The question “how much money is in the Social Security fund?” is one that surfaces frequently, reflecting a widespread public interest in the stability and future of one of America’s most vital social programs. For many, Social Security represents a cornerstone of their financial security in retirement, disability, or as survivors. However, the answer is more nuanced than a simple balance sheet figure. Understanding the “fund” requires delving into the mechanics of how Social Security is structured, funded, and managed. It’s not a vault overflowing with cash, but a sophisticated system of trust funds holding special U.S. government bonds, designed to provide a safety net for millions of Americans. This article aims to demystify the Social Security Trust Funds, explore their current status, and discuss the factors influencing their long-term sustainability, all viewed through the lens of personal and national financial prudence.

![]()

Demystifying the Social Security Trust Funds

To truly grasp the concept of “money in the Social Security fund,” it’s crucial to understand that Social Security operates through specific accounting mechanisms known as Trust Funds, rather than a single, monolithic bank account. These funds are distinct and serve different purposes within the broader Social Security program.

What Are the Trust Funds? (OASI and DI)

Social Security is composed of two primary trust funds:

- The Old-Age and Survivors Insurance (OASI) Trust Fund: This is the larger of the two, responsible for paying retirement benefits to eligible individuals and survivor benefits to the spouses, children, and parents of deceased workers. The vast majority of Social Security beneficiaries receive payments from the OASI fund.

- The Disability Insurance (DI) Trust Fund: This fund provides benefits to workers who become disabled and are unable to work, as well as to their dependents. While smaller than the OASI fund, it plays an equally critical role in providing financial stability for those facing unexpected health challenges.

It’s important to clarify a common misconception: these aren’t literal cash reserves sitting idle in a bank. Instead, when Social Security collects more in payroll taxes than it pays out in benefits, the surplus is invested in special-issue U.S. Treasury bonds. These bonds are backed by the full faith and credit of the U.S. government, making them an extremely secure investment. The Trust Funds, therefore, primarily consist of these interest-bearing government securities, which represent an obligation of the U.S. Treasury to repay the principal and interest to the Social Security program when needed. This arrangement ensures that the funds are not simply spent, but are instead generating income for future benefit payments.

The Source of Funds: Where Does the Money Come From?

The financial lifeblood of the Social Security Trust Funds flows primarily from three main sources:

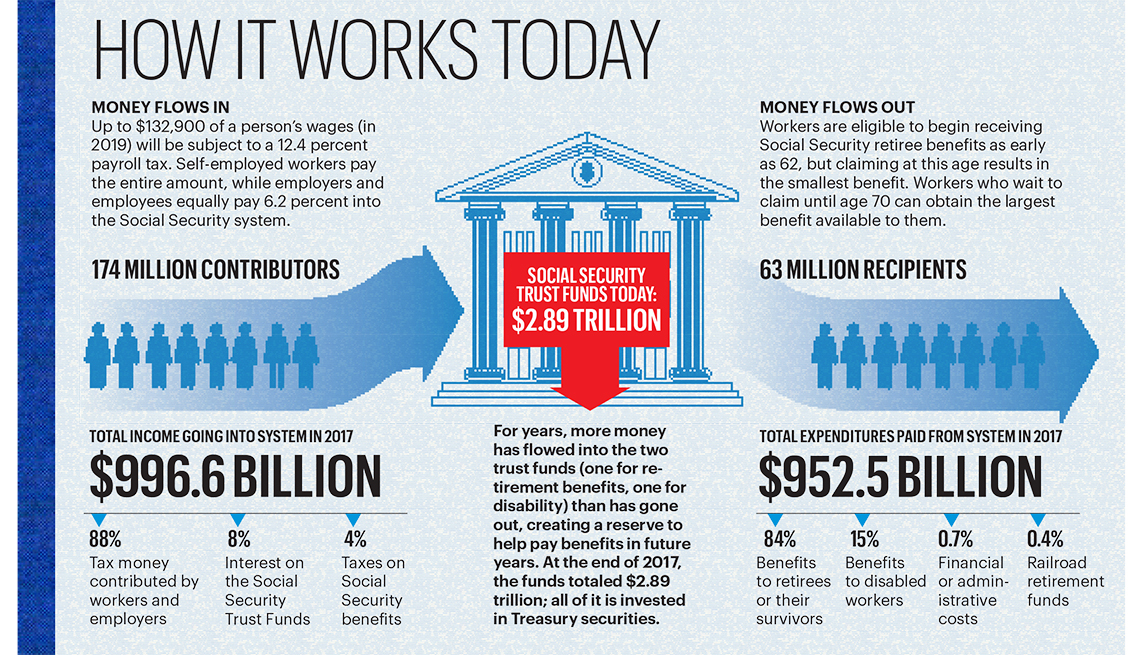

- Payroll Taxes (FICA and SECA): This is the largest and most significant source of revenue. Most employees, employers, and self-employed individuals contribute a portion of their earnings to Social Security through dedicated payroll taxes. For employees, this is known as the Federal Insurance Contributions Act (FICA) tax, where both the employee and employer pay 6.2% each (for a total of 12.4%) on earnings up to a certain annual limit (the “taxable maximum,” which adjusts annually). Self-employed individuals pay both halves of this tax under the Self-Employment Contributions Act (SECA). These taxes are specifically earmarked for Social Security and Medicare.

