In the realm of personal finance, business operations, and investment strategies, percentages are not just mathematical constructs; they are the bedrock upon which sound financial decisions are built. Among the myriad percentage calculations one might encounter, understanding “how to calculate 20 percentage of total” stands out as particularly crucial. The 20% figure appears with striking frequency across various financial domains, from down payments on homes to savings goals, investment allocations, and even everyday consumer discounts and gratuities. Mastering this calculation is more than just a numerical exercise; it’s a fundamental skill that empowers individuals and businesses to better understand their financial landscape, make informed choices, and work towards their monetary objectives with greater precision and confidence.

This guide will delve into the various methods of calculating 20% of a total, explore its widespread applications in finance, and provide insights into leveraging this simple yet powerful concept for enhanced financial literacy and decision-making. By the end, you’ll not only be proficient in the calculation but also appreciate the significant role 20% plays in shaping your financial future.

The Fundamental Importance of Percentages in Finance

Percentages provide a standardized way to express proportions and relative values, making it easier to compare different quantities and understand their significance within a larger whole. In finance, where numbers can often be large and complex, percentages simplify communication and allow for quick assessment of financial health, performance, and risk.

Imagine trying to understand a company’s profit margin without percentages, or evaluating the interest rate on a loan solely by the absolute dollar amount. It would be incredibly challenging. Percentages abstract these figures into a universally understood scale, allowing for direct comparison across different scales and contexts. They are essential for tracking growth, measuring change, analyzing costs, and distributing resources effectively.

Why 20% is a Common Financial Benchmark

The number 20% holds a unique, almost iconic, status in finance, frequently appearing as a recommended benchmark or critical threshold. This isn’t arbitrary; it reflects a practical balance between significant commitment and achievable goals.

For instance, a 20% down payment on a home is often seen as the gold standard, helping buyers avoid Private Mortgage Insurance (PMI) and secure more favorable loan terms. In personal savings, financial advisors frequently recommend saving at least 20% of one’s income, often referred to as the “20% rule” or a component of the “50/30/20 rule” (50% for needs, 30% for wants, 20% for savings and debt repayment). This benchmark provides a solid foundation for building an emergency fund, saving for retirement, or accumulating wealth for future goals.

In business, a 20% profit margin can indicate a healthy operation, while a 20% discount can be a significant marketing incentive. Even in gratuities, 20% has become a widely accepted standard for excellent service. This ubiquity means that understanding how to quickly and accurately calculate 20% is not just academic but directly applicable to numerous real-world financial scenarios, making it an indispensable skill for anyone managing money.

Beyond Basic Calculations: Understanding Proportions

While calculating 20% is a straightforward mathematical operation, its true power in finance comes from understanding the underlying concept of proportions. A percentage represents a part out of a hundred. When we calculate 20% of a total, we are essentially determining what portion of that total is equivalent to twenty parts out of every hundred.

This understanding allows for deeper financial analysis. For example, knowing that your debt payments represent 20% of your gross income signals a healthy debt-to-income ratio in many cases. If your investment portfolio allocates 20% to a specific asset class, you understand its relative weight and potential impact on overall performance. This proportional thinking extends beyond simple calculations, enabling more sophisticated analysis of financial statements, budget allocations, and risk management strategies.

Step-by-Step Calculation Methods

Calculating 20% of any total is a simple process, and there are several methods you can use depending on your preference and the tools available. Each method yields the same accurate result, so choose the one that feels most intuitive to you.

Method 1: The Decimal Approach

This is arguably the most common and universally applicable method. To find a percentage of a number, you convert the percentage into its decimal equivalent and then multiply it by the total.

- Convert 20% to a decimal: To do this, divide the percentage by 100.

20 ÷ 100 = 0.20 - Multiply the decimal by the total: Take your decimal (0.20) and multiply it by the total amount.

