Understanding your income is the bedrock of sound financial planning. For many, the journey into the workforce begins with an hourly wage, and one of the most common questions that arises is how that hourly rate translates into an annual salary. Specifically, if you earn $16 an hour, what does that mean for your yearly financial outlook? This article will break down the calculation, delve into the critical difference between gross and net income, explore budgeting strategies for this income level, and offer pathways to enhance your financial well-being.

The Basic Calculation: Understanding Your Gross Annual Income

At its core, converting an hourly wage to an annual salary is a straightforward multiplication problem. However, it’s crucial to understand the assumptions involved to arrive at an accurate figure. This initial calculation yields your gross annual income – the amount you earn before any deductions are taken out.

Standard Work Week Assumptions

The most common assumption in calculating an annual salary from an hourly wage is a standard full-time work schedule. In most developed countries, a full-time work week is considered to be 40 hours. This forms the basis for converting hourly pay into a weekly, and then yearly, figure. While some industries or roles might have slightly different standard work weeks (e.g., 35 or 37.5 hours), 40 hours remains the widely accepted benchmark for full-time employment. Similarly, a standard working year typically comprises 52 weeks. Even with paid holidays or vacation time, employers often calculate annual salaries based on 52 weeks of work.

The Simple Math Explained

With these assumptions in place, the calculation for your gross annual income becomes quite simple:

-

Hourly Rate x Hours per Week = Weekly Pay

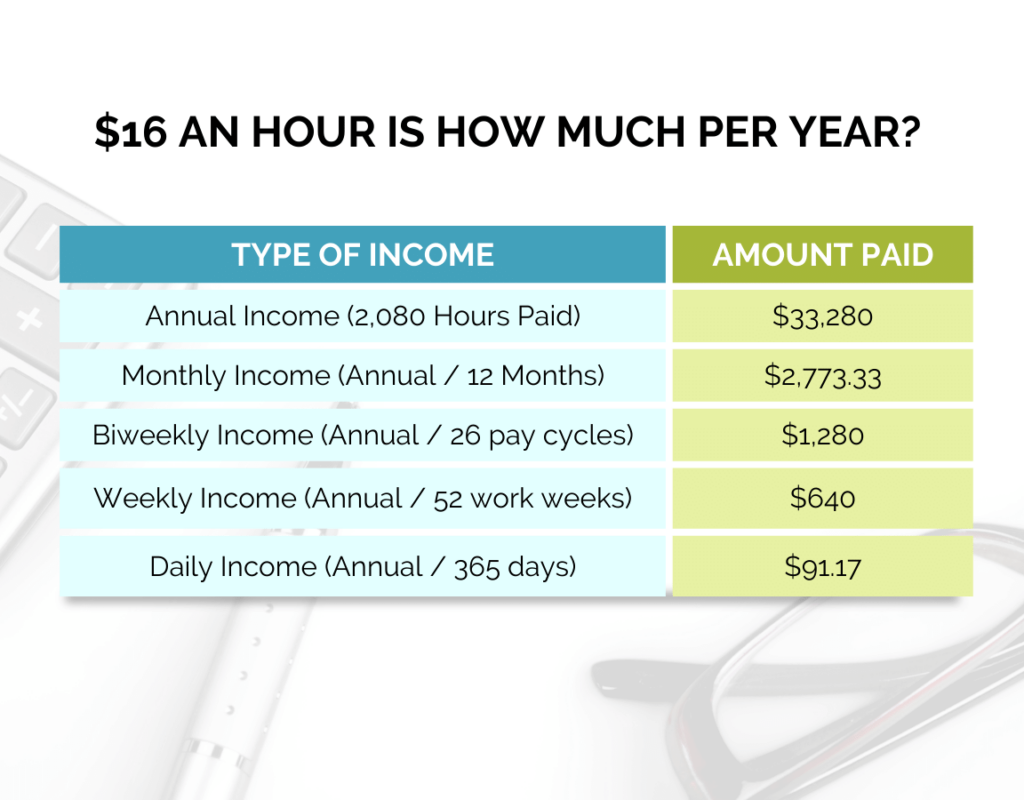

- $16/hour x 40 hours/week = $640/week

-

Weekly Pay x Weeks per Year = Annual Gross Income

- $640/week x 52 weeks/year = $33,280/year

So, a person earning $16 an hour and working a standard 40-hour week for 52 weeks a year would have a gross annual income of $33,280.

