Understanding the average cost of health insurance is a crucial, yet often complex, endeavor for individuals, families, and businesses alike. In a world where healthcare expenses continue to climb, securing adequate coverage without breaking the bank is a top financial priority. However, arriving at a single, definitive “average” figure is challenging due to the myriad of factors that influence premiums, deductibles, and out-of-pocket costs. This article will delve into the intricacies of health insurance expenses, breaking down what you can expect to pay, what drives these costs, and strategies to manage them effectively, all within the context of sound personal and business financial planning.

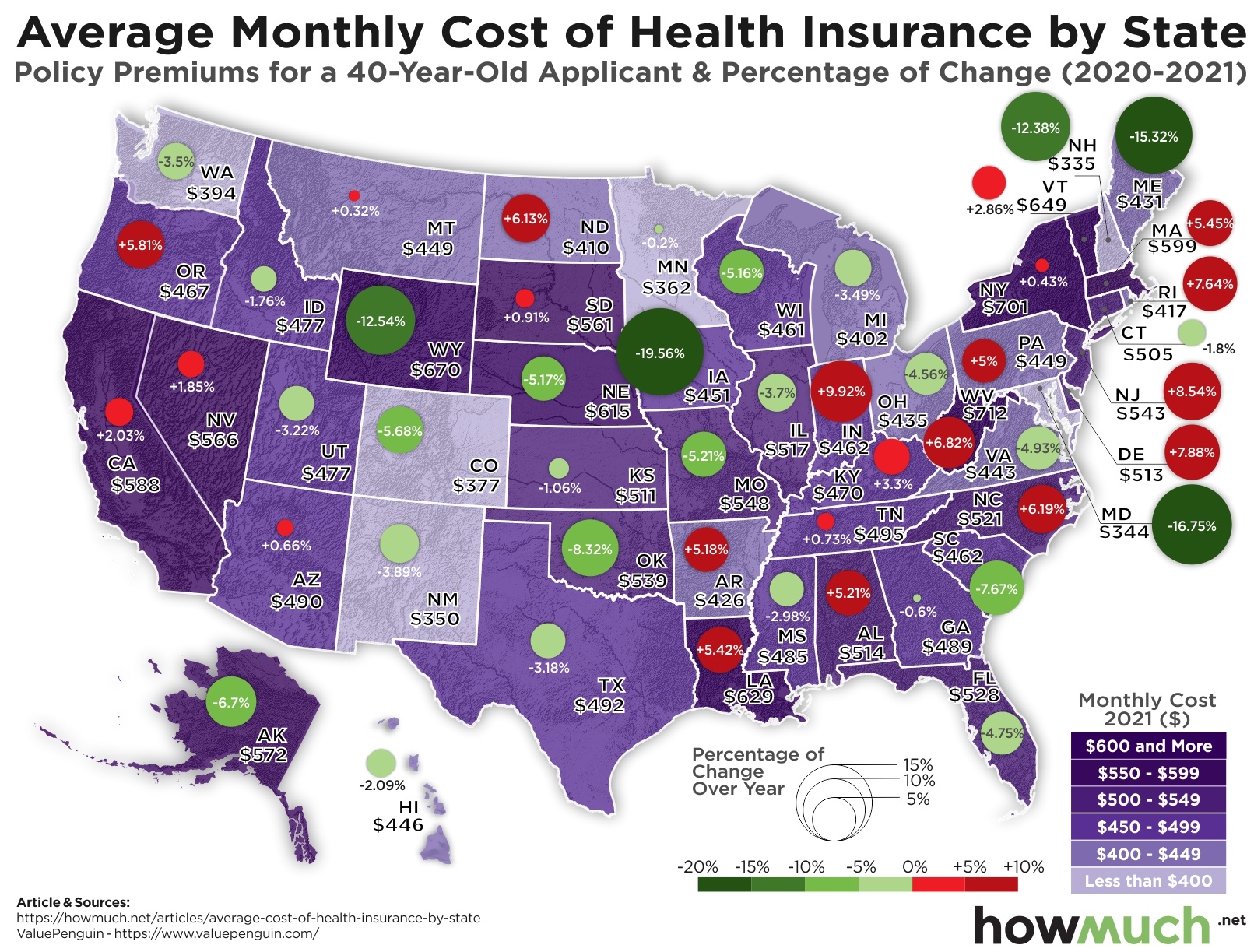

The cost of health insurance is not static; it fluctuates based on a complex interplay of personal demographics, geographic location, chosen plan type, and prevailing market conditions. While national averages can offer a starting point, they rarely tell the full story for any given individual. For instance, the average monthly premium for individual health insurance plans can range from a few hundred dollars to well over a thousand, depending on whether you’re purchasing through an employer, a state marketplace, or other avenues. For families, these costs multiply, often running into several hundred or even thousands of dollars per month. Understanding these nuances is the first step toward making informed financial decisions about your healthcare coverage.

