In an increasingly complex world, mastering the art of money management isn’t just a desirable skill; it’s a fundamental pillar of personal well-being, freedom, and future security. The phrase “how to handle money” encapsulates a journey that extends far beyond merely earning and spending. It delves into the realms of understanding, planning, saving, investing, and protecting one’s financial resources to achieve life’s aspirations and navigate unforeseen challenges. For many, the idea of financial mastery can feel overwhelming, shrouded in jargon and complex strategies. However, at its core, it’s a systematic approach to making informed decisions that align with your values and goals.

This comprehensive guide aims to demystify the process, offering actionable insights and a structured framework to help you take control of your financial destiny. Whether you’re just starting your career, planning for significant life events, or nearing retirement, the principles of sound money management remain universally applicable. By embracing a proactive and disciplined approach, you can transform your relationship with money, turning it from a source of stress into a powerful tool for building the life you envision. Let’s embark on this journey to cultivate financial intelligence and empower your future.

1. Understanding Your Financial Landscape

The initial step in effectively handling money is to gain a clear, honest picture of your current financial standing. You cannot chart a course without knowing your starting point. This foundational understanding sets the stage for all subsequent financial decisions and strategies.

Acknowledging Your Current Financial Position

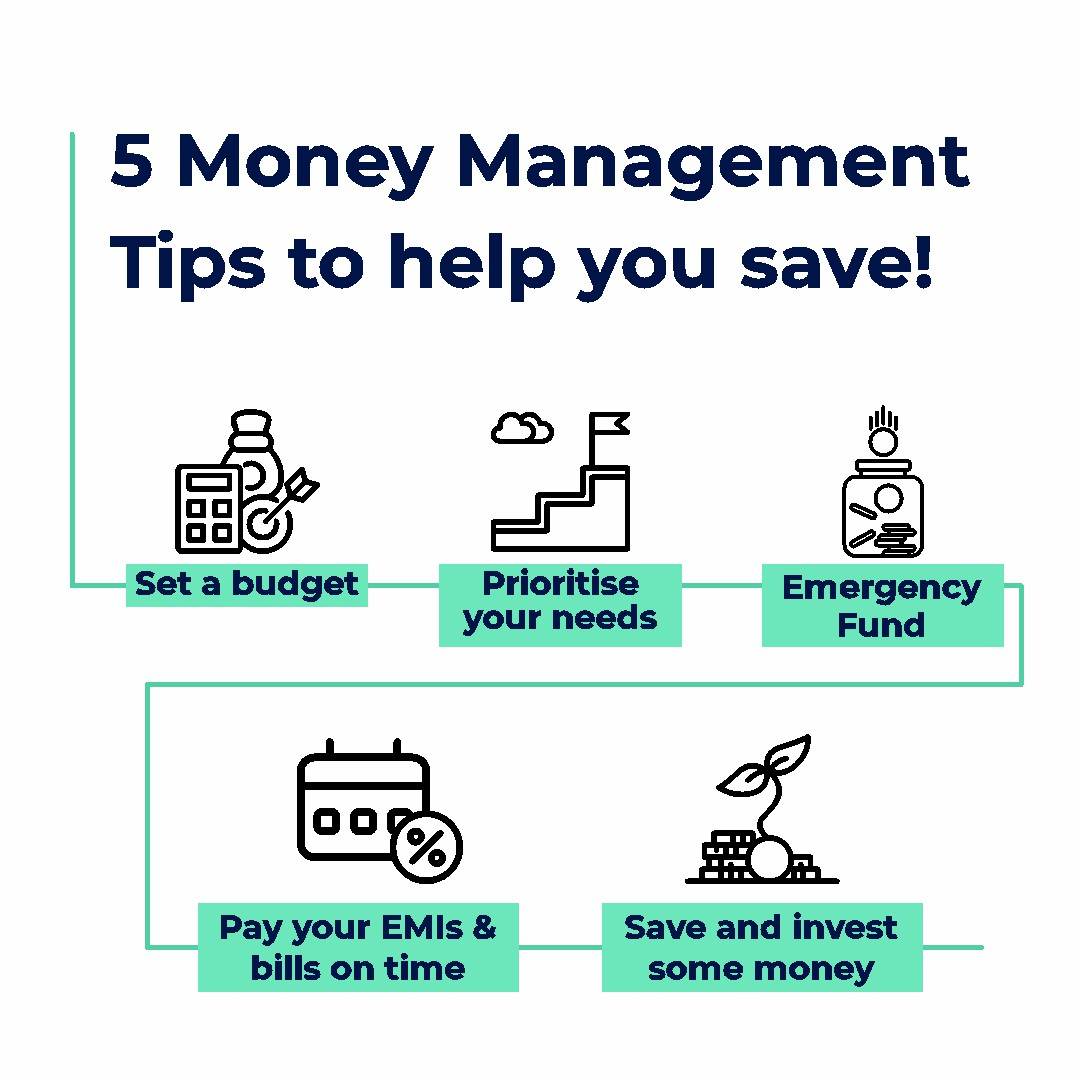

Start by performing a thorough financial health check. This involves a clear-eyed assessment of your assets (what you own – savings, investments, property) versus your liabilities (what you owe – debts, loans, mortgages). Calculate your net worth by subtracting your total liabilities from your total assets. This figure provides a snapshot of your financial health at a specific point in time. Equally critical is understanding your cash flow: the money coming in (income) versus the money going out (expenses). Track every dollar for a month or two to truly grasp where your money is flowing. Many are surprised to find how much discretionary spending accumulates. This exercise reveals spending habits, potential leakage points, and areas where immediate adjustments can be made. It’s a sobering but essential step toward conscious financial management.

Defining Your Financial Goals

Once you understand your present, it’s time to envision your future. What do you want your money to do for you? Financial goals provide direction and motivation. These can range from short-term objectives like saving for a vacation or a down payment on a car, to medium-term goals such as buying a home or funding a child’s education, and long-term aspirations like a comfortable retirement or starting a business. Make your goals SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For instance, instead of “save money,” aim for “save $10,000 for a down payment on a house in 3 years.” Clearly defined goals allow you to prioritize your financial efforts and allocate resources effectively, ensuring that every dollar has a purpose.

