The pursuit of homeownership is a cornerstone of the American dream, and for the nation’s veterans, service members, and eligible surviving spouses, the VA loan program stands as a powerful testament to that dream. Administered by the U.S. Department of Veterans Affairs, this program offers significant benefits designed to make homeownership more accessible and affordable. However, a common misconception often arises when discussing these loans: the idea of a single, fixed “VA interest rate” that applies to all borrowers. In reality, while VA loans are known for their competitive rates, the interest rate you secure is a dynamic figure influenced by a multitude of factors. Understanding these nuances is crucial for any eligible borrower looking to leverage this invaluable benefit.

This comprehensive guide aims to demystify VA loan interest rates, breaking down what they are, how they are determined, and how borrowers can navigate the market to secure the most favorable terms. We’ll explore the underlying principles of the VA loan program, delve into the specific variables that influence your rate, and provide actionable strategies to ensure you make the most informed financial decisions on your path to homeownership.

Understanding the VA Loan Program and Its Unmatched Benefits

Before diving into the specifics of interest rates, it’s essential to grasp the fundamental nature of the VA loan program. Established in 1944 as part of the Servicemen’s Readjustment Act (the “G.I. Bill”), VA loans were designed to help returning World War II veterans purchase homes without needing a down payment. Today, the program continues this mission, offering one of the most advantageous mortgage options available.

Who is Eligible for a VA Loan?

Eligibility is primarily determined by service history and status. Generally, active-duty service members, veterans, National Guard members, Reservists, and certain surviving spouses are eligible. The specific requirements include minimum service durations, which vary based on when and where an individual served. A Certificate of Eligibility (COE) is the official document confirming a veteran’s eligibility for the VA home loan benefit. Obtaining a COE is typically the first step in the VA loan process and can often be facilitated by a VA-approved lender. This step confirms that the individual has met the service requirements set forth by the VA, paving the way for accessing the program’s myriad benefits.

Key Advantages of VA Loans

VA loans stand out due to several compelling benefits that significantly reduce the barriers to homeownership:

- No Down Payment Requirement: This is perhaps the most celebrated benefit. Eligible borrowers can purchase a home with no money down, saving them years of arduous saving that might be required for conventional loans. This feature is particularly impactful for younger service members or those just starting their careers, making homeownership a realistic goal much sooner.

- No Private Mortgage Insurance (PMI): Unlike conventional loans with less than a 20% down payment or FHA loans, VA loans do not require PMI. This can result in substantial savings on monthly payments, often hundreds of dollars, over the life of the loan. The absence of PMI is a direct financial advantage that significantly enhances affordability.

