For most people, a home represents the single largest financial investment they will ever make. The mortgage, the financial instrument used to purchase that home, is inherently tied to a rate of interest that can significantly impact the total cost of ownership over decades. Understanding “how much are mortgage rates” is not merely about checking a daily figure; it’s about comprehending a complex interplay of economic forces, personal financial health, and lending strategies. This article delves into the intricacies of mortgage rates, equipping you with the knowledge to navigate this crucial aspect of personal finance with confidence and insight.

The Basics of Mortgage Rates: What You Need to Know

At its core, a mortgage rate is the interest rate charged by a lender for a loan secured by real estate. It’s the cost of borrowing money to buy a house, expressed as a percentage of the loan amount. This percentage dictates how much extra you’ll pay above the principal loan amount over the life of the mortgage. A seemingly small difference in the interest rate can translate into tens or even hundreds of thousands of dollars in total payments over 15, 20, or 30 years.

Defining Mortgage Rates

A mortgage rate is essentially the price you pay to borrow money from a bank or other financial institution to purchase a home. This rate is usually quoted as an annual percentage. When you make your monthly mortgage payment, a portion goes towards paying down the principal (the actual amount you borrowed), and another portion covers the interest charged by the lender. Early in the loan’s life, a larger share of your payment often goes to interest, gradually shifting towards principal as the loan matures. Understanding this fundamental concept is the first step in demystifying your home loan.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

Mortgages broadly fall into two categories: fixed-rate and adjustable-rate. A fixed-rate mortgage offers a constant interest rate for the entire duration of the loan. This provides predictability and stability in your monthly payments, making budgeting easier and shielding you from future interest rate hikes. It’s a popular choice for those who value stability.

Conversely, an adjustable-rate mortgage (ARM) features an interest rate that can change periodically after an initial fixed period (e.g., 5/1 ARM, 7/1 ARM). For example, a 5/1 ARM has a fixed rate for the first five years, after which the rate adjusts annually based on an index plus a margin set by the lender. ARMs often start with a lower interest rate than fixed-rate mortgages, making them attractive initially. However, they carry the risk of higher payments if interest rates rise in the future. They can be suitable for borrowers who plan to sell or refinance before the fixed-rate period ends, or those comfortable with potential payment fluctuations.

