In the intricate landscape of personal finance, one of the most critical aspects is understanding your tax obligations. The thought of owing the Internal Revenue Service (IRS) can be daunting, often accompanied by uncertainty and anxiety. However, ignorance is far from bliss when it comes to tax debt; unaddressed balances can lead to accumulating penalties, interest, and more severe enforcement actions. Proactive management and clear knowledge of your tax status are not just good practice—they are essential components of sound financial health.

This guide provides an exhaustive walkthrough of the various methods available to ascertain whether you owe the IRS, delving into the financial implications, the tools at your disposal, and the steps to take once you have a clear picture of your obligations. By equipping yourself with this knowledge, you can navigate your tax responsibilities with confidence, ensuring compliance and safeguarding your financial future.

The Critical Importance of Proactive Tax Management

Understanding your tax liability isn’t merely about fulfilling a civic duty; it’s a fundamental pillar of responsible personal finance. The ability to promptly and accurately determine if you have an outstanding balance with the IRS is crucial for several reasons, all of which directly impact your financial well-being and peace of mind.

Avoiding Penalties and Interest

One of the most immediate and tangible benefits of proactive tax management is the avoidance of unnecessary financial burdens. The IRS imposes a range of penalties for non-compliance, including failure to file, failure to pay, and accuracy-related penalties. These penalties can quickly inflate your initial tax liability, often accruing interest daily from the due date of the tax. For instance, the failure-to-pay penalty is 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, maxing out at 25% of your unpaid taxes. Interest rates, adjusted quarterly, can add further significant costs. By checking your status regularly and addressing any outstanding balances promptly, you can mitigate or even entirely avoid these additional charges, preserving your hard-earned money.

Maintaining Financial Health and Peace of Mind

Financial stability is intrinsically linked to predictability and control. When you are unaware of a potential tax debt, it creates an underlying current of uncertainty that can undermine your overall financial planning. Unanticipated tax bills can derail budgets, delay investment plans, or force you to dip into savings reserved for other purposes. Knowing your exact tax standing empowers you to budget effectively, allocate funds appropriately, and make informed financial decisions without the specter of a hidden IRS debt looming. This clarity brings a profound sense of peace, allowing you to focus on your financial goals rather than worrying about potential arrears.

Understanding Your Obligations

Beyond the immediate financial costs, proactive checks foster a deeper understanding of your tax obligations. This involves comprehending how your income, deductions, and credits translate into a final tax liability. Regular engagement with your tax records and the IRS system demystifies the tax process, transforming it from an intimidating annual chore into a manageable component of your financial life. This understanding is invaluable, enabling you to identify potential issues before they escalate, plan for future tax years more effectively, and even uncover opportunities for tax savings. It cultivates financial literacy that extends far beyond just paying your dues.

