In the landscape of personal finance and civic responsibility, few documents hold as much significance as the income tax return. Often perceived as a complex, annual chore, an income tax return is, in essence, a formal declaration submitted to a tax authority (like the IRS in the United States, HMRC in the UK, or ATO in Australia) that reports an individual’s or entity’s income, expenses, and other relevant financial information for a specific tax year. Far from being a mere bureaucratic exercise, understanding and accurately filing your income tax return is a cornerstone of sound financial management, impacting everything from your annual budget to your long-term financial stability.

This comprehensive guide will demystify the income tax return, delving into its fundamental purpose, key components, the filing process, and its broader implications for your financial well-being. Whether you’re a first-time filer or looking to deepen your understanding, grasping the intricacies of this vital document is indispensable for navigating the modern financial world.

Understanding the Fundamentals of an Income Tax Return

At its heart, an income tax return is a communication tool between taxpayers and the government. It’s how you inform the tax authorities about your financial activities over the past year, enabling them to assess your tax liability or determine if you are due a refund.

The Core Definition

An income tax return is an official document or set of forms that taxpayers use to report their taxable income, calculate their tax liability, and declare any tax payments already made (such as through payroll withholdings or estimated tax payments). It is the mechanism by which individuals and businesses comply with tax laws, ensuring they contribute their fair share to public services and infrastructure. The information provided typically includes gross income, deductions, credits, and capital gains or losses, culminating in a net tax owed or an overpayment to be refunded.

Who Needs to File?

The requirement to file an income tax return isn’t universal for every individual. Generally, filing is mandatory if your gross income exceeds a certain threshold, which varies based on factors such as your age, filing status (e.g., single, married filing jointly, head of household), and whether you are self-employed. Even if your income is below the filing threshold, you might still choose to file. This is particularly relevant if you had taxes withheld from your paychecks or made estimated tax payments, as filing is the only way to receive a refund for any overpaid taxes or to claim certain refundable tax credits. For example, individuals eligible for credits like the Earned Income Tax Credit (EITC) or the Child Tax Credit often need to file a return to receive these benefits, even if they owe no tax.

Why Filing is Crucial

Filing an income tax return is crucial for several compelling reasons beyond mere compliance. Firstly, it ensures you meet your legal obligations and avoid penalties, interest, and potential legal issues from tax authorities. Secondly, it is the pathway to receiving any tax refunds you are owed, which can significantly boost your personal finances. Thirdly, an accurate tax return can be vital for demonstrating your income for various financial purposes, such as applying for loans, mortgages, or financial aid. It serves as an official record of your earnings and financial standing. Moreover, for many, tax returns are an opportunity to reduce their overall tax burden through eligible deductions and credits, effectively optimizing their financial outflow.

Navigating the Components of Your Tax Return

An income tax return is a structured document, comprising various sections that meticulously detail your financial year. Understanding these components is key to accurate filing and maximizing your financial position.