The Impact of Interest on Total Loan Cost

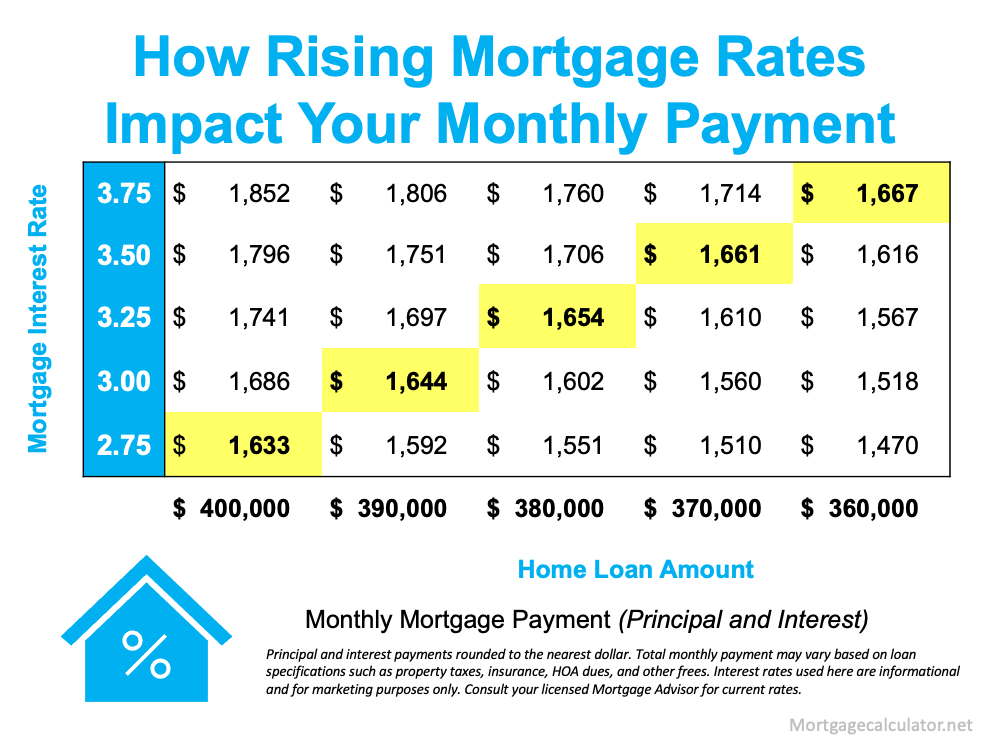

The interest rate profoundly influences the total cost of your mortgage. To illustrate, consider a $300,000, 30-year fixed-rate mortgage. At 4% interest, your monthly principal and interest payment might be around $1,432, leading to total interest paid of approximately $215,500 over 30 years. If the rate were 5%, the monthly payment jumps to about $1,610, and total interest paid surges to roughly $279,600. That one percentage point difference adds over $64,000 to the total cost. This simple comparison underscores why even marginal changes in mortgage rates are a critical concern for homebuyers and existing homeowners alike.

Key Factors Influencing Mortgage Rates

Mortgage rates are not static figures set by a single entity; rather, they are dynamic and influenced by a confluence of macroeconomic forces, lender-specific policies, and individual borrower characteristics. Understanding these drivers is essential for anyone looking to secure a home loan.

Economic Indicators: Inflation, Federal Reserve Policy, and Treasury Yields

The broader economic environment plays a significant role in shaping mortgage rates. Inflation, the rate at which prices for goods and services are rising, is a primary driver. Lenders charge higher interest rates when inflation is expected to increase, to ensure their future returns are not eroded by a decrease in purchasing power.

The Federal Reserve’s monetary policy is another colossal influence. While the Fed does not directly set mortgage rates, its actions, particularly regarding the federal funds rate, have a ripple effect. When the Fed raises its benchmark rate to combat inflation, it typically leads to higher borrowing costs across the economy, including mortgages. Conversely, a reduction in the federal funds rate usually translates to lower mortgage rates.

Treasury yields, specifically the 10-year Treasury bond yield, are often considered a strong predictor of long-term mortgage rates. This is because mortgage-backed securities (MBS), which are a major component of the mortgage market, compete with Treasury bonds for investors. If Treasury yields rise, MBS must offer higher yields (and thus higher mortgage rates) to attract investors.

Lender-Specific Factors: Margins and Business Strategy

While economic forces set a baseline, individual lenders also factor in their own costs and business strategies. Banks and mortgage companies have overheads, administrative costs, and profit margins they need to cover. Different lenders may offer slightly varying rates based on their risk assessment, their current loan portfolio, competitive landscape, and their desired profit margins. Some lenders might offer lower rates to attract more business, while others might focus on specific market segments or offer more personalized services at a slightly higher premium.

Borrower-Specific Factors: Credit Score, Down Payment, and Debt-to-Income (DTI)

Your personal financial profile is arguably the most direct determinant of the rate you’ll be offered. Your credit score is paramount; a higher score (typically 740 and above) signals lower risk to lenders, often qualifying you for the most favorable rates. A lower score indicates higher risk, resulting in higher interest rates.

The down payment also matters. A larger down payment (e.g., 20% or more) reduces the loan-to-value (LTV) ratio, meaning the lender takes on less risk. This often translates to better rates and can also help you avoid private mortgage insurance (PMI).

Your debt-to-income (DTI) ratio is another critical factor. This ratio compares your total monthly debt payments (including the prospective mortgage) to your gross monthly income. Lenders use DTI to assess your ability to manage monthly payments. A lower DTI (generally below 43%) suggests better financial health and can lead to more attractive loan terms.