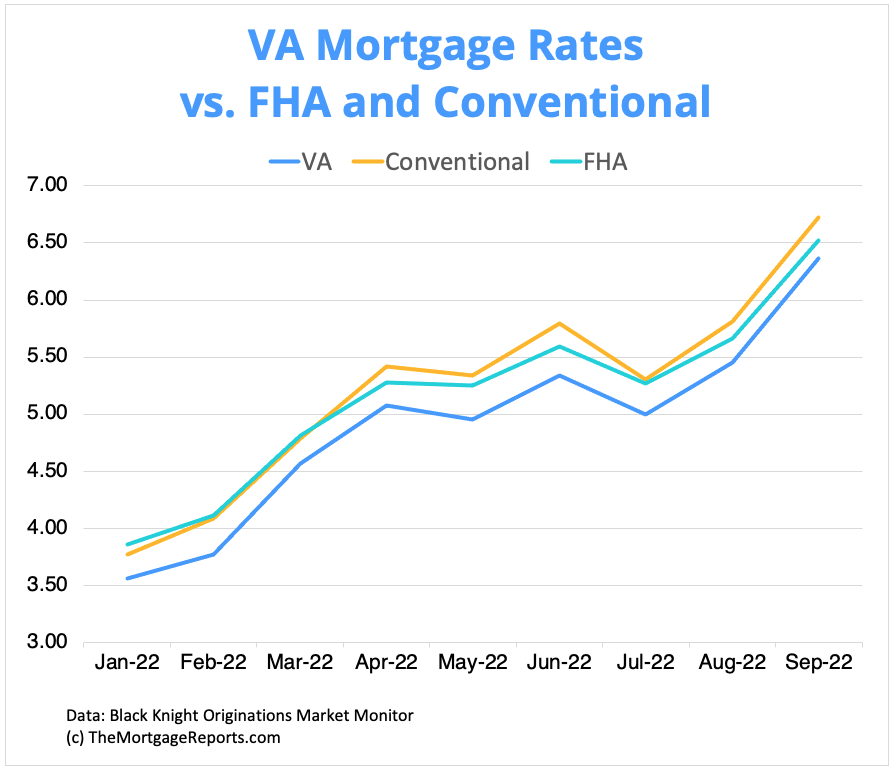

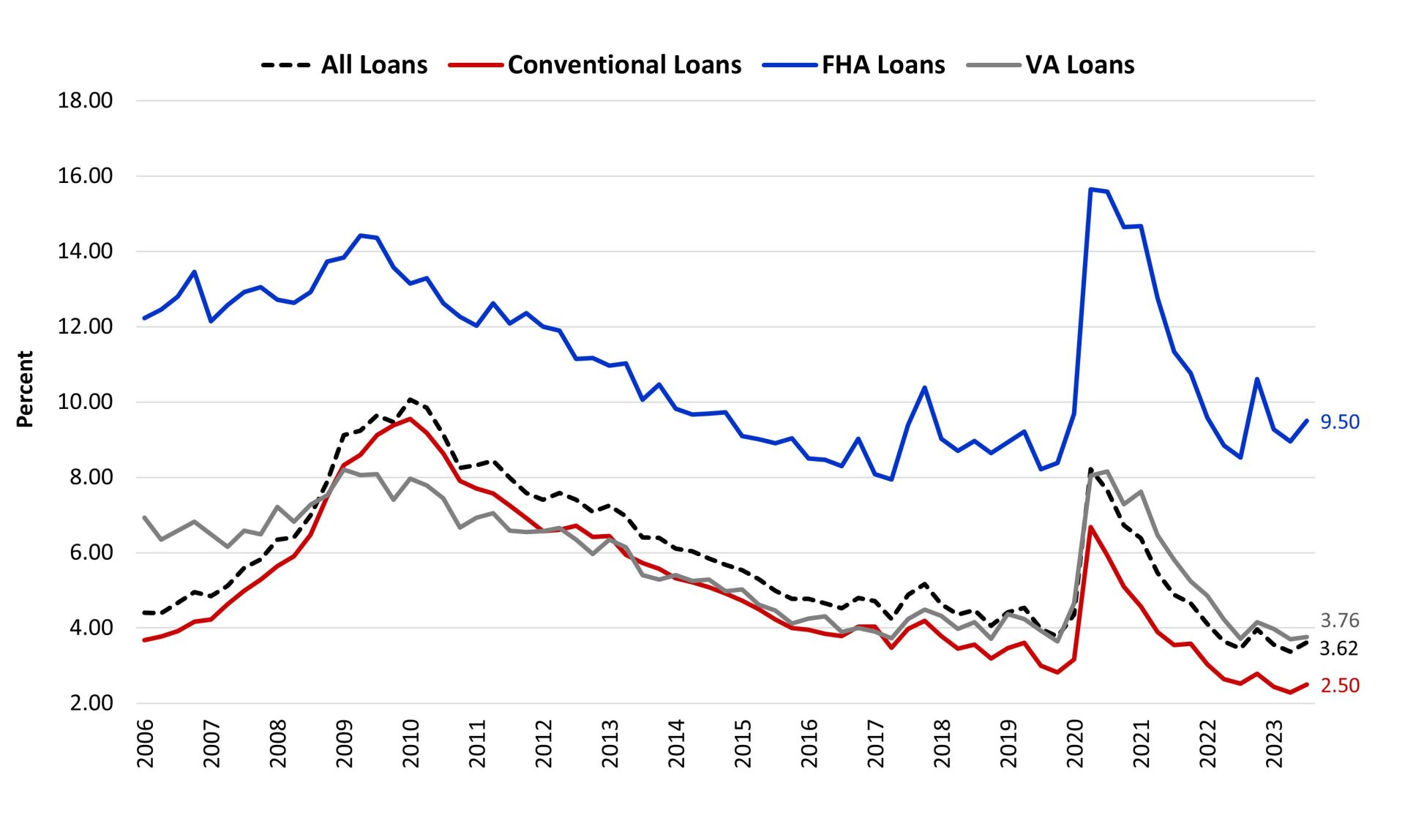

- Competitive Interest Rates: While there isn’t a single “VA interest rate,” the program typically offers rates that are competitive with, and often lower than, those found with conventional and FHA loans. This is due to the VA’s guarantee to lenders, which reduces their risk.

- Limited Closing Costs: The VA sets limits on certain closing costs lenders can charge, and some fees, like the VA funding fee, can be waived for veterans with service-connected disabilities.

- No Prepayment Penalties: Borrowers can pay off their loan early without incurring any additional fees, providing financial flexibility.

- Assumability: Under certain conditions, VA loans can be assumed by another eligible veteran, which can be an attractive feature for future buyers, especially in a rising interest rate environment.

How VA Loans Differ from Conventional and FHA Loans

Understanding these differences highlights the unique value of the VA loan. Conventional loans often require a significant down payment and mandate PMI if less than 20% is put down. FHA loans, while offering low down payment options, always require mortgage insurance premiums (MIP), both upfront and annually, for the life of the loan in many cases. The VA loan, with its no down payment and no PMI features, often provides a superior financial package for eligible borrowers, making it a cornerstone of accessible home financing.

Deconstructing VA Loan Interest Rates

The question “what is the VA interest rate?” is not easily answered with a single number because, like all mortgage products, VA loan interest rates are subject to market forces and individual borrower characteristics. The VA does not set interest rates; rather, they are determined by individual lenders within the competitive mortgage market. The VA’s role is to guarantee a portion of the loan, which encourages private lenders to offer favorable terms to veterans.

The Myth of a Single “VA Interest Rate”

