Interest rates are a ubiquitous, yet often misunderstood, force that profoundly shapes the economic landscape and the financial well-being of individuals and businesses alike. From the cost of a mortgage to the returns on a savings account, and from the valuation of a company to the overall pace of economic growth, interest rates are the invisible hand guiding countless financial decisions. Understanding what current interest rates are, the factors that influence them, and their multifaceted impact is not just for economists or financial experts; it is crucial knowledge for anyone navigating the complexities of modern finance. This article will demystify current interest rates, offering insights into their mechanisms, their ripple effects across different financial instruments, and actionable strategies to help you adapt and thrive in any rate environment.

The Fundamentals of Interest Rates: A Core Economic Concept

At its heart, an interest rate is simply the cost of borrowing money or the return on lending it. It represents the “price” of money over time, expressed as a percentage of the principal amount. When you borrow money, you pay interest to the lender for the privilege of using their capital. When you lend money (e.g., by depositing it in a savings account), you earn interest as compensation for parting with your funds and for the risk involved.

Defining Interest Rates

More formally, an interest rate is the percentage charged by a lender to a borrower for the use of assets, typically expressed as an annual percentage rate (APR). It compensates the lender for inflation, the opportunity cost of not using the money for other ventures, and the risk of default by the borrower. For the borrower, it represents the additional cost on top of the principal they must repay. This seemingly simple concept becomes incredibly complex due to the vast array of factors that can influence this percentage.

Key Types of Interest Rates

The financial world is populated by a multitude of interest rates, each serving a specific purpose and influencing different aspects of the economy. While they are interconnected, it’s important to differentiate between them:

- Policy Rates (e.g., Federal Funds Rate, ECB Main Refinancing Operations Rate): These are the benchmark rates set by a country’s central bank. They dictate the rate at which commercial banks borrow from each other or from the central bank. The Federal Funds Rate in the U.S., for instance, is not a rate you directly pay, but it serves as the foundation for virtually all other interest rates in the economy.

- Prime Rate: This is the interest rate commercial banks charge their most creditworthy corporate customers. It is directly influenced by the central bank’s policy rate, typically moving in lockstep with it (e.g., Prime Rate often quoted as Federal Funds Rate + 3%).

