For ambitious entrepreneurs and established small business owners alike, securing a loan can be the catalyst for pivotal growth, strategic expansion, or crucial operational stability. Whether you’re looking to purchase new equipment, expand your inventory, hire more staff, or simply navigate a period of tight cash flow, understanding how to effectively obtain a small business loan is fundamental to your enterprise’s financial health and future success. This guide will walk you through the intricate landscape of small business financing, equipping you with the knowledge and steps necessary to secure the capital you need.

Understanding Small Business Loans: Your Foundation for Growth

Before diving into the application process, it’s crucial to understand what small business loans entail, why they are a common necessity, and what fundamental considerations you must make as a borrower.

Why Small Businesses Need Loans

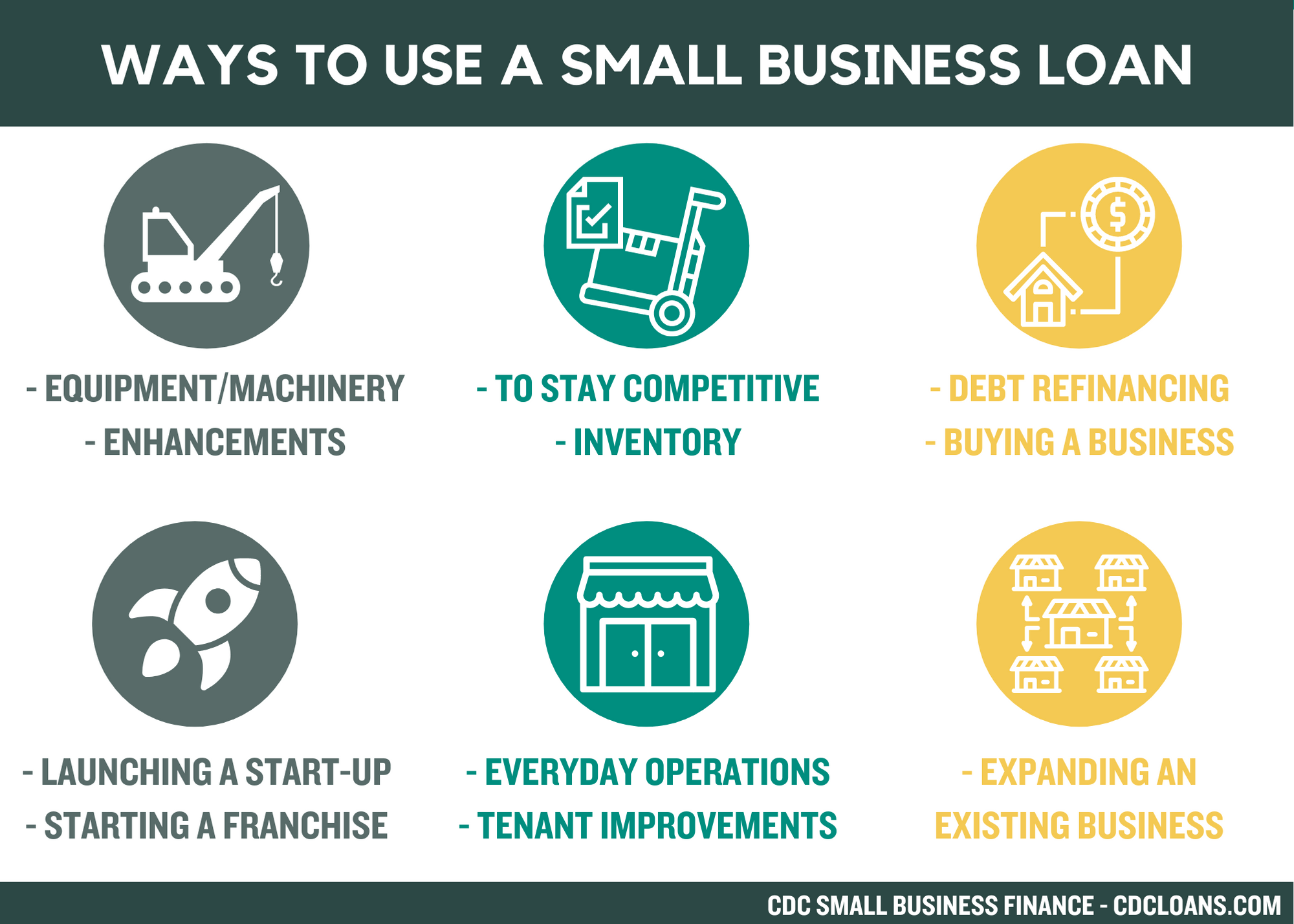

Small businesses often operate with lean budgets, making external funding a critical component of their operational strategy and growth trajectory. Loans serve various vital purposes:

- Working Capital: To cover day-to-day operational expenses like rent, utilities, payroll, and supplies, ensuring smooth business continuity.

- Inventory Purchase: To stock up on goods, especially for seasonal demand or when expanding product lines, preventing lost sales due to stockouts.

- Equipment Acquisition: For purchasing essential machinery, vehicles, or technology that enhances productivity, efficiency, or service delivery.

- Business Expansion: To fund the opening of new locations, entering new markets, or significantly scaling up existing operations.

- Emergency Funding: To provide a safety net for unexpected expenses, economic downturns, or unforeseen challenges that could otherwise cripple the business.

- Debt Consolidation: To combine multiple high-interest debts into a single, more manageable loan with better terms.

Key Considerations Before Seeking Funding

Approaching a lender without a clear understanding of your needs and capacity can be a costly mistake. Prioritize these considerations:

- Assess Your True Need: Clearly define why you need the loan and how the funds will be utilized. A well-articulated purpose demonstrates foresight and responsibility to potential lenders. Is it a short-term cash flow gap, or a long-term investment in growth?

