Embarking on the journey of entrepreneurship is an exhilarating prospect, a leap of faith for many, and a meticulously calculated risk for others. While the allure of autonomy and innovation is strong, the bedrock upon which every successful business is built is its financial strategy. Understanding how to conceptualize, fund, operate, and scale your venture from a financial perspective is not just crucial – it is the business itself. This guide delves into the essential monetary considerations and strategic financial planning required to transform a fledgling idea into a thriving enterprise.

I. Laying the Financial Foundation: From Ideation to Viability

The genesis of any business begins with an idea, but for that idea to manifest as a profitable entity, it must pass rigorous financial scrutiny. This initial phase is about ensuring your concept holds economic promise and mapping out the financial contours of your nascent venture.

Identifying a Profitable Niche and Validating Your Idea

Before a single dollar is spent, the entrepreneur must answer a fundamental question: Is there a market for what I want to offer, and are customers willing to pay for it? This isn’t just about demand; it’s about profitable demand. Researching your target market, identifying unmet needs, and assessing the competitive landscape are financial exercises at heart. A unique value proposition that solves a real problem often commands a premium, indicating higher revenue potential.

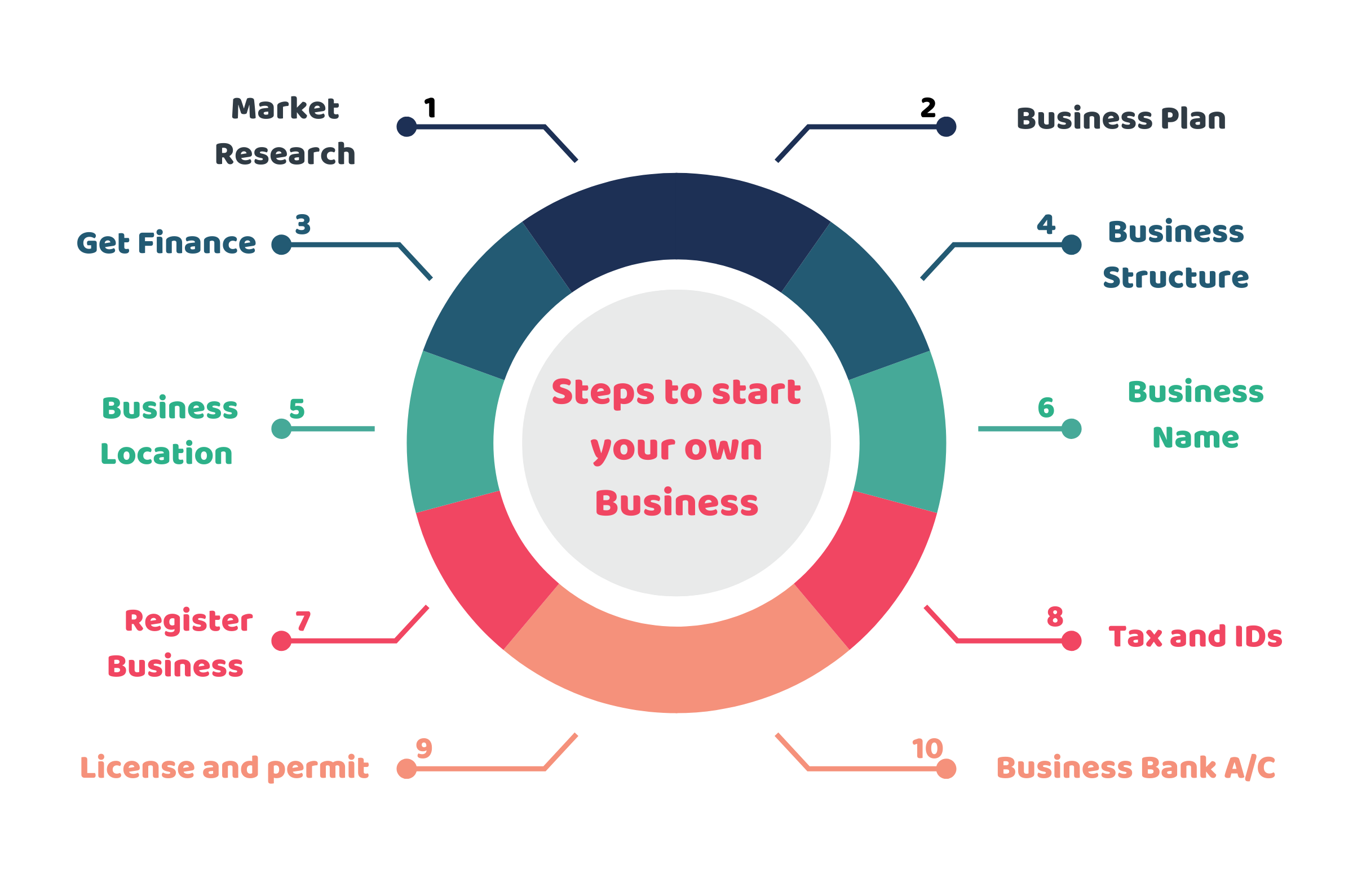

- Market Research: Understand the size, growth potential, and spending habits of your target audience.

- Competitor Analysis: Evaluate the pricing strategies, cost structures, and profitability of existing players. Can you offer something better, cheaper, or more unique?

- Problem-Solution Fit: Does your product or service genuinely address a significant pain point for customers, making them eager to part with their money?

- Value Proposition: Clearly articulate what makes your offering superior or distinct, justifying its price point and ensuring market acceptance.

Validation isn’t just about enthusiasm; it’s about securing early commitments, pre-orders, or letters of intent that signify actual monetary interest. This groundwork ensures you’re not building a business that nobody wants to pay for.

Initial Capital Assessment: Bootstrapping vs. Funding

Once your idea shows promise, the next financial hurdle is determining how much money you’ll need to get started and where that money will come from. This critical assessment shapes your business model and dictates your early operational capabilities.

