Embarking on the journey of homeownership is one of the most significant financial decisions an individual or family can make. At the heart of this decision lies the home loan, and arguably its most critical component: the interest rate. Far more than just a number, the home loan rate dictates the total cost of borrowing, directly influencing your monthly payments and the overall affordability of your dream home. Understanding “what are home loan rates?” is not merely a matter of curiosity; it’s a fundamental requirement for making informed choices that can save you tens, even hundreds, of thousands of dollars over the lifetime of your mortgage.

This comprehensive guide delves into the intricate world of home loan rates, demystifying their definition, exploring the myriad factors that influence them, outlining the various options available, and equipping you with strategies to secure the most favorable terms. Whether you’re a first-time homebuyer or looking to refinance, a clear grasp of this crucial financial metric is your strongest asset.

Understanding the Fundamentals of Home Loan Rates

Before diving into the complexities, it’s essential to lay a solid foundation by understanding what home loan rates truly represent and how they function.

Definition and Core Components

At its most basic, a home loan interest rate is the cost of borrowing money from a lender, expressed as a percentage of the principal loan amount. This percentage is added to your loan payments, compensating the lender for the use of their capital and for the risk they undertake. It’s the engine that drives your mortgage payment calculation. When a lender quotes a rate, it’s typically an Annual Percentage Rate (APR), which includes not just the interest rate but also certain other costs and fees associated with the loan, providing a more holistic view of the total cost of borrowing. However, the initial quoted interest rate is what primarily determines the size of your monthly principal and interest payment.

Beyond the numerical rate, several core components are at play:

- Principal: The original amount of money borrowed for the home purchase.

- Interest: The charge for borrowing the principal, calculated as a percentage.

- Term: The length of time over which you agree to repay the loan (e.g., 15 years, 30 years).

- Amortization: The process of gradually paying off a debt over time through a series of regular payments. In the early years of a mortgage, a larger portion of your payment goes towards interest; later, more goes towards principal.

Fixed vs. Adjustable Rates: A Crucial Distinction

One of the most significant choices you’ll face when securing a home loan is whether to opt for a fixed-rate mortgage or an adjustable-rate mortgage (ARM). Each has distinct characteristics and implications for your financial planning.

- Fixed-Rate Mortgage (FRM): With a fixed-rate mortgage, the interest rate remains constant for the entire duration of the loan term. This means your principal and interest payment will stay the same every month, regardless of market fluctuations. Borrowers often prefer fixed rates for their predictability and stability, making budgeting easier and offering protection against rising interest rates. The most common terms are 15-year and 30-year fixed mortgages.

- Adjustable-Rate Mortgage (ARM): An ARM features an interest rate that is initially fixed for a period (e.g., 3, 5, 7, or 10 years) and then adjusts periodically based on an underlying index plus a margin set by the lender. While ARMs typically offer a lower initial interest rate than fixed-rate mortgages, the uncertainty of future rate adjustments introduces risk. If interest rates rise, your monthly payments could increase significantly; if they fall, your payments could decrease. ARMs often appeal to borrowers who plan to sell or refinance before the fixed-rate period ends, or those who anticipate a future increase in income.

