The question of “how much Facebook is worth” is far more complex than a single, static number. It’s a dynamic valuation, a constant negotiation between market forces, financial performance, strategic vision, and future potential. As Meta Platforms, Inc. (formerly Facebook, Inc.) navigates the ever-evolving landscape of digital communication, advertising, and its ambitious pivot to the metaverse, understanding its true economic value requires a deep dive into financial metrics, market sentiment, and the fundamental principles of business finance. For investors, financial analysts, and even casual observers, deciphering Meta’s worth offers profound insights into the mechanics of modern capitalism and the intricate valuations of tech giants.

At its core, a company’s worth, particularly a publicly traded one like Meta, is often primarily reflected in its market capitalization. However, market cap is merely a snapshot, a product of millions of individual decisions by buyers and sellers on a given day. The real art and science of valuation delve into what drives that market cap, what future earnings are discounted into today’s price, and what risks and opportunities lie ahead. This exploration will dissect the layers of Meta’s valuation, moving beyond the superficial to understand the true financial underpinnings of one of the world’s most influential companies.

Understanding Market Capitalization: The Basic Measure

When most people ask “how much Facebook is worth,” they are typically referring to its market capitalization. This is the most straightforward and widely quoted metric for a public company’s value. It provides an immediate, albeit volatile, indicator of how the market collectively assesses the company.

What is Market Cap?

Market capitalization (or “market cap”) is simply the total value of all of a company’s outstanding shares. It is calculated by multiplying the current share price by the total number of shares outstanding. For instance, if Meta’s stock is trading at $300 per share and it has 2.5 billion shares outstanding, its market cap would be $750 billion. This figure represents the total cost to buy every single share of the company at its current market price.

Market cap is critical for investors as it helps categorize companies by size (large-cap, mid-cap, small-cap) and is often a factor in determining stock index inclusions. It reflects what the market believes the company is worth based on its current profitability, future growth prospects, asset base, and perceived risks. However, it’s essential to remember that market cap fluctuates minute-by-minute with stock price changes and is not necessarily a reflection of the company’s intrinsic value – the true underlying economic worth of the business based on its assets, earnings, and cash flow. It’s a market-driven value, susceptible to investor sentiment, news cycles, and macroeconomic trends.

Meta’s Market Cap: A Dynamic Reflection

Meta Platforms, being a prominent tech giant, consistently ranks among the largest companies globally by market capitalization. Its market cap is a dynamic figure, swinging with daily trading. Periods of strong earnings reports, positive user growth, successful product launches, or favorable economic conditions can see its valuation soar. Conversely, market downturns, regulatory challenges, competitive pressures, or disappointing financial results can lead to significant drops. For example, the company’s ambitious investments into the metaverse, coupled with a slowdown in advertising revenue growth, have historically led to periods of increased investor scrutiny and valuation adjustments.

The size of Meta’s market cap signifies its immense influence on the global economy and investment markets. It’s a testament to the scale of its user base across Facebook, Instagram, and WhatsApp, and the vast advertising revenue generated from these platforms. However, its constant fluctuations underscore the high stakes and inherent volatility associated with investing in rapidly evolving tech businesses. The market cap, while a critical benchmark, serves as a starting point for deeper financial analysis, rather than the final word on the company’s true worth.

Beyond Market Cap: Factors Influencing Meta’s Valuation

While market capitalization provides a headline figure, a comprehensive valuation of Meta requires a deeper dive into the qualitative and quantitative factors that fundamentally drive its worth. These factors span financial performance, strategic direction, competitive pressures, and the broader economic and regulatory environment.

Financial Performance & Growth Potential

At the heart of any company’s valuation lies its financial performance. For Meta, this primarily revolves around its ability to generate revenue and profit, largely from its digital advertising business.

