The concept of compound interest is often heralded as one of the most powerful forces in finance, a silent engine that steadily propels wealth creation over time. Often attributed to Albert Einstein as the “eighth wonder of the world,” compound interest is not merely an academic concept but a practical tool available to anyone committed to financial growth. It’s the secret behind why starting early with investments makes such a dramatic difference and why seemingly small, consistent contributions can accumulate into substantial sums. Understanding and actively harnessing compound interest is fundamental for personal finance, enabling individuals to build savings, accelerate retirement planning, and achieve long-term financial independence. This article delves into the mechanics of compounding, explores strategies to maximize its benefits, and outlines the disciplined approach required to truly unlock its transformative power.

Understanding the Power of Compounding

At its core, compound interest is about earning returns on your initial investment and on the accumulated interest from previous periods. It’s a snowball effect where your money starts working harder, generating its own earnings, which then also start generating earnings. This cyclical growth differentiates it fundamentally from simple interest and forms the bedrock of long-term wealth accumulation.

What is Compound Interest?

Compound interest is the interest on a loan or deposit calculated based on both the initial principal and the accumulated interest from previous periods. In simpler terms, it’s interest on interest. Imagine you invest $1,000 at a 10% annual interest rate. With simple interest, you would earn $100 each year, so after five years, you’d have $1,500. With compound interest, the first year you earn $100, bringing your total to $1,100. In the second year, you earn 10% on $1,100, which is $110, bringing your total to $1,210. This accelerating growth continues, making compound interest a far more potent force for wealth creation than simple interest over extended periods.

The “snowball effect” metaphor perfectly illustrates this phenomenon. A small snowball rolling down a hill gathers more snow, becoming larger and picking up even more snow at an increasing rate. Similarly, a modest initial investment, given enough time and consistent contributions, can grow exponentially as the base on which interest is calculated steadily expands. This inherent power of compounding is why it’s so critical to understand and utilize it in your financial strategy.

The Key Variables in Compounding

Several factors dictate the pace and magnitude of compound interest growth. Understanding and optimizing these variables is crucial for maximizing your returns.

- Principal Amount: This is your initial investment or the amount of money you start with. A larger principal generally leads to greater absolute returns, assuming all other factors are equal. However, even a small principal, combined with the other variables, can achieve significant growth over time.

- Interest Rate: The percentage return your investment generates. A higher interest rate naturally accelerates the compounding process, leading to faster wealth accumulation. Seeking reasonable, risk-adjusted returns is a critical component of successful compounding.

- Time Horizon: This is arguably the most crucial variable for compound interest. The longer your money has to grow, the more pronounced the effect of compounding becomes. The exponential nature of compounding means that growth in later years vastly outstrips growth in earlier years, making early investment a paramount strategy.

- Compounding Frequency: This refers to how often the interest is calculated and added back to the principal. Interest can compound annually, semi-annually, quarterly, monthly, daily, or even continuously. The more frequently interest is compounded, the faster your money grows, as you start earning interest on your interest sooner. For instance, an investment compounding daily will grow slightly faster than one compounding annually, even with the same nominal interest rate.

Strategies to Maximize Your Compounding Returns

Harnessing the full potential of compound interest requires more than just understanding its definition; it demands a strategic approach to saving, investing, and managing your financial assets. By actively implementing certain practices, you can significantly amplify your compounding returns.

Start Early and Be Consistent

The single most impactful strategy for leveraging compound interest is to begin investing as early as possible. Time is the silent partner in compounding, allowing your money to grow exponentially over decades. Even small contributions made in your 20s can far surpass larger contributions made in your 40s or 50s, simply because of the extended period over which compounding can occur.

Beyond an early start, consistency is key. Regular contributions, even modest ones, feed the compounding machine. This strategy, often referred to as dollar-cost averaging, involves investing a fixed amount of money at regular intervals, regardless of market fluctuations. This practice helps to smooth out market volatility and ensures that you are continuously adding to your principal, thereby maximizing the base upon which future interest is earned. Automating your savings and investments can make consistency effortless, removing the temptation to skip contributions.

Choose the Right Investment Vehicles

The effectiveness of compounding is directly tied to the types of assets you choose for your investments. Different vehicles offer varying levels of risk, return, and compounding frequency.

