The question “how do I know if I owe the IRS?” is one that surfaces frequently, often accompanied by a mix of anxiety and uncertainty. For many taxpayers, the intricacies of the U.S. tax system can feel like a labyrinth, making it difficult to ascertain their true financial standing with the federal government. Understanding your tax obligations and knowing how to verify your status with the Internal Revenue Service (IRS) is not just about avoiding penalties; it’s about financial peace of mind and responsible personal finance management. This guide will walk you through the common reasons you might owe, the official methods to check your IRS account, and crucial steps to take if you discover an outstanding balance.

Understanding Your Tax Obligations: A Foundational Overview

The United States operates on a “pay-as-you-go” tax system. This means that income tax is generally paid throughout the year as income is earned, either through employer withholding or through estimated tax payments for self-employed individuals and those with other sources of income not subject to withholding. The annual tax return, filed by the tax deadline, is essentially a reconciliation process where you report your total income, deductions, and credits, and compare the tax you’ve already paid against your actual tax liability.

The U.S. “Pay-As-You-Go” Tax System

At its core, the pay-as-you-go system is designed to prevent a large, unmanageable tax bill at the end of the year. Employers withhold a portion of each paycheck based on the Form W-4 submitted by the employee. Similarly, individuals who are self-employed, own a business, or have significant income from investments, rents, or other sources typically make quarterly estimated tax payments using Form 1040-ES. When the amount withheld or paid through estimates falls short of the actual tax due, an underpayment occurs, leading to a balance owed to the IRS. Conversely, if too much was paid, you’ll receive a refund. The challenge lies in accurately estimating one’s income and deductions throughout the year to align payments with the final tax liability.

Common Reasons for Underpayment

Several factors can lead to an underpayment, even for diligent taxpayers. A primary reason is insufficient withholding. If your W-4 form isn’t updated to reflect life changes like marriage, divorce, a new child, or a second job, your employer might withhold too little. For the self-employed, an unexpected increase in income that wasn’t accounted for in estimated payments is a frequent culprit. Significant capital gains from investments, untaxed retirement distributions, or even unexpected bonuses can also push you into an underpayment situation if not properly anticipated and managed. Other reasons include miscalculating deductions or credits, or simply making an error when preparing your tax return. The complexity of tax law means that even minor oversight can lead to a discrepancy.

The Importance of Accurate Record-Keeping

Diligent record-keeping is the bedrock of effective tax management. Maintaining organized records of all income, expenses, deductions, and credits throughout the year is invaluable. This includes pay stubs, W-2s, 1099s, receipts for deductible expenses, bank statements, and any correspondence from the IRS. Good records not only simplify tax preparation but also provide the necessary documentation to justify your claims if the IRS ever audits your return. More importantly, they allow you to project your income and adjust your withholding or estimated payments proactively, significantly reducing the likelihood of an unexpected tax bill.

Key Indicators You Might Owe the IRS

While proactive planning helps, sometimes the signs that you might owe the IRS become evident only after the fact. Recognizing these indicators can prompt you to investigate your situation before it escalates.

Insufficient Withholding or Estimated Tax Payments

This is arguably the most common reason for owing the IRS. If you’ve started a new job and didn’t fill out your W-4 correctly, or if you picked up a side gig and didn’t account for the self-employment taxes, your payments throughout the year might not have kept pace with your earnings. A good rule of thumb is to review your withholding annually, especially if your income or deductions change. For estimated tax payers, failing to adjust quarterly payments after a substantial increase in income can quickly lead to an underpayment.

Changes in Income or Life Circumstances

Life events often have tax implications. Getting married or divorced, having a child, buying or selling a home, starting a new business, or receiving a significant inheritance can all alter your tax liability. Forgetting to update your W-4 or adjust your estimated payments after these changes is a common oversight that results in owing money. For instance, if you get married and both you and your spouse work, your combined income might push you into a higher tax bracket, requiring more withholding than you initially accounted for as single filers.

Miscalculated Deductions or Credits

Tax deductions and credits are fantastic ways to reduce your taxable income or your actual tax bill, respectively. However, miscalculating them, claiming ones you’re not eligible for, or not having adequate documentation to support them can lead to problems. If the IRS reviews your return and disallows a significant deduction or credit, your tax liability will increase, potentially resulting in an unexpected bill. It’s crucial to understand the eligibility requirements for any deduction or credit you claim.

Errors on Your Filed Tax Return

Simple human error can also lead to an underpayment. A forgotten income source, a misplaced decimal point, or a transposition error during data entry can all throw off your calculations. While tax software helps minimize these mechanical errors, it’s still possible for incorrect data entry or oversight to occur. The IRS has sophisticated systems to cross-reference reported income with what employers and financial institutions report, making it likely that such errors will be flagged.