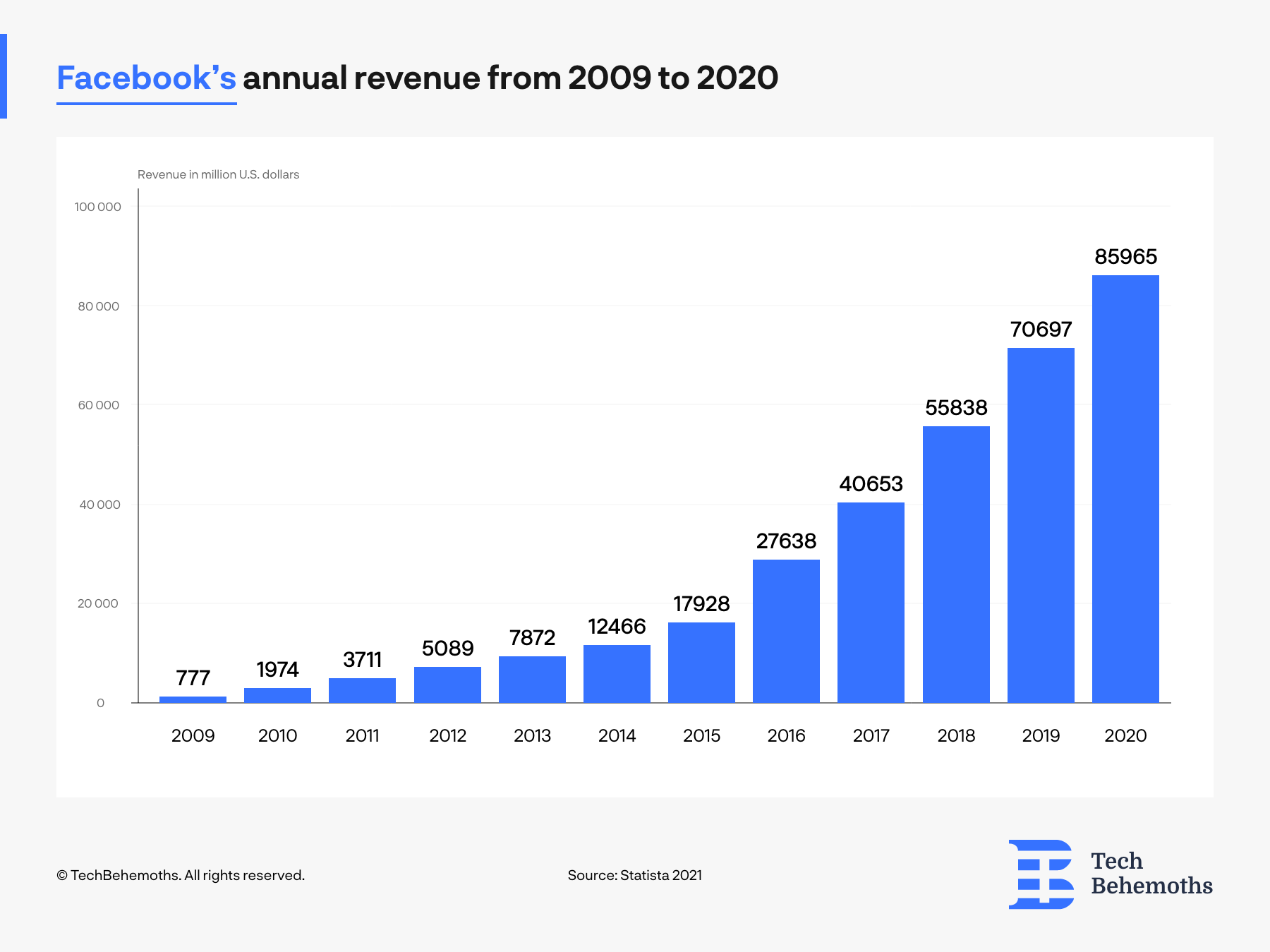

- Revenue Streams: The vast majority of Meta’s revenue comes from advertising across its Family of Apps (Facebook, Instagram, Messenger, WhatsApp). Analysts closely watch advertising revenue growth rates, average revenue per user (ARPU), and the efficiency of its ad delivery systems. Diversification efforts, such as e-commerce integrations and new monetization features, are also scrutinized.

