The thought of owing money to the Internal Revenue Service (IRS) can be a source of significant anxiety for many individuals and businesses. The tax system, with its myriad rules, deadlines, and forms, often feels like a labyrinth, making it difficult to ascertain one’s true financial standing with the government. However, understanding your tax obligations and proactively monitoring your status is not only possible but crucial for maintaining financial peace of mind. This article will guide you through the process of determining whether you owe the IRS money, how to interpret official communications, and what steps to take if you find yourself with a tax bill.

Understanding the Foundations of Tax Liability

Before diving into how to check if you owe, it’s essential to grasp the fundamental reasons why a tax liability might arise in the first place. Taxes are a complex interplay of income earned, deductions claimed, credits applied, and the amount already paid through withholding or estimated taxes. A discrepancy in any of these areas can lead to an unexpected tax bill.

Common Scenarios Leading to a Tax Bill

Several common situations can result in you owing money to the IRS, even if you’ve filed your taxes diligently:

- Insufficient Withholding (W-4 Issues): For most employees, income tax is withheld from each paycheck based on the information provided on Form W-4 (Employee’s Withholding Certificate). If you haven’t adjusted your W-4 correctly, perhaps due to multiple jobs, marriage, or other income sources, too little tax might be withheld. This common oversight can lead to a significant tax bill come filing season.

- Untaxed Income Sources: Many forms of income are taxable but may not be subject to automatic withholding. This includes income from the gig economy (freelancing, consulting, ride-sharing), capital gains from investments, interest and dividends from savings and investments, rental income, and certain types of retirement distributions. If you earn substantial income from these sources and don’t make estimated tax payments, you will likely owe at tax time.

- Estimated Tax Underpayment: Individuals who are self-employed, independent contractors, or have significant income not subject to withholding (like those mentioned above) are generally required to pay estimated taxes quarterly. If these payments are not made on time, or if the amounts paid are insufficient, you could face both a tax bill and potential penalties for underpayment.

- Changes in Life Circumstances: Major life events can significantly impact your tax situation. Getting married or divorced, having a child, buying or selling a home, or experiencing a substantial increase or decrease in income can all alter your tax liability. Failing to adjust your tax planning in response to these changes can lead to owing money or receiving a smaller refund than anticipated.

- Errors in Filing: While less common with modern tax software, mathematical errors, incorrect deductions or credits claimed, or misreporting income on your tax return can lead to a revised assessment from the IRS, often resulting in a bill. It’s crucial to ensure the accuracy of all information submitted.

Understanding these common pitfalls is the first step in demystifying why you might owe the IRS. It highlights the importance of ongoing vigilance and proper planning throughout the year, rather than just during tax season.

Proactive Monitoring: Staying Ahead of Your Tax Status

The best way to avoid the surprise of an unexpected tax bill is to proactively monitor your tax situation throughout the year. This involves regularly reviewing your income, expenses, and withholding, and making adjustments as needed.

Regular Review of Your Withholding (W-4)

For employees, your W-4 form is your primary tool for managing your tax liability. It dictates how much federal income tax your employer withholds from your paycheck.

- How to Adjust Your W-4: It’s advisable to review your W-4 annually, or whenever you experience a significant life event (marriage, divorce, new job, new dependent, substantial change in income). You can typically update your W-4 through your employer’s HR or payroll department.

- IRS Tax Withholding Estimator: The IRS provides an excellent online tool, the Tax Withholding Estimator, which helps you perform a “paycheck checkup.” By inputting information about your income, deductions, and credits, it calculates the appropriate amount of tax to withhold and recommends how to adjust your W-4. Using this tool ensures you’re not withholding too little (leading to a tax bill) or too much (giving the government an interest-free loan).

Tracking Income and Deductions Throughout the Year

Maintaining meticulous records of your income and expenses is paramount, especially for self-employed individuals, investors, or anyone with diverse income streams.

- Record-Keeping Importance: Keep organized records of all income received (W-2s, 1099s, bank statements), expenses that might be deductible (business expenses, medical expenses, charitable contributions), and any estimated tax payments made. This organized approach simplifies tax preparation and provides a clear picture of your financial status.

- Using Financial Software: Personal finance software like QuickBooks Self-Employed, TurboTax, H&R Block, or even simple spreadsheets can help you track income and expenses in real-time, making tax calculations much easier and reducing the likelihood of errors.

