The question “how much is the interest rate?” is far more complex than a simple numerical answer. Interest rates are the lifeblood of our financial system, a dynamic force that dictates the cost of borrowing and the reward for saving, influencing everything from the price of your mortgage to the performance of global economies. They are not static figures but rather ever-changing metrics shaped by a confluence of economic policies, market forces, and global events. Understanding interest rates—what they are, how they are determined, and their pervasive impact—is fundamental to making informed financial decisions, whether you’re an individual saving for retirement, a small business seeking expansion capital, or an investor navigating the markets. This exploration will delve into the intricacies of interest rates, demystifying their calculation, highlighting the factors that drive their fluctuations, and examining their profound implications for both personal finance and the broader economy.

Understanding the Fundamentals of Interest Rates

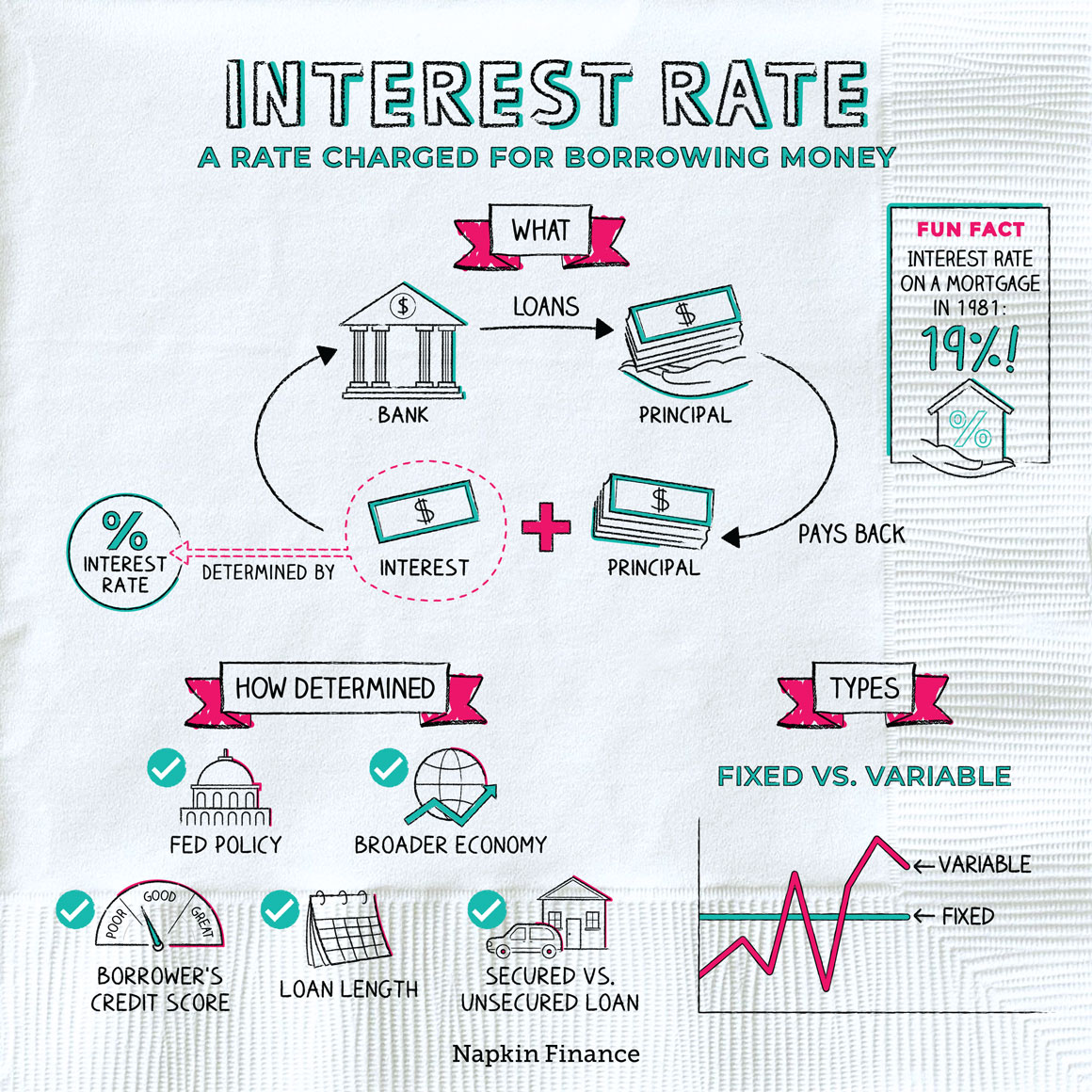

At its core, an interest rate is the cost of borrowing money or the return on lending it. It represents the percentage of the principal (the initial amount borrowed or saved) that is paid by the borrower to the lender over a specific period. This seemingly simple concept underpins nearly every financial transaction in the modern world.

What Exactly is an Interest Rate?

An interest rate is essentially a fee. When you borrow money, whether for a car, a house, or through a credit card, the lender charges you interest as compensation for the risk they take and for the opportunity cost of not using that money elsewhere. Conversely, when you deposit money into a savings account or invest in a bond, the financial institution or issuer pays you interest for the privilege of using your funds. This rate is typically expressed as an annual percentage rate (APR) for loans or annual percentage yield (APY) for savings, which factors in compounding. The numerical value itself is a reflection of many underlying economic conditions and policies, making it a crucial barometer of economic health.

The Dual Nature of Interest: Borrowing vs. Saving

The dual nature of interest rates means they have a profound impact on both sides of the financial spectrum. For borrowers, a higher interest rate translates to higher monthly payments and a greater overall cost of debt, which can dampen consumer spending and business investment. Conversely, lower interest rates make borrowing cheaper, stimulating economic activity. For savers and investors, higher interest rates mean greater returns on deposits and fixed-income investments, encouraging saving. Lower rates, however, can erode the purchasing power of savings over time, pushing individuals towards riskier assets in search of better yields. Recognizing this dichotomy is key to understanding how interest rate shifts ripple through the economy, influencing decisions at every level from individual households to multinational corporations.

