The phrase “getting a tax return” often conjures images of a welcome refund check arriving in the mail or a direct deposit hitting your bank account. For many, it’s an annual financial event, a moment of relief or even excitement. However, the process itself, from understanding your obligations to navigating the complexities of tax law, can feel daunting. This comprehensive guide aims to demystify the journey of filing your tax return, explaining what it entails, how to approach it efficiently, and how to maximize your financial outcomes. Whether you’re a first-time filer or looking to streamline your annual ritual, understanding the fundamentals is the first step towards a successful and potentially rewarding tax season.

Understanding the Fundamentals of Tax Returns

Before diving into the “how-to,” it’s crucial to grasp the basic concepts surrounding tax returns. This foundational knowledge will empower you to make informed decisions and approach the process with confidence.

What Exactly Is a Tax Return?

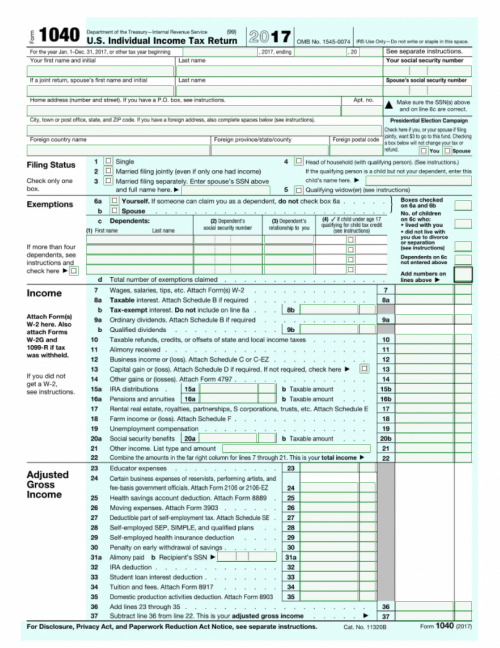

At its core, a tax return is a form filed with a tax authority (like the IRS in the United States) that reports your income, expenses, and other relevant financial information. Based on this data, the government determines how much tax you owe for the year. This isn’t just about paying taxes; it’s also how you claim any tax refunds you might be due, report changes in your financial situation, and ensure compliance with tax laws. It’s an annual reconciliation between what you’ve earned, what you’ve already paid in taxes throughout the year (through withholding or estimated payments), and what your final tax liability is.

Tax Refunds vs. Tax Due: Clarifying the Difference

A common misconception is that “getting a tax return” automatically means receiving a refund. This isn’t always the case.

- Tax Refund: You receive a refund when you’ve paid more in taxes throughout the year (via payroll deductions or estimated payments) than your actual tax liability. This often happens if your W-4 withholding is set too high or if you qualify for significant tax credits. A refund isn’t “free money”; it’s your own money being returned to you.

- Tax Due: Conversely, if you haven’t paid enough in taxes during the year to cover your final tax liability, you will owe additional money to the government. This can occur if your withholding is too low, you have significant income from sources not subject to withholding, or your deductions and credits are less than anticipated.

The goal of filing is to accurately report your financial situation so that either the correct refund is issued, or the correct amount due is calculated.

Who Needs to File a Tax Return?

Not everyone is required to file a federal income tax return. The requirement generally depends on your gross income, filing status (single, married filing jointly, etc.), and age. For instance, if your income falls below a certain threshold, you might not be obligated to file. However, even if you’re not required to file, you might want to file if:

- You had federal income tax withheld from your pay.

- You made estimated tax payments.

- You qualify for refundable tax credits, such as the Earned Income Tax Credit or the Additional Child Tax Credit.

Filing in these situations is the only way to get your money back. Always check the IRS guidelines for the current tax year to determine your specific filing obligation.