Understanding Estimated Tax Payments

If you expect to owe at least $1,000 in tax for the year (or $500 for corporations), you might be required to make estimated tax payments. This requirement primarily applies to those who are self-employed, partners, or have significant income from interest, dividends, rent, or alimony.

- Who Needs to Pay Estimated Taxes: If you don’t have an employer withholding taxes or if your withholding isn’t sufficient to cover your tax liability, you’ll need to pay estimated taxes. This prevents a large tax bill and potential penalties for underpayment at the end of the year.

- Payment Deadlines: Estimated taxes are typically paid in four installments: April 15, June 15, September 15, and January 15 of the following year. Missing these deadlines or underpaying can result in penalties.

By taking these proactive steps, you can significantly reduce the chances of being surprised by a tax bill and gain greater control over your financial obligations.

Deciphering Official Communications and Confirming Your Debt

Despite your best efforts, sometimes you might still find yourself in a situation where you suspect or discover you owe the IRS. Knowing how to verify this information and respond appropriately is crucial.

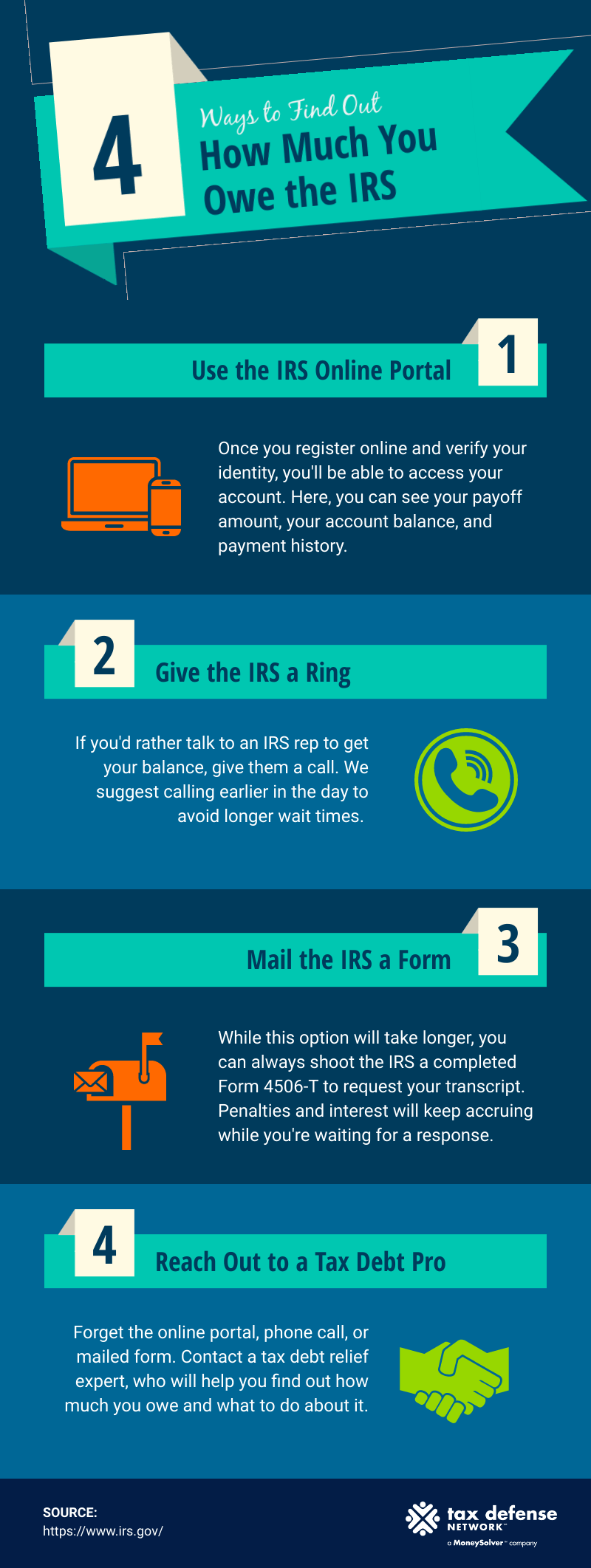

The Power of Your IRS Online Account

The IRS provides a valuable online tool that allows taxpayers to access their personal tax information directly. This is often the most reliable way to confirm if you owe money.

