Navigating the landscape of car financing can be a daunting task, with numerous variables influencing the final cost of your vehicle. Among the most critical of these variables is the interest rate—the price you pay for borrowing money. Understanding what constitutes a “good” interest rate on a car loan is not merely about finding the lowest percentage; it’s about grasping the factors that shape these rates, recognizing market benchmarks, and implementing strategies to secure the most favorable terms for your personal financial situation. In an environment where even a small difference in the Annual Percentage Rate (APR) can translate into hundreds, if not thousands, of dollars over the life of a loan, empowering yourself with knowledge is the first step toward a financially savvy purchase. This comprehensive guide will demystify car loan interest rates, equip you with the insights to evaluate offers, and outline actionable steps to drive away with a deal that truly benefits your wallet.

Understanding Car Loan Interest Rates

To truly assess what makes an interest rate “good,” one must first grasp the fundamental mechanics of car loan interest and the myriad elements that contribute to its calculation. It’s more than just a number; it’s a reflection of risk, market conditions, and your financial profile.

What is an Interest Rate?

At its core, an interest rate is the cost of borrowing money, expressed as a percentage of the principal loan amount. For car loans, this is commonly referred to as the Annual Percentage Rate (APR), which encompasses not just the interest charged but also certain fees associated with the loan, providing a more holistic view of the total borrowing cost. When you take out a car loan, the lender provides you with a lump sum to purchase the vehicle, and in return, you agree to repay that principal amount plus interest over a predetermined period. This interest accrues over time, meaning the longer you take to repay the loan, the more interest you will ultimately pay, even if the monthly payments seem lower. A lower APR directly translates to less money spent on interest over the life of the loan, making it the primary target for any discerning borrower.

Factors Influencing Your Interest Rate

Several key factors converge to determine the interest rate you are offered on a car loan, each playing a significant role in how lenders assess the risk associated with lending to you:

- Credit Score: This is arguably the most influential factor. Lenders use your credit score as a snapshot of your creditworthiness and your history of managing debt. Individuals with excellent credit scores (typically 750+) are perceived as low-risk borrowers and thus qualify for the lowest interest rates. Conversely, lower credit scores signal higher risk, leading to higher interest rates to compensate the lender for that increased risk.

- Loan Term: The length of your loan repayment period directly impacts the interest rate. Shorter terms (e.g., 36 or 48 months) generally come with lower interest rates because the lender’s money is tied up for a shorter duration, reducing their exposure to risk. Longer terms (e.g., 60 or 72 months, or even 84 months) often have higher interest rates, although they offer lower monthly payments.

- Down Payment: A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. Consequently, borrowers who put down a substantial down payment are often rewarded with better interest rates.

- New vs. Used Car: Loans for new cars typically carry lower interest rates than those for used cars. This is primarily because new cars retain their value better in the initial years, making them less of a depreciating asset for lenders to secure. Used cars are considered higher risk due to their age, mileage, and potential for unforeseen mechanical issues.

- Lender Type: Different lenders have different risk appetites and pricing structures. Traditional banks, credit unions, online lenders, and dealership financing arms each offer unique rates. Credit unions, for instance, are often known for competitive rates as they are member-owned and not-for-profit.

- Market Conditions: Broader economic factors, such as the prime interest rate set by the Federal Reserve, significantly influence car loan interest rates. When the Fed raises rates, borrowing costs across the board tend to increase, and vice-versa.

Understanding these interconnected factors is crucial for not only evaluating an interest rate offer but also for proactively improving your financial standing before even applying for a loan.

Benchmarking Good Interest Rates in Today’s Market

Defining a “good” interest rate is not a static endeavor; it’s a dynamic assessment that shifts with economic tides and, critically, with an individual’s financial health. While the ideal rate would always be the lowest possible, realistic expectations are shaped by current market averages and one’s personal credit profile.