Direct Pathways to Ascertaining Your IRS Debt

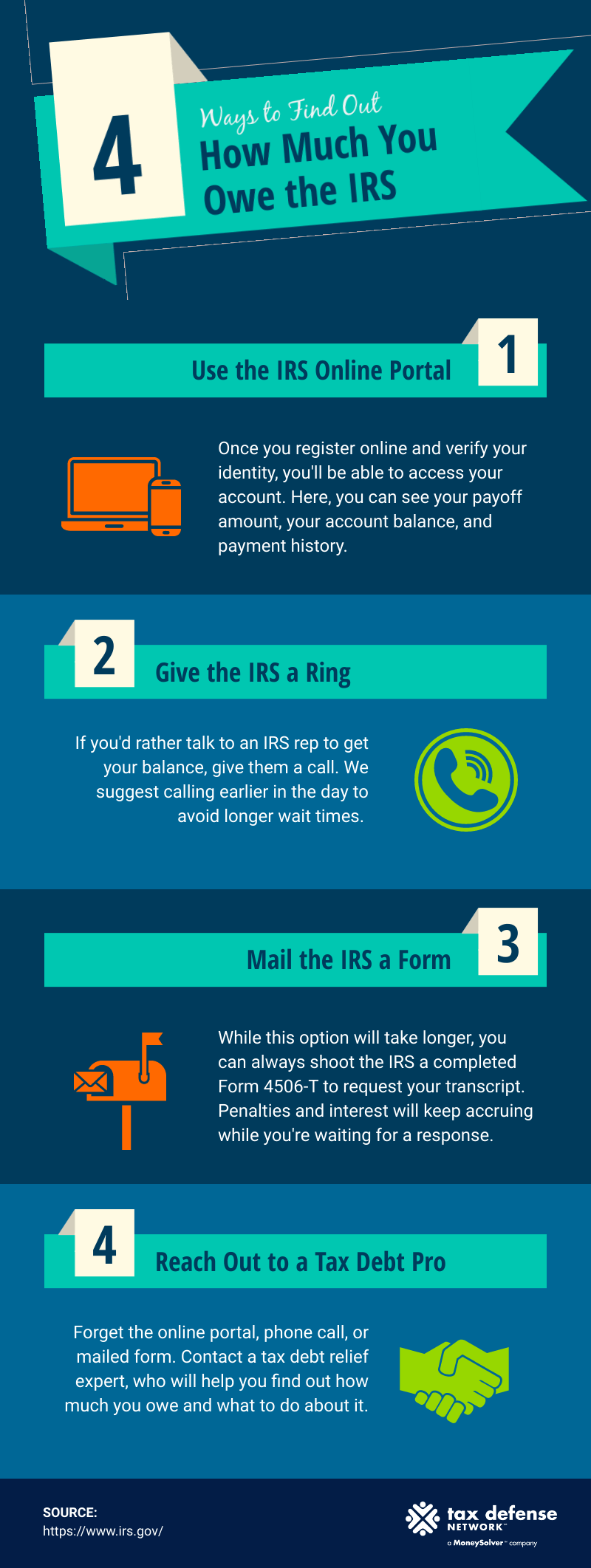

The IRS has significantly enhanced its digital infrastructure and direct communication channels, making it more accessible for taxpayers to inquire about their account status. Leveraging these tools is the most efficient way to determine if you owe the IRS.

Leveraging Your IRS Online Account

The IRS Online Account is arguably the most powerful and convenient tool at your disposal. This secure portal provides a personalized gateway to your tax information, offering a comprehensive overview of your federal tax account.

- Detailed Look at What’s Available: Through your online account, you can typically view:

- Your current balance due, including any interest and penalties.

- Your payment history for the past 18 months.

- Key information from your most recent tax return.

- Payment plan details, if you have one.

- Digital copies of certain IRS notices you’ve received.

- Your tax records via “Get Transcript.”

- Step-by-Step Access: To access your IRS Online Account, visit IRS.gov and search for “IRS Online Account.” You will need to create an account or log in using an existing ID.me account, which involves a robust identity verification process for security purposes. This usually requires providing personal information, a photo ID, and sometimes a live video chat. Once verified, you gain immediate access to your tax data.

Requesting a Tax Transcript

A tax transcript is a summary of your tax return information, wage and income data, or account activity. While not an actual copy of your tax return, it provides crucial details that can help you understand your tax obligations.

- Types of Transcripts:

- Account Transcript: Shows most line items from your original tax return, along with any adjustments made by you or the IRS, and financial transactions such as payments, penalties, and interest. This is the primary transcript for checking current balances.

- Record of Account Transcript: Combines the information from the tax return transcript and the account transcript, providing a complete picture of your tax return and subsequent account activity.

- Wage and Income Transcript: Displays data from information returns, such as Forms W-2, 1099, 1098, and Form 5498.

- How to Request: You can request transcripts online via the IRS “Get Transcript” service (which is part of your IRS Online Account or accessible directly), by mail using Form 4506-T, Request for Transcript of Tax Return, or by phone. Online requests offer immediate access for most years.

- What Information It Provides: An Account Transcript, for example, will clearly show any balance due, including penalties and interest, for a specific tax period.

Direct Communication with the IRS

Sometimes, the most direct approach is necessary, especially if online tools don’t provide the clarity you need or if your situation is complex.

- Phone Inquiries: You can call the IRS directly at 1-800-829-1040 (for individuals). Be prepared for potentially long wait times, especially during peak tax season. Have your Social Security number, date of birth, and any recent tax returns or notices handy for verification. An IRS representative can usually tell you if you have an outstanding balance and discuss payment options.

- Written Correspondence: For complex issues or if you prefer a paper trail, you can write to the IRS. However, this is the slowest method, with response times that can span several weeks or even months. Ensure your letter is clear, concise, and includes your identifying information.

- In-Person Assistance: Taxpayer Assistance Centers (TACs) offer face-to-face help. You typically need to schedule an appointment online before visiting. While TACs can help with account inquiries, their services might be limited compared to what’s available online or over the phone.

Reviewing Your Own Financial Records

Before even contacting the IRS, your personal records are an invaluable first stop.

- Past Tax Returns (Form 1040, Schedules): Your filed tax returns will show the tax liability you reported. If you remember sending a payment but didn’t keep clear records, this can be your starting point.