- Viewing Tax Records, Payment History, Tax Transcripts: By creating an account at IRS.gov, you can view your tax account balance, make payments, see your payment history, and access tax transcripts (which summarize your tax return information). This is particularly useful if you’ve lost track of past filings or payments.

- Checking for Notices and Outstanding Balances: Your online account will typically show if you have any outstanding balances due or if the IRS has issued any notices to you. This is a critical first stop when you suspect you might owe.

Understanding IRS Notices and Letters

The IRS communicates through official letters and notices, not typically via email, text, or social media. It’s vital to recognize legitimate communications and understand their implications.

- CPAs, LTRs, Different Types of Notices: The IRS sends various types of notices, often identified by a “CP” or “LTR” number in the top right corner. These notices can range from routine confirmations of changes to your account to demands for payment or audit notifications. For example, a CP14 notice indicates you have a balance due. A CP2000 notice suggests there’s a discrepancy between income reported to the IRS by third parties (like employers or banks) and what you reported on your tax return.

- How to Respond and Verify Authenticity: Always read IRS notices carefully. They will explain the issue, the amount owed (if any), and the required actions and deadlines. If you’re unsure about the authenticity of a notice, you can call the IRS directly using the phone number on their official website (IRS.gov), not a number from the letter itself, to avoid scams. Never share personal information in response to unsolicited emails or calls claiming to be from the IRS.

Professional Verification: When to Consult a Tax Expert

Sometimes, the complexity of your situation or the nature of an IRS notice warrants professional help.

- CPAs, Enrolled Agents, Tax Attorneys: Certified Public Accountants (CPAs), Enrolled Agents (EAs), and Tax Attorneys are qualified tax professionals who can help you understand your tax situation, interpret IRS notices, and represent you before the IRS.

- When an Expert is Essential: If you receive an audit notice, a notice of intent to levy or seize assets, or if you believe the IRS assessment is incorrect and complex, consulting a tax professional is highly recommended. They can help navigate the complexities, ensure you understand your rights, and potentially resolve the issue in your favor.

What to Do When You Confirm You Owe and Avoiding Future Surprises

Discovering you owe the IRS can be daunting, but it’s a manageable situation with clear steps you can take. Ignoring the debt will only lead to further penalties and interest.

Options for Paying Your Tax Bill

The IRS offers several payment options designed to accommodate different financial situations.

- Full Payment: If you can afford it, paying your tax bill in full by the due date is the best option to avoid additional penalties and interest. You can pay online, by phone, or by mail.

- Short-Term Payment Plans: If you need a little more time, you may be granted up to 180 days to pay your tax liability in full, though interest and penalties still apply.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than they originally owed. This option is typically available when a taxpayer is experiencing significant financial hardship and cannot pay the full amount. The IRS will evaluate your ability to pay, income, expenses, and asset equity.

- Installment Agreements: If you can’t pay your full tax bill immediately, you may be able to set up an installment agreement with the IRS, allowing you to make monthly payments for up to 72 months. While interest and penalties still apply, this option can prevent enforced collection actions.

Challenging an Incorrect Tax Assessment

If you believe the IRS has made an error in assessing your tax liability, you have the right to challenge it.

- Appealing a Notice: The IRS notice will usually outline your appeal rights and the process for disputing the assessment. You may need to provide additional documentation or clarification.

- Amended Returns: If you discover an error on your original tax return that resulted in an underpayment, you can file an amended return (Form 1040-X) to correct the mistake.

Strategies to Prevent Future Tax Debt

The best defense against owing the IRS is a robust proactive strategy.

- Annual W-4 Review: Make it a habit to review and adjust your W-4 form at least once a year, or whenever major life changes occur.

- Meticulous Record-Keeping: Maintain organized and complete records of all income and expenses throughout the year. This simplifies tax preparation and provides a clear audit trail.

- Budgeting for Taxes: If you have income not subject to withholding, create a budget that allocates funds specifically for estimated tax payments. Treat these payments like any other essential bill.

- Professional Advice: Consider consulting a tax professional regularly, especially if your financial situation is complex or changes frequently. Their expertise can save you money and stress in the long run.

Knowing if you owe the IRS money doesn’t have to be a mystery. By understanding the reasons for tax liability, proactively monitoring your finances, recognizing legitimate IRS communications, and knowing your options for payment or dispute, you can confidently navigate your tax obligations and maintain control over your financial future. The key is engagement, preparation, and timely action.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.