Variations: Part-Time vs. Full-Time & Overtime Considerations

It’s vital to recognize that this calculation is a baseline. Your actual gross annual income can vary significantly based on your employment status and work patterns:

- Part-Time Employment: If you work less than 40 hours a week, your annual income will be proportionally lower. For instance, if you work 20 hours a week at $16 an hour:

- $16/hour x 20 hours/week = $320/week

- $320/week x 52 weeks/year = $16,640/year

- Overtime: Many hourly positions offer the opportunity for overtime pay, typically at 1.5 times the regular hourly rate (time and a half) for hours worked beyond 40 in a week. If you consistently work overtime, your actual annual income would be higher. For example, if you worked 5 hours of overtime ($24/hour) each week:

- Regular weekly pay: $640

- Overtime weekly pay: 5 hours x ($16 * 1.5) = 5 hours x $24 = $120

- Total weekly pay: $640 + $120 = $760

- Annual gross income with overtime: $760/week x 52 weeks/year = $39,520/year

- Unpaid Leave or Seasonal Work: If your job involves periods of unpaid leave or is seasonal, resulting in fewer than 52 paid weeks per year, your annual income would be reduced accordingly.

Always calculate your gross income based on your actual, anticipated hours and any consistent overtime, rather than just the standard assumptions, for a more precise understanding.

Beyond the Basics: Gross vs. Net Income

While knowing your gross annual income is a critical starting point, it’s equally important – if not more so – to understand your net income. Your net income, often referred to as your “take-home pay,” is the amount of money you actually receive after all deductions have been made from your gross pay. This is the figure you use for budgeting and daily expenses.

Essential Deductions: Taxes (Federal, State, Local)

The largest portion of deductions typically comes from taxes. These can include:

- Federal Income Tax: This is levied by the national government and is progressive, meaning higher earners pay a larger percentage. The exact amount depends on your total income, filing status (single, married filing jointly, etc.), and the number of allowances claimed on your W-4 form.

- State Income Tax: Many states also impose an income tax, which varies widely from state to state (some states have no state income tax at all).

- Local Income Tax: In some cities or counties, you might also be subject to local income taxes.

- FICA Taxes (Social Security and Medicare): These are mandatory federal payroll taxes that fund Social Security and Medicare programs. Social Security tax is typically 6.2% of your gross wages (up to an annual limit), and Medicare tax is 1.45% of all your wages, with no income limit. Your employer also pays a matching amount.

These taxes can significantly reduce your take-home pay. For someone earning $33,280 annually, taxes could easily account for 15-25% or more of your gross income, depending on your location and specific tax situation.

Pre-Tax Deductions: Health Insurance, Retirement Contributions

Beyond taxes, several other deductions can come out of your paycheck. Some of these are “pre-tax,” meaning they are deducted from your gross income before taxes are calculated, which can lower your taxable income and, consequently, your overall tax liability.

- Health Insurance Premiums: If your employer offers health insurance, your share of the premium is often deducted from your paycheck. Many employer-sponsored health plans offer pre-tax deductions.

- Retirement Contributions (401k, 403b, etc.): If you contribute to an employer-sponsored retirement plan like a 401(k) or 403(b), these contributions are typically pre-tax, reducing your current taxable income. This is a powerful benefit for long-term financial planning.

- Flexible Spending Accounts (FSAs) or Health Savings Accounts (HSAs): Contributions to these accounts, used for qualified medical expenses, are also typically pre-tax.

Post-Tax Deductions: Other Benefits, Garnishments

Some deductions are taken after taxes have been calculated.

- Life Insurance or Disability Insurance: While some basic employer-provided coverage might be pre-tax, additional voluntary coverage is often post-tax.

- Union Dues: If you are part of a union, your dues will be deducted, often post-tax.

- Wage Garnishments: In cases of unpaid debts (e.g., child support, student loans, court-ordered judgments), a portion of your wages may be legally withheld.

