Securing a home loan is one of the most significant financial milestones an individual will ever achieve. It is not merely a transaction but a strategic maneuver that requires meticulous planning, a deep understanding of personal finance, and an awareness of the broader economic landscape. In an era of fluctuating interest rates and evolving lending standards, knowing how to position yourself as an ideal borrower is the difference between a rejected application and a keys-in-hand success.

This guide provides a professional roadmap for navigating the complexities of the mortgage market, ensuring you are financially prepared to secure the best possible terms for your future home.

1. Strengthening Your Financial Foundation

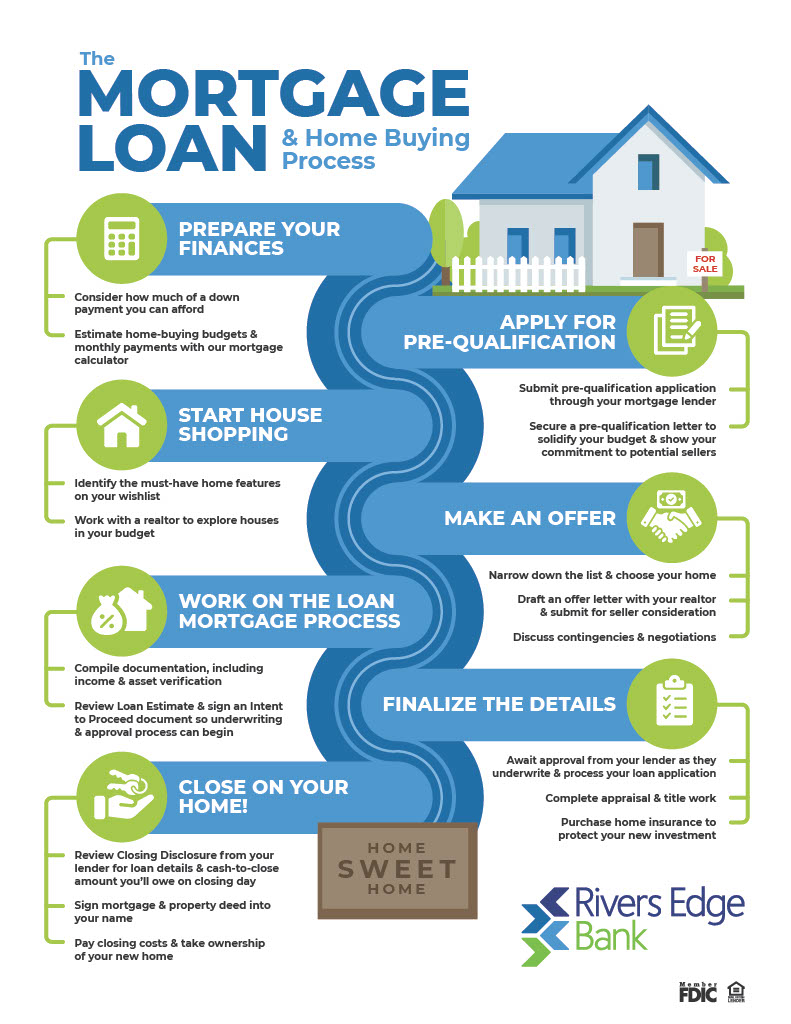

Before you ever step foot in an open house or contact a real estate agent, you must conduct a rigorous audit of your personal finances. Lenders view a mortgage through the lens of risk management; your goal is to prove that you are a low-risk investment.

