Navigating the landscape of homeownership often begins with understanding the financial instruments available, and among the most prominent for many prospective buyers are FHA loans. While the appeal of these government-insured mortgages is clear—offering more lenient qualification standards, particularly for those with less-than-perfect credit or smaller down payments—a crucial question consistently arises: “What is the current FHA interest rate?” This isn’t a straightforward answer you’ll find on a single government website; rather, it’s a dynamic figure shaped by a confluence of market forces, individual borrower profiles, and lender policies. Understanding these intricacies is paramount for anyone considering this path to homeownership.

Understanding FHA Loans: A Foundation for Homeownership

The Federal Housing Administration (FHA), a part of the U.S. Department of Housing and Urban Development (HUD), does not lend money directly. Instead, it insures loans made by FHA-approved lenders. This insurance protects lenders from losses if a borrower defaults, which in turn encourages them to offer more favorable terms to a broader spectrum of homebuyers, including those who might not qualify for conventional financing.

The Purpose and Benefits of FHA Loans

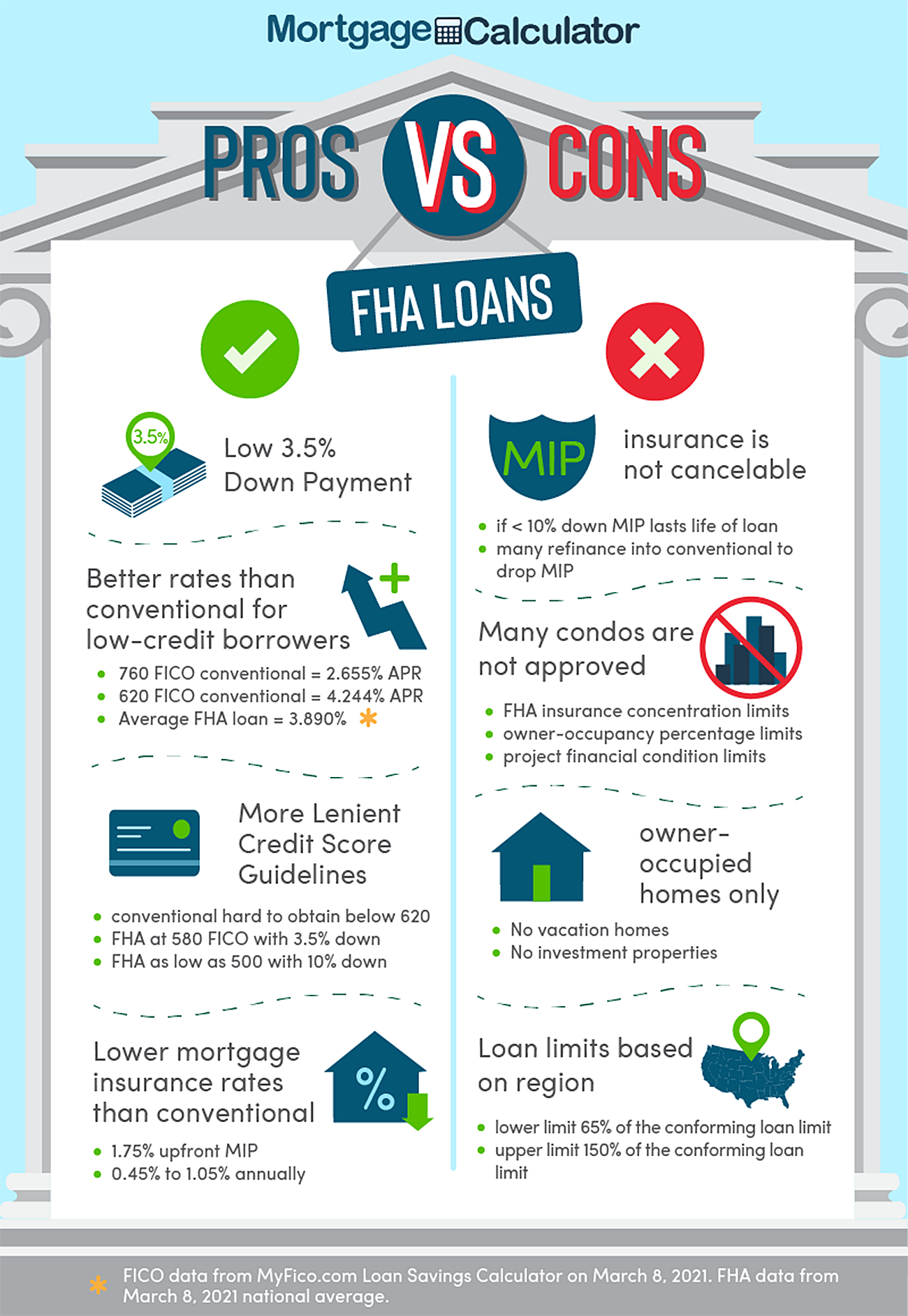

FHA loans were established during the Great Depression to stimulate the housing market and make homeownership more accessible. This core mission remains unchanged today. Their primary benefit lies in their inclusivity. Borrowers with credit scores as low as 580 can qualify for the maximum financing (3.5% down payment), and even those with scores between 500-579 might qualify with a 10% down payment. This flexibility contrasts sharply with conventional loan standards, which typically demand higher credit scores and larger down payments (often 5% to 20%).

Beyond credit and down payment flexibility, FHA loans offer competitive interest rates because of the government backing. They also allow for higher debt-to-income (DTI) ratios than many conventional loans, providing more leeway for those carrying existing debt. Furthermore, FHA loans are assumable, meaning a qualified buyer can take over an existing FHA mortgage, potentially saving on closing costs and securing a lower rate if market conditions have changed. They are particularly popular among first-time homebuyers who may not have accumulated substantial savings or established a lengthy credit history.

Key Requirements for FHA Eligibility

While FHA loans are known for their leniency, they are not without specific criteria. Eligibility hinges on several factors:

- Credit Score: As mentioned, a minimum FICO score of 580 typically qualifies for the 3.5% down payment. Scores between 500-579 may require a 10% down payment.