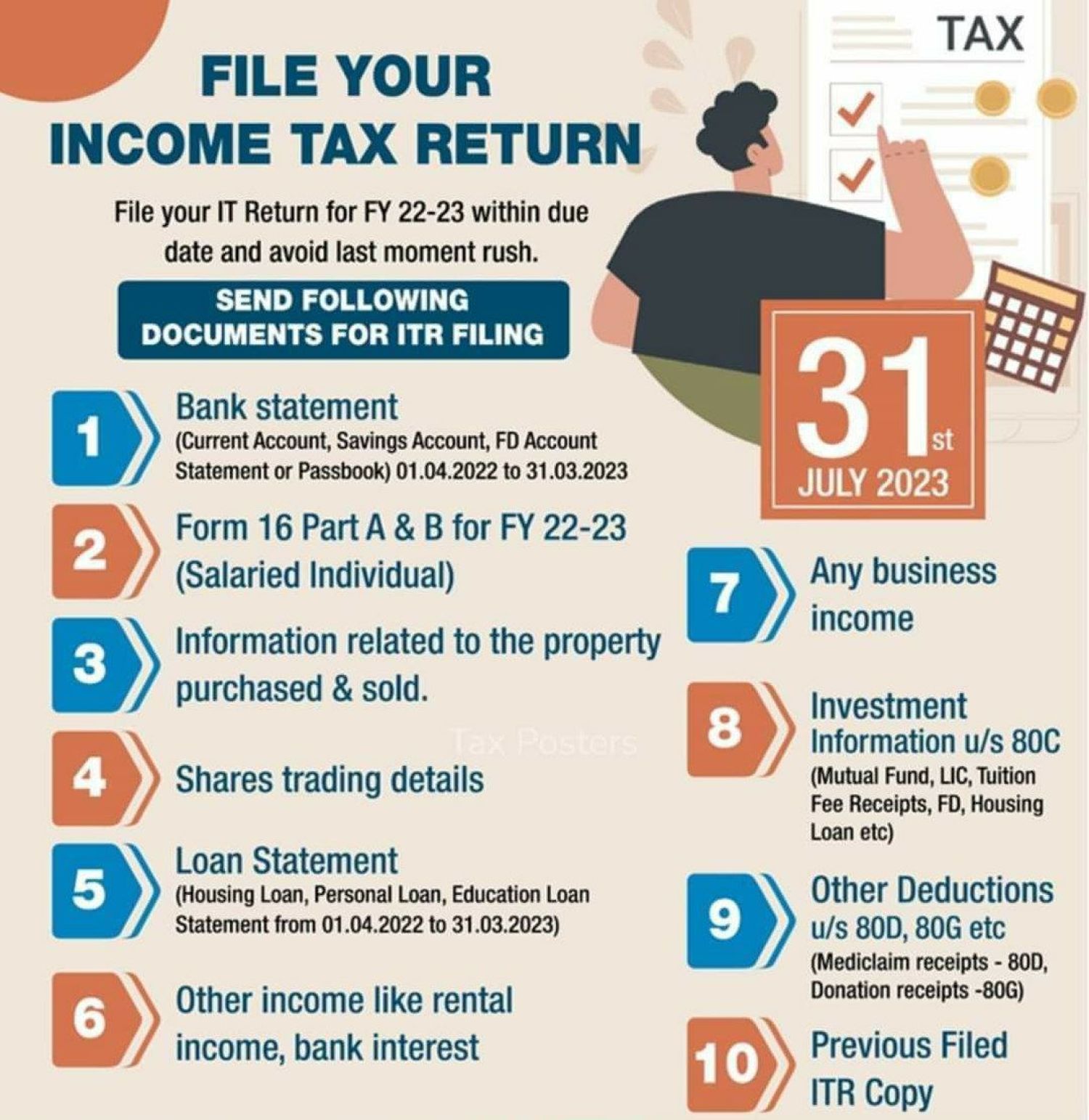

Essential Documents You’ll Need

Gathering your documents proactively is key to a smooth filing process. Here are some of the most common forms and records you’ll need:

- W-2 Forms: From each employer, showing your wages and taxes withheld.

- 1099 Forms: For various types of income not from an employer, such as:

- 1099-NEC (Nonemployee Compensation for contractors)

- 1099-DIV (Dividends and distributions)

- 1099-INT (Interest income)

- 1099-R (Distributions from IRAs, pensions, etc.)