Loan Type and Term: Conventional, FHA, VA, USDA, and Loan Durations

The type of mortgage you choose, and its duration, will also influence the rate. Conventional loans are not insured or guaranteed by the government and typically require good credit. FHA loans are government-insured and are popular for borrowers with lower credit scores or smaller down payments, but they come with mandatory mortgage insurance premiums. VA loans are for eligible veterans and service members and often offer competitive rates with no down payment or mortgage insurance. USDA loans are for rural properties and also offer no down payment for qualified borrowers. Each loan type carries its own risk profile for lenders and thus its own rate structure.

The loan term is also significant. Shorter terms (e.g., 15-year fixed) typically have lower interest rates than longer terms (e.g., 30-year fixed) because the lender assumes less interest rate risk over a shorter period. While monthly payments are higher for a 15-year loan, the total interest paid over the life of the loan is substantially less.

Navigating the Mortgage Application Process and Rate Shopping

Securing a mortgage involves more than just finding a house; it requires strategic financial planning and diligent rate shopping. The process can seem daunting, but breaking it down into manageable steps can lead to a more favorable outcome.

Pre-Approval: Understanding Your Borrowing Power

Before you even start house hunting seriously, getting pre-approved for a mortgage is crucial. Pre-approval involves a lender reviewing your financial information (credit, income, assets) and providing you with a conditional commitment for a specific loan amount and estimated interest rate. This step not only gives you a realistic budget for your home search but also demonstrates to sellers that you are a serious and qualified buyer, which can be a significant advantage in competitive markets. It also gives you an early indication of the interest rate you might qualify for, allowing you to fine-tune your financial expectations.

The Importance of Shopping Around for Rates

One of the biggest mistakes homebuyers make is only checking with one lender. Mortgage rates can vary significantly between different financial institutions, even on the same day for the same borrower. Shopping around means contacting multiple lenders—banks, credit unions, and mortgage brokers—to compare their rates, fees, and loan terms. Get quotes from at least three to five lenders. Many online tools allow for quick comparisons, but always follow up directly with a loan officer to get a personalized quote based on your specific financial situation. A difference of even 0.25% can save you thousands over the life of the loan, so this step is critical for securing the best possible rate.

Understanding Loan Estimates and Closing Costs

Once you apply for a mortgage, lenders are required to provide you with a Loan Estimate (LE) within three business days. This standardized form details the loan’s estimated interest rate, monthly payment, and total closing costs. It also outlines other important information like loan terms, projected payments, and costs at closing. Pay close attention to all the fees listed, including origination fees, appraisal fees, title insurance, and escrow charges. These closing costs can add up to 2-5% of the loan amount, so understanding them upfront is vital for budgeting. Compare the LEs from different lenders meticulously to ensure you’re comparing apples to apples and not just focusing on the interest rate in isolation.

Locking In Your Rate

Mortgage rates fluctuate daily, sometimes even hourly. After you’ve chosen a lender and a specific loan product, you’ll typically have the option to “lock in” your interest rate. This means the lender guarantees that rate for a specific period, usually 30 to 60 days, while your loan is processed and underwritten. Rate locks protect you from rising rates during the closing period. However, be aware of the lock-in period’s duration and any associated fees. If rates drop significantly after you’ve locked, you might be able to “float down” your rate, but this often comes with a fee or is only available under specific lender policies. Discuss the rate lock policy thoroughly with your loan officer.

Strategies for Securing the Best Possible Mortgage Rate

Beyond understanding the market, there are actionable steps you can take to position yourself for the most favorable mortgage rates. A proactive approach to your financial health and a strategic mindset during the loan process can yield substantial savings.

Improving Your Financial Profile

As discussed, your credit score, down payment, and DTI ratio are major determinants of your rate. Improving these aspects before applying can make a significant difference.

- Boost your credit score: Pay bills on time, reduce credit card balances, and avoid opening new credit accounts in the months leading up to your mortgage application.

- Increase your down payment: Saving more for a down payment reduces your loan-to-value ratio, lowering the lender’s risk and potentially earning you a better rate. A 20% down payment also typically allows you to avoid private mortgage insurance (PMI).