It’s crucial to dispel the notion that the VA dictates a universal interest rate. Instead, the VA provides the framework and guarantee, allowing approved private lenders (banks, credit unions, mortgage companies) to originate these loans. Each lender sets its own rates based on its operational costs, profit margins, and risk assessment, all while adhering to VA guidelines. This means that comparing offers from multiple lenders is not just advisable, but essential, to find the best available rate.

Factors Influencing Your VA Interest Rate

Several key factors play a significant role in determining the specific interest rate you will be offered for your VA loan:

- Credit Score: Your credit score is one of the most critical determinants. Lenders use it as an indicator of your creditworthiness and your likelihood of repaying the loan. A higher credit score (typically 700+) signals lower risk to a lender, usually resulting in a lower interest rate. While the VA itself doesn’t set a minimum credit score, individual lenders often have their own internal credit score requirements, which are typically in the mid-600s or higher.

- Loan Term: The length of your mortgage loan (e.g., 15-year or 30-year fixed-rate) significantly impacts the interest rate. Shorter-term loans generally come with lower interest rates because the lender’s risk is spread over a shorter period. However, shorter terms also mean higher monthly payments.

- Market Conditions: Mortgage interest rates are intrinsically linked to the broader economic environment. Factors such as inflation, the Federal Reserve’s monetary policy, and the bond market directly influence daily interest rates. When the economy is robust and inflation is a concern, rates tend to rise. Conversely, during periods of economic uncertainty or lower inflation, rates may fall. These fluctuations mean that the best time to lock in a rate can change frequently.

- Lender-Specific Offerings: Different lenders have different overheads, pricing strategies, and risk appetites. One lender might offer a slightly lower rate but charge higher closing costs, while another might have a slightly higher rate but more competitive fees. This variation underscores the importance of shopping around.

