Student loans can be a substantial financial burden, yet they are also an investment in your future. For many graduates, the transition from academic life to managing loan repayments can feel overwhelming. Understanding your obligations, exploring available options, and strategically planning your payments are crucial steps toward financial freedom. This comprehensive guide will dissect the complexities of student loan repayment, offering insights and actionable strategies to help you navigate your journey effectively and efficiently.

Understanding Your Student Loan Landscape

Before you can effectively pay your student loans, you must first understand what you owe. This involves taking a detailed inventory of your loans, knowing their terms, and identifying who services them. A clear picture of your debt is the foundation for any successful repayment strategy.

Types of Student Loans: Federal vs. Private

The first critical distinction to make is between federal and private student loans, as they offer vastly different protections, interest rates, and repayment options.

- Federal Student Loans: Issued by the U.S. Department of Education, these loans typically come with more flexible repayment plans, including income-driven options, deferment, and forbearance. They may also qualify for loan forgiveness programs. Examples include Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans, and Perkins Loans (though new Perkins loans are no longer being issued).

- Private Student Loans: These loans are issued by banks, credit unions, and other private lenders. They often have variable interest rates, fewer borrower protections, and stricter eligibility requirements. Repayment terms are generally less flexible, and options for deferment or forbearance are limited and at the discretion of the lender.

Knowing which type of loans you have is paramount, as it dictates the range of strategies available to you. Federal loans, with their inherent flexibilities, often provide a safety net that private loans do not.

Key Loan Terms to Know: Interest Rates, Repayment Period, Loan Servicer

Deciphering the jargon associated with student loans is essential for informed decision-making.

- Interest Rates: This is the cost of borrowing money, expressed as a percentage of the principal balance. Federal loan interest rates are fixed for the life of the loan, while private loans can have fixed or variable rates. Variable rates can fluctuate with market conditions, potentially increasing your monthly payments. Understanding your interest rates helps you prioritize which loans to pay off first, especially if some are significantly higher.

- Repayment Period: This is the length of time over which you are expected to repay your loan. Standard federal repayment plans are typically 10 years, but other options can extend this period to 20 or 25 years. Private loan repayment periods vary widely based on the lender and loan terms. A longer repayment period usually means lower monthly payments but more interest paid over the life of the loan.

- Loan Servicer: This is the company that handles the billing and other services for your loan. They are your primary point of contact for questions about your balance, payment options, and deferment/forbearance requests. For federal loans, common servicers include Nelnet, Aidvantage, MOHELA, and Edfinancial. For private loans, it will be the bank or financial institution that issued the loan. Keeping track of your servicer(s) is crucial for managing your account.

The Importance of Loan Inventory

Before making any strategic moves, create a comprehensive list of all your student loans. Include:

- Loan Type (Federal/Private)

- Original Loan Amount

- Current Balance

- Interest Rate (fixed or variable)

- Loan Servicer

- Minimum Monthly Payment

- Original Repayment Start Date

This inventory will serve as your roadmap, highlighting high-interest loans that might warrant aggressive repayment and identifying federal loans eligible for specific programs. You can access federal loan information through the National Student Loan Data System (NSLDS) or studentaid.gov. For private loans, check your credit report or contact the lenders directly.

Navigating Standard Repayment Strategies

Once you have a clear understanding of your loans, you can begin to explore the various repayment strategies available. The “standard” approach involves making consistent payments, but there are nuances even within this seemingly straightforward method.

Standard Repayment Plan

The default repayment plan for federal student loans is the Standard Repayment Plan. This plan spreads your payments out equally over a 10-year period (or 10 to 30 years for consolidated loans). While it often results in the highest monthly payments compared to other federal plans, it also ensures you pay the least amount of interest over the life of the loan. This plan is ideal for borrowers who can comfortably afford the monthly payments and want to minimize their overall cost of borrowing.

Graduated Repayment Plan

For those who expect their income to increase over time, the Graduated Repayment Plan offers an alternative. Under this plan, payments start lower and gradually increase every two years, typically over a 10-year period. While it can ease the financial burden in the initial years after graduation, borrowers will pay more interest over the life of the loan compared to the Standard Repayment Plan due to the smaller initial payments.

Extended Repayment Plan

If you have a large student loan balance (over $30,000 in direct loans) and need lower monthly payments than the standard plan offers, the Extended Repayment Plan might be suitable. This plan allows you to extend your repayment period for up to 25 years, resulting in significantly lower monthly payments. However, like the Graduated Plan, extending the repayment period means you will pay substantially more interest over the long term. This plan is available for both federal Direct Loans and FFEL Program loans.