- 1099-G (Unemployment compensation, state tax refunds)

- 1099-K (Payment card and third-party network transactions for gig workers)

- 1098 Forms: For certain deductible expenses, such as:

- 1098 (Mortgage interest)

- 1098-E (Student loan interest)

- 1098-T (Tuition statement)

- Other Income Records: Records for self-employment income, rental income, capital gains/losses, alimony received.

- Deduction & Credit Records: Receipts for medical expenses, charitable donations, business expenses, child care costs, property taxes, retirement contributions, and any other documentation supporting deductions or credits you plan to claim.

- Previous Year’s Tax Return: Useful for reference, especially if you’re claiming carryovers or need prior year information.

Organizing these documents beforehand will save you considerable time and reduce stress during tax season.

Navigating the Tax Return Process: Step-by-Step

Once you understand the basics and have your documents in hand, you’re ready to tackle the actual filing process. There are several paths you can take, each with its own advantages.

Choosing Your Filing Method

The method you choose depends on your comfort level with tax forms, the complexity of your financial situation, and your budget.

- Do-It-Yourself (DIY) Tax Software: Online tax software (e.g., TurboTax, H&R Block, TaxAct) guides you step-by-step, performs calculations, and helps identify potential deductions and credits. Many offer free versions for simple returns, with paid tiers for more complex scenarios. This is a popular choice for those with straightforward finances who want control over the process.

- Free Tax Filing Options:

- IRS Free File: If your adjusted gross income (AGI) is below a certain threshold, you might qualify to use free tax software provided by IRS partners.

- VITA/TCE Programs: The Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) programs offer free tax preparation services by IRS-certified volunteers for qualifying individuals. These are excellent resources for low-to-moderate-income individuals, persons with disabilities, the elderly, and those with limited English proficiency.

- Professional Tax Preparer: For complex returns (e.g., small business owners, investors with diverse portfolios, individuals with international income), or if you simply prefer professional assurance, a certified public accountant (CPA), enrolled agent (EA), or professional tax preparer can be invaluable. They can offer advice, ensure compliance, and often identify deductions you might overlook.

Completing Your Tax Form Accurately

Regardless of the method, the core task is to accurately populate your tax form. This involves:

- Reporting All Income: Enter all your income from W-2s, 1099s, and any other sources.

- Claiming Deductions: Decide whether to take the standard deduction (a fixed amount that reduces your taxable income) or itemize deductions (listing out specific eligible expenses like mortgage interest, state and local taxes, charitable contributions, medical expenses). You should choose the method that results in a lower taxable income.

- Applying for Credits: Identify and claim any tax credits you qualify for. Credits directly reduce the amount of tax you owe, dollar for dollar, and some are even refundable, meaning they can result in a refund even if you don’t owe any tax.

- Calculating Tax Liability: The software or preparer will calculate your gross tax, then subtract any payments you’ve already made (withholding, estimated taxes) to determine if you’re due a refund or owe additional tax.

Reviewing for Accuracy and Submitting Your Return

Before submitting, a thorough review is critical. Check for:

- Typographical Errors: Mistakes in Social Security numbers, dates, or amounts.

- Missing Information: Forgotten income sources or overlooked deductions.

- Correct Filing Status: Ensure you’ve selected the most advantageous filing status.

- Bank Account Information: If receiving a refund via direct deposit, confirm your routing and account numbers.

Once satisfied, you can submit your return. Most individuals choose to e-file (electronically file), which is faster, more accurate, and allows for quicker refund processing. If mailing, ensure you send it to the correct IRS address and keep a copy for your records. Always submit by the deadline (typically April 15th, unless it falls on a weekend or holiday).

Maximizing Your Refund or Minimizing Your Tax Bill

The goal of filing isn’t just compliance; it’s also about optimizing your financial outcome. By strategically utilizing deductions and credits, you can either increase your refund or reduce the amount of tax you owe.

Leveraging Deductions to Reduce Taxable Income

Deductions reduce your taxable income, meaning you pay tax on a smaller portion of your earnings.