- Lower your debt-to-income ratio: Pay down existing debts, especially high-interest consumer debt, and avoid taking on new debt before applying for a mortgage. This demonstrates greater financial capacity to manage your future mortgage payments.

Considering Points and Lender Credits

When comparing rates, you’ll often encounter the option to pay discount points (also known as mortgage points) or receive lender credits.

- Discount Points: These are upfront fees paid to the lender at closing in exchange for a lower interest rate over the life of the loan. One point typically costs 1% of the loan amount. For example, on a $300,000 loan, one point would be $3,000. Deciding whether to pay points depends on how long you plan to stay in the home. If you plan to live there for many years, the long-term savings from a lower interest rate might outweigh the upfront cost.

- Lender Credits: These are the opposite of points. The lender offers to cover some of your closing costs in exchange for a higher interest rate. This can be beneficial if you have limited cash for closing, but it means you’ll pay more interest over the loan’s term.

Refinancing: When and Why to Consider It

If you already own a home, keeping an eye on current mortgage rates is essential for potential refinancing opportunities. Refinancing involves taking out a new mortgage to pay off your existing one, often to secure a lower interest rate, change the loan term, or convert an ARM to a fixed-rate mortgage.

- Lowering your interest rate: If current rates are significantly lower than your existing mortgage rate, refinancing can lead to substantial savings on monthly payments and total interest paid.

- Changing your loan term: You might refinance from a 30-year to a 15-year loan to pay off your home faster, or vice-versa to reduce monthly payments.

- Accessing home equity (cash-out refinance): Some homeowners use a cash-out refinance to tap into their home equity for large expenses like home renovations or debt consolidation.

A good rule of thumb for considering refinancing is if you can reduce your interest rate by at least 0.75% to 1%, and the savings outweigh the closing costs associated with the new loan.

Seeking Professional Guidance

The mortgage market is complex and constantly evolving. Engaging with a qualified mortgage broker or a knowledgeable loan officer can provide invaluable guidance. These professionals can help you:

- Understand the nuances of different loan products.

- Identify the best loan type for your specific financial situation and goals.

- Navigate the application process efficiently.

- Access a wider range of lenders and potentially better rates.

- Analyze the trade-offs between points and credits.

While online tools are useful for initial research, personalized advice from an expert can save you time, stress, and money in the long run.

The Future Outlook: What to Expect from Mortgage Rates

Predicting the exact trajectory of mortgage rates is challenging, as they are subject to a multitude of economic and geopolitical factors. However, understanding the underlying trends and monitoring key indicators can help you make more informed financial decisions.

Monitoring Economic Forecasts

Staying informed about economic forecasts from reputable sources (e.g., Federal Reserve, major financial institutions, independent economists) can provide insights into potential rate movements. Factors like GDP growth, unemployment rates, global events, and the central bank’s stance on inflation all contribute to the overall economic outlook, which in turn influences mortgage rates. While forecasts are not guarantees, they offer a probabilistic view of future trends.

The Long-Term Trend of Interest Rates

Historically, interest rates have fluctuated, but over the very long term, they tend to reflect the broader economic health and inflation expectations. Understanding this historical context can help temper reactions to short-term volatility. Periods of high inflation often lead to higher rates, while economic slowdowns or recessions can sometimes prompt central banks to lower rates to stimulate borrowing and investment.

Adapting to Market Changes

The most practical approach to the future of mortgage rates is to remain adaptable. If you are planning to buy a home, aim to get pre-approved and be ready to act when rates are favorable for your financial situation. If you are an existing homeowner, regularly assess your mortgage to see if refinancing makes sense, especially during periods of declining rates. The key is not necessarily to “time the market” perfectly, but to be prepared and flexible enough to take advantage of opportunities as they arise, or to mitigate risks when rates are less favorable.

In conclusion, “how much are mortgage rates” is a question with a multi-faceted answer. It’s a blend of global economics, national monetary policy, lender competition, and individual creditworthiness. By educating yourself on these dynamics, actively shopping for the best terms, and strategically managing your financial profile, you can empower yourself to make intelligent decisions that profoundly impact your financial well-being and homeownership journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.