Understanding how interest is calculated on a car loan is a fundamental aspect of personal finance, empowering you to make informed decisions and manage your budget effectively. While numerous online calculators and lender statements automate this process, knowing how to manually crunch the numbers provides invaluable insight. It demystifies the lending process, helps you verify figures, and equips you with the knowledge to potentially save money over the life of your loan. This guide will walk you through the precise steps to calculate car loan interest manually, enhancing your financial literacy and giving you a clearer picture of your automotive investment.

Understanding the Fundamentals of Car Loan Interest

Before diving into the actual calculations, it’s crucial to grasp the core concepts that dictate how much you pay for the privilege of borrowing money. These terms are the building blocks of any loan agreement, and a solid understanding of each will make the manual calculation process much clearer.

What is Interest?

At its simplest, interest is the cost of borrowing money. When you take out a car loan, a lender provides you with a sum of money (the principal) to purchase a vehicle. In return for this service, you agree to pay back the principal amount plus an additional fee – the interest. This fee compensates the lender for the risk and the opportunity cost of lending you money that could otherwise be earning them a return elsewhere. For car loans, interest is typically calculated as a percentage of the outstanding principal balance.

Key Loan Terms You Need to Know

Several specific terms define the structure and cost of your car loan. Familiarizing yourself with these is the first step towards manual calculation:

- Principal (P): This is the initial amount of money you borrow to buy the car. If you make a down payment or trade in an old vehicle, the principal will be the total cost of the car minus these contributions.

- Interest Rate (i/r): Expressed as a percentage, this is the rate at which the lender charges you for borrowing the principal. Car loan interest rates are almost always quoted annually.

- Annual Percentage Rate (APR): The APR is a broader measure of the cost of borrowing money. It includes the interest rate plus any other fees associated with the loan (e.g., origination fees). For car loans, the quoted interest rate often closely aligns with the APR, but it’s important to confirm. When calculating manually, you’ll typically convert the annual APR into a monthly interest rate.

- Loan Term (n): This refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term generally means lower monthly payments but results in paying more total interest over the life of the loan.

Why Calculate Manually?

In an age of digital convenience, one might wonder why bother with manual calculations. The reasons are compelling:

- Empowerment and Understanding: It demystifies the financial process, allowing you to truly understand how your money is being allocated each month between principal and interest.

- Verification: You can cross-reference your lender’s statements or online calculator results, ensuring accuracy and catching potential errors.

- Informed Decision-Making: By understanding the mechanics, you can better evaluate different loan offers, assess the impact of a larger down payment, or determine the savings from an early payoff.

- Budgeting Confidence: Knowing exactly how much of your payment goes to interest versus principal provides a clearer picture for personal financial planning.

The Essential Formula: Simple Interest vs. Amortization

Most car loans use a method called simple interest, but it’s applied within an amortization schedule. This means interest is calculated only on the remaining principal balance, and your payments are structured to pay off the loan completely over a set period.

Simple Interest Explained

Simple interest for car loans is calculated on the outstanding principal balance. Unlike some other forms of debt where interest might compound on previously accrued interest, car loans typically apply simple interest daily or monthly. Each time you make a payment, a portion goes to cover the interest accrued since your last payment, and the remainder goes towards reducing the principal. As the principal balance decreases, the amount of interest accrued in subsequent periods also decreases.

The Amortization Schedule Concept

An amortization schedule is essentially a table that details each payment made over the life of a loan, showing how much of each payment is allocated to interest and how much to principal, and the remaining loan balance after each payment. In the early stages of a car loan, a larger portion of your monthly payment goes towards interest. As the loan matures and the principal balance decreases, a greater percentage of each payment is applied to the principal.