Essential Information Required

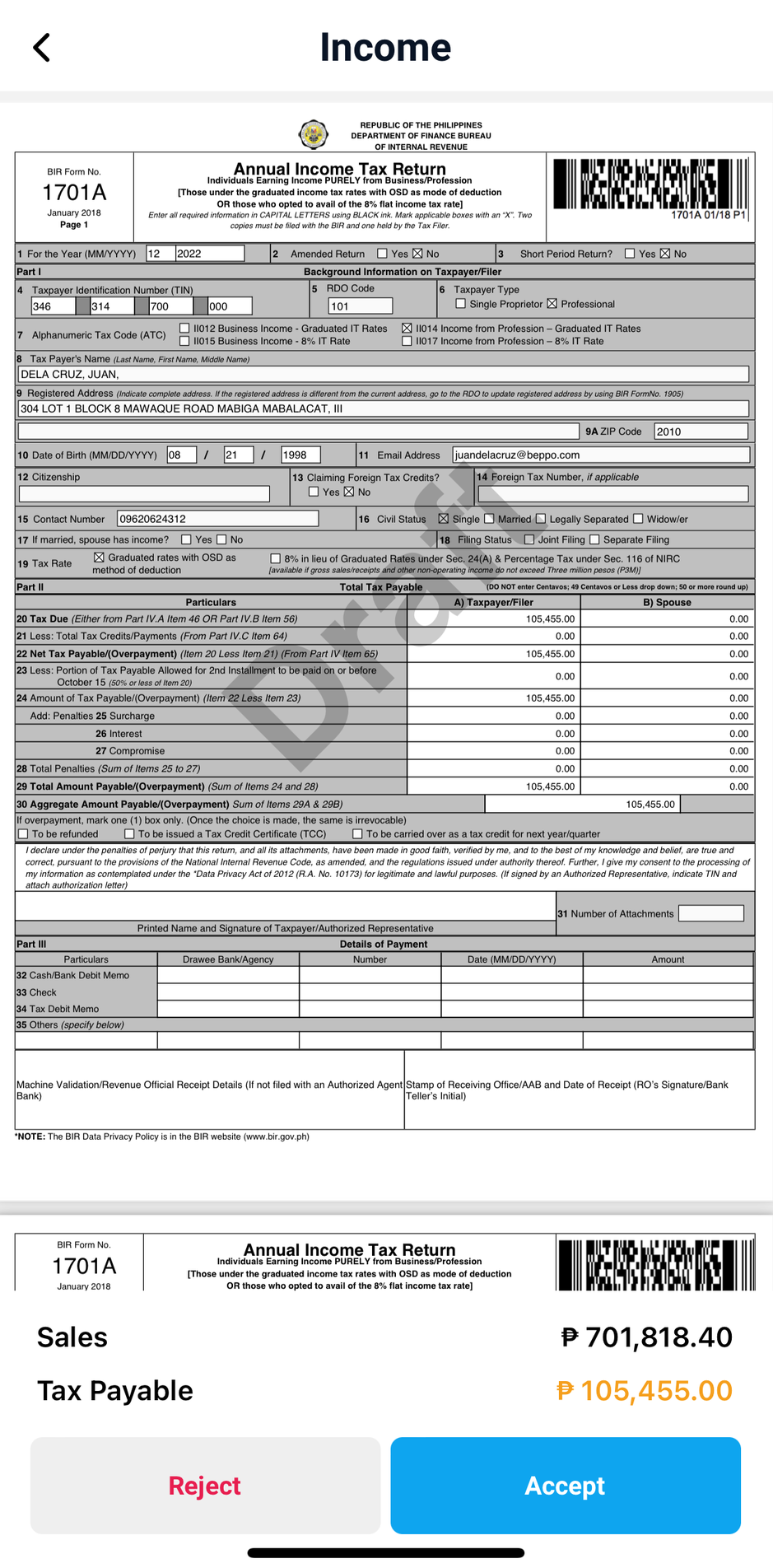

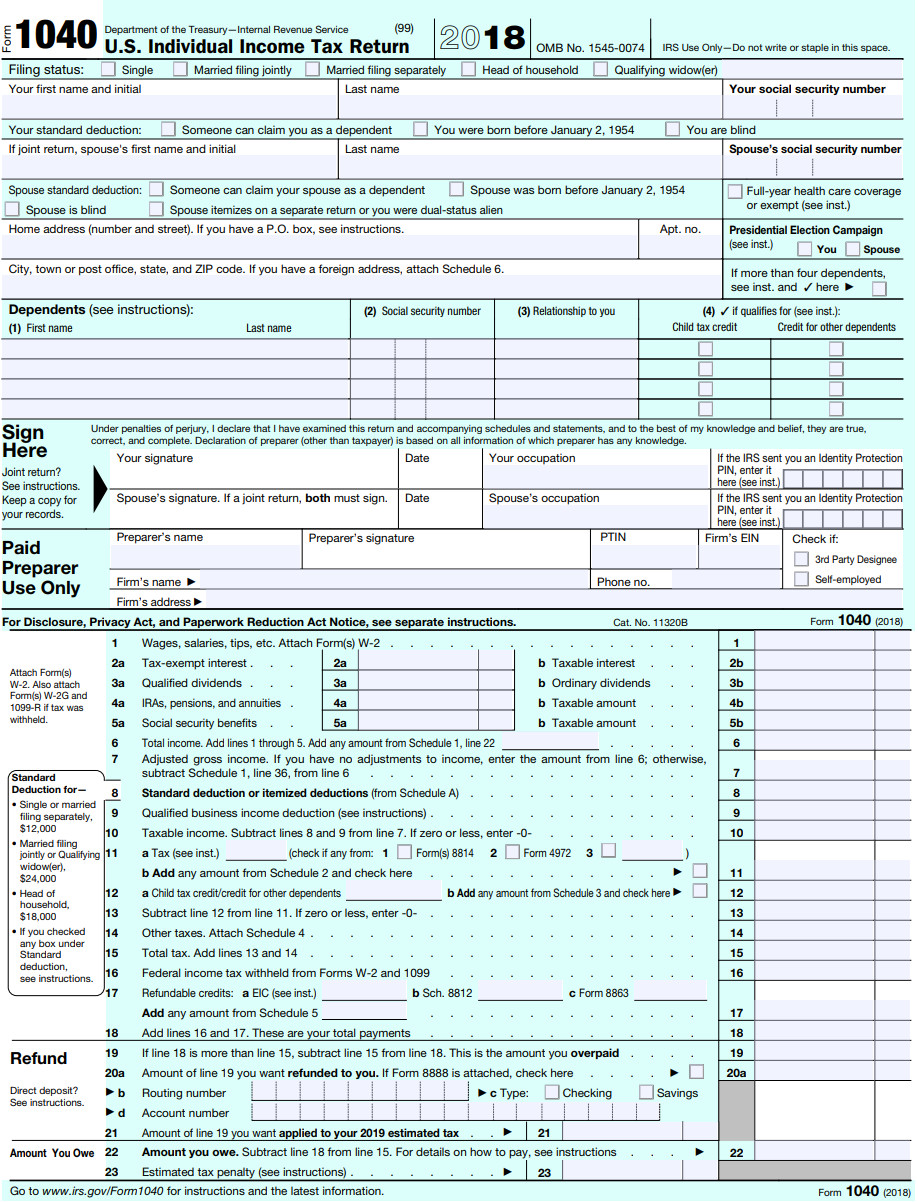

Before diving into numbers, every tax return requires fundamental personal information. This includes your full name, Social Security number (or equivalent taxpayer identification number), date of birth, and current address. Your filing status is also critical as it dictates your standard deduction amount, tax rates, and eligibility for certain credits. Common filing statuses include Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Widow(er). Accurately selecting your filing status can have a substantial impact on your tax liability.

Income Sources to Report

The core of an income tax return revolves around reporting all sources of taxable income earned throughout the year. This isn’t just limited to your salary from a primary job. Common income sources include:

- Wages, Salaries, and Tips: Typically reported on Form W-2.

- Self-Employment Income: Earnings from freelance work, independent contracting, or running a business, often reported on Schedule C.

- Interest and Dividends: Income earned from savings accounts, bonds, stocks, and mutual funds, usually reported on Forms 1099-INT and 1099-DIV.

- Rental Income: Earnings from rental properties, reported on Schedule E.

- Capital Gains/Losses: Profits or losses from selling investments like stocks or real estate, reported on Schedule D.

- Retirement Income: Distributions from pensions, IRAs, and 401(k)s, usually on Form 1099-R.

- Alimony (for certain agreements), unemployment benefits, and even gambling winnings.

It’s imperative to report all taxable income to avoid discrepancies that could lead to audits or penalties.

Deductions, Credits, and Their Impact

This is where strategic tax planning often comes into play. Deductions and credits are mechanisms designed to reduce your overall tax burden, but they function differently.

