For many aspiring homeowners and those looking to refinance, the 30-year fixed mortgage is the cornerstone of their financial planning. It represents stability, predictability, and a long-term commitment that underpins one of the largest financial decisions most individuals will ever make. But what exactly are current 30-year fixed mortgage rates, and more importantly, what influences them? Understanding the dynamics behind these rates is crucial for making informed financial decisions in the ever-evolving housing market. This article delves into the mechanisms, influences, and strategies surrounding current 30-year fixed mortgage rates, providing a comprehensive guide for navigating this essential financial landscape.

Understanding the 30-Year Fixed Mortgage

The 30-year fixed-rate mortgage is the most popular mortgage product in the United States, and for good reason. Its widespread appeal stems from a combination of stability, predictability, and manageable monthly payments, making homeownership accessible and less financially volatile for millions of people.

Why 30-Year Fixed Is Popular

The primary allure of a 30-year fixed mortgage lies in its unwavering interest rate. Unlike adjustable-rate mortgages (ARMs), where the interest rate can fluctuate over time based on market conditions, a fixed-rate mortgage locks in the same interest rate for the entire 30-year term of the loan. This means your principal and interest payment remains constant from the day you close on your home until the day you pay it off. This predictability is a huge advantage for household budgeting, allowing homeowners to forecast their housing expenses precisely, regardless of economic shifts or changes in the broader interest rate environment.

Furthermore, spreading the repayment over three decades results in lower monthly payments compared to shorter-term mortgages, such as a 15-year fixed loan. While a 15-year mortgage typically offers a lower overall interest rate and results in less interest paid over the life of the loan, its higher monthly payments can be a barrier for many homebuyers, especially first-time buyers or those with budget constraints. The lower monthly payment of a 30-year fixed mortgage provides greater financial flexibility, potentially freeing up cash flow for other investments, savings, or discretionary spending. It also offers a cushion against unexpected financial challenges, as the fixed payment remains manageable even if incomes are temporarily disrupted.

How Fixed Rates Work

When you secure a 30-year fixed mortgage, the lender and borrower agree on a specific interest rate at the time of closing. This rate is then applied to the outstanding loan balance for the next 360 months (30 years). Your monthly payment is calculated using an amortization schedule, which determines how much of each payment goes towards interest and how much goes towards the principal balance. In the early years of the loan, a larger portion of your payment goes towards interest, while in later years, more is allocated to paying down the principal.

Lenders determine the fixed interest rate they offer based on a complex interplay of factors, including their cost of funds, their desired profit margin, and the perceived risk of lending to a particular borrower. Once the rate is locked in, it remains unchanged, offering a crucial layer of security against rising interest rates. This stability is particularly valuable during periods of economic uncertainty or expected rate hikes, as it shields homeowners from the increased payment burdens that adjustable-rate mortgages might impose. However, it also means that if market rates fall significantly after you’ve locked in, you would need to refinance to take advantage of the lower rates, incurring additional costs in the process.

Factors Influencing Current Mortgage Rates

Mortgage rates are not static; they are highly dynamic, responding to a myriad of economic, financial, and even geopolitical forces. Understanding these underlying drivers is key to anticipating future movements and making timely decisions.

The Federal Reserve and Monetary Policy

The Federal Reserve plays a pivotal, though indirect, role in shaping mortgage rates. While the Fed does not directly set mortgage rates, its monetary policy decisions significantly influence the broader interest rate environment. The primary tool is the federal funds rate, which is the target rate for overnight lending between banks. When the Fed raises the federal funds rate, it generally makes borrowing more expensive for banks, which then pass these higher costs on to consumers in the form of higher rates on various loans, including credit cards, auto loans, and to some extent, mortgages.

Beyond the federal funds rate, the Fed also engages in quantitative easing (QE) or quantitative tightening (QT). During QE, the Fed purchases large quantities of government bonds and mortgage-backed securities (MBS) from the open market. This increases demand for these securities, driving up their prices and, consequently, pushing down their yields. Mortgage rates tend to track the yields on MBS, so lower yields generally translate to lower mortgage rates. Conversely, during QT, the Fed allows its holdings of these securities to mature without reinvesting, effectively reducing demand and allowing yields, and thus mortgage rates, to rise.