- Evaluate Repayment Capacity: This is paramount. Lenders will scrutinize your ability to repay the loan on time, every time. Conduct a thorough analysis of your current and projected cash flow to determine a comfortable repayment amount. Over-leveraging can lead to significant financial strain.

- Align with Your Business Plan: Your loan application should seamlessly integrate with your overarching business strategy. How does this funding support your mission, vision, and strategic objectives? Lenders want to see that the loan is a strategic move, not a desperate plea.

Preparing Your Business for Lender Scrutiny

Securing a small business loan is often a competitive process. Lenders are looking for reliable borrowers with a strong potential for repayment. Thorough preparation is key to presenting your business in the best possible light.

The Importance of a Solid Business Plan

Your business plan is the cornerstone of your loan application. It’s more than just a document; it’s your narrative, vision, and strategic roadmap. A comprehensive business plan should include:

- Executive Summary: A concise overview of your business, its mission, and its goals.

- Company Description: Details about your legal structure, history, and what makes your business unique.

- Market Analysis: A thorough understanding of your industry, target market, competitors, and competitive advantages.

- Organization and Management: Information about your management team, their experience, and legal structure.

- Service or Product Line: Detailed descriptions of what you offer and their value proposition.

- Marketing and Sales Strategy: How you plan to reach customers and generate revenue.

- Financial Projections: The most critical section for lenders, including historical financial data (if available) and detailed forecasts for the next 3-5 years (profit and loss statements, balance sheets, cash flow projections). These must be realistic and well-supported.

Financial Health and Documentation

Lenders are primarily interested in numbers. Organized, accurate financial documentation is non-negotiable. Gather the following:

- Business Bank Statements: Typically for the last 12-24 months.

- Business Tax Returns: For the last 2-3 years.

- Profit & Loss (P&L) Statements: Also known as Income Statements, showing revenue, costs, and profits over a period.

- Balance Sheets: Snapshot of your business’s assets, liabilities, and equity at a specific point in time.

- Cash Flow Projections: Detailed forecasts of money coming in and going out, demonstrating your ability to meet future obligations.

