The Free Application for Federal Student Aid (FAFSA) is a cornerstone of college funding for millions of students each year. It’s the gateway to federal grants, scholarships, work-study programs, and federal student loans. For many, receiving that financial aid offer letter is a moment of both anticipation and, often, confusion. The document, packed with acronyms and figures, can be daunting. Understanding “how much FAFSA did I get?” isn’t just about spotting a total number; it’s about dissecting your award package, grasping its implications, and strategically planning your educational investment. This guide aims to demystify your financial aid offer, empowering you to make informed decisions about funding your higher education journey.

The FAFSA Journey: From Application to Award Letter

The path to receiving your financial aid offer begins long before the letter arrives. It starts with the meticulous completion and submission of the FAFSA, which collects crucial financial information from you and your family. This data then undergoes a federal calculation to determine your eligibility for various aid types.

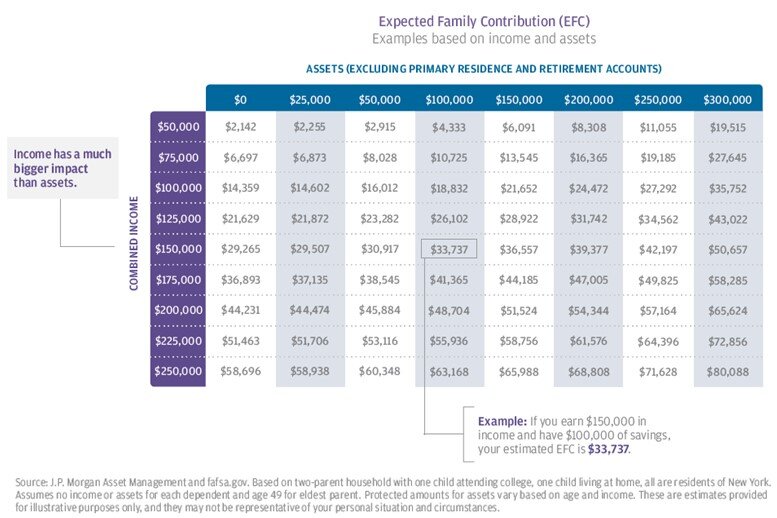

Understanding Your Student Aid Index (SAI)

Historically, this calculation yielded an Expected Family Contribution (EFC). However, with the implementation of the FAFSA Simplification Act, the EFC has been replaced by the Student Aid Index (SAI). The SAI is a number derived from the financial information you provide on your FAFSA, representing an eligibility index used to determine the types and amounts of federal student aid you may receive. A lower SAI generally indicates a higher level of financial need. It’s important to note that the SAI is not the amount of money your family is expected to pay; rather, it’s an eligibility index that colleges use to calculate your financial need. This need is the difference between the school’s Cost of Attendance (COA) and your SAI.

The Role of Cost of Attendance (COA)

Every college and university establishes a Cost of Attendance (COA), which is an estimated total cost of attending that institution for one academic year. The COA isn’t just tuition and fees; it’s a comprehensive figure that includes:

- Tuition and Fees: The direct costs charged by the institution for instruction.

- Room and Board: Costs for housing and meals, whether on-campus or an estimated allowance for off-campus living.

- Books and Supplies: An allowance for textbooks, course materials, and other academic necessities.

- Transportation: An allowance for travel to and from campus.

- Personal Expenses: An allowance for miscellaneous costs like toiletries, laundry, and entertainment.

Your financial aid eligibility is directly tied to this COA. A school subtracts your SAI from its COA to determine your financial need: COA – SAI = Financial Need. Colleges then attempt to meet this demonstrated need through various aid components.

The Timeline of Your Financial Aid Offer

While the FAFSA typically opens on October 1st (with the exception of the 2024-25 FAFSA, which opened later), the timing of your financial aid offer can vary significantly. Most colleges begin sending out financial aid packages shortly after you receive your admission decision, often in late winter or early spring (February to April). However, some institutions, especially those with rolling admissions, might send them earlier or later. It’s crucial to be aware of each school’s specific timeline and deadlines for accepting or declining aid. Missing these deadlines can result in forfeiture of certain aid types.

Deconstructing Your Financial Aid Package

Once your financial aid offer arrives, it’s critical to understand each component. Financial aid generally comes in two main forms: “gift aid” (money you don’t have to repay) and “self-help aid” (money you do repay, or earn).

Grant Money: Free Aid You Don’t Repay

Grants are the most desirable form of financial aid because they do not need to be repaid. They are typically awarded based on financial need, as determined by your FAFSA. Key federal grants include:

- Pell Grants: These are awarded to undergraduate students with exceptional financial need. The maximum award changes annually and depends on your SAI and enrollment status.