Key Components of an Interest Rate

The advertised interest rate isn’t just a random number; it’s a composite of several critical components. The primary component is the risk-free rate, which is the theoretical return on an investment with zero risk, often benchmarked against short-term government securities. To this, a risk premium is added, compensating the lender for the specific risk of the borrower defaulting. This premium varies based on the borrower’s creditworthiness, the type of loan, and market conditions. Another crucial factor is the inflation premium, which accounts for the expected erosion of purchasing power over the life of the loan due to inflation. Lenders need to ensure the real return on their money is preserved. Finally, a liquidity premium may be included, reflecting the ease with which the lender can convert the loan back into cash if needed. Together, these components determine the precise “how much” behind any given interest rate.

The Forces That Shape Interest Rates

Interest rates are not set in a vacuum. They are dynamic figures, constantly adjusting in response to a complex interplay of macroeconomic policies, market dynamics, and global events. Understanding these influential forces is crucial to anticipating changes and their potential impact.

Central Banks and Monetary Policy

The most significant driver of interest rates in most developed economies is the central bank, such such as the U.S. Federal Reserve, the European Central Bank, or the Bank of England. Central banks use monetary policy tools to manage inflation, maximize employment, and maintain financial stability. Their primary tool for influencing interest rates is the benchmark interest rate (e.g., the Federal Funds Rate in the U.S.). When a central bank raises its benchmark rate, it typically makes borrowing more expensive for commercial banks, which then pass on these higher costs to consumers and businesses. Conversely, lowering the benchmark rate aims to stimulate borrowing and economic growth. Open market operations, quantitative easing, and reserve requirements are other tools employed by central banks to inject or withdraw liquidity from the financial system, indirectly affecting interest rates. Their decisions are closely watched by markets worldwide, as they can signal a shift in economic conditions or future policy direction.