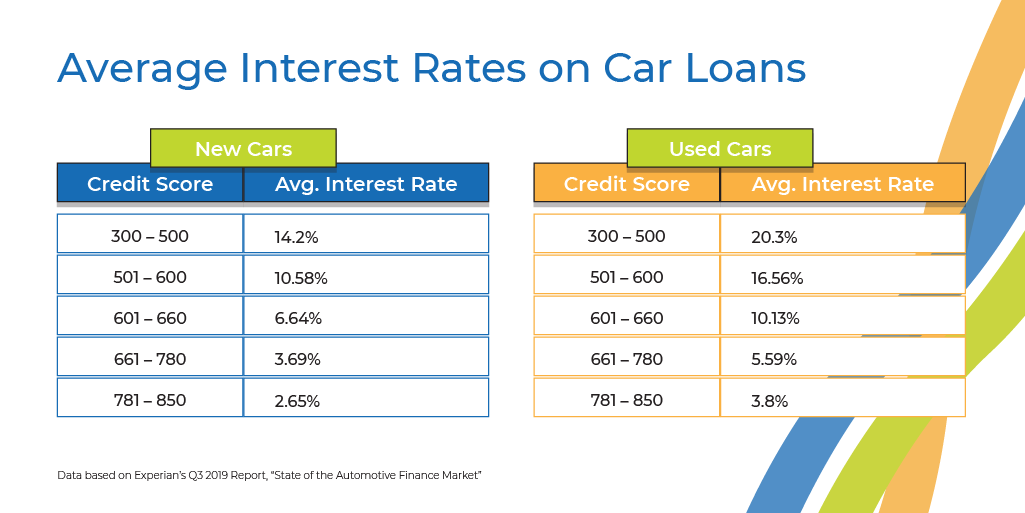

Average Rates by Credit Score Tier

Lenders categorize borrowers into different tiers based on their credit scores, with each tier correlating to a general range of interest rates. These are not rigid boundaries but provide excellent benchmarks:

- Excellent Credit (750+): Borrowers in this tier typically qualify for the lowest available rates, often in the single digits (e.g., 3-6% APR) for new cars, and slightly higher for used cars. This group represents the lowest risk to lenders.

- Good Credit (670-749): While still considered strong, individuals in this range might see rates slightly higher than those with excellent credit, potentially ranging from 5-8% for new cars and 7-10% for used cars.

- Fair Credit (580-669): This tier signifies a moderate risk. Rates here can climb significantly, often ranging from 8-12% for new cars and 10-15% or more for used cars.

- Poor Credit (Below 580): Borrowers with poor credit are considered high risk, and consequently, face the highest interest rates. These can easily reach 15-25% APR, or even higher, particularly for used cars, if they are approved for a loan at all.

It’s important to note that these are averages and can fluctuate based on other factors like the loan term, the lender, and the specific vehicle being financed. However, they serve as a vital guide for understanding where your own potential interest rate might fall.

Impact of Loan Term on Interest Rates

The length of your loan significantly influences both the monthly payment and the interest rate offered. While a longer loan term (e.g., 72 or 84 months) might seem attractive due to lower monthly payments, it typically comes with a higher interest rate and results in paying significantly more in total interest over the life of the loan. Lenders view longer terms as riskier because their capital is tied up for a longer period, increasing the chance of default or depreciation exceeding repayment. Conversely, shorter terms (e.g., 36 or 48 months) usually command lower interest rates, resulting in less overall interest paid, but demand higher monthly payments. A “good” interest rate should ideally be paired with a loan term that aligns with your budget without unduly inflating the total cost of the vehicle.

New vs. Used Car Loan Rate Differences

There’s a consistent disparity between interest rates for new and used car loans, with new car loans almost universally offering lower rates. This difference is largely due to the lower depreciation risk associated with new vehicles for lenders. A new car generally holds more of its value in the initial years, making it a more secure asset for the lender to reclaim if a borrower defaults. Used cars, by contrast, have already undergone significant depreciation, and their future value is less predictable, especially as they age or accumulate mileage. This higher inherent risk for used cars translates into higher interest rates to offset the potential loss for the lender. Therefore, when benchmarking a “good” rate, it’s crucial to distinguish between whether you’re financing a new or a used vehicle, as the acceptable range for each will vary considerably.

Strategies to Secure a Better Car Loan Rate

Securing a favorable interest rate isn’t solely dependent on your current financial standing; it also hinges on proactive strategies and informed decision-making. By taking deliberate steps before and during the loan application process, you can significantly improve your chances of getting a “good” rate.