- Standard Deduction: A fixed amount provided by the IRS, which varies by filing status and age. Many taxpayers find the standard deduction to be simpler and higher than their itemized expenses.

- Itemized Deductions: If your eligible expenses (e.g., mortgage interest, state and local taxes up to a limit, charitable contributions, significant medical expenses) exceed the standard deduction, you can itemize them using Schedule A.

- Above-the-Line Deductions: Some deductions reduce your income before your AGI is calculated, regardless of whether you itemize. Examples include contributions to traditional IRAs, student loan interest, and health savings account (HSA) contributions. Don’t overlook these!

Exploring Tax Credits for Direct Tax Reduction

Tax credits are often more powerful than deductions because they directly reduce the amount of tax you owe, dollar for dollar.

- Refundable Credits: These can result in a refund even if your tax liability is zero. Key examples include the Earned Income Tax Credit (EITC), Additional Child Tax Credit, and a portion of the American Opportunity Tax Credit.

- Non-Refundable Credits: These can reduce your tax liability to zero, but they won’t generate a refund beyond that. Examples include the Child Tax Credit, Lifetime Learning Credit, and Credit for Other Dependents.

It’s crucial to research and understand all credits you might qualify for, as they can significantly impact your final tax outcome. Tax software is very helpful in prompting you for these, but knowing what generally exists can help you prepare the necessary documentation.

The Impact of Withholding and Estimated Taxes

The amount of tax withheld from your paycheck (via Form W-4) or paid through estimated taxes determines how much you’ve pre-paid your tax bill.

- Adjusting W-4: If you consistently receive a large refund, it means you’re overpaying taxes throughout the year, essentially giving the government an interest-free loan. You might consider adjusting your W-4 with your employer to have less tax withheld, increasing your take-home pay. Conversely, if you frequently owe a significant amount, you might need to increase your withholding.

- Estimated Taxes: If you’re self-employed, have significant investment income, or other income not subject to withholding, you might need to make quarterly estimated tax payments to avoid underpayment penalties.

Proactive management of your withholding and estimated payments can help you avoid a large tax bill at year-end and put your money to work for you sooner.

What Happens After You File?

Once your tax return is submitted, the process isn’t entirely over. There are a few more steps and potential scenarios to be aware of.

Tracking Your Refund

If you’re expecting a refund, you’ll naturally want to know its status.

- IRS “Where’s My Refund?” Tool: The IRS offers an online tool that allows you to track the status of your federal refund. You’ll need your Social Security number, filing status, and the exact refund amount.

- State Refund Trackers: Most states that collect income tax also provide similar online tools to track state refunds.

- Timing: E-filed returns with direct deposit are generally processed much faster, often within 21 days. Mailed paper returns can take several weeks or even months.

Direct Deposit vs. Check

When filing, you’ll typically have the option to receive your refund via direct deposit or a paper check.

- Direct Deposit: This is the fastest and most secure method. Your refund is deposited directly into your bank account.

- Paper Check: If you don’t opt for direct deposit, a check will be mailed to the address on file. This method is slower and carries a higher risk of loss or theft.

Planning for Next Year

Tax planning isn’t just an annual event; it’s an ongoing process. Use insights from your current year’s return to plan for the future:

- Review Your W-4: If your income or deductions changed significantly, adjust your W-4.

- Keep Good Records: Maintain meticulous records of income and expenses throughout the year. Digital copies and cloud storage can be invaluable.

- Consult a Professional: If your financial situation becomes more complex, consider establishing a relationship with a tax professional who can offer year-round advice.

- Stay Informed: Tax laws can change, so staying informed about potential new deductions or credits can help you optimize your future returns.

Obtaining your tax return, whether it results in a refund or a payment due, is an essential part of sound financial management. By understanding the process, organizing your documents, choosing the right filing method, and strategically utilizing available deductions and credits, you can navigate tax season efficiently and confidently. Remember, proactive planning and accurate reporting are your best tools for a smooth and financially optimized outcome.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.