- Savings Accounts & Certificates of Deposit (CDs): While offering lower interest rates, these provide a secure, low-risk environment for your principal. They are suitable for emergency funds or short-term savings where capital preservation is paramount. Interest on these typically compounds daily or monthly.

- Stocks, Exchange-Traded Funds (ETFs), & Mutual Funds: These offer significantly higher growth potential over the long term, albeit with higher risk. Investing in a diversified portfolio of stocks, or through ETFs and mutual funds that hold a basket of stocks, allows your capital to compound through price appreciation and dividend reinvestment. Dividends, when reinvested, act as additional principal, fueling further compounding.

- Retirement Accounts (401k, IRA): These are particularly powerful vehicles for compounding due to their tax advantages and long-term nature. Contributions often grow tax-deferred (Traditional IRA/401k) or tax-free (Roth IRA/401k), meaning your earnings compound without being eroded by annual taxes, providing a substantial boost to growth over decades. Employer matching contributions in 401ks essentially offer an immediate, guaranteed return that compounds over time.

- Real Estate: While requiring more capital, real estate can provide compounding returns through property appreciation and rental income. Rental income, if reinvested into paying down the mortgage or acquiring more property, further enhances the compounding effect on your overall net worth.

Reinvest Your Earnings

To truly harness compounding, it’s essential to let your earnings stay in the investment. Many investment accounts offer options for automatic dividend reinvestment programs (DRIPs) or capital gains reinvestment. Instead of taking dividends or interest payments as cash, choose to have them automatically used to purchase more shares or increase your principal. This immediately adds to your base, allowing those reinvested earnings to start earning interest themselves, accelerating the growth of your portfolio. Avoiding premature withdrawals from your investments is equally critical, as each withdrawal reduces the principal and slows down the compounding process.

Minimize Fees and Taxes

Fees and taxes can act as significant drag on your compounding returns, eroding your gains over time. High management fees on mutual funds, trading commissions, or unnecessary administrative charges can noticeably reduce your net returns. Seek out low-cost investment options, such as index funds or ETFs, which often have significantly lower expense ratios.

Similarly, taxes on investment gains can reduce the amount available for compounding. Utilizing tax-advantaged accounts like 401ks, IRAs, and 529 plans (for education savings) allows your investments to grow untouched by annual taxes, significantly boosting their long-term compounding potential. Understanding capital gains taxes and strategic tax planning, such as holding investments for longer than a year to qualify for lower long-term capital gains rates, can also protect your compounding engine.

Calculating and Visualizing Compound Growth

Understanding the underlying math and utilizing available tools can help you grasp the magnitude of compound interest and plan your financial future more effectively. Visualizing the growth curve can be incredibly motivating and insightful.

