The question of “how low will mortgage rates go” is a perennial one, echoing through boardrooms and kitchen tables alike. For prospective homebuyers, current homeowners, and real estate investors, understanding the trajectory of mortgage rates is paramount to making informed financial decisions. The journey of mortgage rates is rarely a straight line; it’s a complex dance influenced by a myriad of economic indicators, central bank policies, and global events. While predicting the absolute bottom is a fool’s errand, we can dissect the forces at play to better anticipate potential movements and prepare for the future of home financing.

Understanding the Drivers Behind Mortgage Rate Fluctuations

Mortgage rates are not set in a vacuum. They are a reflection of broader economic conditions and expectations, influenced by several key factors that interact in intricate ways. Grasping these foundational drivers is the first step toward understanding their potential future trajectory.

The Federal Reserve and Monetary Policy

At the epicenter of interest rate movements lies the Federal Reserve (or central banks globally). The Fed doesn’t directly set mortgage rates, but its actions significantly impact the federal funds rate, which is the benchmark for short-term borrowing between banks. Changes in the federal funds rate ripple through the financial system, affecting everything from credit card rates to savings accounts. More directly, long-term fixed mortgage rates are more closely tied to the yield on 10-year Treasury bonds. When the Fed signals a more hawkish stance (raising rates to curb inflation) or a dovish one (lowering rates to stimulate growth), bond yields and, consequently, mortgage rates react. Quantitative easing (QE) – where the Fed buys bonds – can also depress yields and rates, while quantitative tightening (QT) has the opposite effect. The Fed’s dual mandate of maximum employment and stable prices (low inflation) dictates its policy decisions, making their communications a crucial barometer for rate watchers.

Inflation Expectations

Inflation is arguably the single most significant determinant of long-term interest rates. Lenders charge interest to compensate for the risk of lending money and to ensure their returns aren’t eroded by future price increases. If inflation is expected to be high, lenders demand a higher nominal interest rate to achieve a desired real (inflation-adjusted) return. Conversely, if inflation is subdued or falling, the pressure on rates to rise diminishes. This relationship is why periods of high inflation almost inevitably lead to higher mortgage rates, and a sustained fight against inflation is often a prerequisite for rates to fall significantly. The market’s perception of future inflation, often gleaned from economic data like the Consumer Price Index (CPI) and Producer Price Index (PPI), along with inflation expectations embedded in Treasury Inflation-Protected Securities (TIPS), heavily influences bond investors and therefore mortgage rates.

Economic Growth and Labor Market Health

A robust economy, characterized by strong GDP growth and a healthy labor market with low unemployment, often implies higher demand for credit and potential inflationary pressures, which can push rates up. Conversely, a weakening economy, perhaps teetering on recession, typically leads to lower demand for loans, concerns about borrower default, and usually prompts central banks to lower rates to stimulate activity. This is because in a slowdown, investors often flock to safe-haven assets like government bonds, driving down their yields and, in turn, mortgage rates. The monthly jobs report, manufacturing data, and consumer sentiment indices are all closely watched for signals about the economy’s direction and its potential impact on rates. A strong job market, in particular, can be a double-edged sword: it signals economic health but can also contribute to wage-driven inflation, making the Fed less inclined to cut rates.

Global Economic Events and Geopolitics

In an interconnected world, domestic mortgage rates are not immune to international influences. Major geopolitical events, such as wars, trade disputes, or political instability in key regions, can trigger flights to safety, pushing investors towards U.S. Treasury bonds and thus lowering yields. Conversely, global economic booms can increase demand for capital worldwide, potentially raising borrowing costs. Currency fluctuations, commodity prices (especially oil), and the economic performance of major trading partners also play a role. For instance, a global slowdown might depress demand for goods, potentially easing inflation and allowing central banks to consider lower rates. This complex web of international relationships adds another layer of unpredictability to the mortgage rate forecast.

Current Landscape and Short-Term Outlook (The “Now” and Near Future)

After a period of unprecedented volatility, mortgage rates have shown signs of stabilizing, albeit at levels significantly higher than the ultra-low rates seen during the pandemic. Understanding the present situation and what might drive rates in the immediate future is crucial for anyone contemplating a housing move.