- Taxation of Social Security Benefits: A portion of Social Security benefits may be subject to federal income tax for individuals whose combined income exceeds certain thresholds. The revenue generated from this taxation is also deposited into the Social Security Trust Funds.

- Interest Earned on Investments: As mentioned, the surplus payroll taxes are invested in special-issue Treasury bonds. The interest earned on these bonds contributes significantly to the Trust Funds’ assets, ensuring their growth and helping to cover benefit payments, especially during periods when tax income might not fully cover expenditures.

These interconnected revenue streams ensure a continuous flow of funds into the Social Security system, enabling it to meet its ongoing obligations to millions of beneficiaries across the nation.

The Current State of the Trust Funds: A Snapshot

Understanding the “how” and “where from” leads us to the critical question of “how much” and what that means for the present and future. The financial status of the Social Security Trust Funds is regularly assessed and reported, offering transparency into their health.

Latest Reported Balances

As of the most recent annual Trustees’ Report (typically released in late spring/early summer), the Social Security Trust Funds hold a substantial amount in assets. While specific real-time figures fluctuate daily, the combined assets of the OASI and DI Trust Funds are consistently in the trillions of dollars. For instance, recent reports have shown combined trust fund assets exceeding $2.8 trillion. This figure represents the accumulated surplus of payroll taxes and interest earned over decades, invested in the aforementioned special U.S. Treasury securities.

It’s crucial not to mistake this multi-trillion-dollar sum for a mere checking account balance. These are not liquid cash but rather government bonds that the U.S. Treasury owes to the Social Security program. When Social Security needs to pay benefits, it redeems these bonds, and the Treasury pays back the principal and interest, funding those payments from general government revenues or by issuing new debt to other investors. Therefore, the “money” in the fund is a legal claim on the U.S. government, backed by its taxing authority and borrowing power. The sheer magnitude of these assets underscores the program’s significant financial foundation.

Understanding the “Investment”

The investment strategy of the Social Security Trust Funds is unique and highly secure by design. Unlike private pension funds or individual investment accounts that might invest in stocks, corporate bonds, or real estate, the Trust Funds are legally mandated to invest exclusively in U.S. government securities.

- Security and Stability: This policy prioritizes absolute security and stability over potentially higher, but riskier, returns. Because the bonds are backed by the full faith and credit of the U.S. government, they are considered virtually risk-free in terms of default. This is paramount for a program that millions depend on for their basic financial survival.

- Interest Rates: The interest rates on these special-issue Treasury bonds are determined by market rates for similar government securities. While these rates are generally modest compared to some private sector investments, they consistently generate billions of dollars in interest income annually, contributing significantly to the Trust Funds’ growth.

- Distinction from Private Markets: It’s vital to differentiate this from investing in the private stock market. Social Security is explicitly prohibited from investing in equities, a measure designed to shield it from market volatility and political influence over corporate America. This approach ensures that the principal of the Trust Funds is always safe, even if it means foregoing potentially larger returns during bull markets. The “investment” is thus a mechanism to earn income on surpluses while guaranteeing the safety and availability of funds when needed to pay promised benefits.

The Mechanics of Outflows: Where Does the Money Go?

While understanding the inflows and current holdings is essential, an equally important aspect of the Social Security system is comprehending how money flows out. The vast majority of expenditures directly support beneficiaries, fulfilling the program’s core mission.

Benefit Payments

The primary purpose of the Social Security Trust Funds is to pay benefits to eligible individuals. These payments constitute the overwhelming majority of the program’s annual outflows and are categorized primarily as:

- Retirement Benefits: These are paid to retired workers who have met the eligibility criteria based on their work history and contributions. This group represents the largest segment of Social Security beneficiaries. The benefit amount is calculated based on a worker’s average indexed monthly earnings (AIME) over their working life.

- Survivors’ Benefits: When a worker dies, certain family members—including surviving spouses, minor children, and dependent parents—may be eligible to receive benefits. These payments provide crucial financial support to families facing the loss of a primary wage earner.

- Disability Benefits: Workers who become severely disabled and are unable to engage in substantial gainful activity may qualify for disability benefits. These benefits are also extended to their dependents. The DI Trust Fund specifically covers these payments, offering a critical safety net for individuals whose ability to earn a living has been severely compromised by illness or injury.