The Power of Extra Payments

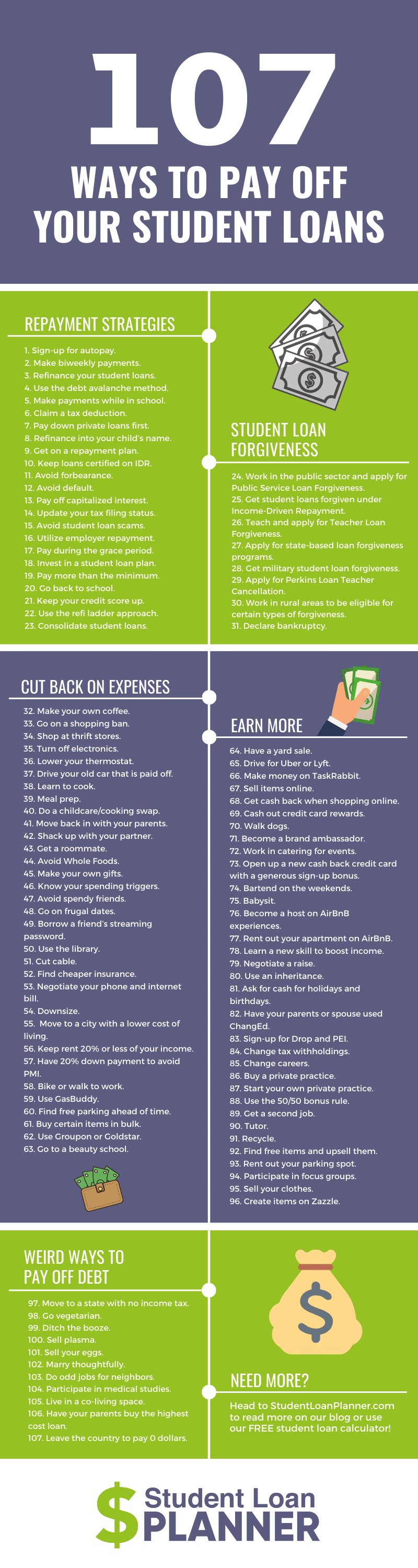

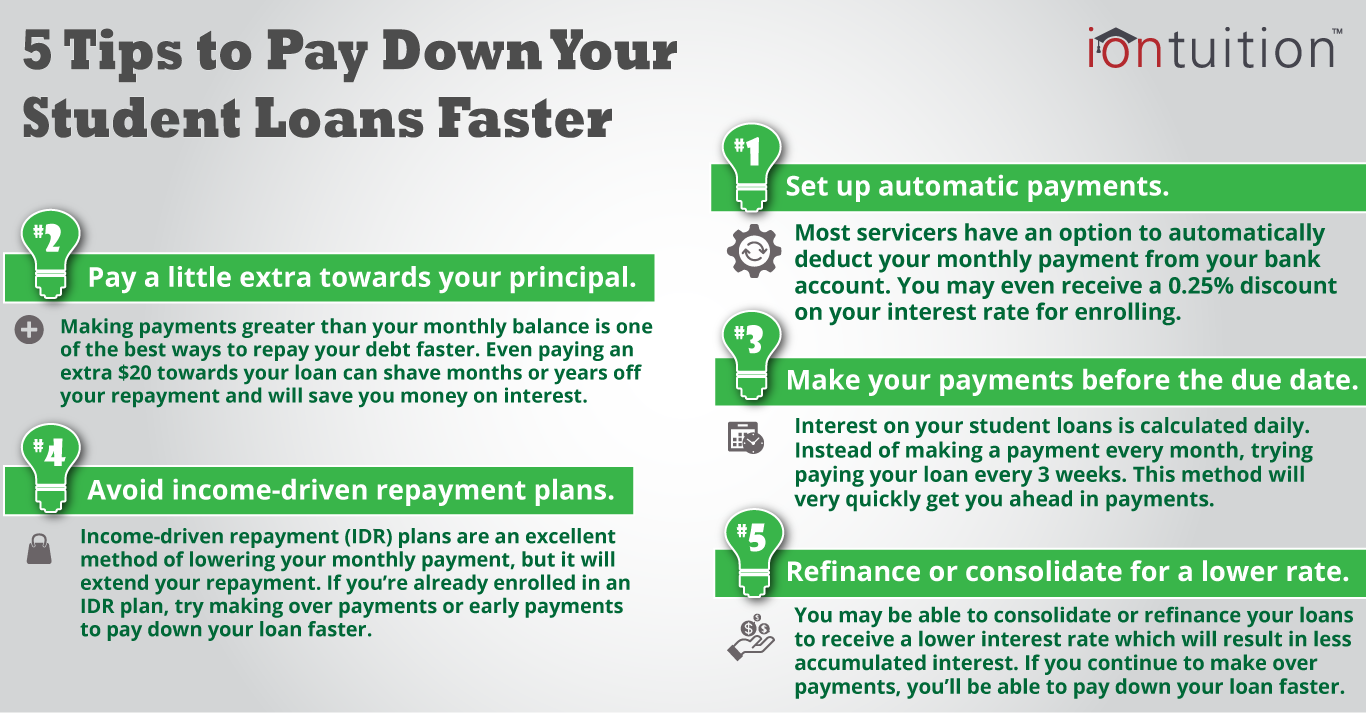

Regardless of the plan you’re on, making extra payments can dramatically reduce the total interest paid and shorten your repayment timeline. Even small additional contributions can make a big difference. When making extra payments, always specify to your loan servicer that the additional amount should be applied to the principal balance of a specific loan, ideally the one with the highest interest rate. This strategy, known as the “debt avalanche” method, is mathematically the most efficient way to save money on interest.

Exploring Income-Driven Repayment (IDR) Options

For federal loan borrowers facing financial hardship or who anticipate their income to be modest relative to their debt, Income-Driven Repayment (IDR) plans offer a vital safety net. These plans adjust your monthly payment based on your income and family size.

What are IDR Plans? (PAYE, REPAYE, IBR, ICR)

There are several federal IDR plans, each with slightly different terms:

- Pay As You Earn (PAYE): Generally caps payments at 10% of your discretionary income, recalculated annually. Remaining balance is forgiven after 20 years of payments.

- Revised Pay As You Earn (REPAYE) / SAVE: Also caps payments at 10% of discretionary income (or 5% for undergraduate loans starting July 2024), but includes both undergraduate and graduate loans. Any remaining balance is forgiven after 20 years for undergraduate loans or 25 years for graduate loans. This plan is generally more generous in its calculation of discretionary income, providing lower payments for many.

- Income-Based Repayment (IBR): Caps payments at 10% or 15% of your discretionary income, depending on when you took out your loans. Remaining balance is forgiven after 20 or 25 years.

- Income-Contingent Repayment (ICR): The oldest IDR plan, payments are capped at 20% of your discretionary income or what you’d pay on a fixed 12-year plan, whichever is less. Remaining balance is forgiven after 25 years.

Discretionary income is typically the difference between your adjusted gross income (AGI) and 150% of the poverty guideline for your family size. These plans are designed to make loan payments affordable, even if your income is low.

Who Benefits from IDR?

IDR plans are particularly beneficial for:

- Borrowers with a high debt-to-income ratio.

- Individuals in public service careers aiming for Public Service Loan Forgiveness (PSLF), as IDR payments count toward the 120 required payments.

- Anyone experiencing temporary or long-term financial hardship.

- Those who value the safety net of lower payments, even if it means paying more interest over time or aiming for eventual loan forgiveness.