Improve Your Credit Score

Your credit score is the most powerful determinant of your interest rate. Even modest improvements can move you into a better rate tier. Before applying for a car loan, access your credit report from the three major bureaus (Equifax, Experian, TransUnion) and review them for errors. Dispute any inaccuracies, as these can negatively impact your score. Focus on paying all your bills on time, as payment history is the largest factor in credit scoring. Reduce existing debt, especially high-interest credit card balances, to lower your credit utilization ratio, another key factor. Avoid opening new credit accounts just before applying for a car loan, as this can temporarily lower your score. Giving yourself a few months to clean up and build your credit can pay dividends in the form of a significantly lower interest rate.

Save for a Larger Down Payment

A larger down payment directly reduces the amount of money you need to borrow, which, from a lender’s perspective, lowers their risk. The less money they lend, the less they stand to lose if you default. Consequently, lenders are often willing to offer lower interest rates to borrowers who make substantial down payments. Aim for at least 10-20% of the vehicle’s purchase price for a new car and potentially more for a used car, where depreciation is more pronounced. A significant down payment also means you’ll reach an equity position (owing less than the car is worth) sooner, protecting you from being “upside down” on your loan.

Shop Around for Lenders

Never accept the first loan offer you receive, especially from a dealership. Dealerships often mark up interest rates to increase their profit. It is highly advisable to get pre-approved for a loan from multiple financial institutions before you even set foot in a dealership. Explore options from:

- Traditional Banks: Large national and regional banks offer a range of auto loan products.

- Credit Unions: Often provide some of the most competitive rates due to their non-profit, member-owned structure.

- Online Lenders: Companies like LightStream, Capital One, and others specialize in online lending and can offer quick approvals and competitive rates.

Comparing pre-approvals allows you to arrive at the dealership with leverage. If the dealership offers a better rate, great; if not, you already have a strong offer in hand to fall back on or use as a bargaining chip. Multiple loan inquiries within a short period (typically 14-45 days, depending on the credit model) are usually treated as a single inquiry, minimizing the impact on your credit score, so shop around confidently.

Consider a Co-signer

If your credit score is fair or poor, or if you’re a young borrower with a limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a much lower interest rate. A co-signer legally agrees to be responsible for the loan repayment if you default, thereby reducing the lender’s risk. However, this is a significant commitment for the co-signer, as the loan will appear on their credit report and any late payments will affect their score. Ensure you and your co-signer fully understand the implications before proceeding.

Negotiate the Car Price Separately

When you’re at the dealership, it’s crucial to negotiate the car’s purchase price independently of the financing. Many dealerships try to distract buyers with monthly payment figures, which can obscure the true cost of the vehicle and the interest rate. By agreeing on the vehicle’s price first, you ensure you’re getting a fair deal on the car itself. Only after the car price is locked in should you discuss financing options, using your pre-approved loan offers as a baseline. This two-step approach prevents you from overpaying on either the car or the loan interest.

Beyond the Interest Rate: Total Cost of Ownership

While a good interest rate is paramount, it’s only one piece of the puzzle when evaluating the true cost of your car loan and, by extension, your vehicle. Focusing solely on the APR without considering other elements can lead to unforeseen financial strain down the road.

Understanding the Total Loan Cost

The total cost of your car loan extends far beyond the principal amount you borrowed. It encompasses the principal plus all the interest you will pay over the entire loan term. A lower interest rate certainly reduces this total, but the loan term plays an equally critical role. For example, a 60-month loan at 5% APR will accumulate significantly more interest than a 36-month loan at the same 5% APR, simply because the interest has more time to accrue. Always ask for the total amount you will pay over the life of the loan before signing, as this provides the clearest picture of your financial commitment. This total cost is what ultimately matters for your long-term financial health.

Impact of Loan Term on Total Interest Paid

It’s a common misconception that lower monthly payments from longer loan terms are always financially beneficial. While they can ease immediate budget constraints, they invariably lead to paying substantially more in total interest. Consider a $30,000 car loan at 6% APR:

- 36-month term: Monthly payment around $913, total interest paid approx. $2,870.

- 60-month term: Monthly payment around $579, total interest paid approx. $4,740.

- 72-month term: Monthly payment around $498, total interest paid approx. $5,850.