The Impact of Interest Rates on Your Mortgage Payments

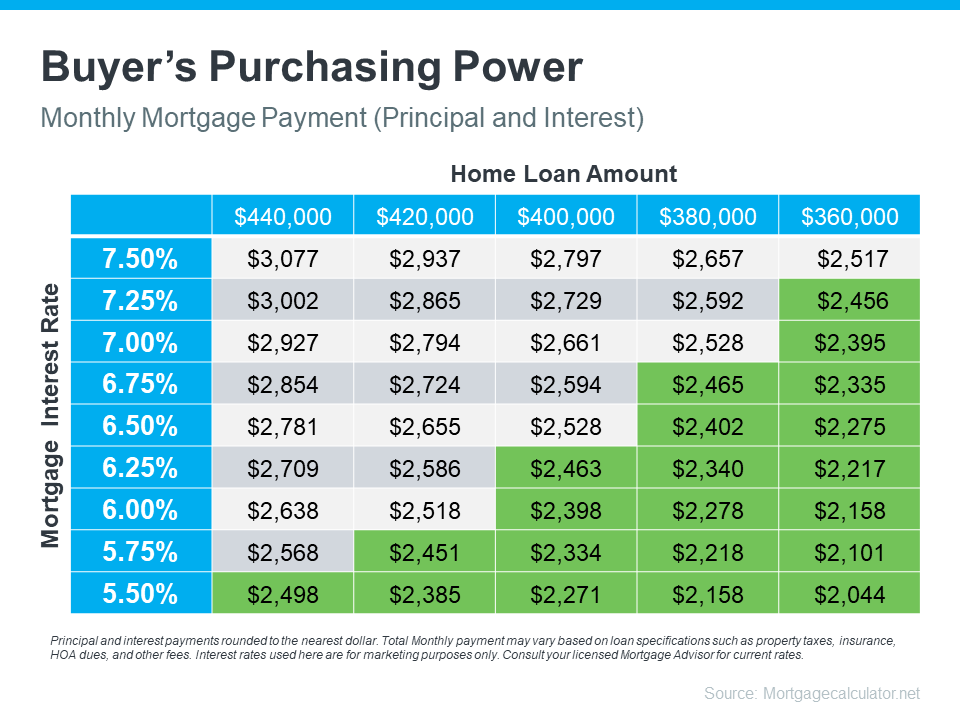

Even a seemingly small difference in an interest rate can have a profound impact on your monthly mortgage payment and the total cost of your home over the loan’s lifetime. For instance, on a $300,000 30-year fixed-rate mortgage, a difference of just 0.5% (e.g., from 6.0% to 6.5%) can add hundreds of dollars to your monthly payment and tens of thousands to the total interest paid over the life of the loan. This demonstrates why securing the lowest possible rate, even if it’s just a fraction of a percent lower, is incredibly advantageous and central to smart financial planning for homeowners.

Key Factors Influencing Home Loan Rates

Home loan rates are not static; they are dynamic and influenced by a complex interplay of macroeconomic forces, financial market conditions, and individual borrower characteristics. Understanding these drivers is crucial for anticipating market movements and timing your loan application.

Economic Indicators: Inflation, GDP, and Employment

The broader economic landscape plays a pivotal role in shaping interest rates. Lenders and investors assess economic health to gauge risk and return.

- Inflation: When inflation (the rate at which prices for goods and services are rising) is high, lenders demand higher interest rates to ensure that the return on their loans outpaces the erosion of purchasing power. The expectation of future inflation is a significant upward pressure on rates.

- Gross Domestic Product (GDP): A strong, growing economy (indicated by rising GDP) often leads to increased demand for credit, which can push rates higher. Conversely, a weakening economy might see rates fall as demand for loans decreases and lenders compete for business.

- Employment Data: Robust job growth and low unemployment signal a healthy economy, which can contribute to higher inflation expectations and, consequently, higher interest rates. Weak employment data, on the other hand, might prompt the Federal Reserve to lower rates to stimulate economic activity.

Federal Reserve Policy and the Federal Funds Rate

The Federal Reserve, the central bank of the United States, is arguably the most influential entity in determining the direction of interest rates. While the Fed does not directly set mortgage rates, its actions significantly impact them.

- Federal Funds Rate: The Fed primarily influences rates through its target for the federal funds rate – the rate at which banks lend reserves to each other overnight. When the Fed raises this target, it makes borrowing more expensive for banks, which then pass these higher costs on to consumers in the form of higher interest rates for various loans, including mortgages. Conversely, lowering the federal funds rate aims to stimulate borrowing and economic activity.

- Quantitative Easing/Tightening: Beyond the federal funds rate, the Fed also engages in open market operations, such as buying or selling government bonds and mortgage-backed securities (MBS). Buying MBS can inject liquidity into the mortgage market, pushing rates down, while selling them can have the opposite effect.

Market Competition Among Lenders

The mortgage market is highly competitive. Lenders are constantly vying for borrowers’ business, and this competition can be a downward force on interest rates. When there are many lenders offering similar products, they might lower their rates to attract more customers. This underscores the importance of shopping around and comparing offers from multiple lenders to ensure you’re getting the most competitive rate available.