It’s crucial to understand that while IDR plans offer lower monthly payments, they often lead to more interest accruing over the life of the loan. If your balance is forgiven, the forgiven amount may be considered taxable income by the IRS, unless you qualify for specific exemptions (like PSLF).

Annual Recertification and Its Importance

To remain on an IDR plan, you must reapply and provide updated income and family size information annually. Your loan servicer will notify you when it’s time to recertify. Failing to recertify on time can lead to your monthly payments reverting to the standard 10-year amount, and any unpaid interest capitalizing (being added to your principal balance), increasing your overall debt. Timely recertification is critical to maintaining affordable payments and tracking progress toward loan forgiveness.

Strategies for Managing Difficult Repayment Situations

Life is unpredictable, and sometimes even the best-laid financial plans go awry. Fortunately, federal student loan programs offer mechanisms to help borrowers navigate periods of financial difficulty.

Deferment and Forbearance: When to Use Them

Both deferment and forbearance allow you to temporarily postpone or reduce your student loan payments. However, they differ in how interest accrues and who qualifies.

- Deferment: During deferment, the U.S. Department of Education pays the interest on subsidized federal loans. Interest continues to accrue on unsubsidized federal loans and private loans. Common reasons for deferment include unemployment, economic hardship, active military service, or returning to school.

- Forbearance: Interest typically accrues on all types of loans (subsidized and unsubsidized federal, and private) during forbearance. This is a more general option for financial hardship or medical leave, often used when you don’t qualify for deferment.

Both options should be used judiciously, as they extend your repayment period and generally increase the total amount you pay due to interest capitalization (when unpaid interest is added to your principal). They are intended as temporary relief, not long-term solutions. Always explore IDR plans first if your hardship is due to low income, as they are generally a better long-term solution.

Loan Consolidation: Streamlining Your Payments

Federal student loan consolidation allows you to combine multiple federal student loans into a single Direct Consolidation Loan. This can simplify your repayment by giving you one monthly payment and one loan servicer. The interest rate on a Direct Consolidation Loan is the weighted average of your original loans’ interest rates, rounded up to the nearest one-eighth of a percent.