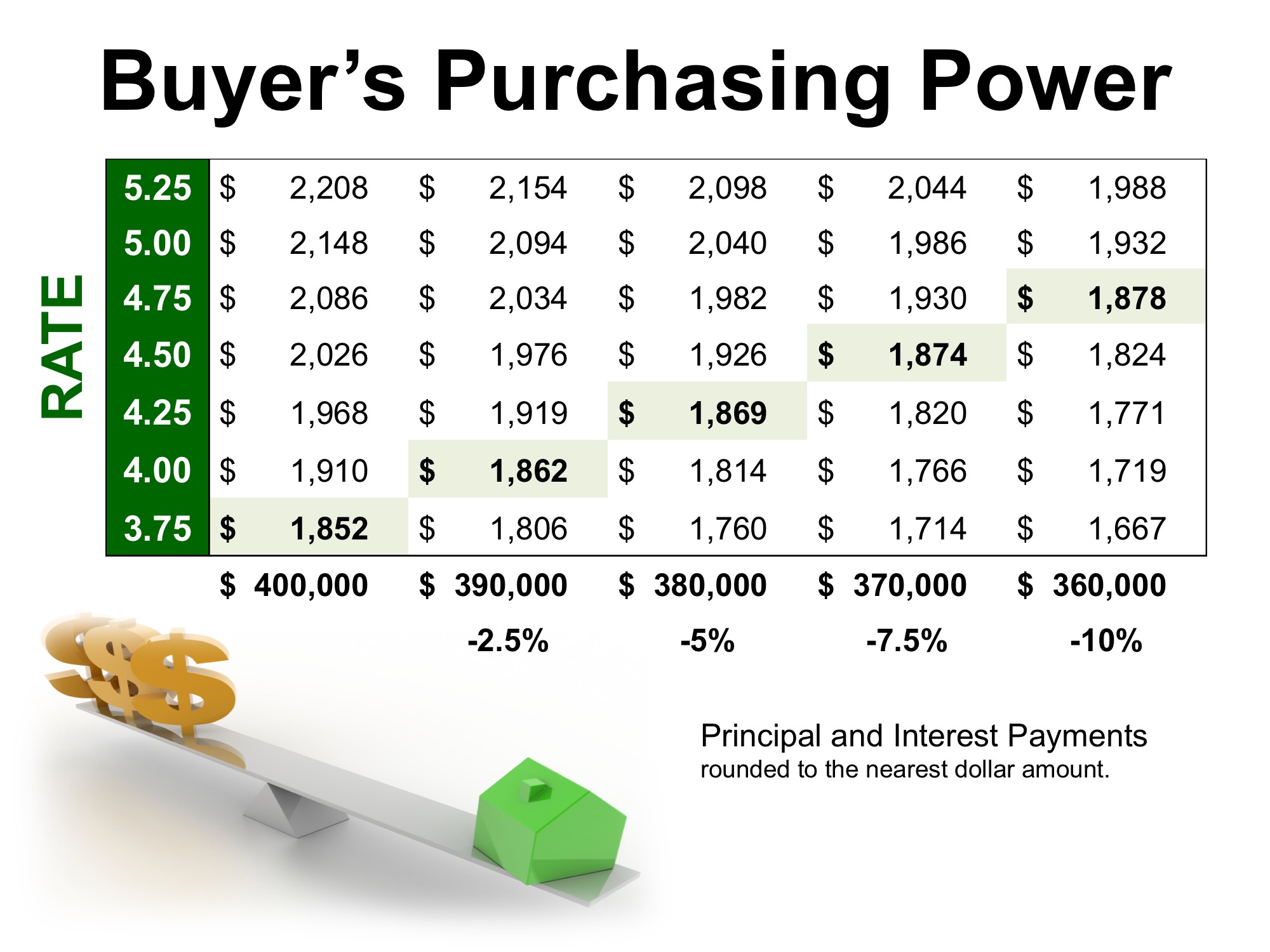

- Mortgage Rates: These are the rates charged on loans used to purchase real estate. They come in various forms, such as fixed-rate mortgages (where the interest rate remains constant for the life of the loan) and adjustable-rate mortgages (ARMs, where the rate can change periodically). Mortgage rates are influenced by bond markets (particularly Treasury yields) and the overall economic outlook.

- Savings Rates (e.g., Savings Accounts, Certificates of Deposit (CDs), Money Market Accounts): These are the rates banks pay to depositors for holding their money. They tend to be lower than lending rates but are crucial for savers looking to grow their capital.

- Loan Rates (Personal, Auto, Credit Card): These rates vary significantly based on the borrower’s creditworthiness, the type of loan, and the lender. Credit card interest rates, in particular, are often among the highest due to their unsecured nature and revolving credit lines. Auto loan rates are typically tied to the prime rate but also depend on the vehicle and borrower’s credit.

Factors Influencing Current Interest Rates

Interest rates are not static; they are in constant flux, responding to a complex interplay of economic forces, central bank policies, and global events. Understanding these drivers is key to anticipating future movements and making informed financial decisions.

Central Bank Monetary Policy

The most significant influence on interest rates comes from a country’s central bank. Institutions like the U.S. Federal Reserve, the European Central Bank (ECB), or the Bank of England utilize monetary policy tools to manage the economy, primarily by adjusting their benchmark policy rates.

- Interest Rate Hikes: When inflation is high or the economy is overheating, central banks typically raise rates to cool down economic activity, making borrowing more expensive and encouraging saving.

- Interest Rate Cuts: During economic downturns or periods of low inflation, central banks may lower rates to stimulate borrowing, investment, and consumer spending.

- Quantitative Easing/Tightening: Beyond setting rates, central banks can also influence longer-term rates through large-scale asset purchases (quantitative easing, QE) or sales (quantitative tightening, QT) of government bonds and other securities. QE drives down long-term rates, while QT pushes them up.

Inflation Expectations

Inflation, the rate at which the general level of prices for goods and services is rising, is a critical determinant of interest rates. Lenders need to ensure that the interest they earn compensates them for the erosion of purchasing power caused by inflation. If inflation is expected to rise, lenders will demand higher interest rates to ensure a real (inflation-adjusted) return on their money. Conversely, low inflation can allow for lower interest rates. Central banks actively monitor inflation and often target a specific inflation rate (e.g., 2%) as part of their mandate.