- Accounts Receivable and Payable Aging Reports: To show the health of your cash cycle.

Personal Credit Score and Business Credit Score

Lenders assess both your personal and business creditworthiness.

- Personal Credit Score: For small businesses, particularly startups or those without a long operational history, the owner’s personal credit score (FICO score) is a significant factor. A higher score (generally 680+) indicates responsible financial behavior and improves your chances of approval and better terms.

- Business Credit Score: As your business grows, it establishes its own credit profile. Lenders will review scores from agencies like Dun & Bradstreet, Experian Business, and Equifax Business. Maintaining a strong business credit score is crucial for future financing.

Collateral and Guarantees

Many small business loans require some form of security for the lender.

- Collateral: Assets pledged by the borrower to secure the loan, which the lender can seize if the borrower defaults. Common forms of collateral include real estate, equipment, inventory, accounts receivable, and even intellectual property.

- Personal Guarantee: Often required, especially for small businesses. This means the business owner is personally responsible for repaying the loan if the business cannot. This significantly increases the lender’s security.

Exploring Your Funding Avenues: Types of Small Business Loans

The world of small business financing offers a diverse range of products, each suited for different needs and business profiles. Understanding your options is key to choosing the right fit.

Traditional Bank Loans

These are offered by conventional financial institutions. They typically offer competitive interest rates and longer repayment terms, but often have stringent qualification requirements and a slower application process.

- Pros: Lower interest rates, longer terms, established relationship with a bank.

- Cons: Strict eligibility criteria (strong credit, revenue, collateral), lengthy approval process.

- Best for: Established businesses with solid financial history and collateral.

SBA Loans (Small Business Administration)

The U.S. Small Business Administration (SBA) doesn’t lend money directly, but guarantees a portion of loans made by participating lenders (banks, credit unions). This guarantee reduces the risk for lenders, making it easier for small businesses to qualify for loans with favorable terms.

- SBA 7(a) Loan Program: The most common and flexible SBA loan, used for a wide range of purposes including working capital, equipment, real estate, and refinancing debt.

- SBA 504 Loan Program: Provides long-term, fixed-rate financing for major fixed assets like real estate or machinery.

- SBA Microloan Program: Smaller loans (up to $50,000) for startups and small businesses, often with technical assistance.

- Pros: Lower down payments, longer repayment periods, competitive interest rates.

- Cons: Extensive paperwork, slower approval process than some alternatives, strict eligibility requirements.

- Best for: Businesses that meet SBA criteria and can wait for approval.

Online Lenders and Fintech Platforms

In recent years, online lenders have emerged as a popular alternative, known for speed and convenience. They often have less stringent requirements than traditional banks.

- Pros: Fast application and approval times, less paperwork, more flexible criteria (some cater to businesses with less-than-perfect credit).

- Cons: Often higher interest rates, shorter repayment terms, may include various fees.

- Best for: Businesses needing quick access to capital, or those who don’t qualify for traditional bank loans.

Lines of Credit

A flexible financing option that allows businesses to borrow up to a certain limit, repay it, and then borrow again. Interest is only paid on the amount borrowed.

- Pros: Flexibility, ideal for managing cash flow fluctuations or unexpected expenses.

- Cons: Can have higher interest rates than term loans, often requires collateral.

- Best for: Managing working capital, bridging short-term cash flow gaps.

Equipment Financing and Invoice Factoring

These are specialized financing options for specific needs.

- Equipment Financing: A loan specifically for purchasing new or used equipment, where the equipment itself serves as collateral.

- Pros: Easier to qualify, lower down payments, preserves working capital.

- Cons: Only covers equipment, can have higher interest rates than general business loans.

- Invoice Factoring (Accounts Receivable Financing): Selling your unpaid invoices to a third party (a “factor”) at a discount for immediate cash.

- Pros: Quick access to cash tied up in receivables, good for businesses with long payment cycles.

- Cons: Expensive, reduces your profit margins, customer relationships can be impacted.