- Down Payment: A minimum of 3.5% of the purchase price is required for borrowers with a credit score of 580 or higher. This down payment can come from savings, a gift from a family member, or a grant from an approved down payment assistance program.

- Debt-to-Income (DTI) Ratio: The FHA generally looks for a front-end DTI (housing expenses as a percentage of gross income) of no more than 31% and a back-end DTI (all monthly debts, including housing, as a percentage of gross income) of no more than 43%. However, exceptions can be made for higher ratios if other compensating factors, such as significant cash reserves or a history of saving, are present.

- Property Requirements: The property must meet FHA appraisal standards to ensure it is safe, sound, and secure. This typically involves an FHA-approved appraiser verifying the property’s condition, focusing on structural integrity and compliance with minimum property standards.

- Occupancy: The borrower must intend to occupy the property as their primary residence. FHA loans are not typically for investment properties or second homes.

- Mortgage Insurance: All FHA loans require two types of mortgage insurance premiums (MIP): an upfront mortgage insurance premium (UFMIP) and an annual mortgage insurance premium (MIP). These are discussed in more detail later.

Meeting these requirements sets the stage for a borrower to qualify for an FHA loan, but understanding the interest rate itself is the next critical step.

Navigating the Dynamics of FHA Interest Rates

The “current FHA interest rate” is a moving target, constantly influenced by a complex interplay of macroeconomic factors and individual borrower characteristics. It’s a common misconception that the FHA dictates a specific interest rate; in reality, they set the guidelines, but the rates themselves are competitive and determined by the individual lenders.

How FHA Interest Rates Are Determined

FHA interest rates are not static. They fluctuate daily, sometimes hourly, driven by several key factors:

- Broader Market Conditions: The primary driver of all mortgage rates, including FHA, is the overall bond market, specifically the yield on mortgage-backed securities (MBS). When MBS yields rise, mortgage rates generally follow suit. These yields are, in turn, influenced by factors like inflation expectations, the Federal Reserve’s monetary policy decisions (e.g., adjustments to the federal funds rate), and global economic stability. During periods of economic growth and low inflation, rates tend to be lower, while inflationary pressures or uncertainty can push them higher.

- Lender-Specific Factors: Each FHA-approved lender sets its own rates based on its operational costs, profit margins, and risk assessment. This is why shopping around among different lenders is crucial, as rates for the same FHA loan can vary significantly from one institution to another. Lenders also offer different “rate sheets” throughout the day, adjusting based on current market activity.