Your Personal Financial Profile: Credit Score and Debt-to-Income Ratio

While macroeconomic factors set the general market trend, your individual financial health determines the specific rate you qualify for. Lenders assess your risk profile to determine how likely you are to repay the loan.

- Credit Score: Your credit score (e.g., FICO score) is a numerical representation of your creditworthiness. A higher credit score (generally above 740-760) indicates a lower risk to lenders, making you eligible for the most favorable interest rates. A lower score suggests higher risk, leading to higher rates to compensate the lender.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments (including the prospective mortgage payment) to your gross monthly income. A lower DTI ratio (typically below 43%) signifies that you have sufficient income to manage your debts, making you a more attractive borrower and potentially qualifying you for better rates.

Loan Term and Type of Property

The characteristics of the loan itself also influence the rate.

- Loan Term: Shorter loan terms (e.g., 15-year mortgages) generally come with lower interest rates than longer terms (e.g., 30-year mortgages). This is because lenders perceive less risk over a shorter period, and they get their money back faster. While the monthly payments are higher for a 15-year mortgage, the total interest paid over the life of the loan is significantly less.

- Type of Property: Single-family homes typically receive the most favorable rates. Multi-unit properties, investment properties, or certain types of manufactured homes might be considered higher risk by lenders, potentially resulting in slightly higher interest rates.

Navigating the World of Home Loan Rate Options

Beyond the fixed vs. adjustable decision, a variety of loan products exist, each designed to meet different financial situations and objectives. Understanding these options, along with strategies like buying down your rate, is key to optimizing your mortgage.

Exploring Different Loan Products

The loan product you choose can significantly impact the rates you’re offered and the qualification criteria.

- Conventional Loans: These are not backed by a government agency and typically require a higher credit score and a down payment (though some programs allow for as little as 3%). They offer competitive rates for well-qualified borrowers.

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular among first-time homebuyers or those with lower credit scores. FHA loans allow for lower down payments (as low as 3.5%) but require mortgage insurance premiums (MIP) for the life of the loan, which adds to the overall cost.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, these loans are available to eligible service members, veterans, and their spouses. VA loans often offer 0% down payment and highly competitive interest rates, with no private mortgage insurance (PMI) requirement, making them extremely attractive.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans are designed for low-to-moderate-income buyers in eligible rural areas. They also offer 0% down payment options and competitive rates but come with specific income and property location requirements.

The Role of Mortgage Points: Buying Down Your Rate

One way to directly influence your interest rate is by purchasing “mortgage points,” also known as discount points. A mortgage point is essentially an upfront fee paid to the lender, typically equal to 1% of the loan amount. In exchange for paying points, the lender reduces your interest rate.

- Cost-Benefit Analysis: Deciding whether to buy down your rate depends on how long you plan to stay in the home. If you plan to stay for many years, the long-term savings from a lower interest rate might outweigh the upfront cost of the points. However, if you anticipate moving or refinancing within a few years, paying points might not be financially beneficial. It’s crucial to calculate the break-even point to determine if it makes sense for your specific situation.

When to Refinance: Seizing Opportunities for Better Rates

Refinancing involves replacing your existing mortgage with a new one, often to secure a lower interest rate. This can be a highly effective strategy when market rates drop significantly or when your personal financial profile has improved (e.g., higher credit score, increased income).

- Reasons for Refinancing:

- Lowering Your Interest Rate: The primary driver for refinancing is often to reduce your monthly payment and total interest paid over the life of the loan.

- Changing Loan Term: You might refinance from a 30-year to a 15-year mortgage to pay off your home faster, or from a 15-year to a 30-year to reduce monthly payments.

- Switching Loan Type: Moving from an ARM to a fixed-rate mortgage for stability, or vice-versa if market conditions are favorable for ARMs.

- Cash-Out Refinance: Tapping into your home’s equity by taking out a larger new loan and receiving the difference in cash, often for home improvements or debt consolidation.

- Costs Involved: Refinancing also involves closing costs, similar to your original purchase loan. It’s important to weigh these costs against the potential savings to determine if refinancing is worthwhile.