- Loan Type (Fixed vs. ARM): Whether you choose a fixed-rate mortgage or an adjustable-rate mortgage (ARM) will also affect the initial interest rate. Fixed rates offer stability and predictability for your monthly payments, locking in the same rate for the life of the loan. ARMs typically start with a lower introductory rate for a set period (e.g., 3, 5, 7, or 10 years) before adjusting periodically based on market indexes. While ARMs can offer lower initial payments, they carry the risk of future rate increases.

Fixed-Rate vs. Adjustable-Rate VA Mortgages

Most VA loan borrowers opt for a fixed-rate mortgage, providing peace of mind with stable monthly principal and interest payments for the entire loan term (typically 30 or 15 years). This predictability is a huge advantage for personal financial planning. However, VA-guaranteed ARMs are also available. These loans can be attractive for those who expect to sell or refinance before the introductory fixed-rate period ends, or for those who anticipate their income increasing substantially in the future. The choice between fixed and ARM depends heavily on your financial situation, risk tolerance, and long-term housing plans.

How to Secure the Best VA Interest Rate

Given that VA interest rates are not uniform, strategically approaching the loan process can significantly impact the rate you ultimately receive. A proactive and informed approach can translate into substantial savings over the life of your mortgage.

Boosting Your Creditworthiness

Your credit score is paramount. Before even contacting lenders, review your credit report for inaccuracies and work to improve your score. This involves:

- Paying bills on time: Payment history accounts for a large portion of your credit score.

- Reducing outstanding debt: Lowering your credit utilization ratio can boost your score.

- Avoiding new credit applications: Each new application can temporarily ding your score.

- Correcting errors: Dispute any inaccuracies on your credit report immediately.

A higher credit score demonstrates to lenders that you are a reliable borrower, directly correlating with a lower interest rate offer.

Shopping Around for Lenders

This cannot be overstressed. Because interest rates and fees vary between lenders, obtaining quotes from multiple VA-approved lenders is critical. Don’t just look at the interest rate; compare the Annual Percentage Rate (APR), which includes the interest rate plus certain fees, to get a truer picture of the overall cost. Requesting quotes from at least three to five different lenders within a short window (typically 14-45 days) will allow you to compare offers without further impacting your credit score. Many lenders specialize in VA loans and may offer more competitive terms due to their expertise and volume.

Understanding Discount Points and Origination Fees

When evaluating loan offers, you’ll encounter terms like “discount points” and “origination fees.”

- Discount Points (or “Points”): These are upfront fees paid to the lender in exchange for a lower interest rate. One point typically equals 1% of the loan amount. For example, on a $300,000 loan, one point would be $3,000. Paying points can reduce your monthly payment and save you money over the long term, especially if you plan to stay in the home for many years. You need to calculate the “break-even point” to determine if paying points is financially advantageous for your specific situation.

- Origination Fees: These are charges from the lender for processing and underwriting your loan. The VA limits the origination fee that lenders can charge, typically to 1% of the loan amount. Understanding these fees and how they contribute to your overall closing costs is vital.

Locking In Your Rate

Once you’ve found a competitive rate, consider “locking” it in. A rate lock guarantees that your interest rate won’t change between the time you apply for the loan and when you close, provided the closing occurs within a specified period (e.g., 30, 45, or 60 days). This protects you from potential market fluctuations that could cause rates to rise. Be sure to understand the terms of the rate lock, including its duration and any fees associated with extending it if your closing is delayed.

Beyond the Interest Rate: Other Costs Associated with VA Loans

While the interest rate is a primary concern, it’s important to recognize that it’s not the only cost associated with a VA loan. A comprehensive understanding of all expenses will provide a clearer picture of your overall financial commitment.