- Borrower-Specific Factors: While FHA loans are forgiving, an individual’s financial profile still plays a role in the rate they receive. A higher credit score, a lower debt-to-income ratio, and a larger down payment (even if not strictly required by FHA) can signal less risk to a lender, potentially allowing them to offer a more favorable interest rate. The loan-to-value (LTV) ratio also impacts the annual mortgage insurance premium (MIP), which affects the overall cost of the loan.

- Points: Borrowers often have the option to pay “points” (prepaid interest) at closing to secure a lower interest rate for the life of the loan. Each point typically costs 1% of the loan amount. Deciding whether to pay points depends on how long the borrower plans to stay in the home and their available cash for closing.

Fixed-Rate vs. Adjustable-Rate FHA Loans

FHA loans, like conventional mortgages, come in two primary interest rate structures:

- Fixed-Rate FHA Loans: The vast majority of FHA loans are fixed-rate, most commonly for 30-year terms, though 15-year options are also available. With a fixed-rate loan, the interest rate remains constant for the entire duration of the loan. This provides stability and predictability, as your monthly principal and interest payment will never change. This predictability is highly valued by homeowners who prefer consistent budgeting and want to avoid the uncertainty of market fluctuations. For instance, if you secure a 30-year fixed FHA loan at 6%, your principal and interest payment will be calculated based on that 6% for all 360 payments.

- Adjustable-Rate FHA Mortgages (ARMs): FHA also offers ARMs, typically designated as 5/1 ARMs (the interest rate is fixed for the first five years and then adjusts annually), 7/1 ARMs, or 10/1 ARMs. With an ARM, the initial interest rate is often lower than a comparable fixed-rate loan, making the initial monthly payments more affordable. However, after the initial fixed period, the rate adjusts periodically based on a predetermined index (like the Secured Overnight Financing Rate – SOFR) plus a margin set by the lender. These adjustments can cause your monthly payments to increase or decrease, depending on market conditions. ARMs usually have caps on how much the interest rate can increase or decrease per adjustment period and over the life of the loan, offering some protection against extreme volatility. ARMs are often considered by borrowers who plan to sell or refinance before the fixed period ends or who are comfortable with potential payment fluctuations.

Beyond the Interest Rate: Other Costs of FHA Loans

While the nominal interest rate is a critical component of a mortgage, it doesn’t tell the whole story, especially with FHA loans. There are other mandatory costs that significantly impact the total expense of borrowing. Understanding these additional fees is essential for a comprehensive financial picture.

Mandatory Mortgage Insurance Premiums (MIP)

A distinguishing feature of FHA loans is the requirement for mortgage insurance, which protects the lender against loss if the borrower defaults. FHA loans have two types of MIP:

- Upfront Mortgage Insurance Premium (UFMIP): This is a one-time payment made at closing, equal to 1.75% of the loan amount. For example, on a $300,000 loan, the UFMIP would be $5,250. While due at closing, most borrowers finance the UFMIP into their loan, increasing the loan balance slightly but reducing out-of-pocket costs at closing. This amount is financed even if you are paying cash for other closing costs.

- Annual Mortgage Insurance Premium (MIP): This is an ongoing premium paid monthly, included in your mortgage payment. The exact percentage varies based on the loan-to-value (LTV) ratio, loan term, and loan amount. For most FHA loans with a 3.5% down payment and a 30-year term, the annual MIP is 0.55% of the outstanding loan balance for loans endorsed on or after January 26, 2015. Unlike conventional private mortgage insurance (PMI), which can typically be canceled once you reach 20% equity, FHA’s annual MIP generally remains for the life of the loan if your original LTV was above 90% (i.e., less than 10% down payment). If you put down 10% or more, the MIP will be removed after 11 years. This extended duration of MIP is a crucial factor to consider when comparing FHA with conventional loans.

Closing Costs and Fees

In addition to MIP, borrowers will incur standard closing costs, which typically range from 2% to 5% of the loan amount. These fees cover various services and expenses associated with originating and closing the loan:

- Lender Fees: These include origination fees, application fees, underwriting fees, and potentially discount points (if purchased to lower the interest rate).

- Third-Party Fees: This category encompasses charges for services provided by external vendors, such as:

- Appraisal Fee: For the FHA-approved appraiser to assess the property’s value and ensure it meets FHA standards.