Strategies for Securing the Best Home Loan Rates

While you can’t control the overall market, you can significantly influence the rate you personally qualify for. Proactive financial planning and diligent research are your best allies.

Boosting Your Credit Score

As discussed, a strong credit score is paramount. Before applying for a mortgage, take steps to improve your creditworthiness:

- Pay Bills on Time: Payment history is the most significant factor in your credit score.

- Reduce Credit Card Balances: Lowering your credit utilization ratio (amount of credit used vs. available) can quickly boost your score.

- Avoid New Credit Applications: Each application can temporarily lower your score.

- Check Your Credit Report for Errors: Dispute any inaccuracies that could be negatively impacting your score.

Reducing Your Debt-to-Income Ratio

Lenders look for a low DTI to ensure you can comfortably handle your new mortgage payment.

- Pay Down Existing Debts: Prioritize paying off high-interest debts like credit card balances or personal loans.

- Increase Your Income: While not always feasible in the short term, increasing your verifiable income will lower your DTI.

- Avoid New Debt: Refrain from taking on new car loans or other significant debts before applying for a mortgage.

Shopping Around and Comparing Offers

This cannot be stressed enough. Different lenders offer different rates and fees, even for the same borrower profile.

- Get Quotes from Multiple Lenders: Contact at least three to five different lenders (banks, credit unions, mortgage brokers, online lenders).

- Compare Loan Estimates: Lenders are required to provide a standardized Loan Estimate form, which makes it easier to compare interest rates, fees, and other costs side-by-side. Pay attention to the APR, which gives a more complete picture of the loan’s overall cost.

- Don’t Just Look at the Rate: Factor in closing costs, lender fees, and any points that might be involved. A slightly higher rate with lower fees might be better than a lower rate with exorbitant fees.

Understanding Rate Locks

Once you find a desirable interest rate, a “rate lock” protects you from market fluctuations while your loan is being processed.

- What is a Rate Lock? It’s an agreement with your lender to guarantee a specific interest rate for a defined period (e.g., 30, 45, or 60 days).

- When to Lock: Lock your rate when you’re confident you have the best offer and your loan is progressing towards closing. Be mindful of the lock period and potential extensions if the closing is delayed.

- Float-Down Option: Some lenders offer a “float-down” option, allowing you to secure a lower rate if market rates fall significantly before closing, typically for an additional fee.

The Future Outlook: What to Expect from Home Loan Rates

While no one can predict the future with absolute certainty, staying informed about economic forecasts and market trends can help you make more timely and strategic decisions regarding home loan rates.

Economic Forecasts and Market Trends

Mortgage rates are generally influenced by the same factors that impact the broader bond market, particularly the yield on the 10-year Treasury bond.

- Inflationary Pressures: If inflation remains elevated, the Federal Reserve might continue to maintain a tighter monetary policy, potentially leading to higher mortgage rates. Conversely, a significant drop in inflation could pave the way for lower rates.

- Economic Growth: A robust economy often supports higher rates due to increased demand for credit and potential inflationary pressures. A slowdown or recession, however, could see rates fall as the Fed might cut rates to stimulate activity.

- Global Events: Geopolitical events, international trade dynamics, and global economic health can also indirectly influence U.S. bond yields and, by extension, mortgage rates.

Preparing for Rate Fluctuations

For potential homebuyers, it’s prudent to prepare for a range of rate scenarios.

- Financial Flexibility: Ensure your personal finances are in robust health to withstand potential rate increases if you’re considering an ARM or waiting for rates to drop.

- Stay Informed: Regularly monitor economic news, Federal Reserve announcements, and expert forecasts. Reputable financial news outlets and mortgage industry analysts provide valuable insights.

- Consult a Professional: A trusted mortgage loan officer or financial advisor can provide personalized guidance based on current market conditions and your unique financial situation. They can help you understand the nuances of different loan products and how potential rate changes might impact your long-term financial goals.

In conclusion, understanding “what are home loan rates?” is a crucial step towards successful homeownership. By grasping the fundamentals, recognizing the influencing factors, exploring available options, and employing smart strategies, you empower yourself to navigate the complex mortgage landscape with confidence, securing the most favorable terms for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.