Why Your Net Pay Matters More

Understanding the difference between gross and net pay is paramount for financial realism. You cannot spend your gross income; you only have access to your net income. When setting a budget, planning for expenses, or determining what you can afford, always base your calculations on your net pay. Neglecting this distinction is a common pitfall that can lead to overspending and financial stress. For a $16/hour earner, a gross annual income of $33,280 might translate to a net income closer to $25,000-$28,000, or even less, depending on the deductions.

Budgeting and Financial Planning with a $16/Hour Salary

Living comfortably on $16 an hour requires diligent budgeting and strategic financial planning. While it might present challenges in areas with a high cost of living, it is certainly manageable with a disciplined approach.

Creating a Realistic Budget (50/30/20 Rule or similar)

A budget is not about restriction; it’s about control and clarity. It helps you allocate your net income effectively. A popular guideline is the 50/30/20 Rule:

- 50% for Needs: This covers essential expenses like housing (rent/mortgage), utilities, groceries, transportation, insurance, and minimum loan payments.

- 30% for Wants: This includes discretionary spending such as dining out, entertainment, hobbies, vacations, new clothes, and subscriptions.

- 20% for Savings & Debt Repayment: This portion goes towards building an emergency fund, retirement contributions, investments, and aggressively paying down high-interest debt beyond minimums.

On a net income of, for example, $27,000 annually (roughly $2,250 net per month for a $16/hr worker after taxes and basic deductions), this rule would break down to:

- Needs: $1,125/month

- Wants: $675/month

- Savings & Debt: $450/month

While the 50/30/20 rule is a great starting point, you might need to adjust these percentages based on your local cost of living and personal circumstances. The key is to track your income and expenses rigorously.

Essential Expenses: Housing, Utilities, Food, Transportation

These are the non-negotiables that will consume the largest portion of your budget.

- Housing: This is often the biggest challenge. On $16 an hour, affording a standalone apartment in a major city can be difficult. Strategies might include finding roommates, living in a more affordable suburb, or exploring shared living arrangements. Aim to keep housing costs (rent + utilities) under 30% of your net income if possible.

- Utilities: Budget for electricity, water, heating/cooling, internet, and a cell phone plan. Look for ways to conserve energy to keep costs down.

- Food: Groceries are an essential but controllable expense. Meal planning, cooking at home, buying in bulk, and avoiding food waste can save a significant amount. Limit dining out and impulse buys.

- Transportation: Whether it’s car payments, insurance, gas, maintenance, or public transit passes, transportation costs add up. Consider carpooling, cycling, or public transport options if available and practical.

Discretionary Spending and Savings Goals

It’s tempting to cut all discretionary spending, but a sustainable budget allows for some “wants” to prevent burnout. However, prioritizing is key.

- Prioritize Savings: Even small, consistent contributions to an emergency fund (aim for 3-6 months of essential expenses) and retirement accounts are crucial.

- Smart Spending: Instead of cutting out all entertainment, look for free or low-cost activities. Borrow books from the library, enjoy parks, or host potlucks instead of restaurant outings.

- Track Everything: Use budgeting apps or spreadsheets to see exactly where your money is going. This awareness empowers you to make informed choices.

Dealing with Debt on a Modest Income

If you have debt, especially high-interest consumer debt, it’s vital to address it.

- Prioritize High-Interest Debt: Focus extra payments on credit cards or personal loans with the highest interest rates first.

- Minimum Payments: Ensure you always make at least the minimum payments on all debts to avoid penalties and negative impacts on your credit score.

- Avoid New Debt: With a modest income, taking on new debt can quickly create an unmanageable burden.

Strategies to Increase Your Earning Potential

While managing your finances on $16 an hour is achievable, actively seeking ways to increase your income can significantly improve your quality of life and financial security.

Skill Development and Education

Investing in yourself is often the best investment you can make.

- Certifications: Many industries offer certifications that can lead to higher-paying roles without requiring a full degree. Examples include IT certifications (CompTIA, Microsoft), skilled trades certifications, or specific software proficiencies.

- Online Courses: Platforms like Coursera, Udemy, edX, or even community colleges offer affordable or free courses that can teach valuable skills relevant to in-demand jobs.

- Apprenticeships: For skilled trades, apprenticeships offer paid on-the-job training that leads to higher wages upon completion.