Inflation and Economic Growth

Inflation and economic growth are two powerful economic indicators that heavily influence interest rates. When inflation is high or expected to rise, central banks often increase interest rates to cool down the economy and curb rising prices. This is because higher interest rates make borrowing more expensive, reducing demand and slowing economic activity. Lenders also demand higher interest rates during inflationary periods to ensure the real value of their money is preserved. Conversely, in periods of low inflation or deflation, central banks may lower rates to encourage spending and investment. Economic growth also plays a role: during robust economic expansion, demand for credit increases as businesses invest and consumers spend, which can push interest rates higher. During recessions or slow growth periods, demand for credit typically falls, and central banks might lower rates to stimulate activity. The interplay between these two factors is a delicate balancing act for policymakers.

Market Demand, Supply, and Risk

Beyond central bank actions, the fundamental principles of supply and demand significantly impact interest rates. If there is a high demand for borrowed money (e.g., many businesses want to expand, or consumers are taking out more loans) and a limited supply of available funds, interest rates will tend to rise. Conversely, if there’s an abundance of money available for lending but low demand, rates will fall. Furthermore, the perceived risk associated with a borrower or the overall economic environment plays a critical role. Loans to financially stable governments or highly-rated corporations carry lower interest rates due to lower default risk. Loans to individuals with poor credit or to businesses in volatile industries will command higher interest rates to compensate lenders for the increased risk of non-repayment. Market sentiment, investor confidence, and geopolitical stability can all feed into this risk assessment, causing interest rates to fluctuate.

Geopolitical Factors and Global Economic Trends

Interest rates are not solely determined by domestic factors; geopolitical factors and global economic trends increasingly exert their influence. Major international events, such as trade wars, political instability in key regions, or global health crises, can create uncertainty, leading investors to seek safe-haven assets, which can suppress bond yields and interest rates in stable economies. Conversely, if a country’s economic or political stability is perceived to be deteriorating, investors might demand higher interest rates to lend money to that country. Global supply chain disruptions, energy price shocks, and the economic performance of major trading partners can also impact a nation’s inflation outlook and growth prospects, thereby influencing its central bank’s interest rate decisions. In an interconnected world, national interest rates are increasingly sensitive to the ebbs and flows of the international financial landscape.

Interest Rates’ Impact on Your Personal Finances

The abstract concept of an interest rate becomes intensely personal when it translates into the cost of your home, the burden of your debt, or the growth of your savings. Understanding this direct impact is crucial for effective personal financial planning.