Understanding the Landscape of Health Insurance Costs

Navigating the health insurance landscape requires more than just knowing a national average. It demands an appreciation for the variables that sculpt individual and family premiums. From the type of plan you select to where you reside, numerous elements converge to determine your final cost.

The Complexity Behind Averages

When we talk about an “average” cost, it’s essential to recognize that this figure is a statistical representation that can mask significant variations. For example, a national average might combine data from states with very low costs and those with extremely high costs, rendering it less useful for someone in a specific locality. Furthermore, averages often don’t differentiate between plans with vastly different levels of coverage, deductibles, or out-of-pocket maximums. A low-premium plan might have a very high deductible, shifting more of the initial healthcare cost burden onto the insured. Conversely, a high-premium plan might offer comprehensive coverage with minimal out-of-pocket expenses. Therefore, while averages provide a useful benchmark, they should always be interpreted with a critical eye, considering the context of your personal situation and financial capacity.

Key Factors Influencing Premiums

Several pivotal factors directly impact how much you pay for health insurance premiums. Understanding these drivers is crucial for predicting and managing your costs:

- Age: Generally, older individuals pay higher premiums. Health insurance companies are permitted to charge older adults up to three times more than younger adults for the same plan, under the Affordable Care Act (ACA) guidelines.

- Location: Healthcare costs and market competition vary significantly by state and even by county. Urban areas with more hospitals and specialists might have different pricing structures compared to rural areas. State regulations also play a significant role in what insurers can charge.

- Smoking Status: Smokers can be charged up to 50% more for health insurance premiums in many states, reflecting the increased health risks associated with tobacco use.

- Plan Type: The kind of plan you choose (e.g., HMO, PPO, EPO, POS, HDHP) significantly affects the premium. Plans with broader networks and more flexibility (like PPOs) typically cost more than those with restricted networks (like HMOs).

- Coverage Level (Metal Tiers): Under the ACA marketplace, plans are categorized into metal tiers (Bronze, Silver, Gold, Platinum) based on how costs are split between the insurer and the insured. Bronze plans have the lowest premiums but cover about 60% of costs, leaving 40% to the insured. Platinum plans cover about 90% of costs but have the highest premiums. Silver plans, often a popular choice, cover 70% of costs and are the only plans eligible for cost-sharing reductions.

- Number of People Covered: Adding spouses or dependents to a policy naturally increases the premium. Family plans will always be more expensive than individual plans.

Navigating the Individual vs. Group Market

The avenue through which you acquire health insurance also profoundly impacts its cost and structure. The two primary markets are the individual market (often through state and federal marketplaces under the ACA) and the group market (typically employer-sponsored plans). Employer-sponsored plans often benefit from group purchasing power, leading to lower premiums for employees and their families, with employers usually subsidizing a significant portion of the cost. These plans also tend to have a wider range of options and sometimes better benefits. In contrast, individuals purchasing plans on the marketplace face the full premium cost, though many qualify for subsidies that can significantly reduce their out-of-pocket expenses. Self-employed individuals, those working for companies without benefits, or those whose income makes marketplace subsidies less attractive may explore direct purchase from insurers or short-term plans.

Deconstructing Health Insurance Costs for Individuals and Families

The path to obtaining health insurance dictates not only the cost but also the types of plans available and the level of financial assistance one might receive. Understanding these different avenues is critical for both individual financial planning and business finance perspectives.

Individual Marketplace Plans (ACA)

For individuals and families who do not receive health insurance through an employer, the Affordable Care Act (ACA) marketplaces (HealthCare.gov or state-run exchanges) are the primary source of coverage. In 2023, the average unsubsidized individual premium for an ACA plan was around $560 per month. However, this number drastically changes when subsidies are applied. Most people who enroll through the marketplace qualify for premium tax credits, which can significantly reduce their monthly payments. Eligibility for these credits is based on income relative to the federal poverty level. For instance, a substantial portion of enrollees pay less than $100 per month after subsidies. The metal tiers (Bronze, Silver, Gold, Platinum) represent different cost-sharing structures, with Bronze plans offering the lowest premiums but highest deductibles, and Platinum plans offering the highest premiums with the lowest out-of-pocket costs. Silver plans are particularly notable because they are the only tier eligible for Cost-Sharing Reductions (CSRs), which lower deductibles, copayments, and coinsurance for eligible low-income individuals and families.