- Federal Supplemental Educational Opportunity Grants (FSEOG): Administered directly by colleges, FSEOGs are for undergraduate students with the greatest financial need and are limited in funds, so apply early.

- Teacher Education Assistance for College and Higher Education (TEACH) Grants: These grants require recipients to commit to teaching in high-need fields in low-income schools for a specified period after graduation. If the service obligation isn’t met, the grant converts to a loan.

Many states and individual colleges also offer their own grant programs, often based on specific criteria like state residency, academic merit, or specific areas of study.

Scholarships: Merit-Based and Need-Based Opportunities

Like grants, scholarships are funds you don’t have to repay. While some scholarships are need-based, many are awarded based on merit, specific talents (e.g., athletics, arts), academic achievements, community service, or affiliation with particular groups (e.g., ethnicity, religion, employer). Scholarships can come from:

- The College/University: Many institutions offer their own scholarship programs, often tied to admission.

- Private Organizations: Thousands of private organizations, foundations, corporations, and community groups offer scholarships. These require separate applications and often have specific eligibility criteria.

- State Programs: Many states have scholarship programs for residents.

It’s important to actively seek out and apply for external scholarships, as they can significantly reduce your borrowing needs.

Federal Student Loans: Understanding the Types and Terms

Unlike grants and scholarships, loans must be repaid with interest. Federal student loans generally offer more favorable terms than private loans, including fixed interest rates, income-driven repayment options, and potential for deferment or forbearance in times of financial hardship. The main types include:

- Direct Subsidized Loans: Available to undergraduate students with demonstrated financial need. The U.S. Department of Education pays the interest while you’re in school at least half-time, during the grace period (typically six months after you leave school), and during deferment periods.

- Direct Unsubsidized Loans: Available to undergraduate and graduate students regardless of financial need. You are responsible for all interest that accrues on an unsubsidized loan from the time it’s disbursed. You can choose to pay the interest while in school or allow it to accrue and be capitalized (added to the principal balance).

- Direct PLUS Loans: These are available to graduate or professional students (Grad PLUS) and parents of dependent undergraduate students (Parent PLUS). Eligibility is not based on financial need, but a credit check is required. The maximum amount you can borrow is the cost of attendance minus any other financial aid received.

It’s crucial to understand the interest rates, origination fees, and repayment terms associated with each loan type before accepting.

Work-Study Programs: Earning While Learning

Federal Work-Study (FWS) is a need-based program that allows eligible students to earn money to help pay for educational expenses through part-time jobs, either on or off campus. These jobs are often related to your course of study or community service. FWS funds are not disbursed directly to you at the beginning of the semester; instead, you earn the money as you work. This allows you to gain valuable work experience while funding your education without incurring debt.

Evaluating Your Financial Aid Offer: Is It Enough?

Receiving your financial aid offer is just the first step. The next, and perhaps most critical, is to evaluate whether the aid provided is sufficient to cover your educational costs, and if the overall package represents a good financial decision for your future.

Comparing Offers Across Institutions

If you’ve applied to multiple schools, you’ll likely receive different financial aid packages. It’s essential to compare these offers side-by-side, focusing on the “net price” – the cost you’ll actually pay after grants and scholarships are deducted. A school with a higher sticker price might, surprisingly, offer a better net price due to generous institutional grants. Create a spreadsheet to compare:

- Total COA for each school.

- Total grant and scholarship aid.

- Net Price (COA – Grants/Scholarships).

- Amount of federal loans offered.

- Work-study opportunities.

Identifying Unmet Need

After subtracting all gift aid (grants and scholarships) and federal student loans from your COA, you might still have an “unmet need” or a “gap.” This is the amount you or your family will need to cover through savings, private loans, or additional scholarships. It’s vital to identify this gap early to strategize how to fill it without incurring excessive high-interest debt.

The Importance of Net Price Calculators

Before you even apply, Net Price Calculators, available on every college’s website, can provide an estimate of your individualized net price. While not a guarantee, using these tools gives you a realistic preview of what you might expect to pay and can help you gauge the affordability of different institutions relative to your family’s financial situation.

Strategies for Addressing Financial Gaps

If your initial financial aid package doesn’t fully cover your educational expenses, don’t despair. Several strategies can help you bridge the gap.

Appealing Your Financial Aid Offer

Circumstances can change rapidly, and the financial information you provided on your FAFSA might no longer accurately reflect your current financial situation. If your family has experienced a significant change – such as job loss, reduction in income, high medical expenses, or other unusual circumstances – you may be able to appeal your financial aid offer. Contact the financial aid office at your college, explain your situation, and be prepared to provide documentation. This process is often called “professional judgment” or “special circumstances review.”