Mortgages and Homeownership

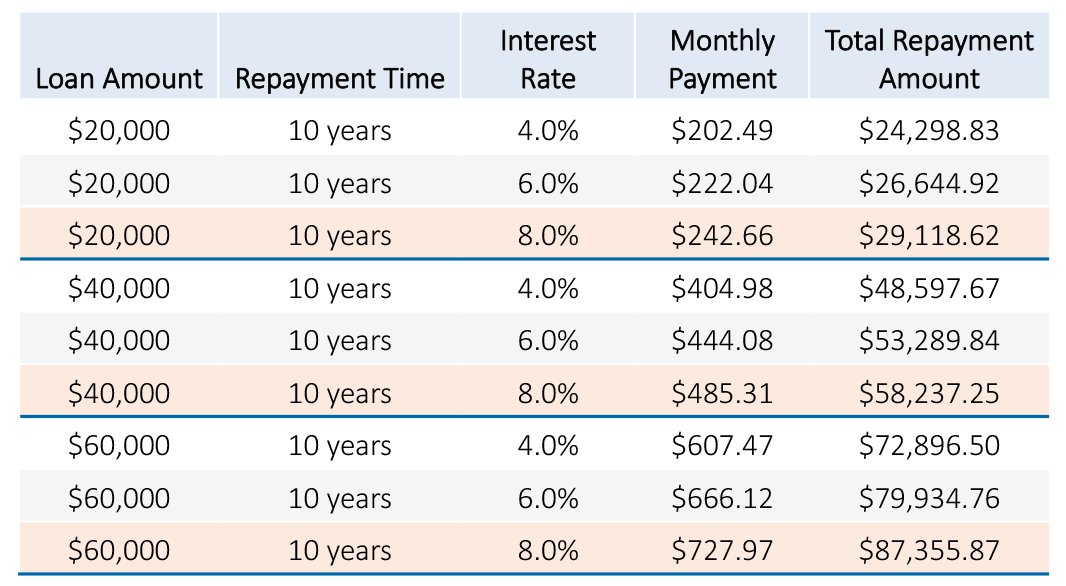

For most individuals, the most significant financial impact of interest rates is felt through mortgages. A small shift in mortgage interest rates can mean thousands of dollars difference over the lifespan of a 15-year or 30-year loan. When interest rates are low, homeownership becomes more affordable, spurring demand and often driving up housing prices. Conversely, rising rates can cool down a hot housing market, making monthly payments higher and potentially pricing some prospective buyers out of the market. Homeowners with adjustable-rate mortgages (ARMs) are particularly vulnerable to rate fluctuations, as their monthly payments can change, sometimes dramatically, with market shifts. Even fixed-rate mortgage holders can be affected, as rising rates might prevent them from refinancing to a lower rate in the future.

Credit Cards and Consumer Loans

Credit card interest rates are typically among the highest, often ranging from 15% to 25% APR or more. These rates are usually variable, meaning they can change based on the prime rate, which is directly influenced by the central bank’s benchmark rate. When the prime rate goes up, your credit card interest rate usually follows, making carrying a balance more expensive. Similarly, auto loans, personal loans, and other consumer financing are directly affected by the broader interest rate environment. Lower rates make it cheaper to finance a new car or consolidate debt, while higher rates can significantly increase the cost of these loans, impacting household budgets and consumer spending decisions. Prudent management of high-interest debt becomes even more critical during periods of rising rates.

Savings Accounts and Investments

On the flip side, interest rates also determine the return on your savings accounts, certificates of deposit (CDs), and fixed-income investments like bonds. When interest rates are low, the returns on these safe-haven instruments are modest, offering little incentive to save in traditional accounts and potentially pushing investors towards riskier assets for higher yields. As rates rise, however, savings accounts and CDs become more attractive, offering a better return on your idle cash. Bond prices typically move inversely to interest rates: when rates rise, new bonds are issued with higher yields, making existing lower-yield bonds less attractive, thus decreasing their market value. Understanding this relationship is vital for building a balanced investment portfolio that aligns with your financial goals and risk tolerance.

Student Loans and Debt Management

Student loans represent another significant area where interest rates have a substantial impact. While federal student loan rates are fixed and set by Congress annually, private student loan rates can be variable and directly tied to market rates. Rising interest rates can make private student loans more expensive, increasing monthly payments and the total cost of education. For individuals managing multiple debts, including student loans, credit cards, and personal loans, changes in interest rates can dramatically alter the effectiveness of their debt management strategies. For instance, a low-interest environment might be ideal for consolidating high-interest debt, while a rising rate environment could make such consolidation less attractive or even counterproductive if the new rate is not fixed. Strategic planning around interest rate cycles is key to minimizing debt burdens.

The Broader Economic Ramifications of Interest Rates

Beyond individual finances, interest rates act as a crucial lever in the broader economic machinery, influencing everything from national growth to international trade. Their ebb and flow can dictate the pace and direction of an economy.

Business Investment and Expansion

Interest rates play a pivotal role in business investment and expansion. Companies, regardless of size, often rely on borrowed capital to fund new projects, purchase equipment, hire staff, or expand their operations. When interest rates are low, the cost of borrowing decreases, making it more attractive for businesses to take on debt, invest in their future, and stimulate job creation. This can lead to increased productivity and economic growth. Conversely, high interest rates increase the cost of capital, making businesses more hesitant to borrow and invest, which can slow down expansion, lead to reduced hiring, and potentially curb overall economic activity. Start-ups and small businesses, often more sensitive to financing costs, are particularly impacted by these fluctuations.