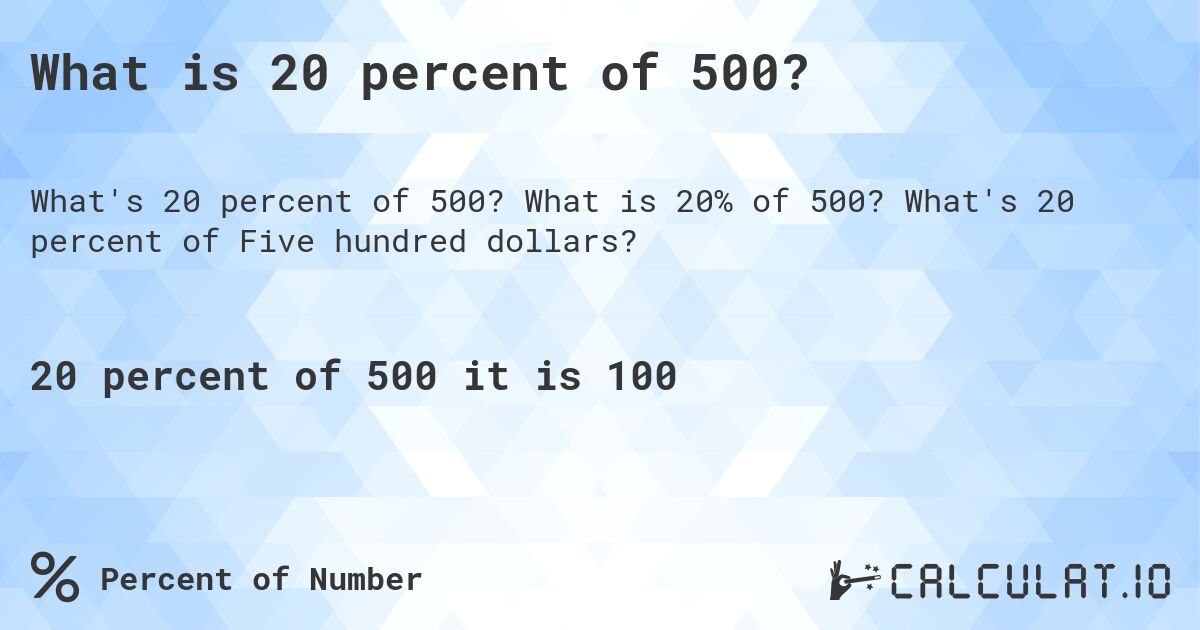

Example: Calculate 20% of $500.

$500 * 0.20 = $100

This method is highly efficient, especially when using calculators, spreadsheets, or programming, as it directly translates the percentage into a workable numerical factor.

Method 2: The Fractional Approach

This method leverages the fact that 20% can be expressed as a simple fraction. Since 20% means 20 out of 100, the fraction is 20/100, which simplifies to 1/5.

- Convert 20% to a fraction: 20/100 = 1/5

- Multiply the total by the fraction (or divide by the denominator): To find 1/5 of a number, you simply divide that number by 5.

Example: Calculate 20% of $500.

$500 * (1/5) = $100

OR

$500 / 5 = $100

The fractional approach is particularly useful for mental math or quick estimates, as dividing by 5 is often easier than multiplying by 0.20 for many people. It underscores that finding 20% is equivalent to finding one-fifth of the total.

Method 3: The Proportion Approach

This method is based on setting up a ratio and solving for the unknown. It’s a more fundamental algebraic way to think about percentages.

- Set up the proportion:

(Part / Total) = (Percentage / 100)

In our case, we know the percentage (20) and the total, and we want to find the part.

(X / Total) = (20 / 100) - Solve for X (the part): Cross-multiply or isolate X.

Example: Calculate 20% of $500.

(X / $500) = (20 / 100)

100 * X = 20 * $500

100X = $10,000

X = $10,000 / 100

X = $100

While slightly more involved for a simple 20% calculation, the proportion approach is powerful because it can be used to solve for any unknown variable (the part, the total, or the percentage) if the other two are known. This makes it a versatile tool for various financial calculations beyond just finding a percentage of a total.

