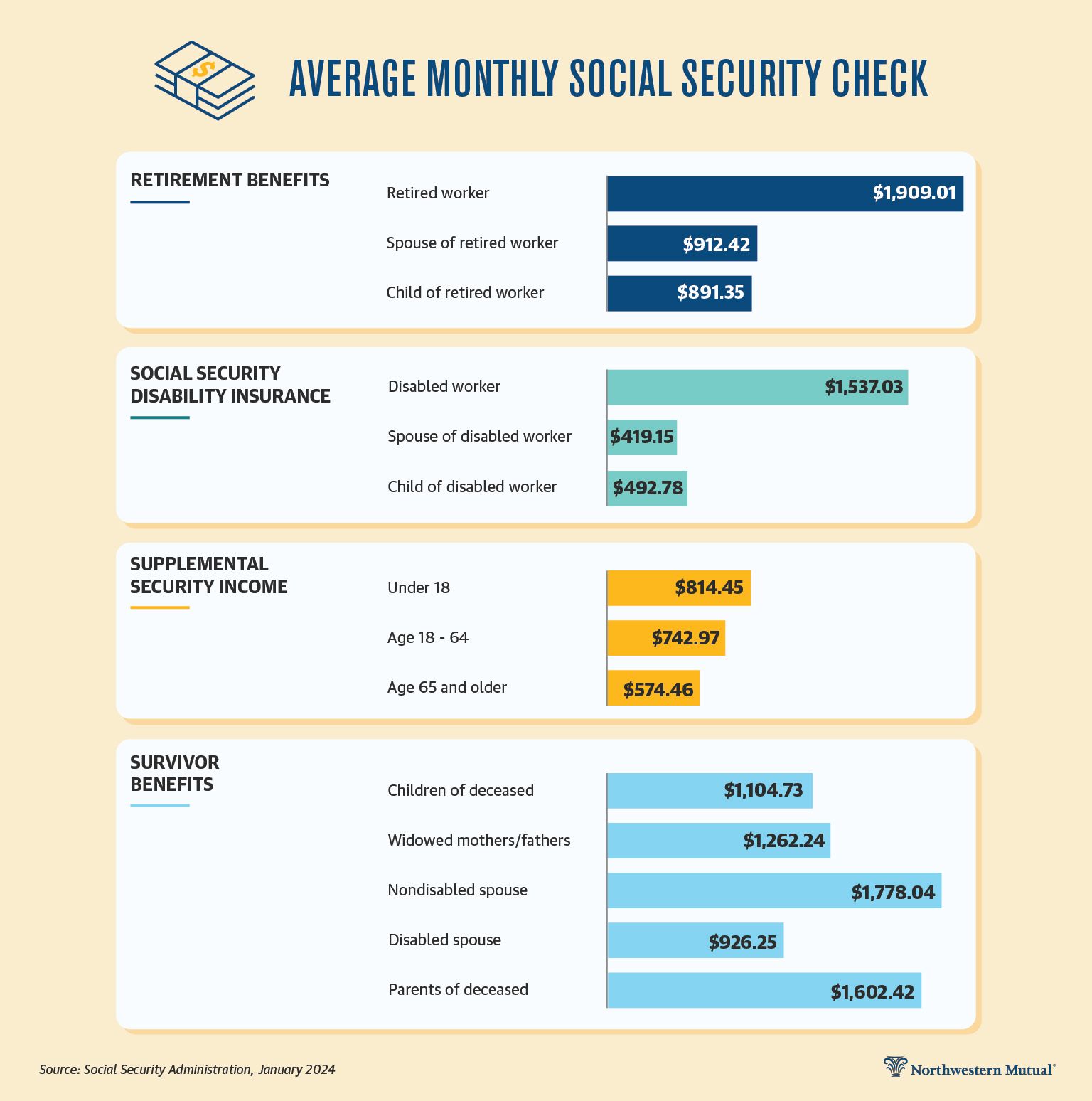

Social Security stands as a cornerstone of financial security for millions of Americans, providing vital income for retirees, individuals with disabilities, and survivors. Far from a simple handout, it represents a complex system built upon decades of contributions from workers and employers. For many, understanding “how much are Social Security checks” is not merely an academic exercise; it’s a critical component of their financial planning for retirement or navigating life’s unexpected challenges.

The amount an individual receives from Social Security is highly personalized, influenced by a myriad of factors including their lifetime earnings, the age at which they claim benefits, and various personal circumstances. While there’s no single answer that applies to everyone, delving into the intricacies of its calculation, eligibility requirements, and available benefit types can demystify the system and empower individuals to make informed decisions that could significantly impact their financial future. This comprehensive guide aims to shed light on these complexities, offering a professional, insightful, and engaging exploration of Social Security checks.