Merchant Cash Advances (MCAs)

A high-cost, short-term advance based on a business’s future credit card sales. The lender takes a percentage of daily credit card sales until the advance is repaid.

- Pros: Very fast funding, minimal qualifications, ideal for businesses with high credit card sales.

- Cons: Extremely expensive (high effective APR), short repayment terms, can trap businesses in a cycle of debt.

- Best for: Businesses with urgent, short-term cash needs and high credit card sales, as a last resort.

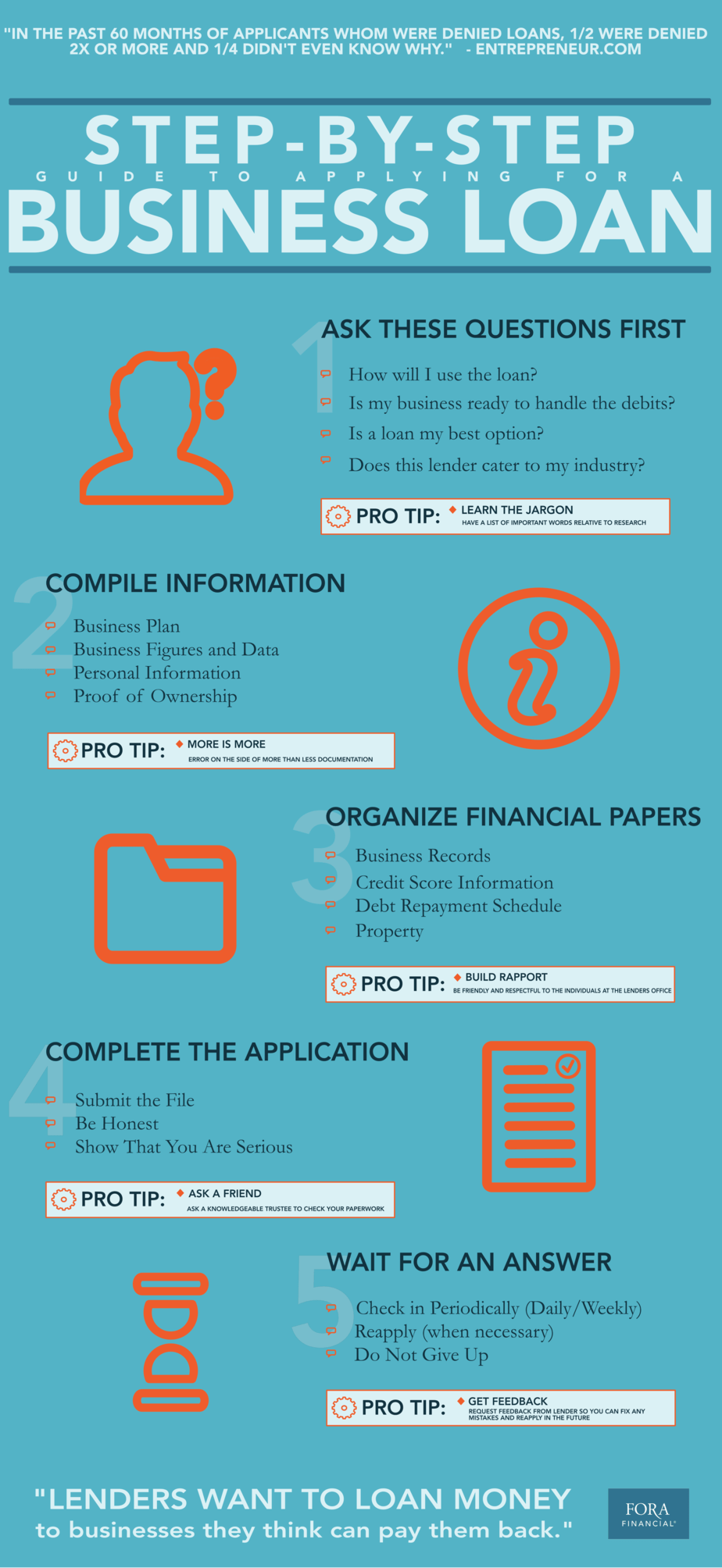

Navigating the Application Process: A Step-by-Step Guide

Once you’ve done your homework and chosen a suitable loan type, the application process itself requires diligence and attention to detail.