Practical Applications of 20% in Personal Finance

The ability to calculate 20% of a total is not just an academic exercise; it’s a vital skill with direct, tangible applications across nearly every facet of personal finance.

Budgeting and Savings: The 20% Rule

One of the most frequently cited benchmarks in personal finance is the recommendation to save at least 20% of your net income. This “20% rule” is often a core component of popular budgeting frameworks like the 50/30/20 rule.

- Calculating Savings Goals: If your monthly net income is $4,000, 20% of that is $4,000 * 0.20 = $800. This is the minimum amount you should aim to allocate to savings, investments, or debt repayment beyond minimums.

- Emergency Fund: Building an emergency fund often involves saving 3-6 months’ worth of essential expenses. Calculating 20% of your income consistently can help you reach this goal faster.

- Retirement Contributions: Many retirement planning tools recommend contributing a significant percentage of your income to retirement accounts, with 10-15% being a common starting point, but 20% offering a more aggressive path to financial independence.

Debt Management: Down Payments and Repayment Strategies

The 20% figure frequently appears in discussions about debt, particularly mortgages and other large loans.

- Mortgage Down Payments: As mentioned, a 20% down payment on a home is often ideal. For a $300,000 home, this means $300,000 * 0.20 = $60,000. This avoids Private Mortgage Insurance (PMI) and typically results in lower interest rates and monthly payments.

- Student Loan or Car Loan Strategies: While less common for initial down payments, using the 20% rule to allocate extra funds towards loan principal can significantly reduce interest paid and shorten the loan term. For example, if your minimum payment is $200, paying an extra 20% ($40) can accelerate debt payoff.

Investing: Portfolio Allocation and Goal Setting

Investors often use percentages to allocate their assets and set realistic targets.

- Asset Allocation: A common strategy might be to allocate 20% of a portfolio to a specific sector, geographic region, or asset class (e.g., 20% in international stocks, 20% in real estate investment trusts). Understanding this helps manage risk and diversify investments.

- Return Targets: While not guaranteed, investors might set a goal to achieve a 20% return on a particular investment over a specific period. Calculating 20% of their initial capital helps them quantify this target.

- Rebalancing: When a portfolio drifts due to market performance, investors might rebalance to restore their original 20% allocation to an asset, buying or selling as needed.

Consumer Spending: Discounts, Tips, and Sales Tax Estimation

In everyday transactions, calculating 20% is incredibly useful for navigating pricing and service charges.

- Discounts and Sales: Spotting a “20% off” sign is common. Knowing how to quickly calculate this discount (e.g., 20% off a $75 item is $15) allows you to understand the actual price and value proposition.

- Tipping Etiquette: Tipping 20% for excellent service has become standard in many service industries. If your meal bill is $60, a 20% tip is $12 ($60 * 0.20).

- Sales Tax (Estimation): While sales tax rates vary, if a local sales tax is around 8-10%, being able to calculate 20% of the item price can give you a quick, rough upper estimate of the total cost with tax, allowing for better budget management while shopping.

Leveraging Financial Tools for Percentage Calculations

While mental math and manual calculations are valuable, modern financial tools can simplify and enhance the accuracy of percentage calculations, especially with larger numbers or complex scenarios.

Spreadsheets: Excel and Google Sheets Formulas

Spreadsheets are indispensable for financial management, and calculating percentages is one of their core strengths.

- Simple Calculation: If your total is in cell A1, you can calculate 20% by entering

=A1*0.20or=A1*20%into another cell. Both formulas yield the same result. The20%format in spreadsheets is automatically interpreted as0.20. - Dynamic Budgeting: You can create a budget where your savings goal is always 20% of your income. If your income is in cell B2, and you want to see your 20% savings in C2, simply enter

=B2*0.20in C2. When B2 changes, C2 automatically updates. - Scenario Planning: Use percentages in what-if scenarios, such as calculating potential loan payments with varying down payments or projecting investment returns based on different growth rates.