As illustrated, extending the loan term by 36 months (from 36 to 72 months) to reduce the monthly payment by $415 nearly doubles the total interest paid. A truly “good” interest rate is one that allows for a loan term you can comfortably manage without incurring excessive interest over time. Prioritizing the shortest possible loan term that fits your budget is often the most financially prudent choice.

Hidden Costs and Fees

Beyond the interest rate and principal, car loans can sometimes come with various fees that add to the overall cost. While some are legitimate and unavoidable (e.g., title and registration fees), others might be negotiable or even questionable. Be vigilant about:

- Origination Fees: A fee charged by the lender for processing the loan.

- Documentation Fees (Doc Fees): Charged by the dealership for processing paperwork. These can vary widely by state and dealership and are often negotiable.

- Prepayment Penalties: Some loans charge a fee if you pay off your loan early. Always check for this clause.

- Add-ons and Extended Warranties: While not strictly loan fees, these are often bundled into the financing and inflate the principal amount, thereby increasing the total interest paid. Evaluate them separately from the car purchase.

Always scrutinize the fine print of your loan agreement and ask for a complete breakdown of all fees. Understand what each fee is for and if it’s genuinely necessary.

The Importance of a Budget

Ultimately, the best car loan—with a “good” interest rate and manageable terms—is one that fits comfortably within your overall budget. Before you even start shopping for a car or a loan, create a detailed budget that accounts for not just the monthly car payment, but also insurance, fuel, maintenance, and potential parking fees. The “20/4/10 rule” is a useful guideline: put down at least 20%, finance for no more than four years, and keep your total monthly car expenses (payment, insurance, fuel) under 10% of your gross income. A car loan with a low interest rate is only “good” if you can afford it without jeopardizing other essential financial goals or daily living expenses.

When to Refinance Your Car Loan

Securing a favorable interest rate at the outset is ideal, but market conditions and your personal financial situation can change. If you’re currently paying a higher interest rate, refinancing your car loan can be a powerful tool to lower your monthly payments, reduce the total interest paid, or even adjust your loan term.

Signs You Could Benefit from Refinancing

Refinancing involves taking out a new loan to pay off your existing car loan, ideally with better terms. Here are key indicators that refinancing might be a wise move:

- Your Credit Score Has Improved: If your credit score has significantly increased since you first took out the loan (e.g., you’ve moved from “fair” to “good” or “good” to “excellent”), you’re likely eligible for a much lower interest rate than you initially received.

- Market Interest Rates Have Dropped: If general interest rates have fallen since you financed your car, you might be able to secure a new loan at a lower APR.

- Your Income Has Increased, or Debt Has Decreased: A stronger financial position makes you a more attractive borrower, potentially qualifying you for better terms.

- You Want a Lower Monthly Payment: While extending the loan term to lower payments can increase total interest, if your current payments are a significant strain, refinancing with a longer term at a lower rate could provide necessary relief, especially if you plan to make extra payments when possible.

- You Want to Pay Off Your Loan Faster: Conversely, if you want to pay off your car faster, you might refinance to a shorter term at a lower rate, leading to higher monthly payments but significant savings in total interest.

- You Have a High-Interest Rate: If your initial interest rate was very high due to poor credit at the time, refinancing is almost always worth exploring once your financial health improves.

The Refinancing Process

Refinancing a car loan is similar to applying for the initial loan:

- Check Your Current Loan Details: Gather information on your current lender, remaining balance, interest rate, and payoff amount.

- Review Your Credit Report: Ensure your credit score is in good standing and address any errors.

- Shop Around for Lenders: Just like with your original loan, compare offers from banks, credit unions, and online lenders. Get multiple quotes to find the best APR.

- Submit Applications: Provide the necessary documentation (proof of income, current loan details, vehicle information).

- Compare Offers and Choose: Select the new loan that offers the most advantageous terms. Pay attention to the new APR, loan term, and any fees associated with the new loan.

- Finalize the New Loan: The new lender will pay off your old loan, and you’ll begin making payments to your new lender.

Refinancing can be a simple yet effective strategy to optimize your car financing, ensuring that your interest rate remains “good” even as market conditions and your personal finances evolve. By proactively managing your car loan, you maintain control over one of your significant financial obligations.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.