Securing a business loan is often the most critical inflection point in a company’s lifecycle. Whether you are looking to bridge a seasonal cash flow gap, invest in new inventory, or expand your operations into a secondary market, capital is the fuel that drives professional ambition. However, the path to funding is rarely a straight line. In today’s complex financial landscape, business owners must navigate a gauntlet of traditional banks, government-backed programs, and innovative fintech lenders.

Success in the application process requires more than just a healthy bank balance; it demands a strategic understanding of how lenders perceive risk and how you can position your business as a sound investment. This guide explores the multifaceted world of business finance, providing a roadmap to help you secure the capital necessary to scale.

Strengthening Your Financial Profile Before You Apply

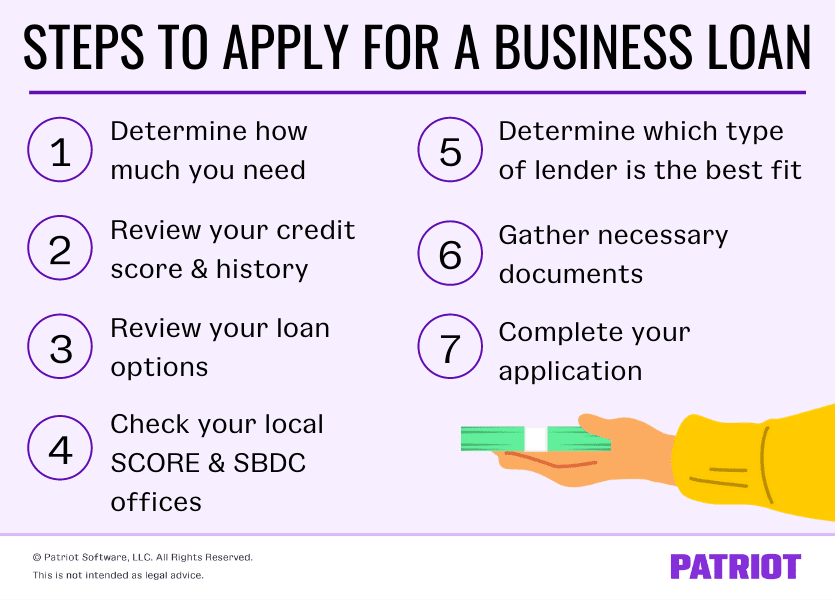

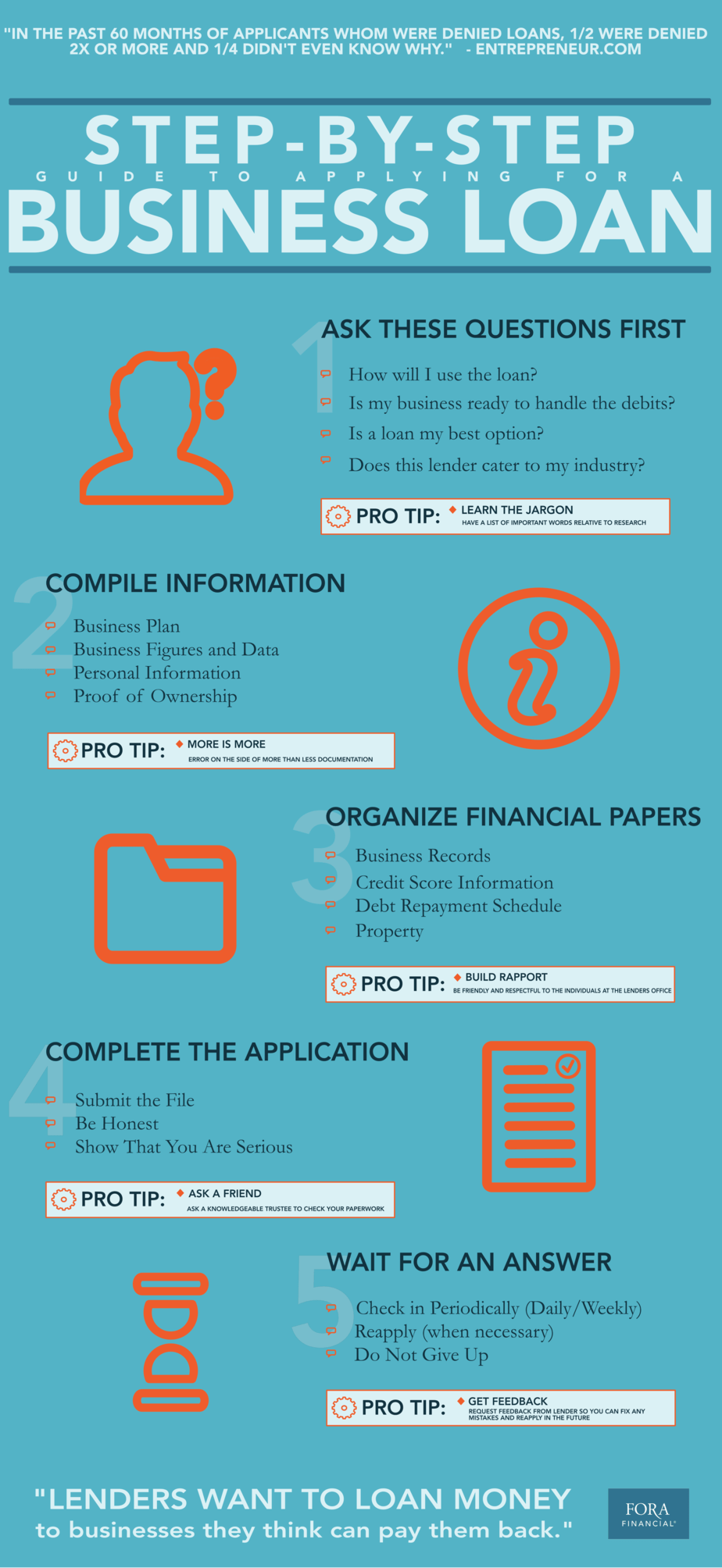

Before you ever step foot in a bank or click “submit” on an online application, you must audit your financial standing from the perspective of an underwriter. Lenders are inherently risk-averse; they are not looking for the next “unicorn” as a venture capitalist might, but rather for a stable entity that demonstrates a high probability of repayment.

The Dual Importance of Credit Scores

Most small business owners mistakenly believe that their business credit score is the only metric that matters. In reality, for many small-to-medium enterprises (SMEs), the personal credit score of the founder is just as critical. Lenders use personal credit history as a proxy for financial responsibility. A score above 700 is generally considered the threshold for favorable interest rates. Simultaneously, you should pull your business credit reports from bureaus like Dun & Bradstreet, Experian, and Equifax to ensure there are no errors that could derail your application.

Organizing Essential Financial Documents