- Startup Costs: Catalog every conceivable expense required before you can generate revenue. This includes legal fees, licenses, permits, equipment, initial inventory, website development, marketing collateral, office rent (if applicable), and salaries for initial hires. Be exhaustive and realistic; underestimating costs is a common pitfall.

- Operating Expenses: Beyond startup, project your monthly burn rate—the amount of money your business spends before it starts making a profit. This includes rent, utilities, salaries, marketing, supplies, and administrative costs.

- Cash Reserves: It’s prudent to have several months’ worth of operating expenses in reserve to weather initial lean periods and unexpected challenges. This financial buffer is crucial for survival.

The decision between bootstrapping (self-funding, minimal external capital) and seeking external funding (loans, investors) is a strategic financial choice. Bootstrapping offers control and avoids debt/equity dilution but limits growth speed. External funding can accelerate growth but comes with financial obligations or relinquishing a share of your company.

Crafting a Robust Business Plan with Financial Projections

A comprehensive business plan isn’t merely a document for investors; it’s a financial roadmap for you. Its core lies in detailed financial projections, translating your vision into tangible numbers.

- Revenue Projections: Forecast your sales based on market research, pricing strategies, and anticipated customer acquisition rates. Be conservative initially, then model optimistic scenarios.

- Cost of Goods Sold (COGS) / Cost of Services: Calculate the direct costs associated with producing your product or delivering your service.

- Operating Expenses: Detail all indirect costs required to run your business.

- Profit & Loss (P&L) Statement: Project your revenue, COGS, and expenses to arrive at your net profit over specific periods (monthly, quarterly, annually).

- Cash Flow Statement: Crucial for understanding liquidity, this projects the actual movement of cash in and out of your business. A profitable business can still fail if it runs out of cash.

- Balance Sheet: Offers a snapshot of your company’s financial health at a specific point in time, detailing assets, liabilities, and owner’s equity.

- Break-Even Analysis: Determine the sales volume needed to cover all your costs, marking the point where your business becomes profitable.

These financial statements are indispensable tools for making informed decisions, attracting financing, and monitoring your financial performance against your goals.

II. Securing the Funds: Funding Your Entrepreneurial Dream

With a solid financial plan in hand, the next step is to secure the capital needed to launch and sustain your business. This involves exploring various funding avenues, each with its own benefits and drawbacks.