Online Calculators and Mobile Apps

The internet is replete with financial calculators, and most mobile banking or budgeting apps also incorporate percentage functionality.

- Dedicated Percentage Calculators: A quick search for “percentage calculator” will bring up numerous online tools where you can input the total and the percentage, and it will instantly give you the result.

- Budgeting Apps: Many apps allow you to set percentage-based budgets, automatically categorizing and calculating your spending and savings percentages relative to your income.

- Loan Calculators: These often require inputting down payment percentages to calculate monthly payments, showcasing how 20% impacts loan affordability.

The Power of Mental Math for Quick Estimates

While tools are great for precision, the ability to quickly estimate 20% mentally is a powerful skill for on-the-spot financial decisions.

- The “Divide by Five” Trick: As discussed in the fractional approach, 20% is 1/5. Mentally dividing a number by 5 is often quite manageable. For $80, 20% is $16 (80/5). For $150, 20% is $30 (150/5).

- The “Ten Percent Twice” Method: Another excellent mental shortcut is to calculate 10% and then double it. To find 10% of a number, simply move the decimal point one place to the left. For $250, 10% is $25. Double that, and 20% is $50. This is particularly useful for tipping or quick discount calculations.

Common Pitfalls and Advanced Considerations

While calculating 20% seems simple, there are nuances and potential pitfalls to be aware of, particularly in more complex financial situations.

Understanding the “Total”: Base Value Importance

One of the most common errors in percentage calculations is misidentifying the “total” or the base value upon which the percentage is applied.

- Gross vs. Net Income: When saving 20%, is it 20% of your gross income (before taxes and deductions) or net income (take-home pay)? Most financial advisors recommend net income for budgeting, as it reflects the money you actually have available.

- Pre-Tax vs. Post-Tax Prices: When calculating discounts or sales tax, ensure you’re applying the percentage to the correct base. A 20% discount on an item is applied to its original price before any sales tax is added. Sales tax is then applied to the discounted price.

- Investment Basis: When calculating a 20% gain or loss, ensure you’re using the original cost basis of the investment, not its current market value, as the total.

Percentage Increase vs. Percentage Decrease

It’s crucial to distinguish between a 20% increase and a 20% decrease.

- 20% Increase: If an item costs $100 and increases by 20%, the new price is $100 + ($100 * 0.20) = $100 + $20 = $120.

- 20% Decrease: If an item costs $100 and decreases by 20%, the new price is $100 – ($100 * 0.20) = $100 – $20 = $80.

While the calculation for the amount of change is the same, how it’s applied (added or subtracted) is critical.

The Impact of Compounding and Sequential Percentages

In finance, particularly with investments or interest, percentages don’t always operate in isolation, especially over time.

- Compounding: Earning 20% interest annually on an investment that compounds means that in subsequent years, the 20% is applied to a larger total (original principal + accumulated interest). This is the “magic” of compound interest.

- Sequential Changes: It’s a common misconception that a 20% increase followed by a 20% decrease will bring you back to the original total. This is incorrect because the base for the second percentage change is different.

- Start with $100.

- Increase by 20%: $100 * 1.20 = $120.

- Decrease by 20%: $120 * 0.80 = $96.

You end up with $96, not $100. This is a critical concept in understanding investment gains/losses or price fluctuations.

By being mindful of these considerations, you can avoid common financial miscalculations and apply your understanding of 20% more effectively in diverse monetary contexts.

The ability to calculate 20% of a total is far more than a basic arithmetic skill; it’s a foundational element of financial literacy. From meticulously planning a budget and making a substantial down payment on a home to strategically diversifying an investment portfolio and confidently navigating consumer transactions, the 20% benchmark consistently serves as a guidepost. By mastering the simple calculation methods, understanding its myriad applications in personal finance, and leveraging available tools while being aware of common pitfalls, you equip yourself with a powerful capability. This skill empowers you to make smarter financial decisions, achieve your monetary goals with greater precision, and ultimately, build a more secure and prosperous financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.