- Employer-Sponsored Training: Check if your current employer offers any training programs or tuition reimbursement benefits that could help you advance.

Negotiating for Better Pay

Even without changing jobs, you might be able to increase your income.

- Performance Reviews: Use your annual performance review as an opportunity to highlight your achievements, demonstrate your value, and request a raise. Research average salaries for your role and experience level in your geographic area to support your request.

- Market Research: Understand what similar roles pay in your region. If you find your pay is significantly below market rate, gather evidence to present to your employer.

- Develop In-Demand Skills: The more valuable and specialized your skills, the more leverage you have in salary negotiations.

Exploring Side Hustles and Supplemental Income Streams

Many people supplement their primary income with part-time gigs.

- Gig Economy: Services like Uber Eats, DoorDash, Instacart, or TaskRabbit offer flexible opportunities.

- Freelancing: If you have skills in writing, graphic design, web development, social media management, or virtual assistance, you can find freelance clients online.

- Selling Goods: Consider selling handmade crafts, reselling items, or offering services like pet sitting, tutoring, or lawn care.

- Part-Time Second Job: If your schedule allows, a second part-time job can significantly boost your income.

Career Advancement and Job Searching Tips

Actively seeking out new opportunities can be a game-changer.

- Network: Connect with professionals in your field. Networking can lead to job opportunities you might not find otherwise.

- Tailor Your Resume and Cover Letter: Customize these documents for each job application, highlighting how your skills and experience align with the specific requirements.

- Practice Interview Skills: Prepare for common interview questions and be ready to articulate your value proposition.

- Look for Growth Opportunities: When job searching, consider not just the starting pay, but also the potential for raises, promotions, and skill development within the company.

Long-Term Financial Health and $16/Hour

While the immediate focus on $16 an hour might be on day-to-day budgeting, it’s essential to integrate long-term financial health into your plan. Even with a modest income, consistent small steps can lead to significant financial security over time.

Building an Emergency Fund

This cannot be stressed enough. An emergency fund is a cash reserve set aside to cover unexpected expenses like job loss, medical emergencies, or major car repairs.

- Start Small: Begin by saving $500-$1,000. This initial cushion can prevent small setbacks from becoming major financial crises.

- Automate Savings: Set up automatic transfers from your checking to a separate savings account each payday. Even $10 or $20 a week adds up.

- Goal: Aim to accumulate 3 to 6 months’ worth of essential living expenses.

Starting Early with Retirement Savings

The power of compound interest is a financial superpower, but it needs time to work its magic.

- Employer Match: If your employer offers a 401(k) match, contribute at least enough to get the full match. This is essentially free money and an immediate 100% return on your investment.

- Roth IRA: Consider contributing to a Roth IRA. Contributions are made with after-tax dollars, but qualified withdrawals in retirement are tax-free.

- Consistency: Even small, consistent contributions can grow substantially over decades.

Understanding Inflation and Cost of Living

Inflation erodes the purchasing power of money over time. What $16 an hour buys today will likely buy less in 5, 10, or 20 years.

- Stay Informed: Be aware of inflation rates and the rising cost of living in your area.

- Advocate for Raises: This awareness highlights the importance of seeking regular raises to keep pace with inflation and maintain your purchasing power.

- Invest: Saving money in a traditional savings account might not keep pace with inflation. Investing your money (e.g., in a diversified portfolio) is generally necessary for it to grow faster than inflation.

Seeking Professional Financial Advice

While many financial principles can be self-taught, sometimes a professional can provide invaluable guidance.

- Free Resources: Many non-profit credit counseling agencies offer free or low-cost advice on debt management and budgeting.

- Financial Planners: For more complex situations or long-term planning, a fee-only financial planner can help create a personalized roadmap. Even if you think your income is too low for a planner, many offer introductory consultations or services tailored to those building their wealth.

In conclusion, earning $16 an hour translates to a gross annual income of $33,280, assuming a standard full-time work week. However, understanding your net pay and meticulously budgeting are crucial for financial stability. By strategically managing expenses, continuously seeking opportunities to increase your income through skill development or side hustles, and consistently planning for the long term, you can build a solid financial foundation and work towards a future of greater financial comfort and security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.