In an unpredictable world, the ability to save money stands as one of the most fundamental pillars of personal well-being and long-term financial freedom. For many, the concept of “saving” can feel daunting, a distant aspiration rather than an achievable reality. The good news is that starting to save doesn’t require a lottery win or a dramatic lifestyle overhaul; it simply requires a clear understanding of your current financial situation, a commitment to making small, consistent changes, and the right strategies to guide you. This guide will demystify the process, providing actionable insights to help you embark on your saving journey, no matter where you’re starting from.

The Imperative of Saving: Why It Matters More Than You Think

Before diving into the “how,” it’s crucial to understand the “why.” Saving isn’t just about accumulating a large sum of money; it’s about building resilience, creating opportunities, and achieving peace of mind. Without a clear understanding of its importance, it’s easy to lose motivation when faced with financial pressures.

Peace of Mind and Emergency Preparedness

Life is full of unexpected twists and turns. A sudden job loss, an unforeseen medical expense, or an urgent car repair can quickly derail your financial stability if you don’t have a safety net. An emergency fund, typically 3-6 months’ worth of living expenses, is your first line of defense. It provides a cushion that prevents minor setbacks from escalating into major crises, allowing you to navigate challenges without resorting to high-interest debt or compromising your future. Knowing you have this fund provides an invaluable sense of security and significantly reduces financial stress.

Achieving Short-Term and Long-Term Goals

Saving isn’t solely about guarding against the bad; it’s also about enabling the good. Whether your aspirations include a down payment on a house, funding a child’s education, taking that dream vacation, or starting your own business, savings are the fuel that powers these goals. Short-term goals might require a few months to a couple of years of saving, while long-term goals demand a more sustained and strategic approach. By breaking down large goals into smaller, manageable saving targets, you make the seemingly impossible achievable.

Building Wealth and Financial Independence

Beyond immediate needs and specific goals, saving is the bedrock of wealth creation and financial independence. Consistent saving, especially when coupled with smart investing, allows your money to grow over time through the power of compounding. This isn’t just about having “enough” for retirement; it’s about building a future where you have the freedom to make choices that aren’t dictated solely by financial constraints. It’s about creating a legacy and securing a stable future for yourself and your loved ones.

Laying the Foundation: Understanding Your Financial Landscape

You can’t chart a course without knowing your starting point. The initial step in any successful saving strategy involves a thorough assessment of your current financial situation. This isn’t always glamorous, but it’s absolutely essential.

The Power of Budgeting: Tracking Income and Expenses

A budget is not a straitjacket; it’s a roadmap. It helps you understand exactly where your money comes from and, more importantly, where it goes. Start by listing all your sources of income. Then, meticulously track every expense for at least a month. Categorize these expenses into fixed costs (rent/mortgage, loan payments, insurance) and variable costs (groceries, entertainment, dining out, utilities). Tools like spreadsheets, budgeting apps (Mint, YNAB, Personal Capital), or even a simple notebook can make this process easier. The goal is to gain clarity, not to judge yourself. Many people are surprised to discover how much they spend on discretionary items once they see it written down.

Identifying Saving Opportunities: Where Can You Cut Back?

Once you have a clear picture of your spending, you can begin to identify areas where you can reduce expenses without significantly impacting your quality of life. Look for “leakage” – small, regular expenses that add up over time (e.g., daily coffee runs, unused subscriptions, impulse purchases). Consider bigger categories: can you negotiate your internet bill? Cook at home more often? Carpool or use public transport? The key is to find sustainable cuts, not drastic deprivation that leads to burnout. Prioritize your spending based on your values and goals. If travel is important, perhaps cut back on dining out.