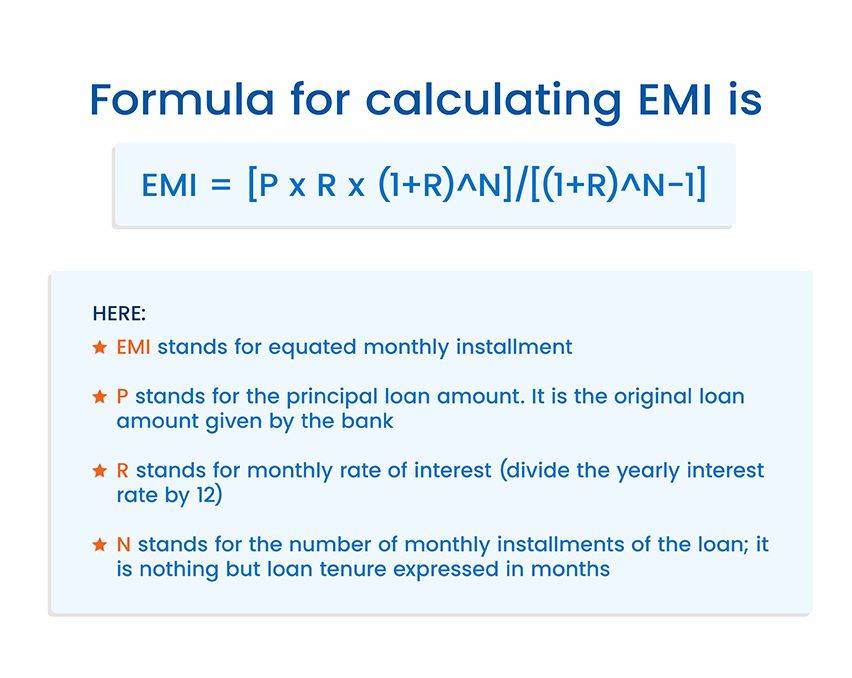

The Monthly Payment Formula

Calculating your fixed monthly car loan payment is the cornerstone of manual interest calculation. The standard formula for an amortizing loan is:

$$ M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1] $$

Where:

- M = Your monthly loan payment

- P = Principal loan amount (the initial amount borrowed)

- i = Your monthly interest rate (annual APR divided by 12 and then by 100 for decimal)

- n = Total number of payments over the loan’s term (loan term in years multiplied by 12)

Let’s break down the variables with an example for calculation:

Suppose you borrow $25,000 for a new car.

Your APR is 6%.

Your loan term is 60 months (5 years).

- P = $25,000

- i = 6% APR / 12 months / 100 = 0.06 / 12 = 0.005 (This is your monthly interest rate as a decimal)

- n = 60 months

Plugging these into the formula:

$$ M = 25000 [ 0.005(1 + 0.005)^{60} ] / [ (1 + 0.005)^{60} – 1] $$

$$ M = 25000 [ 0.005(1.005)^{60} ] / [ (1.005)^{60} – 1] $$

First, calculate $ (1.005)^{60} $: This equals approximately $ 1.34885015 $.

Now substitute this back:

$$ M = 25000 [ 0.005 * 1.34885015 ] / [ 1.34885015 – 1] $$

$$ M = 25000 [ 0.00674425075 ] / [ 0.34885015 ] $$

$$ M = 168.60626875 / 0.34885015 $$

$$ M approx 483.20 $$

So, your estimated monthly payment would be approximately $483.20. This is a crucial number to determine before moving to the amortization schedule.

Step-by-Step Manual Calculation Process

Once you understand the basic terms and have calculated your monthly payment, you can begin to build an amortization schedule manually for a few months to see how the interest and principal components change.

Gather Your Loan Information

Before you start, ensure you have all the necessary details:

- Principal (P): The total amount borrowed.

- Annual Percentage Rate (APR): The yearly interest rate.

- Loan Term (n): The total number of months for the loan.

Using our example: P = $25,000, APR = 6%, n = 60 months.

Convert APR to Monthly Interest Rate

As established earlier, you need the monthly interest rate as a decimal for calculations.

Monthly Interest Rate (i) = APR / 12 / 100

Example: 6% / 12 / 100 = 0.005

Calculate Your Monthly Payment

As demonstrated in the previous section, use the monthly payment formula to determine your fixed monthly payment.

Example: Our calculated monthly payment (M) is $483.20.

Constructing an Amortization Schedule (First Few Months)

Now, let’s manually build a mini-amortization schedule. This shows how each payment is broken down.

