In the intricate landscape of personal finance, certain identifiers serve as fundamental pillars, enabling the seamless flow of money. Among these, the checking account number and routing number stand out as essential components for virtually all banking transactions. Far from mere strings of digits, these numbers are the backbone of direct deposits, automated bill payments, wire transfers, and countless other financial operations that define modern life. Understanding their purpose, how to locate them, and crucially, how to safeguard them, is not just about convenience – it’s a critical aspect of financial literacy and security in an increasingly digital world.

This article delves into the precise definitions, functions, and significance of your checking account and routing numbers, providing a comprehensive guide for anyone looking to master their personal financial operations. We will explore their interplay, highlight their diverse applications, and offer insights into protecting this vital information from potential misuse.

Understanding the Core Identifiers in Your Financial Transactions

At the heart of every bank account are two primary identifiers that facilitate the movement of funds: the routing number and the checking account number. While both are critical, they serve distinct purposes, working in tandem to ensure your money reaches its intended destination securely and accurately.

The Routing Number: Your Bank’s Digital Fingerprint

The routing number, also known as an ABA (American Bankers Association) routing transit number, is a nine-digit code that uniquely identifies your financial institution. It acts like a bank’s address on the vast network of the U.S. financial system. When you initiate a transaction that involves moving money between different banks, the routing number tells the system precisely which bank to send or receive funds from.

Originally developed in 1910 to process paper checks, routing numbers have evolved to facilitate electronic transactions as well. There are currently over 26,000 active routing numbers in the United States, assigned by the ABA and managed by LexisNexis. Each financial institution may have one or several routing numbers, depending on factors like geographic location, mergers, or specific types of transactions (e.g., one for ACH transfers and another for wire transfers, though often they are the same for typical consumer accounts).

Key Uses of the Routing Number:

- Direct Deposits: Employers use your bank’s routing number (along with your account number) to deposit your paycheck directly into your account.

- Automated Clearing House (ACH) Transfers: This includes electronic bill payments, online transfers between your own accounts at different banks, and peer-to-peer payments.

- Wire Transfers: For expedited, often larger, electronic transfers between banks, both domestically and internationally.

- Check Processing: When you write a check, the routing number printed on it directs the check to your specific bank for clearance.

Where to Find Your Routing Number:

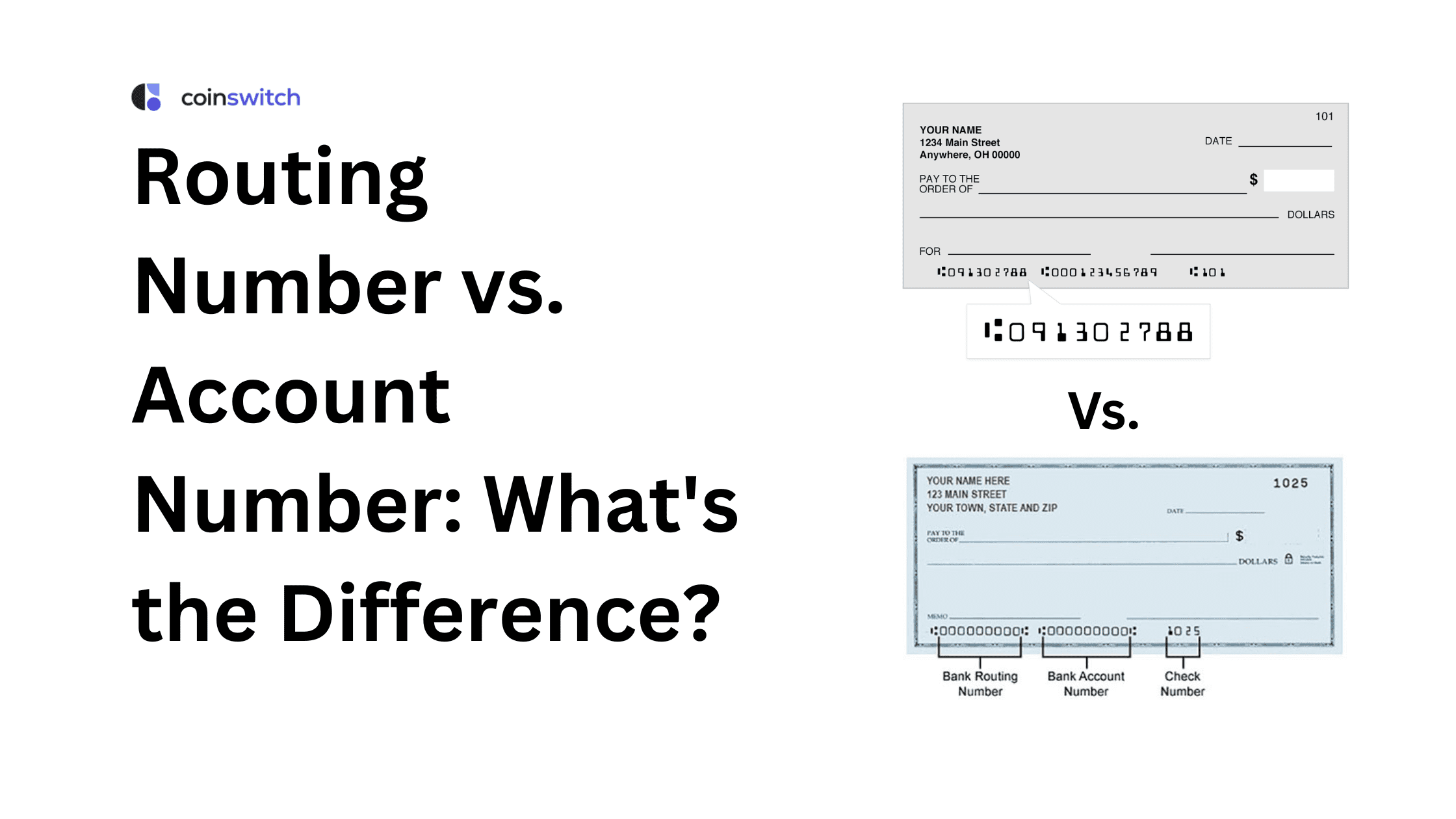

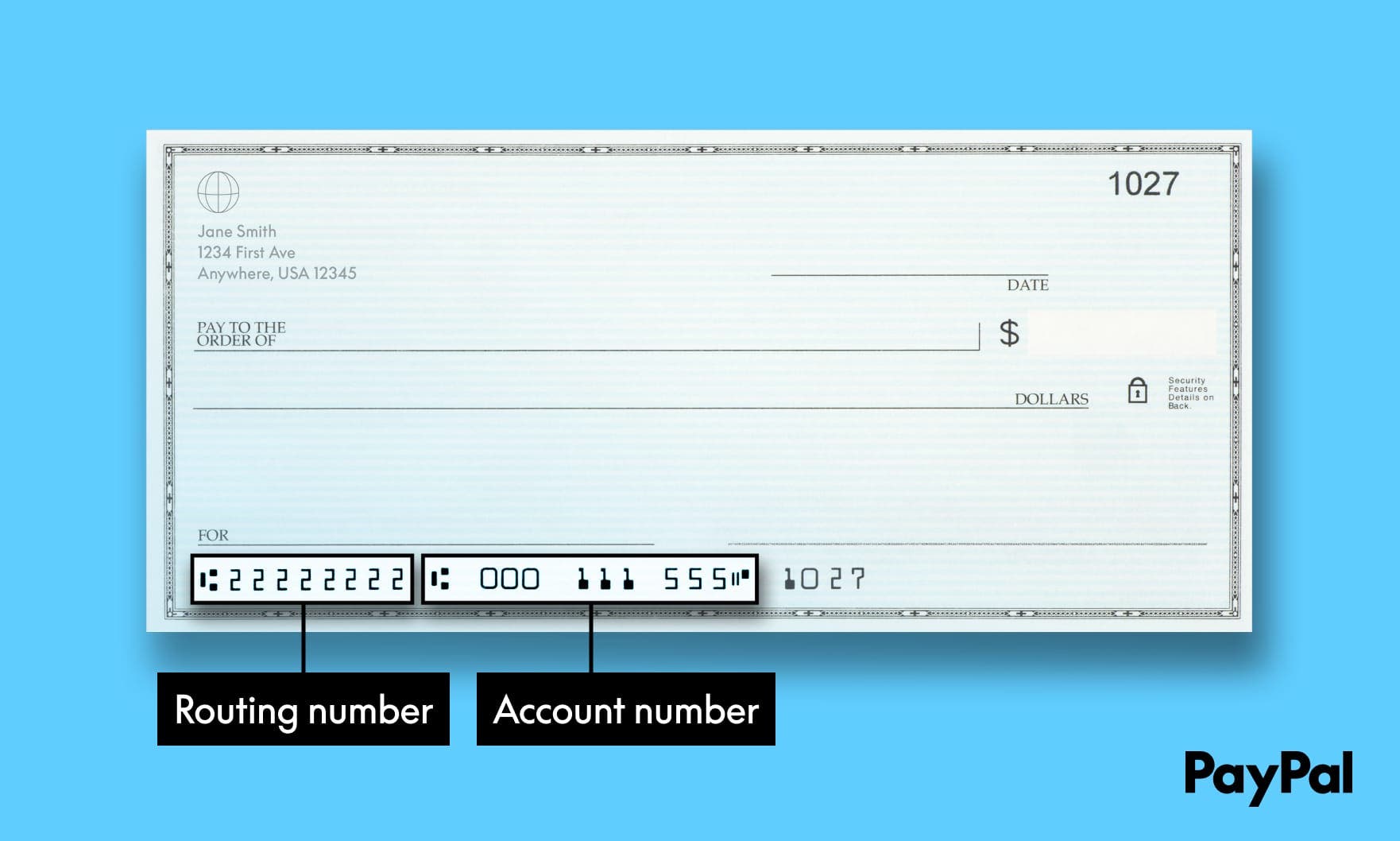

- On a Check: It’s typically the first set of nine digits printed on the bottom left of your checks.

- Online Banking Portal: Log in to your bank’s website or mobile app. The routing number is usually displayed prominently on your account summary page or under account details.

- Bank Statement: Your monthly bank statement will list your account’s routing number, often near your account number and other bank information.

- Bank’s Official Website: Most banks list their routing numbers on their “Contact Us” or “Help” sections. Be cautious when searching online, as some third-party sites may be inaccurate; always verify with your bank directly.

The Checking Account Number: Your Personal Account Identifier

While the routing number identifies your bank, the checking account number is the unique identifier for your specific account within that bank. It’s a personalized sequence of digits (typically 10-12 digits long, though it can vary) that distinguishes your account from all others held at the same financial institution. Think of it as your personal street address within the bank’s “city.”

Without an account number, funds would not know which specific account at a bank to enter or exit. It is crucial for directing money to or from your particular checking balance.

Key Uses of the Checking Account Number:

- Receiving Direct Deposits: Just like with the routing number, your employer needs your account number to ensure your paycheck lands in your checking account.

- Setting Up Bill Payments: For automatic payments to utility companies, loan providers, or other recurring expenses, your account number is essential.

- Transferring Funds: Whether you’re moving money between your own accounts, sending money to a friend, or paying a vendor, your account number directs the funds.

- Initiating Debit Card Transactions (indirectly): While your debit card has its own number, the underlying transactions eventually pull from or credit your checking account using its unique identifier.

Where to Find Your Checking Account Number:

- On a Check: It’s usually the middle set of digits (often 10-12 digits) printed on the bottom of your checks, positioned between the routing number and the check number.

- Online Banking Portal: Similar to the routing number, your account number is almost always visible when you log into your bank’s website or mobile app, typically on your account summary or details page.