- Deductions reduce your taxable income. For example, if you have a taxable income of $70,000 and qualify for $10,000 in deductions, your taxable income becomes $60,000. Deductions can be standard (a fixed amount based on your filing status) or itemized (specific expenses like mortgage interest, state and local taxes, or medical expenses that exceed a certain threshold). You generally choose whichever provides a greater tax benefit.

- Credits directly reduce your tax liability (the actual amount of tax you owe) dollar-for-dollar. A $1,000 tax credit means $1,000 less in taxes paid. Some credits are non-refundable, meaning they can reduce your tax liability to zero but won’t result in a refund if the credit exceeds your tax owed. Others are refundable, meaning if the credit amount is more than your tax liability, you get the difference back as a refund. Examples include the Child Tax Credit, Earned Income Tax Credit, and education credits.

Strategically utilizing eligible deductions and credits is a cornerstone of effective personal finance and can significantly impact your net refund or tax payment.

Understanding Your Tax Liability or Refund

After reporting all income and applying deductions and credits, your tax return calculates your final tax liability. This amount is then compared to any taxes you’ve already paid throughout the year (e.g., through payroll withholdings or estimated tax payments). If the taxes paid exceed your liability, you’re due a refund. If your liability is greater than what you’ve paid, you owe additional tax to the government. This final calculation is the ultimate outcome of your income tax return and dictates whether money flows from you to the government, or vice-versa.

The Process of Filing Your Income Tax Return

Filing an income tax return can seem daunting, but breaking it down into manageable steps makes the process straightforward.

Gathering Your Documents

Preparation is paramount. Before you even begin filling out forms, compile all necessary documents. This typically includes:

- Income Statements: W-2s from employers, 1099-MISC or 1099-NEC for self-employment, 1099-INT for interest income, 1099-DIV for dividends, 1099-R for retirement distributions, and Schedule K-1s for partnership or S-corp income.

- Deduction and Credit Documentation: Mortgage interest statements (Form 1098), property tax records, receipts for charitable contributions, medical expense records, education expense forms (1098-T), and child care statements.

- Previous Year’s Tax Return: Often useful for reference, especially for carrying over losses or checking past deductions.

- Personal Information: Social Security numbers for yourself, spouse, and dependents.

Organizing these documents beforehand saves time and reduces the likelihood of errors.

Choosing Your Filing Method (Software, Professional, Manual)

Taxpayers have several options for filing their returns:

- Tax Software/Online Services: Popular choices like TurboTax, H&R Block, and TaxAct offer user-friendly interfaces that guide you through the process, often with step-by-step questions. Many even offer free filing options for simple returns or those below certain income thresholds. This method is generally cost-effective and efficient.

- Tax Professional: Hiring an accountant, enrolled agent, or tax preparer is ideal for individuals with complex tax situations (e.g., significant self-employment income, investments, foreign income, or intricate deductions). Professionals can offer personalized advice, ensure compliance, and often identify deductions or credits you might overlook.

- Manual Filing (Paper Forms): While less common today, it’s still possible to download and print tax forms from the tax authority’s website and fill them out by hand. This method requires a meticulous understanding of tax laws and calculations and is the slowest method for processing refunds.

The best method depends on the complexity of your financial situation, your comfort level with tax laws, and your budget.

Key Deadlines and Extensions

Tax deadlines are non-negotiable. In many countries, the primary filing deadline for individual income tax returns for the previous calendar year falls in mid-April (e.g., April 15th in the U.S.). For those who need more time, an extension can usually be filed, typically granting an additional six months to submit the return. However, it’s crucial to remember that an extension to file is not an extension to pay. If you anticipate owing taxes, you must pay an estimate by the original deadline to avoid penalties and interest, even if you’re filing an extension for the return itself. Missing deadlines without an extension can lead to significant financial penalties.

What Happens After You File?

Once your tax return is submitted, the tax authority reviews it. If you filed electronically, you’ll usually receive an immediate confirmation that your return has been received. If you’re due a refund, it will typically be issued within a few weeks, especially if you opted for direct deposit. If you owe tax, you’ll need to ensure your payment reaches the tax authority by the deadline. It’s advisable to keep copies of your filed return and all supporting documents for at least three years, or longer for certain types of records, in case of an audit or needing to amend a past return.