Economic Growth and Employment

A robust economy, characterized by strong GDP growth and low unemployment, often correlates with higher interest rates. In such an environment, businesses are more likely to invest, and consumers are more confident to spend, increasing the demand for credit. This higher demand, coupled with the potential for inflationary pressures, gives central banks reason to raise rates. Conversely, a sluggish economy with high unemployment typically leads to lower rates as central banks try to inject liquidity and stimulate activity.

Global Economic Conditions

No economy exists in isolation. Global economic trends, international capital flows, and geopolitical stability can significantly impact domestic interest rates. For instance, if foreign investors perceive a country’s economy as risky, they might demand higher yields on its bonds, pushing up interest rates. Major global events, such as a pandemic or a geopolitical conflict, can trigger shifts in investor sentiment, leading to either a flight to safety (driving down rates on stable assets like U.S. Treasuries) or increased risk premiums (driving up rates on riskier assets).

Market Demand and Supply for Credit

Like any other commodity, the price of money (i.e., the interest rate) is subject to the fundamental laws of supply and demand. If there is a high demand for loans from businesses and consumers, and the supply of available funds is limited, interest rates will tend to rise. Conversely, if there’s abundant capital available for lending but weak demand for credit, rates will likely fall. This market dynamic works in conjunction with central bank policy and other factors to set the “current” interest rates across various financial products.

How Current Interest Rates Impact Your Personal Finances

The movement of interest rates has direct and often immediate consequences for your personal financial situation, affecting both the cost of borrowing and the potential for savings and investments.

Borrowing Costs

- Mortgages: For most people, a home is their largest purchase, and mortgage rates are a primary determinant of affordability. When rates rise, the monthly payment on a new mortgage increases, making homeownership more expensive. For those with adjustable-rate mortgages (ARMs), rising rates mean higher monthly payments over time. Conversely, falling rates can make homes more affordable and create opportunities for refinancing existing mortgages at a lower cost.

- Auto Loans: While generally shorter in duration than mortgages, auto loan rates also respond to the broader interest rate environment. Higher rates mean a more expensive car purchase, increasing your monthly payments and the total cost of the vehicle.

- Personal Loans: These unsecured loans are often used for debt consolidation or unexpected expenses. Their rates are highly sensitive to the prime rate, meaning rising rates make them more costly.

- Credit Cards: Credit card interest rates are typically variable and among the highest. As the prime rate increases, the APR on most credit cards will also rise, making carrying a balance significantly more expensive.

Savings and Investments

- Savings Accounts, CDs, Money Market Accounts: For savers, higher interest rates are generally a positive. Banks offer more attractive yields on these accounts to attract deposits, allowing your money to grow faster. Conversely, in a low-rate environment, these accounts offer minimal returns, sometimes struggling to keep pace with inflation.

- Bond Market Performance: Interest rates and bond prices have an inverse relationship. When interest rates rise, the value of existing bonds with lower fixed interest rates typically falls, as new bonds are issued with higher, more attractive yields. For investors holding bonds, this can mean a decline in their portfolio’s value. However, for those looking to buy new bonds, rising rates offer opportunities for higher future income.

- Impact on Stock Market: The relationship between interest rates and the stock market is more indirect but significant. Higher interest rates can make borrowing more expensive for companies, potentially slowing down their growth and profitability. They also make bonds more attractive relative to stocks, as bonds offer a “risk-free” return. This can lead investors to shift capital from stocks to bonds, potentially putting downward pressure on stock prices. Conversely, lower rates can stimulate economic activity, boost corporate profits, and make stocks more appealing.

Refinancing Opportunities

Understanding current interest rates is critical for identifying refinancing opportunities. If market rates fall significantly below the rate on your existing mortgage, auto loan, or personal loan, refinancing could save you thousands of dollars over the life of the loan by reducing your monthly payments or the total interest paid. However, refinancing also involves closing costs and fees, so a careful cost-benefit analysis is always necessary.

Navigating the Current Interest Rate Landscape: Strategies for Individuals and Businesses

Regardless of whether rates are rising, falling, or holding steady, there are proactive steps individuals and businesses can take to optimize their financial position.