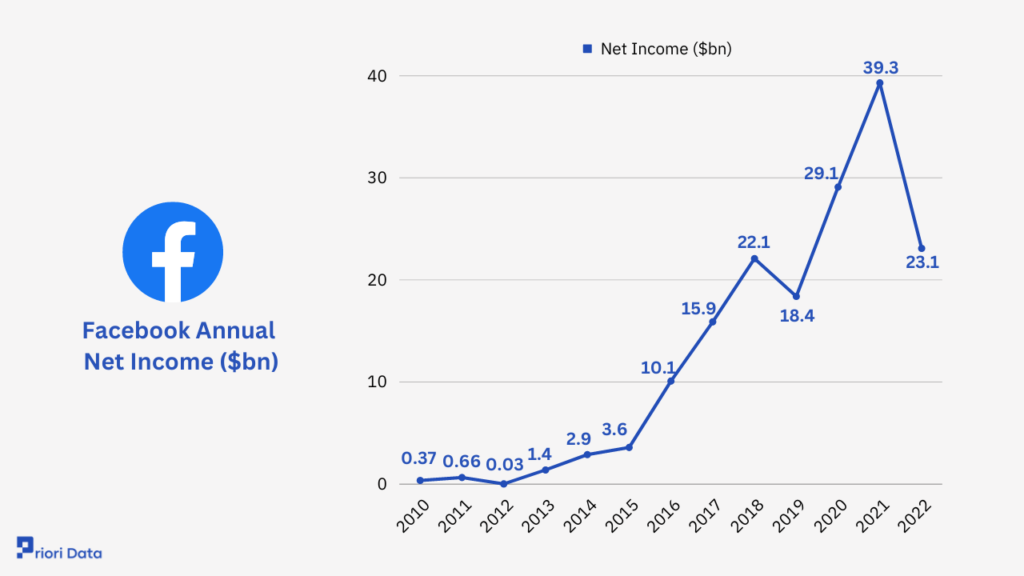

- Profitability: Net income, operating margins, and free cash flow are crucial indicators. Meta’s historical ability to convert its vast user base into significant profits is a key valuation driver. Future profitability hinges on managing expenses, particularly R&D for the metaverse, while maintaining strong ad sales.

- User Growth & Engagement: The sheer scale of Meta’s global user base (Daily Active Users – DAU, Monthly Active Users – MAU) across its family of apps is unparalleled. Growth in these metrics, particularly in developed markets, signals continued reach for advertisers and network effects. Engagement metrics, like time spent on platform, indicate stickiness and platform health.

- Future Growth Areas: Beyond core advertising, the market closely watches the potential of new ventures. The most significant is the Reality Labs segment, encompassing virtual and augmented reality hardware and software, which represents Meta’s long-term bet on the metaverse. While currently a significant cost center, its future potential, though highly speculative, is factored into long-term valuation models.

Strategic Investments & Future Vision (The Metaverse Bet)

Meta’s rebranding from Facebook was a clear signal of its pivot towards the metaverse. This strategic bet has a profound, albeit complex, impact on its valuation.

- Reality Labs & R&D: Meta is pouring billions into Reality Labs, developing VR headsets (Quest series), AR technologies, and the underlying infrastructure for a persistent, immersive digital world. While these investments suppress near-term profitability, they are seen as crucial for future growth by some investors, positioning Meta at the forefront of the next computing platform.

- Investor Sentiment vs. Long-Term Vision: The market is often divided on the metaverse strategy. Some investors view it as a necessary, bold move for future relevance, willing to endure short-term losses for potential long-term dominance. Others see it as a speculative drain on resources, with an uncertain return on investment. This dichotomy creates volatility in Meta’s stock price as sentiment shifts.

- Acquisitions & Ecosystem Building: Meta’s history of strategic acquisitions (Instagram, WhatsApp, Oculus) has been pivotal in building its ecosystem and has directly contributed to its worth. Future acquisitions in the metaverse space could further solidify its position, though they also face increased antitrust scrutiny.

Competitive Landscape & Regulatory Headwinds

No tech giant operates in a vacuum, and Meta faces intense competition and an increasingly stringent regulatory environment, both of which weigh heavily on its valuation.

- Competition: Meta competes fiercely with other social media platforms (e.g., TikTok, Snapchat, X), search engines (Google), and e-commerce giants (Amazon) for user attention and advertising dollars. The rise of short-form video and new platforms constantly challenges Meta’s dominance.