Inflation Control and Economic Stability

One of the primary objectives of central banks in managing interest rates is inflation control and maintaining economic stability. As discussed, when inflation is rampant and the economy is overheating, central banks typically raise interest rates. This makes borrowing more expensive, dampens consumer and business spending, and aims to reduce overall demand in the economy, thereby bringing inflation back down to target levels. Conversely, during periods of economic slowdown or recession, central banks lower interest rates to stimulate borrowing, investment, and consumer spending, aiming to inject liquidity into the economy and avert deflation or prolonged stagnation. The art of monetary policy lies in finding the “just right” interest rate that fosters growth without triggering runaway inflation or deflation.

Currency Valuation and International Trade

Interest rates also have a significant impact on currency valuation and international trade. When a country’s central bank raises interest rates, it generally makes that country’s currency more attractive to foreign investors. Higher interest rates offer better returns on bonds and other interest-bearing assets denominated in that currency, increasing demand for it. This increased demand leads to an appreciation of the currency’s value. A stronger currency makes imports cheaper and exports more expensive, which can affect a country’s trade balance. Conversely, lower interest rates can lead to currency depreciation, making exports more competitive but imports more costly. These currency fluctuations can have profound effects on international trade flows, corporate profits for multinational companies, and the cost of foreign goods and services for consumers.

Navigating the Interest Rate Landscape

Understanding “how much is the interest rate” is not just about knowing the current number, but also about appreciating its implications and strategically planning your financial moves. Navigating this dynamic landscape requires ongoing vigilance and proactive decision-making.

Staying Informed and Planning Ahead

The first step to effectively managing interest rate changes is to stay informed about economic news, central bank announcements, and market forecasts. Major financial news outlets and reputable economic publications regularly report on these developments, providing insights into potential future rate movements. By understanding the underlying economic indicators that influence interest rates—such as inflation data, employment figures, and GDP growth—you can better anticipate shifts. This knowledge allows you to plan ahead for significant financial decisions. For example, if interest rates are expected to rise, you might consider locking in a fixed-rate mortgage or consolidating variable-rate debt sooner rather than later. If rates are anticipated to fall, it might be an opportune time to consider refinancing existing loans.

Optimizing Your Borrowing Strategies

Optimizing your borrowing strategies means making smart choices about when and how you take on debt. In a low-interest-rate environment, it might be advantageous to take out a fixed-rate loan for a major purchase like a home or a car, securing a lower payment for the life of the loan. Conversely, if you have variable-rate debt, consider refinancing to a fixed rate when rates are favorable to protect yourself from future increases. Regularly review your existing loans and credit cards to ensure you’re getting the best possible rates. Paying down high-interest debt, especially credit card balances, becomes even more critical when rates are rising, as the cost of carrying that debt increases significantly. Utilize tools like debt consolidation or balance transfers strategically to reduce your overall interest burden.

Maximizing Your Savings and Investments

Just as you optimize borrowing, you should also maximize your savings and investments in response to interest rate changes. In a rising rate environment, traditional savings accounts, CDs, and money market accounts become more attractive, offering better returns on your cash. This is a good time to reconsider moving funds from low-yielding checking accounts into higher-yield savings products. For investors, rising rates can make fixed-income investments like bonds less appealing in the short term, as existing lower-yield bonds lose value. However, new bonds issued will offer higher yields. Conversely, when rates are low, the returns on safe assets are minimal, which might necessitate exploring other investment avenues, potentially with higher risk, to achieve your financial goals. Diversifying your portfolio and adjusting your asset allocation based on the prevailing interest rate environment is a crucial aspect of long-term wealth building.

In conclusion, the question “how much is the interest rate?” is a gateway to understanding the intricate mechanisms that govern our financial lives. Interest rates are dynamic, multi-faceted economic tools that directly impact personal budgets, business decisions, and the health of the global economy. By grasping their fundamentals, recognizing the forces that shape them, and actively adapting your financial strategies, you can navigate the ever-shifting interest rate landscape with greater confidence and make more informed decisions to achieve your financial aspirations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.