Recent Rate Trends and Market Sentiment

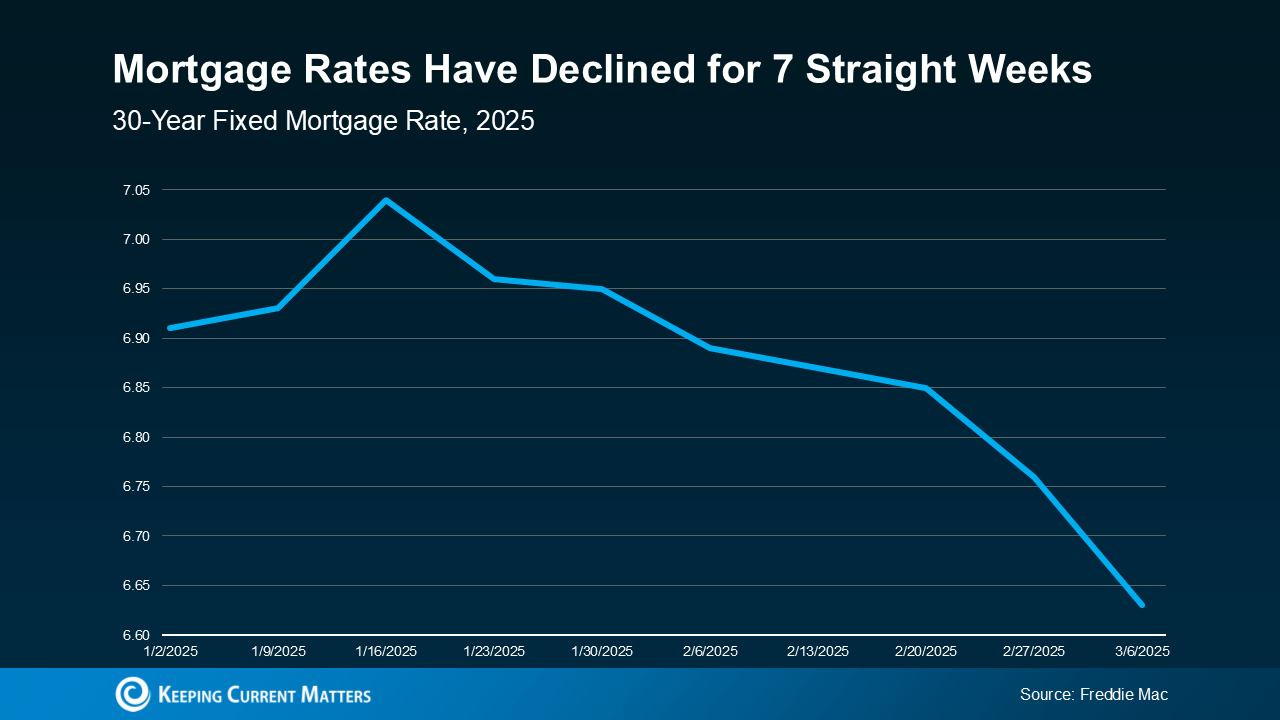

Following a dramatic ascent driven by aggressive Federal Reserve rate hikes to combat surging inflation, mortgage rates have experienced a turbulent journey. We’ve seen periods of rapid increases, followed by temporary plateaus or minor dips, only to potentially climb again based on economic data. Market sentiment is currently a tug-of-war between inflation fears and recession worries. Each piece of economic data—be it a stronger-than-expected jobs report or a higher-than-forecast inflation reading—can cause significant intraday swings in bond yields and, consequently, mortgage rates. The consensus among economists remains cautious, with many acknowledging that the era of near-zero rates is likely behind us for the foreseeable future, but also recognizing the potential for rates to ease from their peaks.

Factors Supporting Potential Decreases

Several scenarios could pave the way for mortgage rates to come down in the short term. The most significant factor would be sustained evidence of decelerating inflation. If the Consumer Price Index and other inflation gauges consistently show a downward trend towards the Fed’s 2% target, it would reduce the pressure on the Fed to maintain high interest rates. This could lead the central bank to pause or even begin cutting the federal funds rate, which would then allow bond yields and mortgage rates to follow suit. A softening labor market could also contribute; if unemployment rises modestly and wage growth cools, it signals less inflationary pressure from the demand side. Furthermore, an economic slowdown or mild recession could trigger a flight to safety among investors, increasing demand for U.S. Treasury bonds and lowering their yields, thereby pulling mortgage rates down. Any unexpected geopolitical de-escalation could also lead to a more stable economic outlook, potentially reducing risk premiums in bond markets.

Factors Limiting Significant Decreases

Despite the potential for rates to fall, several powerful forces could limit any substantial decline, keeping them elevated compared to pre-2022 levels. Persistent inflation, particularly in sticky components like services or housing, would prevent the Fed from easing its monetary policy. If inflation proves more entrenched than anticipated, the Fed might even have to consider further rate hikes, pushing mortgage rates higher. A resilient economy and strong job market could also work against lower rates. If economic growth continues robustly, and unemployment remains historically low, the Fed would have little incentive to cut rates, fearing it could reignite inflation. Government debt and fiscal policy also play a role; large deficits and increased borrowing by the government can put upward pressure on Treasury yields. Finally, a shift in the underlying structural supply/demand dynamics for bonds could mean that the market itself demands a higher baseline yield for long-term debt, regardless of short-term Fed actions. This “term premium” could keep rates from returning to their historical lows.