Developing a Financial Mindset

Beyond numbers and spreadsheets, a crucial component of money management is cultivating the right mindset. This involves shifting your perspective from one of scarcity or impulsive spending to one of abundance, patience, and strategic planning. Embrace financial literacy as a lifelong pursuit, understanding that knowledge empowers better decisions. Challenge limiting beliefs about money that may have been ingrained from childhood or societal influences. Recognize that money is a tool, not an end in itself, and its purpose is to serve your life goals. A positive and disciplined financial mindset fosters resilience, helps you resist instant gratification, and positions you to make choices that serve your long-term interests rather than fleeting desires.

2. Mastering Budgeting and Cash Flow Management

Budgeting is not about restriction; it’s about empowerment. It’s a proactive plan for your money, ensuring that every dollar serves a purpose, whether it’s for needs, wants, or future goals. Effective cash flow management is the engine that drives your financial plan forward.

The Power of Tracking

Before you can budget, you must track. Understanding precisely where your money goes is arguably the most enlightening step in personal finance. Utilize apps, spreadsheets, or even a simple notebook to meticulously record all income and expenses for at least one to three months. Categorize your spending (e.g., housing, food, transportation, entertainment). This practice uncovers spending patterns, identifies areas of overspending, and reveals “money leaks” – those small, often unnoticed expenses that add up significantly over time. Without tracking, budgeting is guesswork; with it, it becomes an informed and strategic exercise.

Choosing the Right Budgeting Method

There’s no one-size-fits-all budget, and the best method is the one you’ll stick to. Popular options include:

- The 50/30/20 Rule: 50% of your after-tax income for needs (housing, utilities, groceries), 30% for wants (dining out, entertainment, hobbies), and 20% for savings and debt repayment. It’s simple and flexible.

- Zero-Based Budgeting: Every dollar is assigned a job. Income minus expenses (including savings and debt payments) should equal zero. This method requires more discipline but offers immense control and clarity over your money.

- Envelope System: A tactile approach where cash for various categories is put into physical envelopes. Once an envelope is empty, spending in that category stops for the month. Ideal for those who struggle with overspending on specific items.

- Reverse Budgeting: Focus on saving first. Automate a percentage of your income to savings and investments, and then spend what’s left. This prioritizes future wealth over current consumption.

Experiment to find what resonates with your lifestyle and provides the most sustainable results.