- Regulatory Scrutiny: Antitrust concerns regarding its past acquisitions and market power, data privacy regulations (like GDPR and CCPA), and content moderation controversies consistently pose risks. Potential legislative actions, forced divestitures, or heavy fines could significantly impact its business model and financial outlook.

- Platform Policy Changes: Apple’s App Tracking Transparency (ATT) initiative, for example, significantly impacted Meta’s ability to target ads, leading to substantial revenue losses and forcing changes in its advertising technology. Such platform policy changes by major ecosystem players represent an ongoing vulnerability.

Brand Strength, User Engagement & Network Effects (Financial Impact)

While often considered “soft” assets, brand strength, user engagement, and network effects translate directly into financial value for Meta.

- Brand Value: Despite controversies, the Facebook and Instagram brands remain incredibly powerful globally, offering trust and recognition that attract advertisers and users. The strength of these brands reduces customer acquisition costs and supports premium ad pricing.

- Network Effects: The more people use Meta’s platforms, the more valuable they become to each user and to advertisers. This creates a powerful moat, making it difficult for competitors to displace Meta, contributing to sustained user engagement and revenue generation. The sheer size of its interconnected network is a unique financial asset.

- Data & AI Capabilities: Meta’s vast trove of user data, combined with its advanced AI capabilities, allows for highly effective ad targeting, which is a key driver of its advertising revenue. This technological prowess is a valuable, intangible asset.

Valuation Methodologies Applied to Meta

Financial analysts employ various methodologies to arrive at a comprehensive valuation for a company like Meta. Each method offers a different perspective and helps piece together a more holistic picture of its worth.

Discounted Cash Flow (DCF)

The Discounted Cash Flow (DCF) model is considered one of the most robust valuation techniques as it attempts to determine the intrinsic value of a company based on its projected future free cash flows, discounted back to their present value.

- Process: Analysts forecast Meta’s free cash flow for several years (e.g., 5-10 years) based on revenue growth, operating expenses, capital expenditures, and working capital changes. A terminal value is then estimated for cash flows beyond the explicit forecast period. These future cash flows are then discounted back to the present using a discount rate, typically the Weighted Average Cost of Capital (WACC), which reflects the riskiness of Meta’s future earnings.

- Challenges for Meta: Applying DCF to Meta, especially with its metaverse pivot, presents unique challenges. Forecasting future cash flows for Reality Labs, a nascent and speculative venture, is incredibly difficult. Assumptions about market adoption, monetization strategies, and competitive success in the metaverse introduce significant variability. Furthermore, the WACC itself can be difficult to pinpoint precisely, especially for a company undergoing such a significant strategic shift. Despite these difficulties, DCF remains a cornerstone of fundamental valuation, providing a perspective on Meta’s long-term earning power.

Comparable Company Analysis (CCA)

Comparable Company Analysis (CCA), also known as “multiples valuation,” involves comparing Meta to similar publicly traded companies to derive a valuation.

- Process: This method identifies a group of publicly traded companies that are similar to Meta in terms of industry, business model, size, and growth prospects. Analysts then calculate various valuation multiples for these comparable companies (e.g., Price-to-Earnings Ratio (P/E), Enterprise Value-to-EBITDA (EV/EBITDA), Price-to-Sales (P/S)). These multiples are then applied to Meta’s relevant financial metrics (earnings, EBITDA, sales) to estimate its value.

- Application to Meta: Finding truly “comparable” companies for Meta is challenging due to its unique scale and diversified offerings. While companies like Google (Alphabet) or Microsoft might be considered for their advertising and tech platform aspects, Meta’s social media dominance and metaverse bet set it apart. Analysts often use a blend of comps, perhaps looking at other social media (Snap, Pinterest), ad tech companies, and broader tech giants, then making adjustments for Meta’s specific characteristics (e.g., higher growth in some segments, higher R&D spend in others). This method provides a market-based valuation relative to its peers.

Sum-of-the-Parts Valuation

Given Meta’s diverse operations, a Sum-of-the-Parts (SOTP) valuation can be particularly insightful. This method breaks the company down into its distinct business units, values each unit separately, and then sums them up to arrive at a total company value.