Analyst Predictions and Consensus

Predicting the future is always challenging, but current analyst predictions generally suggest a modest easing of mortgage rates rather than a dramatic crash to previous lows. Many financial institutions and economic forecasting agencies project rates to remain somewhat elevated throughout the next year, perhaps fluctuating within a certain range (e.g., 6-7% for a 30-year fixed). There’s a common expectation that if the Fed successfully manages to bring inflation under control without triggering a severe recession, we might see rates gradually decline. However, the exact timing and magnitude of such declines are subject to ongoing economic data and central bank policy shifts. Consensus points to a period of adjustment where markets are still trying to find a “new normal” for borrowing costs.

Long-Term Projections and Structural Shifts (Beyond the Immediate Horizon)

Looking beyond the immediate horizon, several long-term trends and structural shifts in the economy and housing market could influence where mortgage rates eventually settle. Understanding these broader forces is key to making strategic financial plans over many years.

The “New Normal” for Interest Rates

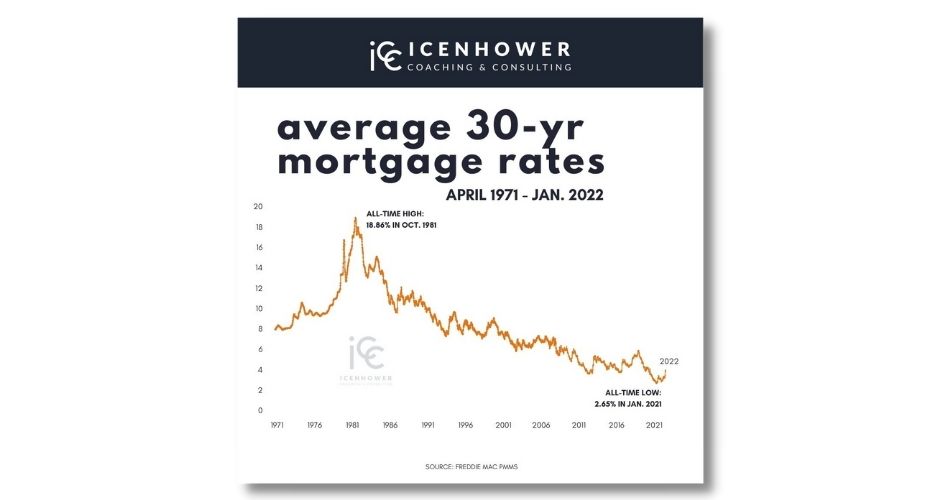

One of the most profound questions facing economists and homeowners alike is whether the era of ultra-low interest rates (0-3% for 30-year fixed mortgages) was an anomaly, or if a return to such levels is plausible. Many argue that the decade following the 2008 financial crisis, characterized by quantitative easing and near-zero policy rates, was an extraordinary period driven by unique economic circumstances. The consensus is shifting towards a belief that the “new normal” for interest rates will likely be higher than the pre-pandemic decade. Factors like higher structural inflation, increased government debt levels globally, and a potential recalibration of risk premiums could mean that baseline rates will sit closer to historical averages (e.g., 4-6%) rather than the extreme lows witnessed previously. This higher equilibrium would necessitate a recalibration of investment and real estate strategies.

Demographic Trends and Housing Demand

Demographic shifts are slow-moving but powerful forces in the housing market. An aging population, particularly in developed economies, can influence demand as older generations downsize or pass on their properties. Conversely, a growing young adult population (like millennials and Gen Z) entering their prime homebuying years can create sustained demand, regardless of rate fluctuations. Migration patterns, both international and internal, also affect regional housing markets. If the supply of housing doesn’t keep pace with demographic-driven demand, house prices can continue to rise, potentially making homeownership more challenging and impacting affordability, which indirectly influences the tolerance for higher mortgage rates. The desire for homeownership remains strong, and this persistent demand provides a floor under the housing market, even as rates fluctuate.