- Credit Report Fee: To pull the borrower’s credit report.

- Title Insurance: Protects the lender and the homeowner against claims against the property’s title.

- Escrow and Closing Fees: Charged by the escrow or title company for facilitating the closing process.

- Recording Fees: To officially record the deed and mortgage with the local government.

- Attorney Fees: If an attorney is involved in the closing process (required in some states).

- Prepaid Items: These are expenses that are paid in advance, such as property taxes, homeowner’s insurance premiums, and per-diem interest (interest from the closing date to the end of the month).

Some of these closing costs can be paid by the seller, the lender (through a lender credit, often in exchange for a slightly higher interest rate), or rolled into the loan amount (though FHA limits how much can be financed).

The Total Cost of an FHA Loan: A Holistic View

When evaluating an FHA loan, it’s essential to look beyond just the nominal interest rate and consider the Annual Percentage Rate (APR). The APR reflects the true annual cost of the loan by incorporating not only the interest rate but also most of the lender fees, UFMIP, and other prepaid finance charges. It provides a more accurate apples-to-apples comparison between different loan offers.

Furthermore, consider the total amount paid over the life of the loan. Even a seemingly small difference in the interest rate can amount to tens of thousands of dollars over 30 years. The added burden of annual MIP, especially for the life of the loan, means that the effective cost of an FHA loan can sometimes exceed a conventional loan, even if the nominal interest rate is lower. It’s crucial to use a mortgage calculator that accounts for both the interest rate and the mortgage insurance premiums to get a clear picture of your monthly payments and overall financial commitment.

Strategies for Securing the Best FHA Interest Rate

While external market forces dictate the general direction of interest rates, prospective FHA borrowers are not powerless. Several proactive strategies can significantly improve your chances of securing a more favorable FHA interest rate and minimize the overall cost of your loan.

Improving Your Financial Profile

Lenders assess risk, and a stronger financial profile translates into lower perceived risk, often leading to better rates.

- Boosting Credit Scores: Even within FHA guidelines, a higher credit score (e.g., 680 vs. 580) can differentiate you and qualify you for the lowest rates available from a lender. Focus on paying bills on time, reducing credit card balances, and avoiding new credit inquiries in the months leading up to your loan application.

- Reducing Debt: A lower debt-to-income (DTI) ratio signals to lenders that you have more disposable income to manage your mortgage payments. Prioritize paying down high-interest debts like credit cards or personal loans before applying for a mortgage. While FHA is more flexible with DTI, a lower ratio is always better.

- Increasing Down Payment: Although FHA allows down payments as low as 3.5%, making a larger down payment (e.g., 5% or 10%) can sometimes lead to a slightly better rate, as it reduces the lender’s risk. It also reduces your loan amount, lowering your monthly payments and potentially the total interest paid over time. Furthermore, a 10% or greater down payment can reduce the duration of your annual MIP from the life of the loan to 11 years.

Shopping Around for Lenders

This is perhaps the single most impactful step a borrower can take. Because the FHA does not set interest rates, different FHA-approved lenders will offer varying rates and terms.

- Compare Multiple Quotes: Obtain loan estimates from at least three to five different FHA-approved lenders. This can include large banks, credit unions, and independent mortgage brokers. Each lender has its own pricing model, overhead costs, and risk assessment, leading to different rate offerings.

- Understand Lender Fees: Don’t just compare the interest rate; scrutinize the entire Loan Estimate. Look at the lender fees (origination fees, processing fees, underwriting fees, discount points) and the Annual Percentage Rate (APR). A seemingly lower interest rate might come with higher fees, making the APR (and thus the true cost) higher.

- Ask About Lender Credits: Some lenders might offer a “lender credit” to cover some closing costs in exchange for a slightly higher interest rate. This can be beneficial if you have limited cash for closing, but be sure to calculate the long-term cost of the higher interest.

Timing Your Application and Market Awareness

While you can’t control the market, being informed can help you make strategic decisions.

- Monitor Interest Rate Trends: Keep an eye on economic news and mortgage rate forecasts. Websites from reputable financial institutions and mortgage news outlets often provide insights into where rates are headed. This awareness can help you decide when to apply or lock in a rate.