Documentation is the bedrock of any loan application. You should have at least two to three years of federal income tax returns (both personal and business), profit and loss (P&L) statements, and balance sheets ready for review. Modern lenders also look closely at your accounts receivable and accounts payable aging reports. These documents provide a snapshot of your liquidity and how efficiently you manage the money flowing through your business. If your bookkeeping is disorganized, it signals a lack of professional oversight, which can be a major red flag for lenders.

Crafting a Compelling Business Plan and Use of Funds

A loan application without a clear purpose is often discarded. Lenders want to see a “Use of Funds” statement that outlines exactly where every dollar will go. Are you purchasing a $50,000 piece of equipment that will increase production by 20%? Or are you hiring three new sales representatives to capture a specific market share? Your business plan should include financial projections that demonstrate how the loan will generate enough additional revenue to cover the new debt service while still maintaining healthy margins.

Identifying the Right Funding Vehicle for Your Business Goals

The “best” loan is not always the one with the lowest interest rate; it is the one that aligns most closely with your specific business needs and repayment capacity. Business finance is not a one-size-fits-all industry.

SBA Loans: The Gold Standard for Small Businesses

The U.S. Small Business Administration (SBA) does not lend money directly to business owners. Instead, it guarantees a portion of loans made by partner banks, reducing the risk for the lender. The SBA 7(a) loan is the most popular, offering versatility for working capital, debt refinancing, or equipment purchases. The SBA 504 loan is specifically designed for fixed assets like real estate or heavy machinery. While these loans offer the most competitive rates and longest terms, the application process is notoriously rigorous and can take several months to close.