Personal Savings and Bootstrapping: The Lean Approach

Many entrepreneurs begin by funding their ventures through personal savings, credit cards, or loans from friends and family. This “bootstrapping” approach minimizes external debt and equity dilution, allowing the founder to retain full control.

- Advantages: Full ownership, no debt repayments or interest initially, forces lean operations and financial discipline.

- Disadvantages: Limited capital, personal financial risk, slower growth potential.

- Strategy: Prioritize revenue generation from day one, minimize overheads, and reinvest profits judiciously.

Debt Financing: Loans, Lines of Credit, and Microfinancing

Debt financing involves borrowing money that must be repaid with interest, regardless of your business’s profitability. It’s suitable for businesses with predictable cash flows and collateral.

- Small Business Loans: Traditional bank loans require a strong business plan, credit history, and often collateral. Government-backed loans (e.g., SBA loans in the U.S.) can offer more favorable terms.

- Lines of Credit: Provides access to a flexible amount of money up to a certain limit, useful for managing working capital fluctuations. Interest is only paid on the amount drawn.

- Microfinancing: Smaller loans typically offered by non-profits or community development financial institutions to startups and small businesses, often in underserved communities.

- Pros: Retain full ownership, interest payments are tax-deductible.

- Cons: Fixed repayment schedule, personal guarantees often required, can strain cash flow if revenue is inconsistent.

Equity Financing: Angels, Venture Capital, and Crowdfunding

Equity financing involves selling a percentage of ownership in your company to investors in exchange for capital. These investors then share in the company’s profits and potential appreciation.

- Angel Investors: High-net-worth individuals who invest their own money, often providing mentorship along with capital. They typically invest earlier than VCs.

- Venture Capital (VC) Firms: Professional investors who manage funds from limited partners and invest in high-growth potential startups in exchange for significant equity. They seek substantial returns and often take a board seat.

- Equity Crowdfunding: Platforms that allow a large number of individuals to invest small amounts of money in a startup in exchange for equity.

- Pros: Provides substantial capital without debt repayment burden, investors often bring valuable expertise and networks.

- Cons: Dilution of ownership and control, pressure for rapid growth and high returns, lengthy fundraising process.

Grants and Accelerators: Non-Dilutive Funding Options

These options provide capital without requiring equity or repayment, making them highly attractive.

- Grants: Offered by government agencies, foundations, or corporations, often for businesses addressing specific social issues, engaging in R&D, or located in particular regions. Highly competitive.

- Business Accelerators: Programs that provide mentorship, resources, and often a small amount of seed funding in exchange for a small equity stake. They help startups rapidly grow and prepare for larger investment rounds.

- Pros: “Free money” (grants), invaluable mentorship and networking (accelerators).

- Cons: Very competitive, often have specific eligibility criteria, limited availability.

III. Operationalizing Your Finances: Managing Money for Growth

Securing funds is just the beginning. Effective financial management is crucial for the day-to-day operations and long-term health of your business.

Setting Up Business Bank Accounts and Accounting Systems

Separating personal and business finances is paramount for legal, tax, and organizational clarity.

- Business Bank Account: Essential for tracking business income and expenses, establishing credit, and streamlining tax preparation.

- Accounting Software: Implement robust accounting software (e.g., QuickBooks, Xero, FreshBooks) from the outset. This tracks transactions, generates financial reports, manages invoices, and simplifies payroll.

- Financial Team: Consider engaging a bookkeeper or accountant early on to ensure accuracy and compliance.

Budgeting and Cash Flow Management: The Lifeblood of Your Business

Poor cash flow management is a leading cause of business failure. A budget acts as a financial plan, while cash flow management monitors the actual flow of money.

- Operating Budget: Allocate funds for all expected expenses based on your financial projections. Regularly compare actual spending to your budget and adjust as necessary.

- Cash Flow Forecasting: Continuously project your incoming and outgoing cash. Identify potential shortfalls before they occur, allowing you to take proactive measures like deferring expenses or seeking short-term financing.

- Accounts Receivable Management: Implement clear invoicing and collection policies to ensure customers pay on time.