- Process: For Meta, this would involve valuing its core Family of Apps (Facebook, Instagram, WhatsApp) as one unit, and Reality Labs (metaverse hardware and software) as another. Each segment might be valued using different methodologies – the Family of Apps perhaps with DCF or CCA based on advertising revenue, while Reality Labs might be valued using more venture-capital-style metrics or by comparing it to emerging tech companies, recognizing its higher risk and longer path to profitability.

- Relevance for Meta: The SOTP approach is increasingly relevant for Meta due to its explicit separation of financial reporting for Family of Apps and Reality Labs. It helps investors understand if the market is correctly valuing both the highly profitable legacy business and the capital-intensive, future-oriented metaverse segment. It can highlight potential undervaluation if one segment is particularly strong, or indicate that the market is overly discounting the value of one part due to another.

The Volatility of a Tech Giant’s Worth

The worth of a company like Meta is rarely stable. It’s an ongoing assessment, influenced by a multitude of factors that can cause significant fluctuations in its market capitalization and perceived intrinsic value.

Market Sentiment and Investor Confidence

Perhaps the most immediate driver of volatility is market sentiment. News headlines, analyst ratings, economic forecasts, and even social media chatter can profoundly impact investor confidence.

- Positive Catalysts: Strong earnings beats, significant product innovations, positive regulatory developments, or upbeat economic data can send Meta’s stock soaring.

- Negative Pressures: Weak user growth, privacy scandals, antitrust investigations, disappointing metaverse progress, or a general economic slowdown can trigger sell-offs.

- Leadership & Vision: The market places significant weight on leadership. Mark Zuckerberg’s long-term vision for the metaverse, while potentially transformative, also carries execution risk, and investor confidence in his ability to deliver impacts the stock price.

Innovation Cycles & Disruptive Technologies

The technology sector is characterized by rapid innovation and constant disruption. Meta’s worth is intrinsically linked to its ability to adapt, innovate, and fend off challengers.

- Need for Reinvention: Companies that fail to innovate risk obsolescence. Meta’s past successes with Instagram and WhatsApp acquisitions, and its current metaverse bet, are attempts to stay ahead of the curve. The market constantly assesses its capacity for future invention.

- Disruptors: The rise of TikTok, for instance, demonstrated how quickly new platforms can erode market share and user attention, directly impacting Meta’s advertising revenue and, consequently, its valuation. Investors are always looking for the “next big thing” that could disrupt Meta.

Global Economic Factors

Macroeconomic conditions exert a broad influence on all companies, and Meta is no exception.

- Advertising Spend: As an advertising-dependent company, Meta is highly sensitive to economic cycles. During recessions or periods of high inflation, businesses tend to cut advertising budgets, directly impacting Meta’s top line.

- Interest Rates: Higher interest rates generally make future earnings less valuable in present terms, which can particularly impact growth stocks like Meta, whose valuation relies heavily on long-term projections. Rising rates can lead to a de-rating of the entire tech sector.

- Currency Fluctuations: As a global company, Meta’s international revenues and expenses are subject to currency exchange rate fluctuations, which can affect reported earnings.

Conclusion

The question of “how much Facebook (Meta Platforms) is worth” reveals itself to be a multifaceted inquiry, devoid of a simple, enduring answer. While its market capitalization provides a real-time gauge, it is merely the tip of the iceberg. A comprehensive understanding requires delving into its robust financial performance, the strategic foresight of its metaverse investments, the intricate web of competitive and regulatory pressures, and the undeniable financial power derived from its colossal user base and network effects.

Ultimately, Meta’s worth is a dynamic synthesis of its current profitability, its anticipated future cash flows, the market’s perception of its long-term vision, and the myriad risks and opportunities it faces. Valuation is not just about numbers; it’s about storytelling, forecasting, and risk assessment. For investors, understanding this intricate dance of finance, technology, and human behavior is paramount to making informed decisions about Meta’s role in their portfolios. It’s a testament to the fact that in the ever-shifting sands of the digital economy, a company’s “worth” is never a fixed destination, but rather a continuous journey of re-evaluation and adaptation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.