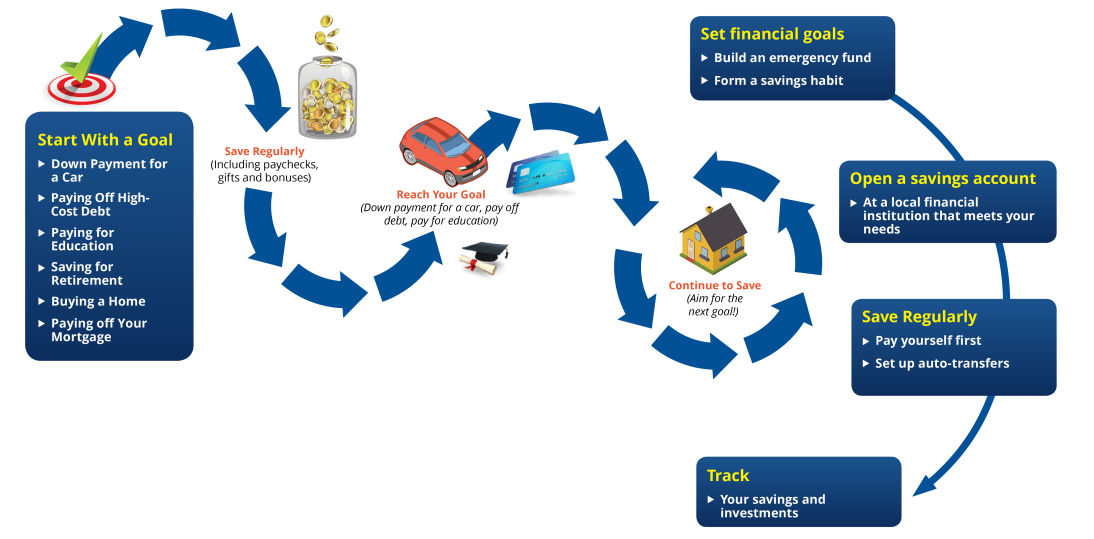

Setting SMART Saving Goals

Vague goals yield vague results. For your saving efforts to be effective, your goals should be SMART:

- Specific: Instead of “I want to save money,” say “I want to save $5,000 for a down payment.”

- Measurable: How much money do you need, and by when?

- Achievable: Is this goal realistic given your income and expenses?

- Relevant: Does this goal align with your broader financial aspirations?

- Time-bound: Set a realistic deadline. “By December 31st of next year.”

Setting SMART goals provides a clear target, a timeline, and a sense of purpose, making your saving journey much more directed and motivating.

Practical Strategies to Kickstart Your Savings Journey

Once you know why you’re saving and what your targets are, it’s time to implement concrete strategies to make saving a consistent habit.

The “Pay Yourself First” Principle

This is arguably the most powerful saving strategy. Instead of saving what’s left over after all your expenses and discretionary spending, you make saving your first “expense.” As soon as your paycheck hits your account, a predetermined amount is immediately transferred to your savings. This shifts your mindset from treating saving as an afterthought to recognizing it as a priority. This principle ensures that your savings grow consistently, irrespective of how much you spend on other things throughout the month.

Automating Your Savings

Building on the “Pay Yourself First” principle, automation makes saving effortless. Set up an automatic transfer from your checking account to your savings account(s) on a specific day, usually payday. You can schedule weekly, bi-weekly, or monthly transfers. The beauty of automation is that it removes the need for conscious decision-making, eliminating the temptation to spend the money instead. Once it’s out of sight, it’s out of mind and less likely to be spent. Most banks allow you to set up recurring transfers with ease.

Embracing the “Small Changes, Big Impact” Mindset

Don’t underestimate the power of small, consistent actions. Finding $5 here, $10 there, and dedicating it to savings can add up significantly over time.

- Round-up apps: Many banking apps offer features that round up your purchases to the nearest dollar and transfer the difference to savings.

- Challenge yourself: Try a no-spend week, or cut out one non-essential expense for a month.

- Found money: If you get a bonus, a tax refund, or a gift, consider saving a portion of it instead of spending it all.

- DIY wherever possible: Making your own coffee, packing lunch, or doing small home repairs can save a surprising amount.

These small shifts, when applied consistently, can create a substantial impact on your savings over time.

Debt Management: A Prerequisite for Effective Saving

While it might seem counterintuitive to focus on debt when discussing saving, high-interest debt (like credit card debt) can severely hinder your ability to save. The interest payments effectively eat away at any money you might be trying to put aside. Prioritizing the repayment of high-interest debt can free up significant cash flow, which can then be redirected to your savings goals. Consider strategies like the debt snowball or debt avalanche methods, or explore consolidation options if appropriate. Once that burden is lifted, your saving power will dramatically increase.

Optimizing Your Savings: Where to Keep Your Money

Once you’ve started accumulating savings, it’s important to ensure your money is working for you, not just sitting idly. Different types of accounts serve different purposes.

High-Yield Savings Accounts (HYSAs)

For your emergency fund and short-term goals, HYSAs are an excellent choice. Offered by online banks, these accounts typically offer significantly higher interest rates than traditional brick-and-mortar bank savings accounts. While the rates might fluctuate, they ensure your money grows faster, counteracting some effects of inflation, all while remaining liquid and easily accessible when you need it. Look for accounts with no monthly fees and FDIC insurance.