Benefits of consolidation include:

- Simplification: One payment instead of many.

- Access to New Repayment Plans: Can make certain loans (like FFEL Program loans) eligible for IDR plans or PSLF.

- Extended Repayment Period: Can extend your repayment period up to 30 years, lowering monthly payments (but increasing total interest paid).

However, consolidating can also cause you to lose certain borrower benefits associated with your original loans, such as interest rate discounts. It also resets the clock on your repayment and any progress toward loan forgiveness programs (unless you strategically consolidate to access PSLF and have a specific type of older loan).

Refinancing Private Student Loans: Lowering Interest Rates

Refinancing is a process where a private lender pays off your existing student loans (federal or private) and issues you a new loan with new terms and a new interest rate. This is distinct from federal consolidation.

Refinancing can be highly beneficial if you have a strong credit score and stable income, as it can potentially lead to a lower interest rate, which translates to significant savings over the life of the loan. You can also choose a new repayment period.

However, there’s a crucial caveat: Refinancing federal student loans into a private loan means you lose all the federal protections, benefits, and repayment options, including IDR plans, deferment, forbearance, and access to federal loan forgiveness programs. This trade-off should be carefully considered. It’s generally recommended for borrowers with a strong financial footing who are confident they won’t need federal protections and want to aggressively pay down their debt.

Advanced Strategies and Loan Forgiveness Programs

Beyond standard repayment and hardship relief, there are advanced strategies and specific programs designed to alleviate the student loan burden for qualifying individuals.

Public Service Loan Forgiveness (PSLF)

PSLF is a powerful program designed to forgive the remaining balance on your federal Direct Loans after you have made 120 qualifying monthly payments while working full-time for a qualifying employer.

To qualify:

- You must have federal Direct Loans (other federal loans can become eligible if consolidated into a Direct Loan).

- You must be on an income-driven repayment plan.

- You must make 120 qualifying payments (10 years’ worth) while employed full-time by a U.S. federal, state, local, or tribal government organization, or a qualifying non-profit organization.

PSLF offers immense relief for public servants, potentially forgiving hundreds of thousands of dollars in debt. It is crucial to track your employment and payments carefully, utilizing the PSLF Help Tool on studentaid.gov.

Teacher Loan Forgiveness and Other Specific Programs

Beyond PSLF, other loan forgiveness programs cater to specific professions or circumstances:

- Teacher Loan Forgiveness: Forgives up to $17,500 of Direct Subsidized/Unsubsidized Loans or FFEL Program loans for highly qualified teachers who teach for five consecutive years in low-income schools.

- Perkins Loan Cancellation: Teachers, nurses, law enforcement officers, and other professionals may qualify for full cancellation of their Perkins Loans after a certain period of service.

- Disability Discharge: If you become permanently and totally disabled, you may qualify for a Total and Permanent Disability (TPD) discharge of your federal student loans.

- Borrower Defense to Repayment: Offers loan forgiveness if your school misled you or engaged in misconduct in violation of state law.

Research these programs thoroughly to see if your profession or circumstances align with the eligibility requirements.

Strategies for Tackling High-Interest Debt First

For those not pursuing forgiveness and who have the means, aggressively tackling high-interest loans first (the “debt avalanche” method) is the most financially efficient strategy. List all your loans by interest rate, highest to lowest. Make minimum payments on all loans, then direct any extra money you can afford to the loan with the highest interest rate. Once that loan is paid off, roll the payment amount you were making (minimum plus extra) into the next highest interest rate loan. This method saves the most money on interest over time.

The Role of Budgeting in Loan Repayment

Effective student loan repayment is intrinsically linked to sound personal finance. A robust budget is the cornerstone of managing your money, ensuring you have enough to cover your loan payments while still meeting other financial obligations and savings goals.

- Create a Detailed Budget: Track all your income and expenses. Identify areas where you can cut back to free up more money for loan payments.

- Automate Payments: Set up automatic payments to avoid missing deadlines and potentially qualify for a small interest rate reduction from your servicer.

- Build an Emergency Fund: Having an emergency fund of 3-6 months’ worth of living expenses is crucial. It provides a buffer against unexpected financial setbacks, preventing you from missing loan payments or needing to resort to deferment/forbearance.

- Increase Income: Consider side hustles, freelance work, or negotiating a raise to accelerate your repayment.

Paying off student loans can be a long journey, but with a clear understanding of your options, a strategic plan, and consistent effort, you can navigate the path to financial freedom. Remember to regularly review your financial situation and adapt your strategy as your income, expenses, and loan terms evolve.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.