Inflation Expectations

Inflation is a critical factor for lenders. When inflation is high or expected to rise, the purchasing power of money decreases over time. For lenders, this means the fixed interest payments they receive over the life of a 30-year mortgage will be worth less in real terms in the future. To compensate for this anticipated loss in purchasing power, lenders demand a higher interest rate to ensure a reasonable return on their investment. Therefore, strong inflation signals or forecasts often lead to an upward pressure on mortgage rates. Central banks, like the Federal Reserve, often use interest rate hikes as a tool to combat inflation, further solidifying the link between inflation expectations and mortgage costs.

Economic Indicators

The health and trajectory of the broader economy are closely watched by lenders and bond investors. Key economic indicators such as Gross Domestic Product (GDP) growth, employment data (e.g., jobless claims, unemployment rate), consumer confidence, and manufacturing output can all influence mortgage rates. A strong and growing economy, characterized by robust job growth and increasing consumer spending, often signals higher inflation and potential interest rate hikes, leading to higher mortgage rates. Conversely, signs of economic weakness or recessionary fears can lead to lower rates, as investors seek the safety of bonds, driving down yields, and the Fed may consider cutting rates to stimulate the economy.

The Bond Market (Treasury Yields)

Perhaps the most direct daily influence on 30-year fixed mortgage rates comes from the bond market, specifically the yield on the 10-year U.S. Treasury note. Mortgage-backed securities (MBS), which are bundles of mortgages sold to investors, compete with U.S. Treasury bonds for investor attention. As such, the yield on the 10-year Treasury note serves as a benchmark for long-term interest rates and is highly correlated with 30-year fixed mortgage rates. When the yield on the 10-year Treasury rises, mortgage rates typically follow suit, and vice-versa. Investors consider Treasuries to be a very safe investment; if their yield increases, mortgage lenders must offer more attractive rates to compete for capital.

Market Sentiment and Global Events

Beyond core economic data, market sentiment and major global events can introduce significant volatility into mortgage rates. Geopolitical tensions, international trade disputes, pandemics, or even significant natural disasters can create uncertainty, causing investors to shift their assets, which in turn affects bond yields and mortgage rates. For instance, during periods of global instability, investors might flock to “safe haven” assets like U.S. Treasuries, driving down their yields and potentially leading to a temporary dip in mortgage rates. Conversely, positive global news that signals stronger economic growth abroad could draw investment away from U.S. assets, pushing yields and mortgage rates higher. The interconnectedness of global financial markets means that seemingly distant events can have tangible impacts on your mortgage payment.

Navigating the Current Rate Environment

Understanding the current landscape of 30-year fixed mortgage rates requires an awareness of recent trends, typical ranges, and how a borrower’s individual financial profile impacts the rate they receive. Mortgage rates are constantly in flux, making it challenging to pinpoint an exact “current” rate without looking at real-time market data.

General Range and Recent Trends

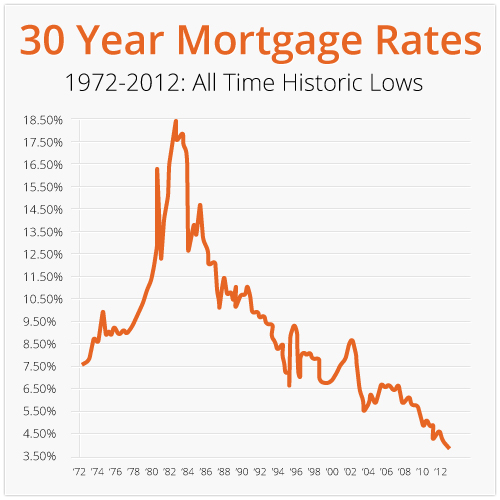

While I cannot provide an exact real-time figure, it’s important to recognize that mortgage rates have generally moved through various cycles. For example, following periods of economic stimulus, rates might have dipped to historic lows, making borrowing incredibly affordable. Conversely, in periods of robust economic growth or high inflation, central banks might raise interest rates, leading to an upward trend in mortgage rates. Recent history has shown periods where rates hovered in the low single digits, followed by significant increases, potentially moving into the mid-to-high single digits, depending on the prevailing economic climate, inflation concerns, and central bank actions.