Receiving an IRS Notice or Letter

This is often the most definitive indicator that you might owe. The IRS communicates almost exclusively through postal mail. If you receive a letter or notice from the IRS, do not ignore it. These letters often detail discrepancies found in your filed return, propose changes to your tax liability, or inform you of outstanding balances, penalties, and interest. Common notices include CP14 (Balance Due), CP2000 (Underreported Income), or various penalty notices. Always open and read IRS mail carefully, as it contains critical information about your tax status.

Official Channels to Verify Your IRS Account Status

The best way to confirm whether you owe the IRS is to go directly to the source. The IRS provides several official, secure methods for taxpayers to check their account status.

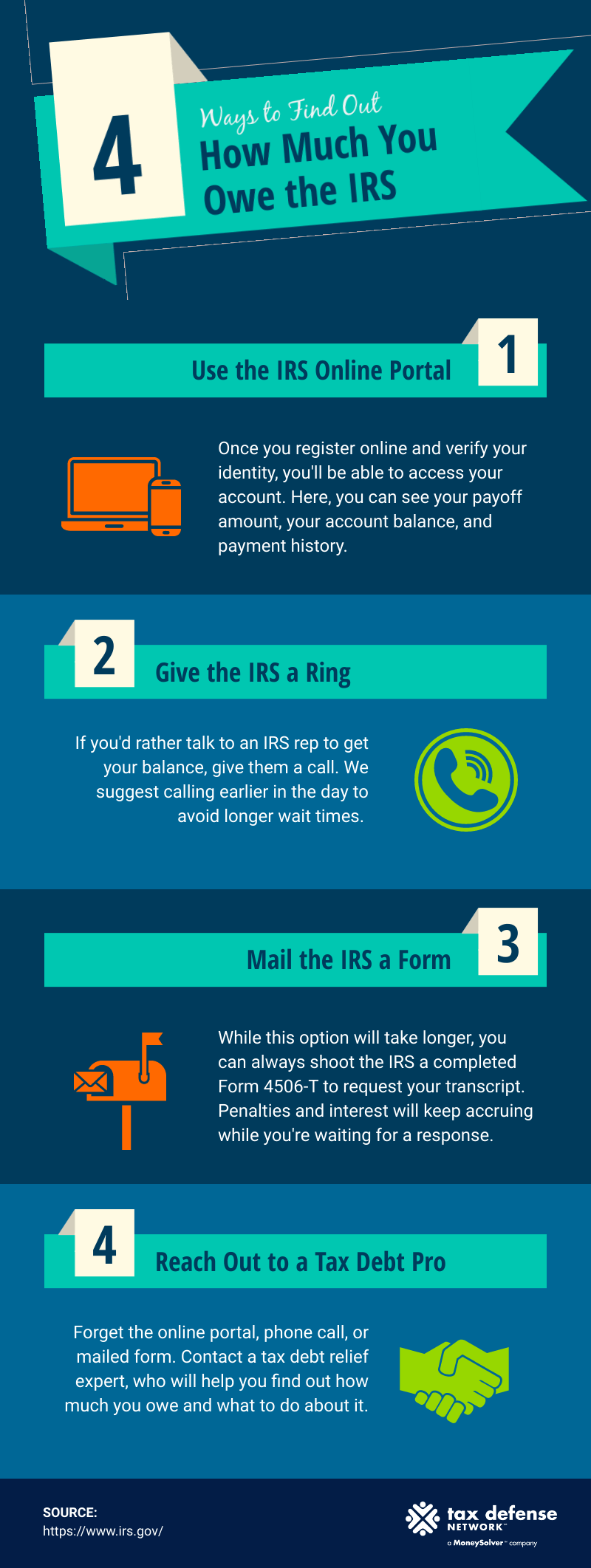

Using the IRS Online Account

The IRS Online Account is a powerful tool for individual taxpayers. By creating and accessing your account on the IRS website (IRS.gov), you can view:

- Your balance, including tax due for the current year and any payment plans.

- Your payment history and any scheduled or pending payments.

- Key information from your most recently filed tax return.

- Digital copies of certain IRS notices.

- Your tax records, including transcripts.

Setting up an account requires a robust identity verification process to protect your sensitive financial information, but it’s well worth the effort for the comprehensive access it provides.

Reviewing Your Tax Transcripts

Tax transcripts provide a detailed summary of your tax return information. While not a copy of your filed return, they contain line-by-line data from your return as it was processed by the IRS, along with any subsequent adjustments. There are different types of transcripts, including:

- Account Transcript: Shows basic data from your return, financial transactions, and any balance due.