- Accounts Payable Management: Strategically manage when you pay your suppliers to optimize cash on hand, without damaging relationships.

Understanding Pricing Strategies and Revenue Models

Your pricing strategy directly impacts your revenue and profitability. It must align with your costs, market value, and competitive positioning.

- Cost-Plus Pricing: Adding a markup percentage to the cost of producing your product or service. Simple but may not reflect market value.

- Value-Based Pricing: Pricing based on the perceived value your product or service delivers to the customer, often allowing for higher margins.

- Competitive Pricing: Setting prices based on what competitors charge, often used in saturated markets.

- Subscription Models: Recurring revenue streams, offering predictability and customer loyalty.

- Freemium Models: Offering a basic service for free to attract users, then charging for premium features.

- Revenue Diversification: Explore multiple income streams to reduce reliance on a single source and mitigate risk.

Managing Business Expenses and Tax Obligations

Controlling expenses is as vital as generating revenue. Every dollar saved on costs directly contributes to your bottom line.

- Expense Tracking: Meticulously track all business expenses for budgeting, tax purposes, and identifying areas for cost reduction.

- Vendor Negotiation: Regularly review and negotiate contracts with suppliers and service providers.

- Tax Compliance: Understand your federal, state, and local tax obligations (income tax, sales tax, payroll tax). Failure to comply can result in severe penalties. Consult with a tax professional to ensure proper setup and filing.

- Deductibles: Be aware of all eligible business deductions to minimize your tax burden legally.

IV. Scaling Responsibly: Financial Growth Strategies

As your business gains traction, financial planning shifts from survival to sustainable growth. Scaling responsibly means making strategic financial decisions that support expansion without overextending your resources.

Reinvesting Profits for Sustainable Expansion

Once profitable, the question arises: distribute profits or reinvest them? Reinvesting earnings back into the business can fuel organic growth, allowing you to expand operations, develop new products, or enter new markets without taking on additional debt or equity.

- Strategic Allocation: Prioritize investments in areas that offer the highest return, such as R&D, marketing, talent acquisition, or infrastructure upgrades.

- Working Capital Management: Ensure sufficient working capital to support increased inventory, accounts receivable, and operational demands that come with growth.

- Controlled Expansion: Avoid growing too fast, which can strain cash flow and operational capabilities. Growth should be measured and supported by strong financial health.

Monitoring Key Financial Metrics for Performance

Continuous monitoring of your financial health is critical for identifying trends, making timely adjustments, and measuring progress against your strategic goals.

- Profit Margins: Gross profit margin, operating profit margin, and net profit margin indicate how efficiently your business converts revenue into profit.

- Burn Rate: Track how quickly your cash reserves are being depleted, especially in early stages or during periods of aggressive investment.

- Customer Acquisition Cost (CAC): The cost associated with acquiring a new customer. Essential for evaluating marketing effectiveness and scalability.

- Customer Lifetime Value (CLTV): The total revenue expected from a customer over their relationship with your business. Comparing CLTV to CAC indicates profitability.

- Return on Investment (ROI): Measure the profitability of specific investments or projects.

Strategic Financial Planning for Future Milestones

As your business matures, financial planning becomes more sophisticated, incorporating long-term goals like securing a second round of funding, considering an acquisition, or planning for an eventual exit.

- Long-Term Forecasts: Extend your financial projections further into the future (3-5 years) to model various growth scenarios and potential challenges.

- Valuation: Understand how your business is valued, which is crucial for attracting investors or preparing for a sale.

- Succession Planning: If applicable, plan for the financial implications of transitioning leadership or ownership.

- Risk Management: Identify potential financial risks (e.g., market downturns, supply chain disruptions, regulatory changes) and develop contingency plans.

Starting your own business is a marathon, not a sprint, and finance is the oxygen that keeps you running. By meticulously planning your financial foundation, shrewdly securing capital, diligently managing your operational finances, and strategically planning for growth, you not only increase your chances of survival but also pave the way for a truly impactful and profitable entrepreneurial journey. The business world is unforgiving of financial missteps, but for those who master its monetary intricacies, the rewards are boundless.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.