When observing “current” rates, one should look for the average rates offered by various lenders, often published by financial news outlets or mortgage industry associations. These averages provide a benchmark, but individual rates can vary. It’s crucial to understand that rates are dynamic; what is “current” today might be different tomorrow. Therefore, prospective borrowers should monitor trends rather than fixating on a single daily figure, considering if rates are generally trending up, down, or sideways.

Impact of Borrower Profile

The “current” rate you personally receive will not only depend on the broader market but also significantly on your individual financial health. Lenders assess risk, and a stronger borrower profile translates to lower perceived risk, often resulting in a more favorable interest rate.

- Credit Score: Your FICO credit score is paramount. Lenders use it to gauge your creditworthiness and your likelihood of repaying the loan. Borrowers with excellent credit scores (typically 760 or higher) consistently qualify for the lowest available rates, as they are considered less risky. Lower credit scores generally lead to higher interest rates to compensate the lender for increased risk.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 36%, though some lenders go higher) indicates that you have sufficient income to manage your existing debts and a new mortgage payment, making you a more attractive borrower.

- Down Payment: A larger down payment reduces the loan-to-value (LTV) ratio, meaning you’re borrowing less relative to the home’s value. This also signals to the lender that you have more equity invested in the property, making you less likely to default. Lenders often offer better rates for larger down payments, sometimes also waiving private mortgage insurance (PMI) if you put down 20% or more.

- Loan Type and Term: While we’re focusing on 30-year fixed, variations like FHA, VA, or USDA loans can also have specific rate implications due to government backing.

- Loan Amount: Very large or very small loan amounts can sometimes affect the offered rate, though this is less common for standard conventional mortgages.

Understanding APR vs. Interest Rate

When comparing mortgage offers, it’s vital to differentiate between the interest rate and the Annual Percentage Rate (APR). The interest rate is simply the cost of borrowing the principal loan amount, typically expressed as a percentage. The APR, however, provides a more comprehensive measure of the total cost of the loan over its term. It includes the interest rate plus certain other costs and fees associated with the loan, such as origination fees, discount points, mortgage insurance, and processing fees.

Because the APR incorporates these additional costs, it will almost always be higher than the interest rate. Comparing the APR across different lenders offers a more accurate “apples-to-apples” comparison of the true cost of borrowing, as it factors in various fees that might not be immediately apparent when only looking at the interest rate. Always ask for and compare the APR when shopping for a mortgage to get a full picture of the loan’s expense.

Strategies for Securing the Best Mortgage Rate

Even in a challenging rate environment, proactive steps can significantly impact the 30-year fixed mortgage rate you ultimately secure. A combination of financial preparedness and diligent shopping is essential.

Improve Your Credit Score

Your credit score is arguably the single most important factor within your control that influences the mortgage rate you’ll be offered. Lenders use it as a primary indicator of your financial responsibility and risk. To improve your score:

- Pay bills on time, every time: Payment history is the largest component of your score.

- Reduce outstanding debt: Especially credit card balances, to lower your credit utilization ratio.

- Avoid opening new credit accounts: New accounts can temporarily lower your score and signal potential risk.

- Check your credit report for errors: Disputing inaccuracies can quickly boost your score.

- Keep old accounts open: A longer credit history is generally beneficial.

Aim for a score in the “excellent” range (typically 760 or above) to qualify for the most competitive rates.

Save for a Larger Down Payment

A larger down payment signals greater financial stability to lenders and reduces their risk. A down payment of 20% or more of the home’s purchase price not only often qualifies you for a better interest rate but also allows you to avoid paying private mortgage insurance (PMI), an additional monthly cost that protects the lender in case you default. Even if you can’t reach 20%, a larger down payment, even if it’s 10% or 15%, can still positively influence the rate you receive compared to a minimal down payment.

Shop Around and Compare Lenders

This is perhaps the most critical step. Just as you wouldn’t buy a car without comparing prices from multiple dealerships, you shouldn’t accept the first mortgage offer you receive. Mortgage rates and fees can vary significantly between lenders for the exact same borrower profile.

- Contact multiple types of lenders: This includes large national banks, smaller community banks, credit unions, and online mortgage brokers.

- Get quotes on the same day: Rates fluctuate daily, so gather all your comparison quotes within a 24-48 hour window for an accurate “apples-to-apples” comparison.

- Request a Loan Estimate: Lenders are legally required to provide a standardized Loan Estimate form, which clearly details the interest rate, APR, closing costs, and other fees. This makes direct comparison much easier.