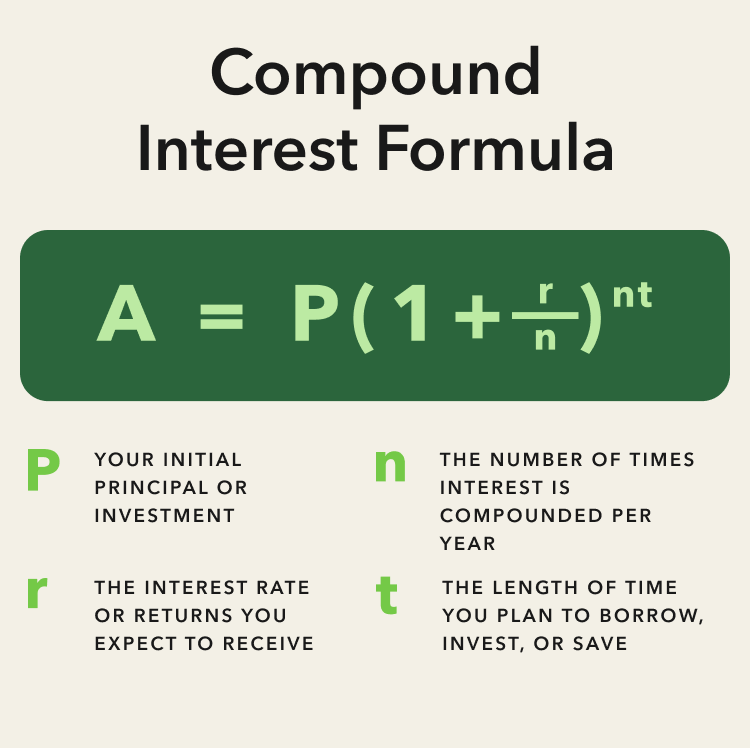

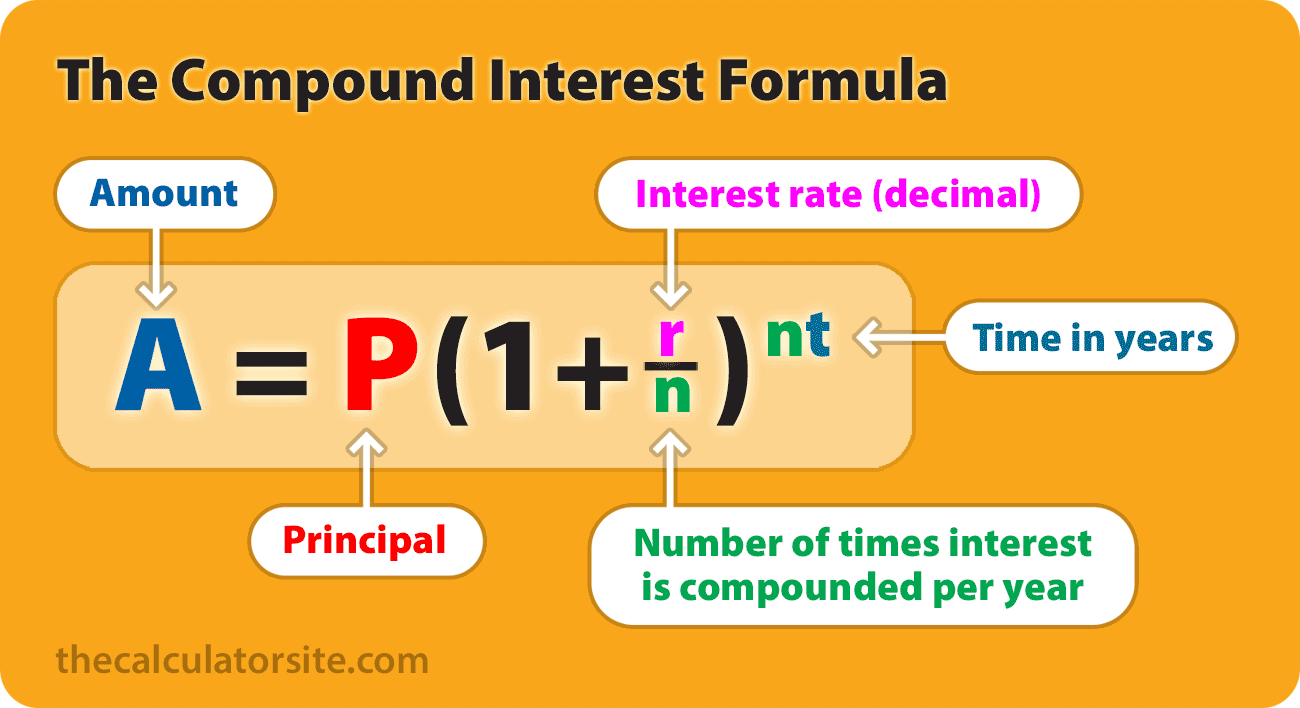

The Compound Interest Formula

The standard formula for compound interest is:

A = P (1 + r/n)^(nt)

Where:

- A = the future value of the investment/loan, including interest

- P = the principal investment amount (the initial deposit or loan amount)

- r = the annual interest rate (as a decimal, e.g., 5% = 0.05)

- n = the number of times that interest is compounded per year (e.g., annually n=1, monthly n=12, daily n=365)

- t = the number of years the money is invested or borrowed for

Let’s illustrate with an example: If you invest $10,000 at an annual interest rate of 7% compounded annually for 20 years:

P = $10,000

r = 0.07

n = 1

t = 20

A = 10,000 * (1 + 0.07/1)^(1*20)

A = 10,000 * (1.07)^20

A = 10,000 * 3.86968

A ≈ $38,696.80

After 20 years, your initial $10,000 would have grown to almost $38,700, with nearly $28,700 of that being earned interest, simply by letting it compound.