- Record of Account Transcript: Combines the account transcript with line-item information from your filed return.

- Wage and Income Transcript: Shows data from information returns like W-2s, 1099s, and 1098s.

You can request these transcripts online, by mail, or by fax. The Account Transcript is particularly useful for checking if you have an outstanding balance or if a payment was applied correctly.

Contacting the IRS Directly

If you prefer to speak with someone or if online tools don’t provide the clarity you need, you can call the IRS directly. The main IRS toll-free number for individuals is 1-800-829-1040. Be prepared for potentially long wait times, especially during tax season. When you call, ensure you have your Social Security Number, date of birth, and your tax return from the prior year to verify your identity. The IRS representative can then access your account and inform you of any outstanding balances or issues.

Consulting a Tax Professional

For complex situations or if you feel overwhelmed, a qualified tax professional (such as a Certified Public Accountant (CPA), Enrolled Agent (EA), or tax attorney) can be an invaluable resource. They can often access your tax transcripts with your permission, interpret IRS notices, and clearly explain your tax situation. A professional can also represent you before the IRS, communicate on your behalf, and help devise a strategy for resolving any tax debt.

What to Do If You Discover You Owe the IRS

Finding out you owe the IRS can be daunting, but it’s a manageable situation. The worst thing you can do is ignore it. The IRS has mechanisms to collect outstanding taxes, and penalties and interest can accrue quickly.

Don’t Panic: Assess the Situation

The first step is to remain calm and thoroughly understand the amount owed and why. Review any IRS notices carefully. If the notice claims you owe due to underreported income, cross-reference it with your records (W-2s, 1099s). If you disagree with the IRS’s assessment, gather your documentation to support your position. If you agree, then focus on payment options.

Payment Options and Agreements

The IRS offers several ways to pay a tax debt:

- Pay in Full: If possible, paying the full amount as soon as possible is the best option to avoid additional penalties and interest. You can pay online, by phone, or by mail.

- Short-Term Payment Plan: If you can pay the full amount within 180 days, you might qualify for a short-term payment plan, though interest and penalties still apply.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. This is typically an option when you have little to no ability to pay the full amount, and the IRS determines that it would not be able to collect the full amount. The IRS considers your ability to pay, income, expenses, and asset equity when evaluating an OIC.

- Installment Agreement: If you can’t pay in full immediately, you can request an installment agreement, which allows you to make monthly payments for up to 72 months. There is a setup fee, and interest and penalties continue to accrue, but at a reduced rate.

Seeking Professional Guidance

When dealing with significant tax debt, complex notices, or if you believe the IRS has made an error, seeking advice from a tax professional is highly recommended. They can help you understand your options, negotiate with the IRS on your behalf, and ensure you pursue the most advantageous resolution strategy for your financial situation. They can also help you understand your rights and responsibilities as a taxpayer.

Amending Past Returns (If Necessary)

If you discover an error on a previously filed tax return that resulted in an underpayment, you can file an amended return using Form 1040-X. This is crucial if you, for example, forgot to report a source of income or made a mathematical error that decreased your tax liability erroneously. Amending your return corrects the mistake and ensures your records with the IRS are accurate, potentially preventing future penalties.

Proactive Steps to Avoid Future Tax Surprises

Preventing a tax debt is always better than resolving one. Implementing a few proactive strategies can significantly reduce your chances of owing the IRS in the future.

Quarterly Reviews and W-4 Adjustments

Regularly review your income and expenses throughout the year. If your income increases or decreases substantially, or if you have a significant life event, adjust your W-4 form with your employer promptly. You can use the IRS Tax Withholding Estimator tool on IRS.gov to help you determine the correct withholding amount. For self-employed individuals, re-evaluate your estimated tax payments each quarter to ensure they align with your projected annual income.

Build an Emergency Fund

Having an emergency fund isn’t just for unexpected job loss or medical bills; it can also be a lifeline for an unexpected tax bill. Setting aside money specifically for potential tax liabilities, especially if your income fluctuates, provides a buffer against financial stress.

Stay Informed and Organized

Tax laws can change, and staying updated on major developments can help you plan. Continuously maintain organized financial records. A well-organized system makes tax preparation easier, reduces errors, and puts you in a better position to verify your tax situation at any time.

In conclusion, knowing whether you owe the IRS is about being informed, proactive, and willing to engage with the available resources. By understanding the reasons for potential tax debt, utilizing the official IRS verification channels, and taking decisive action if a balance is found, you can navigate your tax obligations with confidence and maintain control over your financial health. Remember, the IRS generally wants to work with taxpayers, so open communication and timely action are always in your best interest.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.