Automating Your Finances

One of the most powerful strategies for consistent money management is automation. Set up automatic transfers for savings, investments, and bill payments. When a portion of your income is automatically diverted to your savings account or investment portfolio the moment it hits your bank, you significantly reduce the temptation to spend it. Similarly, automating bill payments ensures you never miss a due date, avoiding late fees and protecting your credit score. This “set it and forget it” approach builds consistency and discipline, allowing your financial plan to work seamlessly in the background.

Regularly Reviewing and Adjusting Your Budget

Life is dynamic, and so should be your budget. Economic changes, salary adjustments, new financial goals, or unexpected expenses all necessitate a review and potential adjustment of your budget. Make it a habit to review your budget monthly, or at least quarterly. Assess if your allocations still align with your goals and current reality. Are you consistently overspending in one area? Has your income changed? Did you achieve a specific savings goal? Regular reviews keep your budget relevant, effective, and a true reflection of your financial life, rather than a rigid, outdated document.

3. Building a Robust Financial Foundation

A strong financial foundation provides stability and resilience, enabling you to weather economic storms and pursue opportunities without undue stress. This involves prioritizing security before embarking on more aggressive wealth accumulation.

The Imperative of an Emergency Fund

The cornerstone of financial security is a well-funded emergency savings account. This dedicated fund should cover 3 to 6 months’ worth of essential living expenses, providing a critical buffer against unforeseen events like job loss, medical emergencies, or significant home repairs. Without an emergency fund, unexpected costs often lead to taking on high-interest debt, derailing other financial goals. Keep this fund in an easily accessible, high-yield savings account, separate from your everyday checking account, to minimize the temptation to tap into it for non-emergencies. It’s not about making money; it’s about buying peace of mind.

Strategically Tackling Debt

Not all debt is created equal. Understanding the difference between “good” debt (e.g., a mortgage or student loan with reasonable interest rates that can build equity or human capital) and “bad” debt (e.g., high-interest credit card debt, payday loans) is crucial. Prioritize eliminating high-interest “bad” debt as aggressively as possible. Two popular strategies are:

- Debt Snowball Method: Pay off the smallest debt first, then roll that payment into the next smallest. This provides psychological wins, maintaining momentum.

- Debt Avalanche Method: Focus on paying off the debt with the highest interest rate first, saving you the most money in interest over time.

Choose the method that best motivates you to stick with the plan. As you pay off debts, redirect those “freed up” funds towards savings and investments, accelerating your journey towards financial independence.

Understanding Your Credit Score

Your credit score is a numerical representation of your creditworthiness, impacting everything from loan interest rates to rental applications and even insurance premiums. A strong credit score (generally above 700) signifies responsible financial behavior. Understand the factors that influence your score: payment history (the most critical), amounts owed, length of credit history, new credit, and credit mix. Regularly monitor your credit report for errors and signs of identity theft. By making timely payments, keeping credit utilization low, and avoiding opening too many new accounts simultaneously, you can build and maintain a healthy credit score, unlocking better financial opportunities and terms.

4. Growing Your Wealth Through Strategic Investing

Once your financial foundation is solid, the next logical step is to make your money work harder for you through strategic investing. Investing allows your capital to grow over time, outpacing inflation and significantly accelerating your journey towards financial independence.

Demystifying Investment Basics

At its heart, investing is simply putting money aside today with the expectation of a greater return in the future. However, it’s crucial to understand fundamental concepts. Risk vs. Return: Generally, higher potential returns come with higher risk. Understanding your personal risk tolerance is paramount. Diversification: Don’t put all your eggs in one basket. Spreading your investments across different asset classes (stocks, bonds, real estate, etc.) and industries reduces overall risk. Time Horizon: The longer your investment horizon, the more time your investments have to recover from market downturns, allowing you to take on slightly more risk. Begin by educating yourself on these basics, perhaps through reputable financial books, courses, or trusted online resources.

Exploring Investment Vehicles

The world of investments offers a diverse array of vehicles, each with its own characteristics:

- Stocks: Represent ownership in a company. They offer potential for high growth but also higher volatility.

- Bonds: Essentially loans to governments or corporations. They are generally less volatile than stocks and provide fixed income.

- Mutual Funds: Professionally managed portfolios of stocks, bonds, or other investments. They offer diversification and convenience.

- Exchange-Traded Funds (ETFs): Similar to mutual funds but trade like stocks on an exchange. Often have lower fees.

- Real Estate: Can provide rental income and appreciation, but typically requires significant capital and management.

