your Social Security benefits.

Their expertise can help ensure you make the most advantageous decision for your long-term financial security.

In conclusion, while there isn’t a universally fixed “minimum” Social Security payment at age 62 in the traditional sense, understanding the factors that influence benefit amounts—primarily your lifetime earnings, the permanent reduction for early claiming, and the very specific criteria for the Special Minimum Benefit—is crucial. For most individuals, the “minimum” they will receive at age 62 will be their calculated Primary Insurance Amount (PIA), reduced by approximately 30% due to claiming early. By leveraging available resources and seeking professional guidance, individuals can make informed decisions that optimize their Social Security income and contribute to a more secure retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.