For Borrowers

- Locking in Rates: If you anticipate interest rates to rise, consider locking in a fixed-rate mortgage or other long-term loans. This secures your repayment terms and protects you from future rate hikes.

- Paying Down High-Interest Debt: Prioritize paying off credit card balances and other high-interest unsecured loans, especially in a rising rate environment. The compounding effect of high interest can quickly erode your financial health.

- Shopping Around for Best Rates: Don’t settle for the first offer. Compare rates from multiple lenders for mortgages, auto loans, and personal loans. Even a slight difference in APR can result in substantial savings over the loan’s term.

- Improving Credit Score: A higher credit score signals lower risk to lenders, often qualifying you for lower interest rates. Regularly check your credit report, pay bills on time, and reduce your credit utilization to boost your score.

For Savers and Investors

- Maximizing High-Yield Savings Accounts and CDs: In a rising rate environment, seek out high-yield savings accounts, money market accounts, or certificates of deposit (CDs) offered by online banks or credit unions, which often provide better returns than traditional brick-and-mortar institutions.

- Considering Short-Term Bonds or Bond Ladders: If you’re investing in bonds and rates are rising, short-term bonds are less sensitive to rate hikes than long-term bonds. A bond ladder strategy, where you invest in bonds with staggered maturity dates, allows you to reinvest maturing funds at potentially higher rates.

- Diversifying Investment Portfolio: Maintain a diversified portfolio across different asset classes (stocks, bonds, real estate, commodities). This helps mitigate risk as different assets perform differently in various interest rate environments.

- Seeking Professional Financial Advice: A qualified financial advisor can help you assess your personal financial situation, risk tolerance, and goals, then tailor an investment strategy that accounts for current and projected interest rate trends.

For Businesses

- Managing Debt and Capital Expenditures: Businesses need to carefully manage their debt load. In a rising rate environment, they should prioritize paying down variable-rate debt and carefully evaluate the cost of new capital expenditures, especially if financing is required.

- Optimizing Cash Flow: Strong cash flow management is always important, but particularly so when borrowing costs are high. Businesses should focus on efficient inventory management, timely accounts receivable collection, and prudent spending.

- Forecasting Interest Rate Movements: Businesses, especially those with significant debt or large capital projects planned, should incorporate interest rate forecasts into their financial planning and budgeting processes to anticipate potential increases in financing costs.

The Future Outlook for Interest Rates: What to Watch For

Predicting future interest rate movements with certainty is impossible, even for experts. However, staying informed about key indicators and central bank communications can provide valuable clues about potential trends.

Central Bank Commentary

Pay close attention to statements, speeches, and meeting minutes from central bank officials. Their “forward guidance” on economic outlook, inflation expectations, and their readiness to adjust policy rates offers significant insight into their likely actions.

Economic Data Releases

Regularly monitor key economic data releases, including inflation reports (e.g., Consumer Price Index, Personal Consumption Expenditures), employment figures (e.g., jobs reports, unemployment rate), and Gross Domestic Product (GDP) growth. These are the primary inputs central banks use to make their policy decisions.

Geopolitical Developments

Global events, such as wars, trade disputes, or major energy price shocks, can have far-reaching economic consequences that influence central bank policy and market sentiment, thereby affecting interest rates.

Expert Predictions vs. Personal Due Diligence

While financial analysts and economists offer forecasts, remember that these are just predictions. It’s essential to understand the underlying rationale for these forecasts and to conduct your own due diligence. Focus on developing a resilient financial plan that can withstand various interest rate scenarios rather than trying to perfectly time the market.

Conclusion

Current interest rates are far more than just numbers on a screen; they are a fundamental component of the economic engine that impacts virtually every aspect of personal and business finance. From determining the affordability of a home to shaping investment returns and influencing corporate growth, their reach is extensive. By understanding the core concepts of interest rates, the factors that drive their fluctuations, and their specific impacts on borrowing and saving, individuals and businesses can make more informed decisions. Staying aware of central bank actions, economic indicators, and global developments allows for proactive adjustments to financial strategies. In an ever-evolving economic landscape, knowledge of current interest rates is not just advantageous—it is indispensable for securing and enhancing your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.