Month 1:

- Starting Balance: $25,000.00

- Interest Portion: Starting Balance * Monthly Interest Rate

- $25,000.00 * 0.005 = $125.00

- Principal Portion: Monthly Payment – Interest Portion

- $483.20 – $125.00 = $358.20

- Ending Balance: Starting Balance – Principal Portion

- $25,000.00 – $358.20 = $24,641.80

Month 2:

- Starting Balance: $24,641.80 (This is the ending balance from Month 1)

- Interest Portion: Starting Balance * Monthly Interest Rate

- $24,641.80 * 0.005 = $123.21 (Notice it’s slightly less than Month 1)

- Principal Portion: Monthly Payment – Interest Portion

- $483.20 – $123.21 = $359.99

- Ending Balance: Starting Balance – Principal Portion

- $24,641.80 – $359.99 = $24,281.81

Month 3:

- Starting Balance: $24,281.81

- Interest Portion: $24,281.81 * 0.005 = $121.41

- Principal Portion: $483.20 – $121.41 = $361.79

- Ending Balance: $24,281.81 – $361.79 = $23,920.02

You can continue this process for all 60 months, though it becomes tedious. This demonstrates clearly how with each payment, the interest portion decreases, and consequently, the principal portion increases.

Calculating Total Interest Paid

To calculate the total interest you will pay over the life of the loan, it’s simpler once you have your monthly payment:

- Total Paid: Monthly Payment * Total Number of Payments

- $483.20 * 60 = $28,992.00

- Total Interest Paid: Total Paid – Principal Loan Amount

- $28,992.00 – $25,000.00 = $3,992.00

So, on a $25,000 car loan at 6% APR over 60 months, you would pay approximately $3,992.00 in interest.

Beyond the Basics: What Affects Your Interest Payments?

Understanding the manual calculation process naturally leads to insights into how different factors can significantly impact the total interest you pay.

The Impact of Interest Rate (APR)

This is perhaps the most obvious factor. A lower APR directly translates to less interest paid over the life of the loan. Even a small difference, say from 6% to 5%, can save you hundreds or even thousands of dollars. Your credit score is the primary determinant of the interest rate you qualify for, emphasizing the importance of maintaining good credit.

The Role of Loan Term

While a longer loan term (e.g., 72 months instead of 60) reduces your monthly payment, it almost always leads to paying more total interest. This is because the principal takes longer to pay down, giving more time for interest to accrue.

- Example (same $25,000 at 6% APR but for 72 months):

- Monthly payment would drop to approximately $414.07.

- Total paid: $414.07 * 72 = $29,812.84

- Total interest: $29,812.84 – $25,000 = $4,812.84

Notice that a 12-month extension added over $800 in total interest paid, despite a lower monthly payment.

Down Payments and Trade-ins

Making a larger down payment or trading in a vehicle reduces the principal amount you need to borrow. A smaller principal directly results in less interest accrued over the loan’s term, regardless of the interest rate or loan term. This is one of the most effective ways to save on interest.

Early Payoff Strategies

Because car loan interest is calculated on the outstanding principal balance, paying off your loan faster than scheduled can save you a significant amount of interest. Any extra payment you make that is specifically designated to reduce the principal will immediately lower the balance on which future interest is calculated. This is why making even small additional principal payments can be beneficial.

Benefits and Limitations of Manual Calculation

While the process of manually calculating interest is empowering, it’s also important to acknowledge its practicalities.

Empowering Financial Literacy

The primary benefit is the profound understanding it grants. You move from passively accepting numbers to actively comprehending their origin. This boosts your confidence in financial discussions and helps you scrutinize loan offers more effectively. It’s a foundational skill for managing personal debt.

Verifying Lender Calculations

Mistakes can happen, even with automated systems. Manually checking your loan’s details, especially the monthly payment and the interest portion of early payments, can help you identify any discrepancies. This ensures you’re not overpaying due to a clerical error or misunderstanding.

Planning and Budgeting

Armed with the knowledge of how your payments are structured, you can better plan your budget. You’ll understand how extra payments impact your loan, helping you strategize for an early payoff or allocate funds more efficiently. It makes financial planning more concrete and less abstract.

Time and Complexity

The most significant limitation is the time and mathematical precision required. For a 60-month loan, manually constructing the full amortization schedule is a monumental task prone to human error. This is precisely why financial calculators and software exist. The goal of manual calculation isn’t to replace these tools for every single instance, but rather to understand the underlying mechanics so you can use those tools intelligently and verify their results. For quick estimates or checking the first few payments, manual calculation is highly effective.

In conclusion, knowing how to manually calculate the interest on a car loan is a valuable skill in your financial toolkit. It strips away the complexity of lending, providing a clear window into how your money works for and against you. While digital tools offer convenience, the intellectual exercise of manual calculation fosters deeper financial literacy, allowing you to confidently manage your car loan and make smarter financial decisions for your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.