- Payment Records: Check your bank statements, cancelled checks, credit card statements, or electronic payment confirmations. If you sent a payment and it cleared, it might be an accounting error if the IRS claims you still owe.

- Notices from the IRS: The IRS communicates through various notices and letters. If you owe, you would have likely received CP14 (Balance Due), CP501, CP503, or CP504 (notices of intent to levy). Always review these letters carefully, as they provide critical information about your debt and deadlines.

Deciphering Your Tax Liability and Due Amounts

Discovering you owe the IRS can be a moment of apprehension, but understanding why and what specifically you owe is crucial for taking appropriate action. Tax liability isn’t a monolithic concept; it comprises several components that contribute to your final balance.

Distinguishing Between Tax Liability and Payment Due

It’s vital to differentiate between your total tax liability for a given year and the amount currently due. Your “tax liability” is the total amount of tax you legally owe based on your income, deductions, and credits. The “payment due” is what remains after subtracting any payments you’ve already made through withholding, estimated taxes, or previous direct payments. For example, your tax liability might be $10,000, but if you had $9,000 withheld from your paychecks, your payment due is $1,000 (plus any penalties/interest). This distinction helps in understanding the true scope of your obligation.

Understanding Penalties and Interest Accrual

As mentioned, the IRS levies penalties for various infractions, primarily for not filing on time and not paying on time.

- Failure-to-File Penalty: If you don’t file your return by the due date (including extensions), the penalty is 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid tax.

- Failure-to-Pay Penalty: If you don’t pay your taxes by the due date, the penalty is 0.5% of the unpaid taxes for each month or part of a month the taxes remain unpaid, also capped at 25%. This penalty is often reduced to 0.25% if an installment agreement is in place.

- Interest: Interest is charged on underpayments, and it applies to both unpaid taxes and penalties. The interest rate is the federal short-term rate plus 3 percentage points, adjusted quarterly. Interest compounds daily, meaning it is calculated on the principal balance plus any accumulated interest. It’s crucial to address tax debt promptly because interest can significantly inflate the total amount owed over time.

The Role of Estimated Taxes and Withholding

Many taxpayers find they owe the IRS because their withholding or estimated tax payments were insufficient throughout the year.

- Withholding: If you’re an employee, your employer withholds income tax from your paychecks. If you don’t adjust your Form W-4 to reflect your current financial situation (e.g., marriage, new job, secondary income, significant deductions), you might not have enough tax withheld, leading to an underpayment at tax time.

- Estimated Taxes: Individuals who are self-employed, receive income from investments, or have other income not subject to withholding are generally required to pay estimated taxes quarterly. Failure to pay enough estimated tax throughout the year can result in penalties, even if you pay your entire balance by the tax deadline.

Addressing Outcomes from Audits or Examinations

Sometimes, a tax debt arises not from an initial filing but from an IRS audit or examination. If an audit uncovers discrepancies or disallows certain deductions, credits, or income exclusions, it can result in an additional tax assessment. The IRS will send you a notice (e.g., Letter 525, Letter 3219N) detailing the proposed changes and your appeal rights. If you agree with the findings or if the appeals process confirms the assessment, you will owe the additional tax plus any applicable penalties and interest. These amounts will be reflected in your IRS Online Account and on subsequent notices.

Strategic Responses When You Discover You Owe

Finding out you owe the IRS can be stressful, but understanding your options for repayment is key to managing the debt effectively. The IRS offers several payment solutions designed to accommodate various financial situations, ranging from immediate payment to structured long-term plans.

Exploring Immediate Payment Options

If you have the financial capacity, paying your tax debt in full and on time is always the best strategy to avoid accruing additional penalties and interest. The IRS provides multiple convenient ways to make payments:

- IRS Direct Pay: This free service allows you to pay directly from your checking or savings account. It’s secure and easy to use on IRS.gov.

- Debit Card, Credit Card, or Digital Wallet: You can pay through third-party payment processors using a credit card, debit card, or digital wallet (e.g., PayPal). Be aware that these processors typically charge a convenience fee, which varies by provider.

- Electronic Federal Tax Payment System (EFTPS): This is a free service provided by the U.S. Department of the Treasury. It’s ideal for businesses and individuals who need to make federal tax payments electronically. You must enroll in advance.

- Payment via Check or Money Order: You can mail a check or money order payable to the “U.S. Treasury” along with a Form 1040-V, Payment Voucher. Always ensure you mail it to the correct IRS address for your state and include your Social Security number and the tax year.