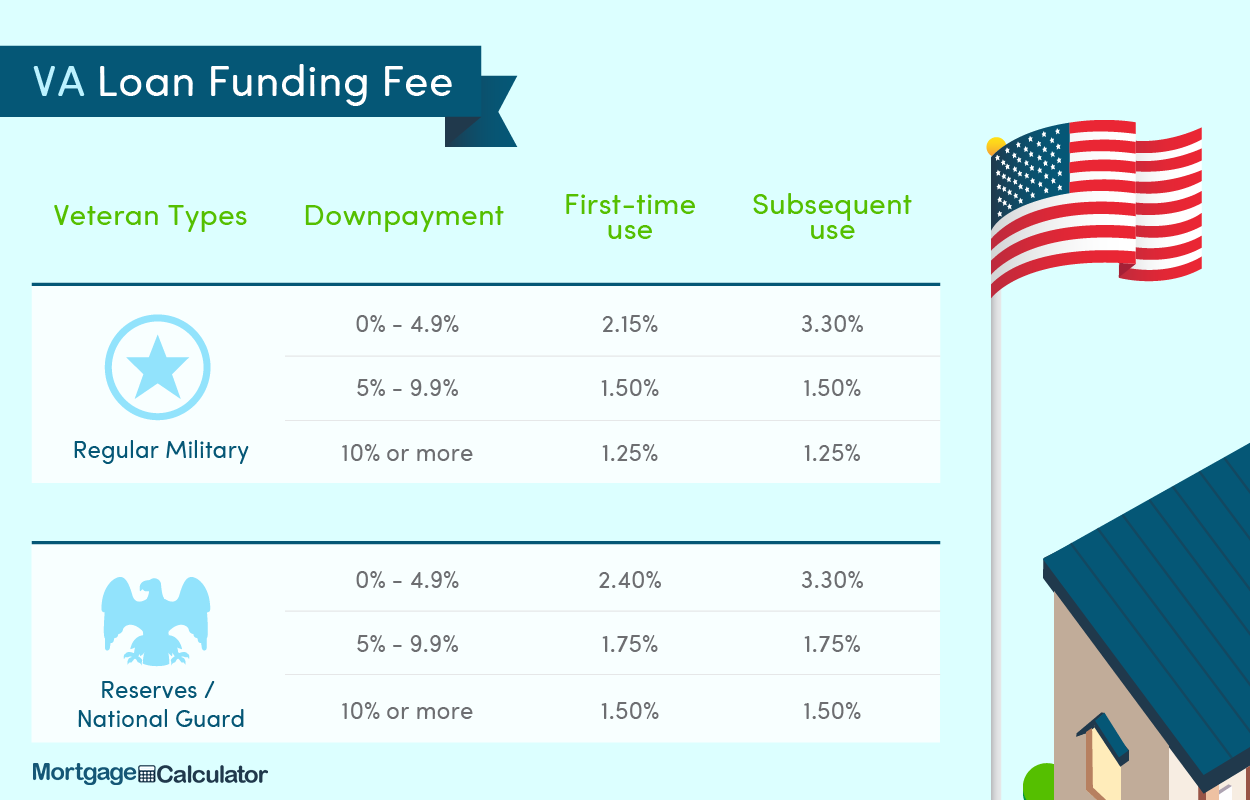

The VA Funding Fee Explained

A unique cost associated with VA loans is the VA Funding Fee. This fee is a one-time charge paid directly to the Department of Veterans Affairs. It helps to keep the VA loan program running and reduces the cost to taxpayers. The amount of the funding fee varies based on several factors, including:

- Service history: Regular military vs. Reserves/National Guard.

- Down payment amount: The more you put down, the lower the fee (though most VA loans are 0% down).

- Prior use of VA loan benefit: First-time use vs. subsequent use.

- Loan type: Purchase, refinance (IRRRL vs. cash-out).

For example, a first-time user with no down payment typically pays a funding fee of 2.15% of the loan amount. This fee can be financed into the loan, meaning you don’t have to pay it out-of-pocket at closing. Importantly, veterans receiving VA compensation for a service-connected disability, as well as certain surviving spouses, are exempt from paying the VA funding fee, providing an additional significant saving.

Closing Costs and How They Impact Your Loan

In addition to the VA funding fee, borrowers will incur other closing costs. These are fees charged by various parties involved in the home purchase transaction, such as the lender, title company, and county or state. Common closing costs include:

- Appraisal fee: For the VA-required home valuation.

- Title insurance: Protects the lender and you from title defects.

- Recording fees: For officially documenting the property transfer.