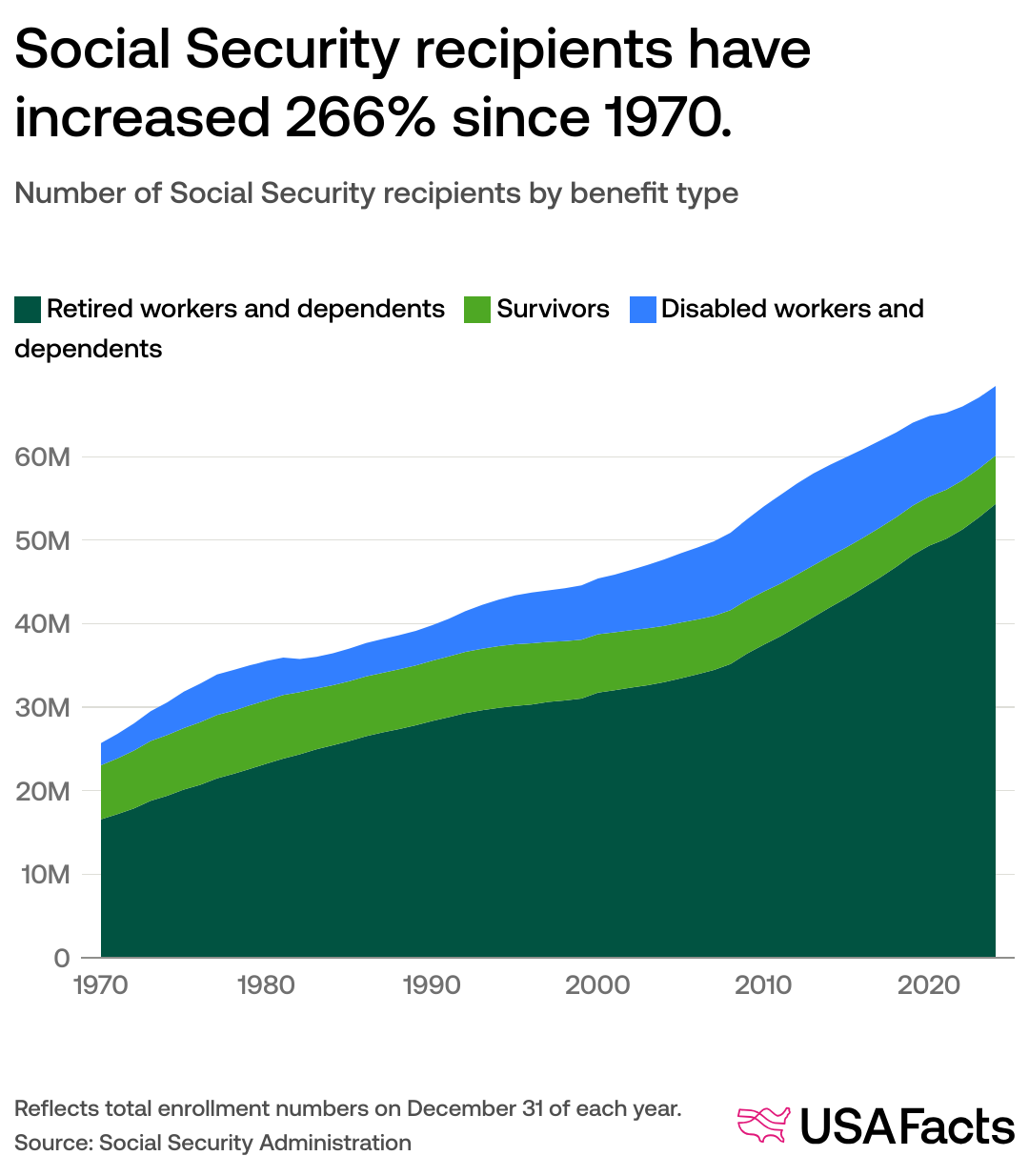

Collectively, these benefits are distributed monthly to tens of millions of Americans, making Social Security an indispensable source of income for retirees, disabled individuals, and surviving families across all socioeconomic strata. The total amount paid out annually in benefits runs into the hundreds of billions of dollars, reflecting the enormous scale and impact of the program.

Administrative Costs

Compared to the massive sums distributed in benefits, the administrative costs of running the Social Security Administration (SSA) are remarkably low.

- Efficiency: The SSA is widely recognized as one of the most efficient government agencies, with administrative expenses typically accounting for less than 1% of total expenditures. This means that over 99 cents of every dollar collected for Social Security goes directly to pay benefits. This efficiency is a testament to the streamlined processes and dedicated workforce of the SSA.

- What Costs Are Included?: Administrative costs cover a range of essential functions, including:

- Processing benefit applications and appeals.