Understanding the Fundamentals of Social Security Benefits

Before diving into specific figures, it’s essential to grasp the foundational principles governing Social Security. This system isn’t just about retirement; it encompasses a broader safety net designed to protect Americans across different life stages.

What is Social Security?

Established in 1935, Social Security was designed to provide a basic level of income protection for older Americans. Over time, its scope expanded to include disability insurance and benefits for survivors. It operates as a pay-as-you-go system, where current workers’ contributions primarily fund the benefits of current retirees and other beneficiaries. These contributions are collected through the Federal Insurance Contributions Act (FICA) tax, levied on wages and self-employment income. The underlying philosophy is one of shared responsibility and collective welfare, ensuring that individuals who contribute throughout their working lives have a safety net when they can no longer work, or their families are faced with the loss of a primary wage earner.

Who is Eligible for Benefits?

Eligibility for Social Security benefits is primarily determined by an individual’s work history. Most people qualify for benefits by earning “credits” through their work. In 2024, you earn one credit for each $1,730 of earnings, up to a maximum of four credits per year.

- Retirement Benefits: Most individuals need 40 credits (10 years of work) to be eligible for retirement benefits.

- Disability Benefits: The number of credits required for disability benefits varies by age. Younger workers generally need fewer credits, and some must have earned credits recently.

- Survivor Benefits: Family members (spouses, children, dependent parents) may be eligible for survivor benefits if the deceased worker had earned enough credits. The specific number depends on the worker’s age at death.

Beyond credits, age plays a crucial role for retirement benefits. While you can claim benefits as early as age 62, your “Full Retirement Age” (FRA) is when you become entitled to 100% of your Primary Insurance Amount (PIA). FRA ranges from 66 to 67, depending on your birth year.

Key Factors Influencing Your Benefit Amount

Several critical variables converge to determine the size of your Social Security check:

- Your Lifetime Earnings: This is perhaps the most significant factor. The higher your earnings over your career, the higher your potential benefit.

- Your Age When You Claim Benefits: Claiming before your FRA results in a permanent reduction, while claiming after your FRA (up to age 70) earns you delayed retirement credits, increasing your benefit.

- Cost-of-Living Adjustments (COLAs): Benefits are periodically adjusted to keep pace with inflation, ensuring their purchasing power isn’t eroded over time.

- Windfall Elimination Provision (WEP) and Government Pension Offset (GPO): These provisions can reduce Social Security benefits for individuals who also receive a pension from work not covered by Social Security (e.g., some government jobs).

- Spousal/Survivor Benefits: If you’re eligible for benefits as a spouse or survivor, your check might be a percentage of another person’s benefit.

The Calculation Behind Your Social Security Check

Understanding the general principles is one thing; deciphering the specific calculation mechanism is another. Social Security uses a formula designed to replace a higher percentage of income for lower earners than for higher earners, reflecting its progressive nature.

Average Indexed Monthly Earnings (AIME): How Past Earnings are Valued

The starting point for calculating your Social Security benefit is your Average Indexed Monthly Earnings (AIME). This isn’t just a simple average of all your earnings. Instead, the Social Security Administration (SSA) “indexes” your past earnings to account for changes in general wage levels over time. This process ensures that your earnings from, say, the 1980s, are valued in terms of current economic standards.

Here’s how it generally works:

- Identify Earnings Years: The SSA takes your earnings from all years you’ve worked.

- Indexing: Your earnings from previous years are adjusted upwards to reflect the average wage growth in the economy up to age 60. Earnings after age 60 are used at their nominal value.

- Top 35 Years: The SSA then identifies your 35 highest-earning indexed years. If you have fewer than 35 years of earnings, the remaining years are counted as zero.

- Calculate Average: These 35 years of indexed earnings are summed up and divided by 420 (the number of months in 35 years) to arrive at your AIME.

This AIME provides a fair representation of your career earnings in today’s terms, serving as the primary input for your base benefit.

Primary Insurance Amount (PIA): Your Full Retirement Age Benefit

Once your AIME is determined, the SSA uses a progressive formula to calculate your Primary Insurance Amount (PIA). The PIA is the monthly benefit you are entitled to if you claim benefits precisely at your Full Retirement Age (FRA).

The PIA formula uses “bend points” – specific dollar amounts that divide your AIME into segments, each multiplied by a different percentage. For individuals who become eligible for retirement benefits in 2024, the formula is:

- 90% of the first $1,174 of your AIME

- 32% of your AIME between $1,174 and $7,078

- 15% of your AIME above $7,078

The sum of these three amounts is your PIA. This progressive structure means that lower earners receive a relatively higher percentage of their pre-retirement income in benefits compared to higher earners, reflecting the program’s social safety net objective.