Conventional Bank Loans and Lines of Credit

Traditional term loans from commercial banks are ideal for established businesses with strong collateral and significant revenue. However, for many businesses, a “Line of Credit” is a more strategic tool. Unlike a term loan, where you receive a lump sum and pay interest on the full amount, a line of credit allows you to draw funds only when needed. This is particularly useful for managing seasonal fluctuations or unexpected expenses, as you only pay interest on the capital you actually use.

Fintech and Alternative Lending Solutions

The rise of financial technology (fintech) has revolutionized the lending space. Companies like OnDeck, BlueVine, and Funding Circle use proprietary algorithms to assess risk faster than traditional banks. If you need capital within 48 to 72 hours, fintech lenders are often the best route. The trade-off for this speed and accessibility is typically a higher interest rate and shorter repayment terms. These are best used for short-term opportunities where the return on investment (ROI) significantly outweighs the cost of the capital.

The Strategic Application Workflow: From Research to Closing

Once you have identified the type of loan you need, the actual application process begins. This stage requires meticulous attention to detail and a proactive approach to communication.

Defining Your Funding Requirements

One of the most common mistakes entrepreneurs make is asking for “as much as the bank will give.” This suggests a lack of financial planning. Instead, calculate your “ask” based on specific data. If you are seeking a loan for expansion, include quotes from contractors, price lists for equipment, and marketing budgets. By presenting a specific, data-backed number, you demonstrate to the lender that you are a disciplined manager of capital.

Navigating the Underwriting Process

Underwriting is the process by which a lender verifies your information and assesses the risk of the loan. During this period, which can last from a few days to several weeks, the lender may ask for “additional disclosures.” It is vital to respond to these requests immediately. Delays in providing a simple document can push your application back into a queue or lead to a decline if the lender perceives a lack of transparency.

Understanding Loan Terms and Covenants

When you receive a loan offer, do not look solely at the interest rate. Read the fine print for “covenants”—rules you must follow to keep the loan in good standing. For example, a lender may require you to maintain a certain debt-to-equity ratio or prevent you from taking on additional debt without their permission. Additionally, check for “prepayment penalties.” If your business grows rapidly and you want to pay the loan off early to save on interest, you don’t want to be penalized for doing so.

Mastering the Economics of Debt: Ratios and Risk

To maximize your chances of approval, you must understand the mathematical formulas lenders use to evaluate your business’s health. These ratios determine not just whether you get the loan, but the terms you are offered.

Calculating Your Debt Service Coverage Ratio (DSCR)

The DSCR is perhaps the most important metric in business finance. It is calculated by taking your Net Operating Income and dividing it by your total annual debt payments. A ratio of 1.0 means you have exactly enough cash flow to cover your debt. Most lenders look for a DSCR of 1.25 or higher, providing a 25% “buffer” to ensure that even if your revenue dips slightly, you can still meet your financial obligations. Understanding your DSCR before you apply allows you to adjust your “ask” to fit within a lender’s comfort zone.

Collateral and the Personal Guarantee

In many cases, especially for larger loans, lenders require collateral—tangible assets like real estate, inventory, or equipment that the bank can seize if you default. If your business lacks sufficient assets, many lenders will require a “Personal Guarantee.” This means you are personally liable for the debt, and your personal assets (like your home or savings) could be at risk if the business cannot pay. This is a significant commitment that should be weighed carefully against the potential growth the loan will facilitate.

The Role of Cash Reserves

Lenders are comforted by “liquidity.” Even if you are applying for a loan, having a healthy cash reserve in your business checking account shows that you have a safety net. It demonstrates that the loan is a strategic choice for growth rather than a desperate attempt to stay afloat. If your bank balances are consistently near zero, lenders will view your business as high-risk, regardless of your revenue.

Conclusion: Debt as a Catalyst for Sustainable Success

Applying for a business loan is a rigorous exercise that forces a business owner to look deeply into the mechanics of their company’s finances. While the process can be daunting, it is an essential skill for any entrepreneur looking to move beyond the startup phase. By maintaining impeccable financial records, choosing the right lending partner, and understanding the underlying economics of debt, you can secure the capital necessary to transform your vision into a scalable reality. Remember, a loan is not merely an obligation; it is a strategic tool that, when used wisely, provides the leverage needed to achieve long-term financial stability and market leadership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.