Employer-Sponsored Plans

Employer-sponsored health insurance remains the most common way for Americans to get coverage. These plans often provide more comprehensive benefits at a lower out-of-pocket cost for employees compared to individual marketplace plans, primarily because employers typically cover a significant portion of the premium. In 2023, the average annual premium for employer-sponsored health insurance was approximately $7,911 for single coverage and $22,463 for family coverage. Employers covered, on average, 83% of the premium for single coverage and 72% for family coverage. This means an average employee paid around $1,327 annually for single coverage and $6,373 for family coverage, or roughly $110 and $531 per month, respectively. The specific cost to an employee will vary widely based on the employer’s contribution strategy, the plan chosen, and the size and industry of the company. These plans are a major component of employee compensation and a significant expense for businesses.

Short-Term Health Insurance and Other Alternatives

Beyond the traditional ACA marketplace and employer-sponsored plans, several alternative options exist, each with its own cost structure and limitations:

- Short-Term Health Insurance: These plans are designed for temporary coverage (typically 3 months to less than a year, though some states allow longer) and are often much cheaper than ACA-compliant plans. However, they do not have to cover essential health benefits, can deny coverage based on pre-existing conditions, and usually have very high deductibles and limits on total payouts. They are best suited for individuals in transition, like those between jobs or waiting for open enrollment.

- Medicaid: For low-income individuals and families, Medicaid provides free or low-cost health coverage. Eligibility is based on income and family size, varying by state.

- Medicare: Primarily for individuals aged 65 or older, and certain younger people with disabilities. Medicare Part B (medical insurance) has a standard monthly premium, while other parts (A, C, D) have varying costs.

- Health Care Sharing Ministries: These are not insurance but involve members sharing healthcare costs based on religious or ethical beliefs. They are generally much cheaper but offer no guarantee of payment and typically do not cover pre-existing conditions.

- Direct Purchase from Insurers: Some individuals might purchase plans directly from insurance companies outside the marketplace. These plans are often ACA-compliant but generally don’t qualify for subsidies.

Beyond Premiums: The True Cost of Healthcare

While premiums are the most visible cost of health insurance, they represent only a part of the overall financial burden. To truly understand the cost of healthcare, it’s essential to consider the out-of-pocket expenses that come into play when you actually use your insurance.

Deductibles, Copayments, and Coinsurance

These three terms are critical to understanding your financial responsibility:

- Deductible: This is the amount you must pay out of your own pocket for covered healthcare services before your insurance plan starts to pay. For example, if you have a $5,000 deductible, you are responsible for the first $5,000 of covered medical expenses each year. Many plans, especially Bronze and Silver tiers, have high deductibles, meaning you could be paying significant amounts before your insurance kicks in for most services.

- Copayment (Copay): A fixed amount you pay for a covered healthcare service after you’ve paid your deductible. For instance, you might have a $30 copay for a doctor’s visit or a $10 copay for a prescription drug. Copays do not usually count towards your deductible but do count towards your out-of-pocket maximum.

- Coinsurance: This is your share of the cost of a covered healthcare service, calculated as a percentage of the allowed amount for the service. For example, if your plan has an 80/20 coinsurance, it means the plan pays 80% and you pay 20% after your deductible has been met. If a service costs $1,000 and you’ve met your deductible, you’d pay $200 (20%).

Out-of-Pocket Maximums: Your Financial Safety Net

The out-of-pocket maximum is a crucial protection built into most health insurance plans. This is the most you will have to pay for covered services in a plan year. Once you reach this limit, your health insurance plan pays 100% of the cost of covered benefits for the remainder of the year. This maximum includes deductibles, copayments, and coinsurance payments. For 2024, the out-of-pocket maximum for ACA-compliant plans is $9,450 for individuals and $18,900 for families. Understanding your out-of-pocket maximum provides peace of mind, knowing there’s a cap on your annual healthcare expenses, regardless of how extensive your medical needs become. It’s a key factor to consider when evaluating the financial risk associated with different plans.

The Value of Preventative Care

It’s easy to focus solely on the costs associated with illness, but preventative care plays a significant role in managing long-term healthcare expenses. The ACA mandates that most health insurance plans cover a range of preventative services—such as annual physicals, screenings for various diseases (e.g., blood pressure, cholesterol, cancer), and immunizations—at no cost to the insured, even before the deductible is met. Utilizing these free services can help detect potential health issues early, often before they become serious and costly to treat. Investing time in preventative care can lead to better health outcomes and ultimately reduce your overall healthcare expenditures over time. This aspect highlights a vital financial strategy: proactive health management as a form of cost control.