Adjustments for Claiming Age: Early vs. Delayed Retirement Credits

Your PIA is your benefit at FRA. However, very few people claim benefits exactly at this age. Your claiming age significantly adjusts your final monthly check:

- Claiming Early (Age 62 to FRA): If you claim benefits before your FRA, your monthly payment will be permanently reduced. The reduction is typically about 5/9 of 1% for each month before FRA, up to 36 months. For any months beyond 36, the reduction is 5/12 of 1% per month. Claiming at the earliest age of 62 can result in a reduction of up to 30% for those with an FRA of 67.

- Claiming Late (FRA to Age 70): Conversely, if you delay claiming benefits past your FRA, you earn “delayed retirement credits.” These credits permanently increase your monthly benefit by 2/3 of 1% for each month you delay, up to age 70. This translates to an 8% annual increase. Delaying from FRA 67 to age 70 can result in a 24% increase in your monthly benefit for the rest of your life.

This flexibility allows individuals to tailor their Social Security income to their financial needs and longevity expectations.

Navigating Common Scenarios and Special Considerations

Social Security isn’t a one-size-fits-all program. It accounts for various life events and family structures, leading to a range of benefit types and rules.

Spousal and Survivor Benefits: Beyond Your Own Earnings Record

Social Security extends its protection to family members, often allowing individuals to claim benefits based on another person’s work record.

- Spousal Benefits: If you are married, you may be eligible to receive up to 50% of your spouse’s PIA, provided your own benefit based on your work record is less than that amount. You can typically claim spousal benefits starting at age 62, though this will be reduced if claimed before your FRA. If your own benefit is higher, you’ll receive your own.

- Survivor Benefits: When a worker dies, certain family members can receive benefits based on the deceased worker’s earnings. A surviving spouse can receive up to 100% of the deceased worker’s PIA (if claimed at their own FRA or later). Dependent children, and sometimes even dependent parents, may also be eligible for benefits. The total amount paid to a family is subject to a “family maximum benefit,” which can range from 150% to 180% of the deceased worker’s PIA.

Disability Benefits: A Lifeline for Those Unable to Work

For individuals who become severely disabled and unable to work, Social Security Disability Insurance (SSDI) provides a critical income stream. To qualify, you must have worked long enough and recently enough under Social Security. The SSA determines disability based on strict criteria: your condition must prevent you from doing substantial gainful activity, be expected to last at least a year, or result in death.

The calculation of disability benefits is similar to retirement benefits, based on your AIME. However, instead of using 35 years, the SSA often uses a shorter period of your earnings to calculate a “disability PIA,” reflecting that disabled individuals typically have fewer years of work.

The Impact of Working While Receiving Benefits

Social Security is designed to replace lost income due to retirement, disability, or death. Therefore, working while receiving benefits, particularly before your FRA, can affect your benefit amount.

- Before Full Retirement Age: If you are under your FRA and continue to work while receiving benefits, your benefits may be temporarily reduced if your earnings exceed a certain annual limit. In 2024, for every $2 you earn above $22,320, $1 is withheld from your benefits.

- In the Year You Reach FRA: A higher earnings limit applies ($59,520 in 2024). For every $3 you earn above this limit, $1 is withheld. This applies only to earnings before the month you reach FRA.

- At or After Full Retirement Age: Once you reach your FRA, there are no earnings limits. You can work and earn as much as you want without your Social Security benefits being reduced.

It’s important to note that any benefits withheld due to earnings limits are not lost forever. They are factored back into your benefit calculation when you reach your FRA, potentially resulting in a higher monthly payment going forward.

Understanding Cost-of-Living Adjustments (COLAs)

One of the vital features of Social Security is its protection against inflation through Cost-of-Living Adjustments (COLAs). Since 1975, benefits have been automatically adjusted annually to help maintain their purchasing power.

COLAs are determined by changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) from the third quarter of the previous year to the third quarter of the current year. If there’s an increase in the CPI-W, benefits increase by the same percentage, effective in December and payable in January checks. These adjustments are crucial for ensuring that Social Security benefits remain relevant and supportive over an individual’s potentially long retirement.

Maximizing Your Social Security Benefits

Given the complexity and the significant role Social Security plays in many people’s financial lives, strategic planning to maximize benefits is paramount.