- Retirement Accounts (401(k)s, IRAs): Tax-advantaged accounts designed specifically for long-term retirement savings, often with employer matching contributions, which are essentially free money.

Start with diversified, low-cost index funds or ETFs within your retirement accounts. As your knowledge and capital grow, you can explore other options.

The Power of Compounding

Albert Einstein reportedly called compounding the eighth wonder of the world. It is the process where the returns on your investments also earn returns, leading to exponential growth. The earlier you start investing, the more time compounding has to work its magic. Even small, consistent contributions made early in life can accumulate into substantial wealth over decades. For example, a monthly investment of $200 earning an average 7% annual return could grow to over $220,000 in 30 years. This phenomenon underscores the importance of starting early and maintaining consistent contributions, even during market fluctuations.

Seeking Professional Guidance

While self-education is invaluable, there comes a point where professional guidance can be highly beneficial. A certified financial planner (CFP) can help you clarify your goals, assess your risk tolerance, create a personalized investment strategy, optimize your tax situation, and ensure your plan remains on track. They can also provide objective advice during volatile market periods. When choosing an advisor, look for a fee-only fiduciary, meaning they are legally obligated to act in your best interest and are compensated directly by you, not through commissions on products they sell.

5. Safeguarding Your Financial Future and Legacy

Handling money isn’t just about accumulation; it’s also about protection and planning for the long term. Safeguarding your assets and ensuring your wishes are honored are crucial steps in comprehensive financial management.

The Role of Insurance

Insurance acts as a safety net, protecting your financial well-being from significant, unexpected costs. It’s a fundamental component of risk management.

- Health Insurance: Essential for covering medical expenses, which can be astronomically high without coverage.

- Life Insurance: Provides financial support to your dependents in the event of your death, ensuring their ongoing financial security. Term life insurance is often recommended for most families.

- Disability Insurance: Replaces a portion of your income if you become unable to work due to illness or injury.

- Property Insurance: Protects your home, car, and other valuable assets from damage, theft, or liability claims.

Adequate insurance coverage prevents a single catastrophic event from derailing your entire financial plan, acting as a critical buffer for your savings and investments.

Planning for Retirement

Retirement planning is arguably the most significant long-term financial goal for most individuals. It involves strategically saving and investing throughout your working life to ensure you have sufficient income to maintain your desired lifestyle once you stop working. Maximize contributions to tax-advantaged accounts like 401(k)s (especially if there’s an employer match), Traditional IRAs, and Roth IRAs. Understand the different contribution limits, tax implications, and withdrawal rules for each. Consider diversifying your retirement portfolio and periodically rebalancing it as you approach retirement. The earlier you start, and the more consistently you contribute, the greater the impact of compounding on your retirement nest egg.

Estate Planning Essentials

Estate planning isn’t just for the wealthy; it’s for anyone who wants to ensure their assets are distributed according to their wishes and that their loved ones are protected. Key components include:

- Will: A legal document specifying how your assets should be distributed after your death.

- Trusts: Can offer more control over asset distribution, tax advantages, and avoid probate.

- Power of Attorney: Designates someone to make financial and/or medical decisions on your behalf if you become incapacitated.

- Beneficiary Designations: For retirement accounts and life insurance policies, ensure your beneficiaries are up-to-date, as these supersede your will.

While a sensitive topic, proactive estate planning provides immense peace of mind, preventing potential family disputes and ensuring your legacy aligns with your intentions.

Continual Financial Education

The financial world is constantly evolving. New investment products emerge, tax laws change, and economic landscapes shift. To effectively handle money over the long term, commit to continuous financial education. Read reputable financial news, listen to podcasts, attend webinars, or consult with your financial advisor. Staying informed allows you to adapt your strategies, identify new opportunities, and make proactive adjustments to your financial plan. This commitment to lifelong learning is perhaps the most powerful tool you possess in your journey toward enduring financial mastery.

In conclusion, handling money effectively is a multifaceted discipline that combines self-awareness, diligent planning, consistent execution, and continuous learning. It’s not a destination but an ongoing journey that evolves with your life stages and financial aspirations. By embracing the principles outlined here – understanding your landscape, mastering budgeting, building a solid foundation, growing wealth through investing, and safeguarding your future – you can transform your relationship with money from one of apprehension to one of confidence, purpose, and enduring prosperity. Your financial future is largely in your hands; equip yourself with the knowledge and tools to shape it wisely.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.