- Bank Statement: Your paper or electronic bank statement will clearly display your checking account number.

- Contact Your Bank: If you cannot locate it through other means, your bank’s customer service can provide it after verifying your identity.

The Interplay and Importance of Routing and Account Numbers

Alone, neither the routing number nor the account number is sufficient for most financial transactions. They are designed to work together, forming a complete address that ensures accuracy and security. Imagine trying to mail a letter with just a street number but no street name, or vice versa; the postal service needs both to deliver it correctly. Similarly, banks need both sets of digits to process your money effectively.

Facilitating Seamless Financial Operations

The combined power of these numbers simplifies and speeds up a vast array of financial activities, making modern banking incredibly efficient.

Direct Deposits and Automated Clearing House (ACH) Transfers

The most common use for these numbers is facilitating direct deposits for paychecks, government benefits, or tax refunds. Your employer or the government entity will request both your bank’s routing number and your specific account number. This enables funds to be transferred electronically and securely from their bank account to yours, often arriving faster than a traditional paper check. ACH transfers also encompass electronic bill payments, where you authorize companies to pull funds directly from your account, and person-to-person transfers through various apps and services. The accuracy of both numbers is paramount for these transactions. A single digit error can cause delays, rejections, or even misdirection of funds to an incorrect account, leading to significant hassle.

Wire Transfers

For larger or time-sensitive transactions, wire transfers are often utilized. Unlike ACH transfers, which can take a few business days, wire transfers are typically processed within the same day or even hours. When sending a domestic wire transfer, you will almost always need the recipient’s bank routing number and their account number. For international wire transfers, additional information like SWIFT/BIC codes (international equivalents of routing numbers) and the recipient’s full name and address are also required, ensuring the funds navigate multiple banking systems to reach their global destination. The robust security protocols surrounding wire transfers rely heavily on the precise identification provided by these numbers.

Connecting Financial Tools and Apps

In an age of sophisticated financial technology, routing and account numbers are often used to link your bank account to various third-party services. This includes budgeting apps that aggregate your financial data, investment platforms where you transfer funds, or digital payment services like PayPal or Venmo. When you set up these connections, you typically provide your routing and account numbers to enable secure, authorized transactions between your bank and the service. This allows for seamless transfers, tracking of spending, and consolidation of your financial picture, all built on the foundation of these unique identifiers.

Beyond Basic Transactions: Other Uses

The utility of these numbers extends beyond just moving money. They are often requested in situations where a clear financial link is needed to your primary banking hub.

- Applying for Loans or Credit: Lenders may ask for your banking details to verify your financial stability or to set up automatic loan repayments from your checking account.

- Identity Verification: In some instances, financial institutions or government agencies might use these numbers as part of a multi-factor authentication or identity verification process, confirming that you are the legitimate owner of the account.

- Tax Purposes: For receiving tax refunds directly or making tax payments electronically, the IRS and other tax authorities require your routing and account numbers.

Safeguarding Your Financial Information

While routing and account numbers are crucial for convenient banking, they are also sensitive pieces of information that, in the wrong hands, could lead to financial fraud. Protecting these numbers is as important as protecting your debit card or credit card details.

Best Practices for Security

Proactive measures can significantly reduce your risk of financial exposure.

Share with Caution

Only share your routing and account numbers with trusted entities and for legitimate financial purposes. This includes your employer, established bill payment services, reputable financial institutions, and government agencies. Be wary of unsolicited requests for this information via email, text, or phone calls, as these are common tactics for phishing scams. Remember, your bank will generally not ask you for your full account number via email or text.

Recognize and Avoid Scams

Scammers often attempt to trick individuals into divulging their banking information. Common tactics include emails or messages purporting to be from your bank or a government agency, claiming there’s a problem with your account or an urgent payment due. Always verify the sender and the legitimacy of the request. If in doubt, contact your bank directly using a verified phone number or website, not one provided in a suspicious communication. Never click on links in suspicious emails or provide information on unverified websites.