Strategic Claiming Ages: A Critical Decision Point

Deciding when to start receiving Social Security benefits is one of the most impactful financial decisions many Americans will make. It’s not just about getting money sooner; it’s about optimizing lifetime income.

- Longevity: If you expect to live a long life, delaying benefits can result in a substantially higher cumulative payout over your lifetime due to delayed retirement credits.

- Health: Poor health or a shorter life expectancy might favor claiming earlier to receive benefits for more years, even if the monthly amount is smaller.

- Other Income and Savings: If you have substantial other retirement income (pensions, 401(k)s, IRAs), you might be able to afford to delay claiming Social Security, allowing your benefit to grow. Conversely, if Social Security will be your primary income, claiming earlier might be necessary.

- Spousal Considerations: When coordinating benefits with a spouse, one might delay to maximize the higher earner’s benefit, which then also maximizes the survivor benefit for the remaining spouse.

A careful analysis, sometimes involving “break-even” calculations (the point at which the cumulative total of a larger delayed benefit overtakes the cumulative total of an earlier, smaller benefit), is often necessary.

Coordinated Spousal Claiming Strategies

For married couples, Social Security offers opportunities for strategic claiming that can yield higher combined lifetime benefits. While some popular strategies like “file and suspend” have been phased out or modified, others remain:

- Restricted Application for Spousal Benefits: Individuals born before January 2, 1954, still have the option to file a “restricted application” at their FRA. This allows them to claim only spousal benefits while their own worker benefit continues to grow with delayed retirement credits until age 70. At age 70, they then switch to their own maximized benefit.

- Claiming Based on Higher Earner: Often, the lower-earning spouse might claim their own reduced benefit early, allowing the higher-earning spouse to delay their benefits until age 70. This maximizes the larger benefit and, critically, the future survivor benefit for the lower-earning spouse.

These strategies require careful planning and understanding of the specific rules applicable to your birth year.

Monitoring Your Earnings Record

The Social Security Administration maintains a detailed record of your earnings throughout your career, which is directly used to calculate your AIME and ultimately your benefits. It is crucial to periodically review your Social Security Statement.

You can access your statement online by creating an account at my Social Security (ssa.gov). This statement shows your earnings history, an estimate of your future benefits at different claiming ages, and an overview of potential disability and survivor benefits. Reviewing this statement ensures that your earnings are accurately recorded. If you find any discrepancies, it’s essential to contact the SSA to correct them, as errors could lead to a lower benefit amount.

Integrating Social Security with Your Overall Retirement Plan

Social Security, while vital, is generally intended to be one leg of a three-legged stool for retirement income, alongside personal savings/investments and employer-sponsored pensions (if applicable). It was never meant to be the sole source of retirement income for most people.

Therefore, integrate your anticipated Social Security benefits into your broader financial plan. Understand how much of your expenses Social Security is projected to cover, and then plan your savings and investments (401(k)s, IRAs, brokerage accounts) to bridge the remaining gap. This holistic approach ensures a more secure and comfortable retirement.

Future Outlook and Financial Planning

The financial health of Social Security is a perennial topic of discussion. While the system has faced challenges, it has also demonstrated remarkable resilience.

Addressing Solvency Concerns

Projections from the Social Security Trustees indicate that the program’s trust funds are projected to be able to pay 100% of promised benefits until the mid-2030s. After that, without congressional action, it might only be able to pay about 80% of scheduled benefits. It’s important to note that this doesn’t mean Social Security will run out of money entirely; it means future generations of retirees might receive a lower percentage of scheduled benefits if no changes are made.

Various proposals for shoring up the system exist, including raising the full retirement age, increasing the Social Security tax rate, raising the cap on taxable earnings, or adjusting the COLA formula. While these discussions continue, individuals should plan for a range of outcomes, understanding that some adjustments may occur in the future.

The Importance of a Diversified Retirement Strategy

Given the potential for future changes and the inherent limits of Social Security benefits, a diversified retirement strategy remains paramount. Relying solely on Social Security for retirement income is generally not advisable for most individuals.

Aggressively saving through 401(k)s, IRAs, and other investment vehicles, combined with a thoughtful Social Security claiming strategy, provides the strongest foundation for financial independence in retirement. Consider working with a qualified financial advisor to develop a personalized plan that integrates your Social Security benefits with your other assets, helping you navigate the complexities and achieve your long-term financial goals.

In conclusion, “how much are Social Security checks” is a multifaceted question with answers unique to each individual’s journey. By understanding the core calculations, eligibility rules, and strategic considerations, individuals can make informed decisions that optimize this essential financial pillar and contribute to a more secure future. Proactive planning and continuous engagement with your Social Security statement are key to unlocking its full potential.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.