- Understand Rate Locks: Once you have an approved loan application, you typically have the option to “lock in” your interest rate for a specific period (e.g., 30, 45, or 60 days). This protects you if rates rise before closing. However, if rates fall during your lock period, you generally cannot get the lower rate unless your lender offers a “float-down” option, which usually comes with a fee. Discuss rate lock options and policies with your lender.

Current Market Outlook and Future Considerations

The mortgage market is in a constant state of flux, influenced by global economics, domestic policy, and consumer sentiment. Understanding the broader context of interest rates helps in making informed decisions about an FHA loan, both for initial purchase and potential future refinancing.

The Current Interest Rate Environment

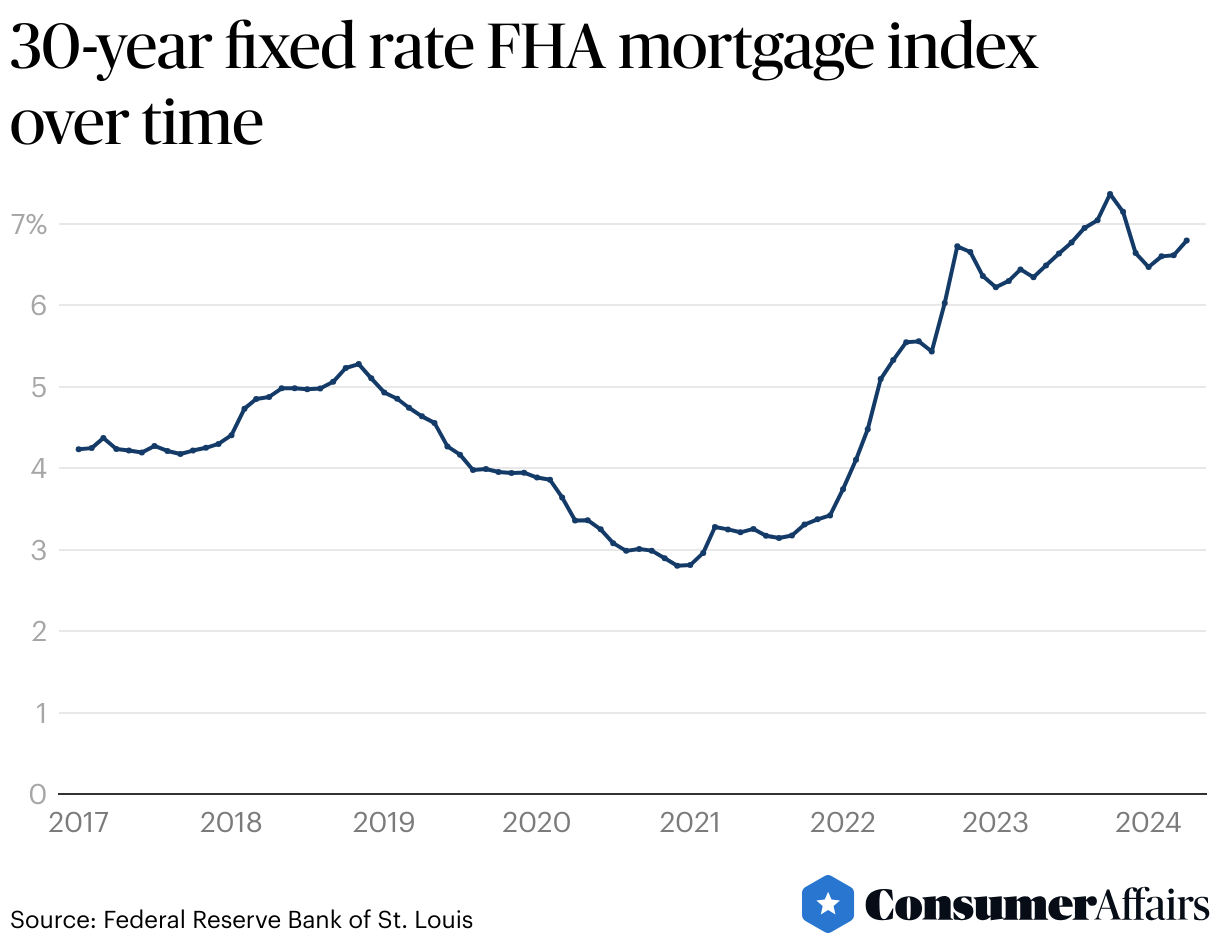

As of the current market, interest rates have experienced significant volatility over the past few years, largely driven by inflation concerns and the Federal Reserve’s response. The Fed’s actions to combat inflation, primarily through raising the federal funds rate, indirectly impact mortgage rates. While the federal funds rate doesn’t directly dictate mortgage rates (which track the 10-year Treasury yield more closely), there’s a strong correlation. When the Fed signals a hawkish stance (favoring higher rates to curb inflation) or economic data shows persistent inflation, mortgage rates tend to rise. Conversely, signs of economic slowdown or receding inflation can lead to a softening of rates.