Establishing Payment Plans and Agreements

If you cannot afford to pay your tax debt in full immediately, the IRS offers several relief options:

- Short-Term Payment Plans: You might be granted up to 180 additional days to pay your tax liability in full, though interest and penalties still apply. You can often request this online.

- Installment Agreements (Online Payment Agreement): If you owe a combined total of under $50,000 (for individuals) or $25,000 (for businesses) in tax, penalties, and interest, you might qualify for a monthly installment agreement. This allows you to make manageable monthly payments for up to 72 months. You can apply for this online via the IRS website, and if you meet the criteria, your agreement is often approved instantly.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. An OIC is typically granted when there’s serious doubt about the taxpayer’s ability to pay the full amount or when exceptional circumstances make it unfair to collect the full amount. The IRS considers your ability to pay, income, expenses, and asset equity. The OIC process is complex and requires careful preparation using Form 656, Offer in Compromise.

Seeking Professional Guidance

Navigating tax debt can be complex, and sometimes professional assistance is warranted.

- Tax Preparers and Enrolled Agents: Qualified tax professionals, such as Certified Public Accountants (CPAs) or Enrolled Agents (EAs), can represent you before the IRS, help you understand your options, and assist with negotiating payment plans or OICs. They can also ensure all necessary forms are correctly filed.

- Tax Attorneys: For highly complex cases, audits, or disputes where legal expertise is required, a tax attorney can provide invaluable assistance. They specialize in tax law and can represent you in appeals or tax court.

- Low-Income Taxpayer Clinics (LITCs): LITCs are independent organizations that provide free or low-cost assistance to low-income individuals who have tax disputes with the IRS or who need help understanding their taxpayer rights and responsibilities.

Proactive Strategies for Future Tax Compliance

The best defense against tax debt is a strong offense—implementing proactive financial strategies that minimize the likelihood of future underpayments and enhance your overall tax management. By taking a few deliberate steps, you can avoid the stress and financial burden of owing the IRS.

Optimizing Your Tax Withholding

For employees, your W-4 form is your primary tool for managing federal income tax withholding.

- Regular Review: Review and update your W-4 annually, or whenever there’s a significant life event (marriage, divorce, birth of a child, new job, second job, substantial change in income or deductions).

- IRS Tax Withholding Estimator: Use the IRS Tax Withholding Estimator tool on IRS.gov. This free online resource helps you determine if you’re withholding the correct amount of tax, helping you avoid an unexpected tax bill at the end of the year or a significant refund (which means you overpaid throughout the year). Adjusting your W-4 can ensure your withholding closely matches your actual tax liability.

Diligent Record-Keeping and Documentation

Maintaining organized and accurate financial records is foundational to effective tax management.

- Centralized System: Keep all income statements (W-2s, 1099s), expense receipts, bank statements, investment account statements, and past tax returns in a centralized, secure location, whether physical or digital.

- Digital Tools: Utilize accounting software, budgeting apps, or simple spreadsheets to track income and expenses throughout the year. This makes tax preparation much smoother and provides an ongoing snapshot of your financial health.

- Proof of Payments: Always retain proof of any tax payments made, including confirmation numbers for electronic payments or cleared checks.

Regular Financial Review and Planning

Your tax situation isn’t static; it evolves with your life. Regular financial reviews ensure your tax strategy aligns with your current circumstances.

- Quarterly Check-ins: If you have varied income or significant deductions, consider performing a “mini-tax review” quarterly. Project your income and expenses, and assess your estimated tax liability to adjust withholding or estimated payments as needed.

- Budgeting for Taxes: Incorporate potential tax payments into your overall financial budget. Set aside funds regularly if you anticipate owing money, especially if you’re self-employed and paying estimated taxes.

- Consult a Professional: Consider an annual check-in with a tax professional, even if you file your own taxes. They can provide personalized advice, identify potential tax-saving strategies, and help anticipate any future liabilities.

Staying Informed on Tax Law Changes

Tax laws are subject to change, often annually. Keeping abreast of these changes is crucial for accurate compliance and effective financial planning.

- IRS Publications and News: Follow official IRS news releases, publications, and taxpayer alerts.

- Reputable Financial News: Subscribe to reputable financial news sources or blogs that cover tax law updates.

- Professional Advice: Your tax professional will typically keep you informed of relevant changes that impact your situation.

By adopting these proactive strategies, you not only minimize the chances of incurring unexpected tax debt but also empower yourself with a greater sense of control and clarity over your personal finances. Understanding how to check if you owe the IRS is merely the first step; the true mastery lies in preventing such debts from arising in the first place through informed and diligent financial management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.