- Lender origination fee: (As discussed, usually capped at 1%).

- Survey fee: If required by the lender or state.

- Prepaid items: Such as property taxes and homeowner’s insurance premiums for a certain period.

The VA sets limits on which closing costs a veteran can pay, helping to protect borrowers from excessive fees. It’s crucial to review the Loan Estimate provided by your lender, which details all these costs, and compare it across different lenders.

Property Taxes and Homeowner’s Insurance

These are ongoing costs of homeownership, not directly part of the VA loan interest rate, but essential to factor into your monthly budget. Property taxes are assessed by local governments and are typically paid through an escrow account managed by your mortgage servicer. Homeowner’s insurance is mandatory to protect your investment against damage and liability, and its premium is also usually included in your monthly mortgage payment (PITI: Principal, Interest, Taxes, Insurance). These costs can vary significantly depending on your home’s location, value, and the insurance policy you choose, and they are important to consider when evaluating overall affordability.

Refinancing Your VA Loan: The IRRRL and Cash-Out Options

For veterans who already have a VA loan, or even those with conventional loans, refinancing can be an excellent strategy to take advantage of lower interest rates, consolidate debt, or access home equity. The VA offers two primary refinancing options tailored to different financial goals.

The Streamline Refinance (IRRRL) for Lowering Rates

The Interest Rate Reduction Refinance Loan (IRRRL), often referred to as a “VA streamline refinance,” is designed to make it easy for veterans to refinance an existing VA loan to obtain a lower interest rate, or to convert from an adjustable-rate mortgage (ARM) to a fixed-rate mortgage. The key benefits of an IRRRL include:

- Reduced Documentation: Typically requires less paperwork and underwriting compared to a full refinance.

- No Appraisal Required: In most cases, a new appraisal is not needed.

- No Credit Underwriting: Lenders often don’t require a new credit report or income verification.

- No VA Funding Fee (potentially): For those already exempt from the funding fee, this exemption carries over. Otherwise, a reduced funding fee (0.50%) applies.

The IRRRL is ideal for veterans whose primary goal is to lower their monthly payments by securing a better interest rate without drawing cash out of their equity.

Cash-Out Refinance for Leveraging Home Equity

A VA Cash-Out Refinance allows veterans to refinance their existing mortgage (VA or non-VA) for an amount greater than the outstanding balance, taking the difference in cash at closing. This option is valuable for:

- Debt Consolidation: Paying off high-interest credit card debt or other loans.

- Home Improvements: Funding renovations or repairs.

- Other Financial Needs: Covering educational expenses, medical bills, or other significant costs.

Unlike the IRRRL, a cash-out refinance typically requires an appraisal, full credit underwriting, and income verification, as it involves a new loan for a larger amount. The VA funding fee for a cash-out refinance is generally higher (e.g., 2.15% for first-time use with no down payment on the original loan, or 3.30% for subsequent use), unless the veteran is exempt due to a service-connected disability.

When Does Refinancing Make Sense?

Refinancing, whether through an IRRRL or a cash-out option, is a significant financial decision. It generally makes sense when:

- Interest rates have dropped significantly: Allowing you to secure a lower rate and reduce your monthly payments.

- Your financial situation has improved: You can qualify for better terms or a shorter loan period.

- You need to access home equity: For legitimate financial needs, and the cost of the refinance (including fees) is outweighed by the benefits.

- You want to convert an ARM to a fixed-rate: To gain payment predictability.

Always calculate the break-even point for any refinance – how long it will take for the savings from the new loan to offset the closing costs and funding fee. If you plan to move before reaching that point, refinancing may not be financially beneficial.

In conclusion, the “VA interest rate” is not a static figure but a dynamic reflection of market conditions, individual creditworthiness, and lender offerings. By understanding the intricacies of the VA loan program, diligently preparing your finances, and thoroughly shopping for the best terms, veterans can harness this incredible benefit to achieve their homeownership goals with confidence and financial prudence. The VA loan remains one of the most powerful and flexible mortgage options available, a fitting tribute to those who have served our nation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.