Utilize Secure Platforms

When conducting online banking or providing your information to a service, ensure the website is secure (look for “https://” in the URL and a padlock icon). Use strong, unique passwords for your online banking accounts and consider enabling two-factor authentication (2FA) for an added layer of security.

Monitor Account Activity Regularly

One of the best defenses against fraud is vigilance. Regularly check your bank statements and online banking activity for any unauthorized transactions. Many banks offer alerts for large transactions or unusual activity, which you should enable. The sooner you detect suspicious activity, the faster you can act to mitigate potential damage.

The Risks of Misuse and Fraud

If your routing and account numbers fall into the wrong hands, the consequences can range from minor inconveniences to significant financial loss and identity theft.

- Unauthorized Withdrawals: Fraudsters can use your numbers to set up unauthorized ACH debits, pulling money directly from your account. This is a common tactic, often disguised as legitimate payments or small test transactions.

- Check Fraud: If someone gets hold of your checks or your account details, they could create counterfeit checks to drain your account.

- Identity Theft: While routing and account numbers alone may not be enough for full identity theft, they are crucial pieces of a larger puzzle. Combined with other personal information, they can be used to open new accounts, apply for credit, or commit other forms of financial fraud in your name.

If you suspect your checking account or routing number has been compromised, contact your bank immediately. They can help you review your account for fraudulent activity, place alerts, and potentially close the compromised account and open a new one. Time is of the essence in these situations.

Navigating Common Questions and Misconceptions

Despite their ubiquity, there are still common questions and misunderstandings surrounding routing and account numbers. Clarifying these can enhance your financial savvy.

Differentiating from Debit Card Numbers

A frequent point of confusion is differentiating between your checking account number and your debit card number. While both are associated with your bank account, they serve entirely different purposes.

- Debit Card Number: This is a 16-digit number found on the front of your debit card. It is primarily used for point-of-sale transactions (swiping, tapping, or inserting your card), online purchases, and ATM withdrawals. It acts as an access key to your account through card networks (Visa, Mastercard, etc.). If your debit card number is compromised, you can typically get a new card issued with a new number, while your underlying checking account number remains the same.

- Checking Account Number: As discussed, this directly identifies your bank account for electronic funds transfers like direct deposits, bill payments, and wire transfers. It grants a different level of access to your account than a debit card.

Never provide your debit card number when a routing and account number are requested for direct bank transfers, and vice-versa. They are not interchangeable.

Finding Your Numbers: A Practical Guide

As reiterated earlier, your checks, online banking portal, and bank statements are the most reliable sources.

- On a Check: The sequence at the bottom typically reads: Routing Number (9 digits) | Account Number (variable length) | Check Number (variable length).

- Online Banking: This is often the quickest and most secure way to retrieve your numbers. Most banking apps and websites make this information readily available under “Account Details” or a similar section.

- Bank Statement: Your monthly statement, whether paper or digital, is an official record containing all your primary account identifiers.

Avoid relying on general web searches for your bank’s routing number, especially if you have an account with a larger bank that might have multiple routing numbers based on region or transaction type. Always verify the information through official bank channels.

What if I Have Multiple Accounts?

If you have multiple checking accounts at the same bank, each account will have a unique checking account number. This is crucial for directing funds to the correct specific account. However, it is very common for all accounts (checking, savings, money market) at the same financial institution to share the same routing number. The routing number identifies the bank itself, while the account number identifies your particular holding within that bank. Always double-check which account number you are providing, especially if you have several accounts for different purposes.

In conclusion, the checking account number and routing number are indispensable elements of the modern financial system. They are the keys that unlock the convenience of direct deposits, automated payments, and efficient money transfers, forming the bedrock of personal finance. A thorough understanding of what these numbers are, where to find them, and how to protect them is not merely good practice—it is a fundamental requirement for navigating your financial life securely and confidently in today’s digital age. By exercising diligence and adopting best security practices, you can harness the power of these identifiers while safeguarding your financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.