- Maintaining earnings records for millions of workers.

- Providing information and services to the public.

- Detecting and preventing fraud.

- Operating and maintaining the necessary technological infrastructure.

- Staff salaries and operational overhead for offices nationwide.

The low administrative overhead underscores the program’s commitment to maximizing the funds available for beneficiaries, ensuring that contributions are primarily directed towards their intended purpose.

Future Projections and Sustainability Concerns

While the Social Security Trust Funds currently hold trillions of dollars in assets, long-term projections highlight future challenges that policymakers and the public must address to ensure the program’s ongoing solvency.

The “Insolvency” Debate: Understanding the Projections

The annual Trustees’ Report regularly projects the financial outlook for Social Security decades into the future. These projections often indicate that, under current law, the combined Trust Funds are expected to be able to pay 100% of promised benefits for a number of years (e.g., into the mid-2030s). However, after that point, the report projects that the funds will only be able to pay a reduced percentage of scheduled benefits (e.g., around 80%).

It’s crucial to understand what “insolvency” in this context does not mean:

- It does not mean Social Security will run out of money entirely. Even after the projected depletion date, the program would still be able to pay a significant portion of benefits (e.g., 75-80%) because payroll taxes would continue to flow in.

- It means the program would be unable to pay 100% of scheduled benefits under current law.

The primary drivers behind these long-term projections are demographic shifts:

- Aging Population: The large Baby Boomer generation is moving into retirement, increasing the number of beneficiaries relative to the number of contributing workers.

- Lower Birth Rates: Fewer births mean a shrinking proportion of young workers entering the workforce to support future retirees.

- Increased Longevity: People are living longer, meaning they collect benefits for more years.

These factors combine to alter the worker-to-beneficiary ratio, putting increasing strain on the system’s ability to pay full benefits without adjustments.

Potential Solutions and Policy Debates

Despite the projected long-term shortfall, economists and policymakers generally agree that Social Security’s challenges are manageable and require policy adjustments, not a complete overhaul or abandonment. Numerous solutions have been proposed and debated, falling broadly into two categories: increasing revenue or decreasing expenditures.

Proposals to Increase Revenue:

- Raising the Payroll Tax Rate: A modest increase in the FICA/SECA tax rate (e.g., from 6.2% to 7.2%) could significantly extend the Trust Funds’ solvency.

- Adjusting the Taxable Earnings Cap: Currently, earnings above a certain threshold (e.g., $168,600 in 2024) are not subject to Social Security taxes. Raising or eliminating this cap would subject more high earners’ income to the tax, dramatically increasing revenue.

Proposals to Decrease Expenditures:

- Raising the Full Retirement Age (FRA): Gradually increasing the age at which individuals can claim full benefits (currently 67 for those born in 1960 or later) would reduce the total number of years benefits are paid.

- Modifying the Cost-of-Living Adjustment (COLA) Formula: Changing how annual benefit increases are calculated, for instance, by adopting a “chained CPI” which reflects changes in consumer spending patterns, could lead to slightly smaller annual increases.

- Means-Testing Benefits: Introducing an income threshold above which individuals receive reduced or no Social Security benefits, though this is often controversial for altering the universal nature of the program.

Other suggestions include investing a portion of the Trust Funds in private equities (though this carries higher risk) or supplementing the funds with general Treasury revenues. Each of these solutions has pros and cons, and finding a politically viable combination will require careful consideration and bipartisan cooperation. The challenges are real, but the program’s fundamental structure remains robust, and with thoughtful policy choices, its future can be secured.

Conclusion

The question “how much money is in the Social Security fund?” uncovers a complex and crucial aspect of America’s financial landscape. It reveals not a simple cash pile, but a sophisticated system of trust funds holding trillions of dollars in special U.S. government bonds, funded by dedicated payroll taxes, taxation of benefits, and interest earnings. These funds are the bedrock of a program that pays retirement, disability, and survivors’ benefits to tens of millions of Americans, doing so with remarkable administrative efficiency.

While the current balances are substantial, long-term projections indicate that demographic shifts—an aging population, lower birth rates, and increased longevity—will eventually necessitate adjustments to ensure the program’s ability to pay 100% of scheduled benefits. However, the projected shortfalls do not signify collapse, but rather a need for measured policy interventions. Solutions such as adjusting the payroll tax rate, raising the taxable earnings cap, increasing the full retirement age, or modifying benefit calculations are all within reach.

Ultimately, Social Security remains a cornerstone of financial security for American families. Understanding its financial mechanics, current status, and future challenges empowers individuals to engage in informed discussions about its future. With continued attention and responsible policy decisions, the Social Security Trust Funds can continue to serve as a vital safety net for generations to come, reinforcing its indispensable role in the nation’s financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.