Common Mistakes to Avoid and Best Practices for Filing

Even experienced filers can make mistakes. Being aware of common pitfalls and adopting best practices can streamline the process and safeguard your financial interests.

Preventing Errors and Omissions

The most frequent mistakes include mathematical errors, incorrect Social Security numbers, selecting the wrong filing status, or simply forgetting to sign the return. Omitting income, even small amounts from less obvious sources like bank interest, can trigger flags. Double-check all figures, especially those transferred from income statements. Review all personal details carefully. Using tax software can significantly reduce mathematical errors as it performs calculations automatically.

Maintaining Accurate Records

The golden rule of tax filing is excellent record-keeping. Keep all W-2s, 1099s, receipts for deductions, charitable donation records, and any other financial statements organized throughout the year. Digital copies are often easier to manage and store securely. This habit not only simplifies the filing process but also provides robust support in the unlikely event of an audit. Consider creating a dedicated tax folder, either physical or digital, where you consistently store relevant documents.

The Benefits of Early Preparation

Don’t wait until the last minute. Starting early provides ample time to gather documents, research eligible deductions and credits, and seek professional help if needed. Early filing also means quicker refunds for those who are due one. It reduces stress and allows for a more thoughtful, error-free submission. Moreover, if you find you owe taxes, filing early gives you more time to plan how to make that payment without financial strain.

Seeking Professional Guidance

While tax software is excellent for many, never hesitate to consult a qualified tax professional if your situation is complex or if you’re unsure about specific tax laws. The cost of a professional can often be offset by the money saved through their expertise in identifying overlooked deductions or credits, preventing costly errors, and offering strategic tax planning advice. They can provide invaluable peace of mind and help you navigate intricate financial landscapes.

The Broader Impact of Income Tax Returns on Personal Finance

Beyond the immediate act of filing, the income tax return holds a significant position within the broader context of personal finance. It’s not just about compliance; it’s about empowerment and strategic financial planning.

Financial Planning and Budgeting Insights

Your annual income tax return provides a detailed snapshot of your financial year. By reviewing your return, you can gain valuable insights into your spending habits, income streams, and tax efficiency. For example, if you consistently receive a large refund, it might indicate that too much tax is being withheld from your paychecks, essentially giving the government an interest-free loan throughout the year. Adjusting your W-4 (or equivalent) can put more money in your pockets monthly, which can be better utilized for savings, investments, or debt repayment. Conversely, if you consistently owe a significant amount, it might signal a need to adjust your withholdings or make estimated tax payments to avoid future penalties. This annual financial review is a powerful tool for improving your budgeting and overall financial planning.

Accessing Financial Opportunities

An accurately filed income tax return serves as an official record of your income, which is often a prerequisite for various financial opportunities. When applying for a mortgage, a car loan, or even certain government benefits, lenders and agencies typically require copies of your past tax returns to verify your income and financial stability. Without properly filed returns, you might face challenges in accessing these crucial financial products, potentially hindering your ability to achieve major life goals like homeownership or funding higher education.

Contributing to Public Services

Finally, it’s important to remember the civic dimension of income tax returns. The taxes collected through this process are the lifeblood of public services that benefit everyone. From funding schools, hospitals, and infrastructure projects (roads, bridges) to supporting national defense and social safety nets, income taxes contribute directly to the functioning of society. Understanding “what is an income tax return” therefore extends beyond personal financial management to an appreciation of its vital role in collective well-being and the social contract between citizens and their government.

In conclusion, an income tax return is a multifaceted financial document that is far more than just a form. It’s a tool for compliance, a record of financial activity, an opportunity for financial optimization, and a contribution to the broader societal good. By approaching it with diligence, understanding, and proactive planning, individuals can transform this annual obligation into a powerful component of their personal financial strategy, ensuring both fiscal responsibility and personal prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.