Certificates of Deposit (CDs)

CDs are suitable for money you won’t need for a specific period (e.g., 6 months, 1 year, 5 years). In exchange for locking up your money for a set term, banks typically offer higher interest rates than standard savings accounts. They are FDIC-insured, making them a very low-risk option. However, withdrawing money before the term ends usually incurs a penalty, so ensure the funds aren’t needed for emergencies. CDs can be great for specific goals with a known timeline.

Exploring Investment Vehicles for Long-Term Growth

While the initial focus of “starting to save” is building liquid cash reserves, for long-term goals like retirement or significant wealth building, you’ll want your money to grow more aggressively than it would in a savings account. This involves investing. Options include:

- Robo-advisors: Platforms like Betterment or Wealthfront automate investing based on your risk tolerance and goals.

- Index funds/ETFs: These passively managed funds offer broad market exposure and diversification at a low cost.

- Mutual funds: Professionally managed funds that invest in a diversified portfolio of stocks, bonds, or other securities.

- Individual stocks/bonds: For those willing to research and manage their own portfolio.

It’s crucial to understand that investing carries risk, and the value of your investments can go down as well as up. However, over long periods, the stock market has historically provided returns that outpace inflation and traditional savings accounts. Start small, educate yourself, and consider consulting a financial advisor.

Retirement Accounts: The Power of Tax Advantages

Don’t overlook dedicated retirement accounts as powerful saving tools, especially if your employer offers a matching contribution (e.g., 401k match).

- 401(k) / 403(b): Employer-sponsored plans that allow pre-tax contributions to grow tax-deferred. Employer matching contributions are essentially free money.

- IRA (Traditional or Roth): Individual Retirement Arrangements offer tax benefits for retirement saving. Traditional IRAs offer tax-deductible contributions (pre-tax), while Roth IRAs offer tax-free withdrawals in retirement (after-tax contributions).

These accounts not only help you save for the future but also provide significant tax advantages, accelerating your wealth accumulation. Even a small contribution, especially early in your career, can grow exponentially over decades due to compounding.

Maintaining Momentum and Overcoming Challenges

Starting to save is a significant achievement, but the journey is ongoing. Staying motivated and adapting to life’s inevitable changes are key to long-term success.

Regular Review and Adjustment of Your Budget

Your financial life isn’t static, and neither should your budget be. Review your budget monthly or quarterly. Have your income or expenses changed? Have you achieved a saving goal and need to set a new one? Regularly adjusting your budget ensures it remains a relevant and effective tool, helping you stay on track with your saving objectives. This flexibility prevents the budget from feeling restrictive and keeps it aligned with your current reality.

Celebrating Milestones and Staying Motivated

Saving can be a long game, and it’s easy to lose steam. Break down your larger goals into smaller milestones and celebrate each achievement. Reaching your first $1,000, paying off a credit card, or hitting your emergency fund target are all reasons to acknowledge your progress. These celebrations don’t have to be expensive; a simple treat or a moment of reflection can reaffirm your commitment and provide the motivation to continue.

Dealing with Setbacks and Unexpected Expenses

Life happens. You might have to dip into your emergency fund, face an unexpected bill, or experience a temporary income reduction. Don’t view these as failures. That’s precisely what your emergency fund is for! Acknowledge the setback, address the issue, and then calmly re-evaluate your budget and saving plan. The key is to get back on track as quickly as possible, not to give up entirely. Financial resilience is built not by avoiding problems, but by effectively navigating them.

Continuous Learning and Financial Literacy

The world of personal finance is vast and ever-evolving. Make it a habit to continuously educate yourself. Read books, listen to podcasts, follow reputable financial blogs, and stay informed about economic trends. Understanding concepts like inflation, different investment types, and tax implications will empower you to make smarter financial decisions and optimize your saving and investing strategies over time. The more you know, the more confident and successful you’ll be in managing your money.

Conclusion

Starting to save money is a journey that begins with a single step, but it’s one of the most impactful steps you can take towards securing your future. It’s about more than just accumulating cash; it’s about gaining control, building resilience, and creating the freedom to live the life you envision. By understanding your current financial situation, setting clear SMART goals, implementing practical strategies like “pay yourself first” and automation, and continuously learning and adapting, you can transform your financial trajectory. Remember, consistency triumphs over intensity. Start small, stay persistent, and watch as your efforts compound into a foundation of financial security and independence. Your future self will thank you for starting today.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.