Tools and Resources

While the formula is powerful, you don’t need to manually calculate it every time. Numerous tools are available to help:

- Online Compound Interest Calculators: Websites of financial institutions, investment platforms, and personal finance blogs often feature free, user-friendly compound interest calculators. These allow you to input different variables (principal, rate, time, frequency, additional contributions) and instantly see the projected growth.

- Spreadsheets: Programs like Microsoft Excel or Google Sheets are excellent for creating customized compound interest models. You can build tables that show year-by-year growth, incorporate varying contribution amounts, and visualize the impact of different interest rates.

- Financial Planning Software: More comprehensive personal finance software often includes sophisticated projection tools that factor in multiple income streams, expenses, and investment accounts to give you a holistic view of your financial future, powered by compounding.

The Rule of 72

A handy mental shortcut for estimating how long it will take for an investment to double in value is the Rule of 72. By dividing 72 by the annual interest rate, you can get an approximate number of years for your investment to double.

For example, if you earn an 8% annual return, it will take approximately 72 / 8 = 9 years for your investment to double. If you earn a 10% return, it will take about 7.2 years. This rule highlights the substantial impact that even slightly higher interest rates can have over the long run and underscores the importance of minimizing fees which eat into your effective return.

Overcoming Challenges and Maintaining Discipline

While the mathematical power of compound interest is undeniable, the human element—patience, discipline, and managing expectations—often presents the biggest challenge. The path to significant wealth accumulation through compounding is rarely a straight line and requires perseverance.

The Illusion of Slow Start

One of the most common reasons people fail to stick with compounding is the illusion of a slow start. In the initial years, the absolute dollar amount of interest earned might seem modest compared to the principal. The exponential growth curve of compounding doesn’t truly “kick in” until much later. For instance, in our $10,000 at 7% example, after 5 years, the balance is $14,025 (earning $4,025 in interest). After 10 years, it’s $19,671 (earning $9,671). But after 20 years, it’s $38,696 (earning $28,696). The last 10 years generated significantly more interest than the first 10.

It’s crucial to understand that the initial years are laying the groundwork. Patience is a virtue in investing; resist the urge to compare your early growth to the dramatic leaps seen in later stages. Trust the math and stay the course.

Battling Inflation

Another significant challenge is inflation, which erodes the purchasing power of your money over time. While your investments may be compounding in nominal terms, if the inflation rate is higher than your net investment return, your real (inflation-adjusted) wealth is actually decreasing. It’s therefore vital to seek investment vehicles that offer returns that comfortably outpace inflation. This often means investing in growth-oriented assets like stocks and real estate, rather than solely relying on low-interest savings accounts, which typically yield less than the long-term inflation average. Diversification across different asset classes can help mitigate this risk by providing different avenues for growth.

Staying Consistent Amidst Life’s Changes

Life is unpredictable, and financial stability can be tested by unexpected expenses, career changes, or personal goals. Maintaining consistency in your saving and investing habits during these periods is a critical challenge.

- Automating Savings: Set up automatic transfers from your checking account to your investment accounts immediately after payday. This “pay yourself first” strategy ensures that you contribute consistently before other expenses arise.

- Budgeting and Financial Planning: A well-structured budget helps you track your income and expenses, identify areas for savings, and allocate funds consistently towards your investment goals. Regular financial planning sessions, whether with a professional or by yourself, allow you to review your progress, adjust your strategies as life circumstances change, and stay focused on your long-term objectives.

- Building an Emergency Fund: Having an accessible emergency fund (typically 3-6 months of living expenses) is crucial. It prevents you from needing to tap into your long-term investments during unexpected crises, thus preserving the power of compounding.

Conclusion

Compound interest is undeniably a cornerstone of successful personal finance and wealth creation. It transforms modest beginnings into substantial fortunes, not through magic, but through the simple, consistent application of time, discipline, and strategic investment. By understanding its mechanics, maximizing its key variables, and consciously making choices to start early, invest consistently, and minimize financial drags like fees and taxes, anyone can harness this “eighth wonder of the world.” The journey of compounding may begin slowly, but with unwavering patience and a commitment to long-term vision, its exponential power will ultimately deliver profound financial rewards, paving the way for financial independence and security.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.