Technological Advancements in Lending

The financial technology (FinTech) revolution is steadily transforming the mortgage industry. AI-driven underwriting, digital mortgage applications, and blockchain-based property records are making the lending process more efficient, faster, and potentially less costly. Automation can reduce operational overhead for lenders, which, in theory, could translate into slightly lower rates or more competitive offerings for consumers over time. Predictive analytics can also improve risk assessment, potentially allowing for more tailored and competitive loan products. While technology isn’t likely to single-handedly drive rates down by percentage points, it could contribute to a more streamlined and transparent lending environment, offering marginal benefits to borrowers and fostering greater competition among lenders.

Government Policies and Housing Initiatives

Future government policies could significantly impact mortgage rates and the housing market. Initiatives aimed at increasing housing supply, such as zoning reform or incentives for new construction, could ease price pressures and improve affordability. Programs designed to support first-time homebuyers, such as down payment assistance or specific loan products, could stimulate demand. Conversely, new regulations on lending or financial institutions could affect their cost of doing business, which might be passed on to consumers. Large-scale fiscal policies, particularly those related to infrastructure spending or national debt management, could also influence overall bond yields and, by extension, mortgage rates. The political landscape and policy priorities will therefore continue to be an important, albeit unpredictable, long-term factor.

Strategies for Homebuyers and Homeowners in a Dynamic Rate Environment

Given the dynamic and often unpredictable nature of mortgage rates, adopting a proactive and adaptable financial strategy is crucial for both prospective buyers and existing homeowners. Focusing on personal financial health and leveraging expert advice can help navigate the complexities.

For Prospective Buyers: Timing the Market vs. Readiness

The adage “time in the market beats timing the market” often applies to real estate, too. While it’s tempting to wait for rates to hit an absolute low, this can lead to missed opportunities, especially if home prices continue to appreciate. Instead, focus on financial readiness: building a strong credit score, saving a substantial down payment, and having a stable income. Understand your personal budget and what you can comfortably afford, irrespective of daily rate fluctuations. Get pre-approved to understand your borrowing power. If rates are high but you are ready to buy, consider an Adjustable-Rate Mortgage (ARM) if you plan to move or refinance within a few years, but always understand the risks involved. Don’t let the pursuit of a hypothetical “perfect” rate overshadow the opportunity to secure a home when your personal finances align.

For Current Homeowners: Refinancing Opportunities

Existing homeowners, particularly those with higher mortgage rates, should remain vigilant for refinancing opportunities. A refinance makes sense when the interest rate drop is significant enough to offset closing costs within a reasonable timeframe (the “break-even point”). Keep an eye on market trends; even a half-percentage point drop can translate into substantial savings over the life of a loan. Besides a traditional refinance, consider alternatives like a Home Equity Line of Credit (HELOC) or a cash-out refinance for major expenses, but always weigh the long-term implications of leveraging your home equity. Regularly reviewing your mortgage terms and comparing them with current market offerings, even if just annually, is a prudent financial habit.

The Importance of Financial Health

Regardless of whether rates are going up or down, your personal financial health is your most powerful tool. A strong credit score (typically 760+) will unlock the best available rates, as lenders view you as a lower risk. Managing debt effectively, especially high-interest consumer debt, not only improves your debt-to-income ratio but also frees up capital for down payments or emergency savings. Building a robust emergency fund ensures you can weather unexpected financial storms without jeopardizing your homeownership. These foundational financial habits are more critical than trying to perfectly time the market; they provide a buffer against rate volatility and enhance your overall financial security.

Working with Financial Professionals

Navigating the mortgage market can be complex, and expert guidance is invaluable. Mortgage brokers can compare offers from multiple lenders, potentially finding you a better rate or more favorable terms than you might find on your own. Financial advisors can help you assess your overall financial picture, determine how a mortgage fits into your long-term goals, and advise on risk management. These professionals stay abreast of market trends, policy changes, and new financial products, offering tailored advice that can save you time, money, and stress. Don’t hesitate to seek out their expertise, especially when making one of the largest financial decisions of your life.

Conclusion: Preparing for What’s Next

The question “how low will mortgage rates go?” remains a subject of intense speculation and economic debate. While a definitive answer eludes even the most seasoned experts, the consensus points to a future where ultra-low rates may be a relic of the past, replaced by a more historically typical, yet still dynamic, rate environment. The interplay of inflation, central bank policy, economic growth, and global events will continue to shape their trajectory.

For consumers, the most effective strategy isn’t to chase an elusive bottom, but to focus on financial preparedness and informed decision-making. By understanding the underlying drivers, monitoring economic indicators, and leveraging professional advice, individuals can position themselves to make sound choices, whether they are buying their first home, refinancing an existing one, or simply planning for their financial future in a world where the cost of borrowing money has found a new equilibrium. The journey of mortgage rates is continuous; preparedness and adaptability will be your greatest allies.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.