Researching and Comparing Lenders

Don’t jump at the first offer. Shop around and compare offers from multiple lenders:

- Interest Rates and APR: Look beyond the nominal interest rate to the Annual Percentage Rate (APR), which includes all fees and costs.

- Repayment Terms: Understand the loan duration, frequency of payments, and any prepayment penalties.

- Fees: Watch out for origination fees, application fees, closing costs, and late payment penalties.

- Lender Reputation: Read reviews, check their standing with the Better Business Bureau, and ask for references.

- Customer Service: Gauge their responsiveness and willingness to answer your questions.

Gathering Essential Documents

Create a comprehensive checklist based on your chosen lender’s requirements. This often includes:

- Completed loan application form.

- Business plan.

- Personal and business tax returns (2-3 years).

- Business financial statements (P&L, Balance Sheet, Cash Flow, AR/AP aging).

- Business bank statements (12-24 months).

- Personal financial statement (for owners).

- Resumes of key management.

- Legal documents (business registration, licenses, articles of incorporation).

- Collateral documents (if applicable).

Submitting Your Application

Whether online or in-person, ensure all information is accurate, consistent, and clearly presented. Any discrepancies or omissions can delay or jeopardize your application. Be prepared to answer follow-up questions promptly.

Understanding Loan Offers and Terms

If approved, you’ll receive a loan offer. This is the time to scrutinize every detail:

- Principal Amount: The total amount you are borrowing.

- Interest Rate and APR: The cost of borrowing.

- Repayment Schedule: Monthly, weekly, or daily payments, and the total duration.

- Collateral Requirements: What assets are pledged.

- Personal Guarantees: Who is liable if the business defaults.

- Covenants: Specific conditions or restrictions imposed by the lender (e.g., maintaining certain financial ratios, not taking on additional debt without permission).

- Prepayment Penalties: Fees for paying off the loan early.

Don’t hesitate to negotiate terms if you believe you have a strong case.

The Underwriting Process and Approval

After submission, the lender’s underwriting team will thoroughly evaluate your application, financial health, creditworthiness, and business viability. This can involve extensive background checks, financial analysis, and interviews. If everything aligns, you’ll receive final approval and the funds will be disbursed.

Beyond Approval: Managing Your Loan and Future Growth

Securing a loan is a milestone, but the journey doesn’t end there. Responsible management is critical for both the success of your business and your ability to access future financing.

Responsible Loan Management

- Timely Payments: This is non-negotiable. Missing payments can damage your credit score, incur late fees, and harm your relationship with the lender.

- Monitor Cash Flow: Continuously track your business’s cash inflows and outflows to ensure you always have sufficient funds to cover loan repayments and operational expenses.

- Adhere to Covenants: If your loan includes covenants, diligently comply with them to avoid triggering a default clause.

Building Lender Relationships

A positive relationship with your lender can be invaluable. Regular communication, especially if you foresee any challenges, can foster trust and potentially lead to more favorable terms on future loans or lines of credit. A lender who understands and trusts your business is a powerful ally.

Exploring Other Funding Options

While this article focuses on loans, it’s worth noting that the broader landscape of business finance includes other avenues you might explore for future growth, such as grants, venture capital, angel investors, or crowdfunding. These options are typically suited for specific types of businesses or growth stages and each comes with its own set of requirements and implications.

In conclusion, navigating the process of getting a small business loan requires thorough preparation, a clear understanding of your financial needs, and careful consideration of the various funding options available. By approaching this endeavor strategically and diligently, you can secure the capital necessary to propel your small business toward sustained success and robust growth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.