Strategies for Managing and Reducing Health Insurance Expenses

Effectively managing health insurance costs is a core component of sound personal and business financial planning. With a strategic approach, individuals and families can find quality coverage that aligns with their budget.

Leveraging Subsidies and Tax Credits

For those purchasing insurance through the ACA marketplace, understanding and leveraging available financial assistance is paramount. Premium tax credits can significantly lower monthly premiums, while cost-sharing reductions (available with Silver plans) reduce out-of-pocket expenses like deductibles and copays. Eligibility for these subsidies is based on income relative to the Federal Poverty Level (FPL). Even those with moderate incomes may qualify for some level of assistance, especially with recent expansions under the American Rescue Plan Act. It’s crucial to accurately report income and household size when applying for coverage to ensure you receive all the financial help you’re entitled to.

Choosing the Right Plan Type (HMO, PPO, EPO, POS)

The structure of your health plan heavily influences both your cost and your access to care:

- HMO (Health Maintenance Organization): Generally lower premiums, but require you to choose a primary care physician (PCP) within the network who then refers you to specialists. Out-of-network care is usually not covered, except in emergencies.

- PPO (Preferred Provider Organization): Higher premiums but offer more flexibility. You don’t need a referral to see a specialist and can see out-of-network providers for a higher cost.

- EPO (Exclusive Provider Organization): Similar to an HMO in that you must use doctors and hospitals within the network, but you typically don’t need a referral to see specialists within that network.

- POS (Point of Service): A hybrid of HMO and PPO, allowing you to use out-of-network providers for certain services, usually with a referral from your PCP.

Selecting the right plan involves balancing cost with flexibility and your anticipated healthcare needs. If you rarely visit specialists and prefer lower premiums, an HMO might be suitable. If you value choice and don’t mind paying more, a PPO could be better.

Exploring High-Deductible Health Plans (HDHPs) with HSAs

High-Deductible Health Plans (HDHPs) typically have lower monthly premiums but higher deductibles. They become particularly attractive when paired with a Health Savings Account (HSA). An HSA is a tax-advantaged savings account that can be used for qualified medical expenses. Contributions to an HSA are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free. This “triple tax advantage” makes HSAs a powerful tool for both managing current healthcare costs and saving for future medical needs, including retirement healthcare expenses. HDHPs with HSAs are often a good choice for healthy individuals who don’t anticipate frequent medical care but want protection against catastrophic events, or for those who want a tax-advantaged way to save for healthcare.

Regular Review and Comparison Shopping

Health insurance costs and available plans change annually. It is a financially savvy move to review your coverage options every year during the Open Enrollment Period. This involves comparing your current plan with other offerings on the marketplace or through your employer. Factors to consider include:

- Premium changes: Have your current plan’s premiums increased significantly?

- Deductible and out-of-pocket maximums: Are there plans with better cost-sharing structures?

- Network changes: Are your preferred doctors and hospitals still in-network?

- Medication coverage: Are your prescription drugs covered, and at what cost?

- Anticipated health needs: Do you expect more medical care in the coming year that might make a higher-premium, lower-deductible plan more cost-effective?

Comparison shopping can reveal new plans that better fit your budget and healthcare requirements, potentially saving you hundreds or even thousands of dollars annually.

The Future of Health Insurance Costs and Your Financial Well-being

The landscape of health insurance costs is dynamic, influenced by legislative changes, economic conditions, and advancements in medical technology. Staying informed and proactively planning are essential for maintaining financial well-being in the face of evolving healthcare expenses.

Policy Changes and Market Dynamics

Government policies and market trends continuously shape health insurance costs. Changes to the Affordable Care Act, state-level regulations, and federal subsidy programs can all impact premiums and the accessibility of coverage. For example, recent enhancements to ACA subsidies have made marketplace plans more affordable for many. Broader economic factors, such as inflation and the cost of prescription drugs, also exert upward pressure on premiums. Furthermore, the consolidation of healthcare providers and insurers can affect competition, which in turn influences pricing. Businesses must adapt their benefits strategies to these changes, while individuals need to understand how these macro shifts translate to their personal financial outlook.

The Importance of Proactive Financial Planning

Given the inherent volatility and complexity of health insurance costs, proactive financial planning is not merely advisable but critical. This includes budgeting for potential out-of-pocket expenses beyond premiums, building an emergency fund to cover unexpected medical bills, and considering tax-advantaged savings vehicles like HSAs. For businesses, this means strategically allocating resources for employee benefits, understanding the tax implications of different plan offerings, and continuously evaluating cost-effective solutions to attract and retain talent. Ultimately, understanding the average cost of health insurance is just the beginning; a comprehensive approach to managing these expenses is key to securing both your physical and financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.