Exploring External Scholarship Opportunities

The search for scholarships doesn’t end after you apply for aid. Many organizations offer scholarships with deadlines throughout the year. Dedicate time to searching scholarship databases (e.g., Fastweb, Scholarship.com, College Board), local community foundations, and professional organizations related to your intended major. Even small scholarships can add up.

Considering Private Student Loans (with Caution)

If all other options are exhausted, private student loans from banks or credit unions can help cover remaining costs. However, these generally come with higher, variable interest rates, fewer borrower protections, and often require a creditworthy co-signer. Always exhaust federal loan options before considering private loans, and only borrow what is absolutely necessary. Understand all terms and conditions before committing.

Smart Budgeting and Financial Planning During College

Once you’re in college, meticulous budgeting can help stretch your aid dollars further. Track your expenses for housing, food, books, and personal items. Look for ways to save money, such as living frugally, working a part-time job (beyond work-study), buying used textbooks, and taking advantage of student discounts. Every dollar saved is a dollar you might not have to borrow.

Responsible Borrowing and Future Financial Health

Understanding “how much FAFSA did I get” also encompasses a forward-looking perspective, particularly concerning student loans and your post-graduation financial health.

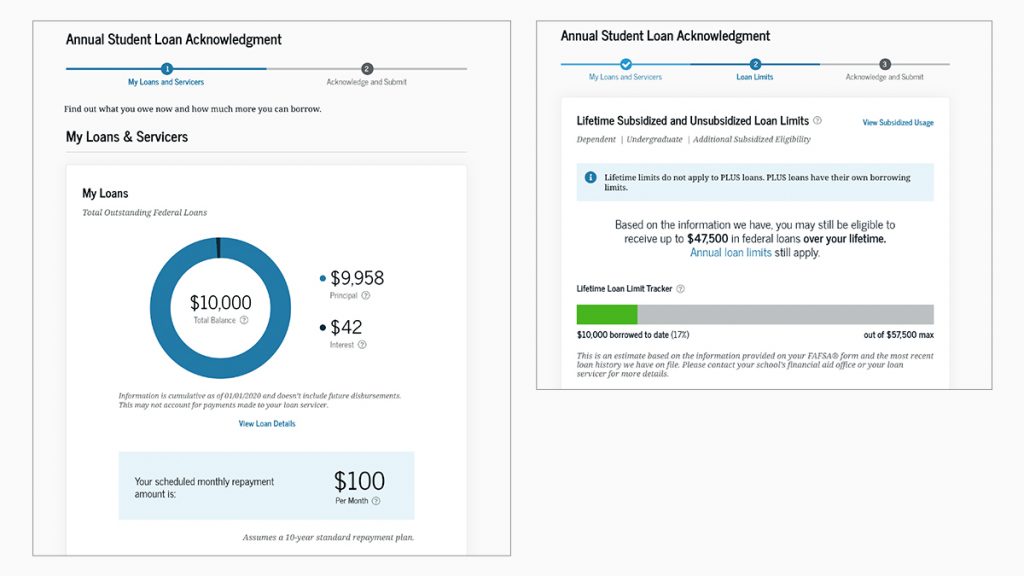

Understanding Loan Repayment Obligations

Federal student loans typically enter repayment six months after you graduate, leave school, or drop below half-time enrollment. You’ll choose a repayment plan, which can range from standard (fixed payments over 10 years) to income-driven (payments adjusted based on your income and family size). Knowing your total loan balance and estimated monthly payments before you even graduate is crucial for post-college budgeting.

The Impact of Student Debt on Your Financial Future

While student loans are an investment in your future, excessive debt can significantly impact your financial freedom post-graduation. High monthly payments can delay major life milestones such as buying a home, starting a family, or saving for retirement. Be mindful of the long-term implications of every dollar you borrow. Borrow only what you need, not what you’re offered.

Building a Strong Financial Foundation Post-Graduation

Even with student loan debt, you can build a strong financial foundation. Focus on:

- Budgeting: Continue to live within your means.

- Emergency Fund: Build a savings cushion to handle unexpected expenses.

- Debt Management: Prioritize high-interest debts, including private student loans if you have them.

- Savings and Investing: Start saving for retirement and other long-term goals as early as possible.

Understanding your FAFSA offer is a critical step in financing your education responsibly. By carefully reviewing your financial aid package, understanding the types of aid you’re offered, and proactively addressing any gaps, you can navigate the complexities of college funding with confidence, setting yourself up for academic success and a healthier financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.