Consider Mortgage Points (Discount Points)

Mortgage points, also known as discount points, are essentially prepaid interest. One point typically costs 1% of the total loan amount and is paid upfront at closing in exchange for a lower interest rate over the life of the loan. This strategy is most beneficial for borrowers who plan to stay in their home for many years, as it takes time for the savings from the lower interest rate to offset the upfront cost of the points. Calculate the break-even point to determine if buying down the rate is financially advantageous for your specific situation.

Lock in Your Rate

Once you’ve found a competitive rate and are ready to proceed with your loan application, ask your lender about “locking in” your interest rate. A rate lock guarantees that your interest rate will not change between the time you lock it and your closing date, typically for a period of 30 to 60 days. This protects you from potential rate increases during the underwriting process. Be aware that some lenders may charge a fee for rate locks, especially for longer lock periods, and confirm if there are any “float down” options if rates happen to drop significantly after you’ve locked.

Beyond the 30-Year Fixed: Other Considerations

While the 30-year fixed mortgage is a staple, it’s not the only option, nor is it always the best fit for everyone. Understanding alternatives and the value of professional guidance is crucial for holistic financial planning.

Refinancing Opportunities

For current homeowners with a 30-year fixed mortgage, refinancing can be a powerful tool. If current rates drop significantly below your existing mortgage rate, or if your credit score and financial situation have improved substantially since you first took out your loan, refinancing could save you a considerable amount of money over the life of the loan. Refinancing involves taking out a new mortgage to pay off your old one, ideally at a lower interest rate or with different terms. It can also be used to switch from an ARM to a fixed-rate mortgage, shorten your loan term (e.g., from 30 to 15 years), or even tap into your home equity through a cash-out refinance. However, refinancing incurs closing costs, so it’s essential to calculate the break-even point to ensure the savings outweigh the expenses.

Adjustable-Rate Mortgages (ARMs)

While fixed-rate mortgages offer stability, Adjustable-Rate Mortgages (ARMs) can sometimes present an attractive alternative, particularly for certain financial situations. ARMs typically offer a lower initial interest rate for an introductory period (e.g., 5, 7, or 10 years), after which the rate adjusts periodically based on a predetermined index plus a margin.

- Pros: Lower initial payments can make homeownership more accessible, and if rates fall, your payments could decrease. They can be ideal for individuals who plan to sell their home before the fixed-rate period expires or who anticipate a significant increase in their income in the near future.

- Cons: The risk of rising rates means your monthly payments could increase substantially, potentially straining your budget. There are usually caps on how much the rate can adjust per period and over the life of the loan, but payments can still become unpredictable.

The Importance of Professional Advice

Navigating the complexities of mortgage rates, loan options, and the application process can be daunting. Engaging with qualified financial professionals can provide invaluable guidance.

- Mortgage Brokers: These professionals work with multiple lenders and can help you compare various loan products and rates from different institutions, potentially finding you the best deal without you having to approach each lender individually.

- Loan Officers/Lenders: Directly working with a loan officer from a specific bank or credit union can also be beneficial, especially if you have an established relationship with that institution.

- Financial Advisors: A broader financial advisor can help you integrate your mortgage decision into your overall financial plan, considering your long-term goals, investment strategies, and risk tolerance.

They can help you understand the fine print, assess your personal financial situation, and choose a mortgage product that aligns with your objectives, saving you time, money, and potential headaches in the long run.

Conclusion

Understanding “what are current 30-year fixed mortgage rates” is far more nuanced than simply looking up a number. It involves grasping the intricate web of economic indicators, monetary policy decisions, and market sentiment that continuously shape these rates. For individuals contemplating homeownership or refinancing, the 30-year fixed mortgage remains a popular choice due to its predictability and stable monthly payments.

However, the rate you secure is ultimately a product of both the prevailing market conditions and your individual financial health. By focusing on improving your credit score, making a substantial down payment, diligently shopping around for lenders, and strategically considering options like mortgage points or refinancing, you can significantly influence the rate you ultimately receive. Furthermore, recognizing when an adjustable-rate mortgage might be a better fit and leveraging the expertise of financial professionals can streamline the decision-making process. In the dynamic world of personal finance, being informed, proactive, and strategic is your greatest asset in securing the most favorable 30-year fixed mortgage rate possible.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.