Prospective homebuyers should expect rates to reflect the ongoing economic narrative—whether it’s persistent inflation, potential recession risks, or the Fed’s pivot towards rate cuts. Therefore, the “current FHA interest rate” is a snapshot, highly sensitive to daily news and market sentiment. It is critical to consult with multiple lenders to get the most up-to-date and personalized quotes.

When Refinancing an FHA Loan Makes Sense

For existing FHA loan holders, or those considering an FHA loan with an eye on future flexibility, refinancing can be a powerful tool, particularly if market conditions change.

- FHA Streamline Refinance: This popular option allows existing FHA borrowers to refinance into a new FHA loan with reduced documentation and no appraisal required. The primary goal is to lower the interest rate, reduce the loan term, or convert an adjustable-rate mortgage to a fixed-rate. The key benefit is that it can be done with minimal paperwork and closing costs, making it attractive when rates drop significantly.

- FHA Cash-Out Refinance: If you have accumulated equity in your home, an FHA cash-out refinance allows you to tap into that equity by replacing your existing mortgage (FHA or conventional) with a new, larger FHA loan. You can take the difference in cash for purposes like home improvements, debt consolidation, or other financial needs. FHA typically allows you to borrow up to 80% of your home’s appraised value.

- Conventional Refinance: If you have substantial equity (at least 20%), you might consider refinancing from an FHA loan to a conventional loan. This can be advantageous because conventional loans typically do not require mortgage insurance once you reach 20% equity (or you can cancel PMI once you hit that threshold), potentially saving you money compared to the potentially lifelong MIP requirement of an FHA loan.

Refinancing decisions should always weigh the new interest rate and loan terms against the closing costs associated with the refinance, as well as the impact of ongoing MIP.

Alternatives to FHA Loans

While FHA loans offer invaluable access to homeownership for many, they aren’t the only option. Depending on your circumstances, other loan types might be more advantageous:

- Conventional Loans: For borrowers with strong credit (typically 620+ FICO), low debt-to-income ratios, and a down payment of at least 3% (though 20% down avoids private mortgage insurance or PMI), conventional loans often offer competitive rates and more flexibility in property types. PMI on conventional loans can typically be canceled once 20% equity is reached.

- VA Loans: Exclusively for eligible service members, veterans, and surviving spouses, VA loans are arguably the most powerful mortgage product available. They require no down payment, no private mortgage insurance, and often offer lower interest rates than FHA or conventional loans.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed to promote homeownership in eligible rural and suburban areas. They offer 100% financing (no down payment required) and low monthly mortgage insurance. Income limits apply, and properties must be in designated rural areas.

Each of these alternatives has specific eligibility criteria and benefits. A knowledgeable mortgage professional can help you compare all options to determine the best fit for your unique financial situation and homeownership goals.

Conclusion

The question “What is the current FHA interest rate?” opens a crucial door to understanding a fundamental pathway to homeownership. While there isn’t a singular, fixed answer, the current FHA interest rate is a daily moving target, influenced by national economic trends, lender-specific policies, and your individual financial profile. FHA loans remain an indispensable tool for many, particularly first-time buyers and those with less traditional financial histories, offering lower down payment requirements and more flexible credit standards.

However, a comprehensive understanding extends beyond just the nominal rate. It requires acknowledging the mandatory upfront and annual mortgage insurance premiums, the array of closing costs, and the overall Annual Percentage Rate (APR). By actively working to strengthen your financial standing, diligently shopping across multiple lenders, and staying informed about market conditions, you can significantly enhance your ability to secure the most favorable terms for your FHA loan. Whether you are buying for the first time, considering a refinance, or exploring alternatives, a thorough and informed approach is your best guide in the complex world of mortgage finance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.