Understanding and Improving Your Credit Score

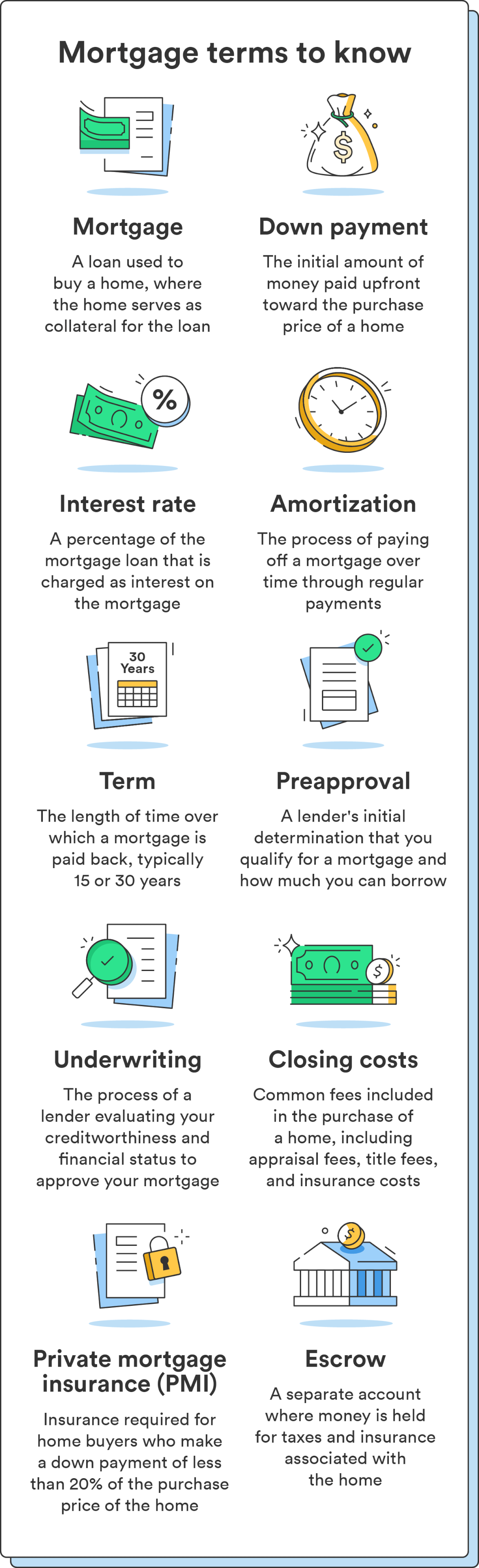

Your credit score is the single most influential factor in determining your interest rate and loan eligibility. For most conventional loans, a score of 620 is the minimum, but to access “prime” rates, you generally need a score of 740 or higher.

To optimize your score, begin by pulling your credit reports from all three major bureaus (Equifax, Experian, and TransUnion). Check for inaccuracies or fraudulent activity that could be dragging your score down. Furthermore, focus on your credit utilization ratio—the amount of debt you owe compared to your total credit limits. Keeping this ratio below 30% signals to lenders that you manage revolving credit responsibly.

Managing Your Debt-to-Income (DTI) Ratio

Lenders use the Debt-to-Income (DTI) ratio to measure your ability to manage monthly payments. This is calculated by dividing your total monthly debt obligations (student loans, car payments, credit card minimums) by your gross monthly income.

Most lenders prefer a DTI ratio of 43% or lower, though some programs allow for higher limits. If your DTI is high, consider an aggressive debt-repayment strategy before applying for a mortgage. Reducing your existing liabilities not only improves your chances of approval but also increases the total loan amount for which you may qualify.

Accumulating Capital for Down Payments and Closing Costs

While the “20% down payment” is often cited as the gold standard to avoid Private Mortgage Insurance (PMI), many modern loan programs allow for significantly less. However, the more capital you bring to the table, the more equity you have from day one.

Beyond the down payment, you must account for closing costs, which typically range from 2% to 5% of the home’s purchase price. These costs cover appraisals, title insurance, attorney fees, and taxes. Having a dedicated “home fund” that is liquid and accessible is essential for a smooth closing process.

2. Navigating Mortgage Types and Lending Institutions

Not all home loans are created equal. The financial industry offers a variety of products tailored to different borrower profiles. Choosing the right one can save you tens of thousands of dollars over the life of the loan.

Conventional vs. Government-Backed Loans

Conventional loans are not insured by the federal government and typically follow the guidelines set by Fannie Mae or Freddie Mac. They are ideal for borrowers with strong credit and stable income.

In contrast, government-backed loans are designed to increase homeownership accessibility:

- FHA Loans: Insured by the Federal Housing Administration, these allow for down payments as low as 3.5% and are more lenient with credit scores.

- VA Loans: Available to veterans and active-duty service members, these often require $0 down and offer highly competitive interest rates.

- USDA Loans: Targeted toward rural and suburban buyers with low-to-moderate incomes, these also offer 100% financing options.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

A fixed-rate mortgage offers a stable interest rate for the duration of the loan (usually 15 or 30 years), providing predictable monthly payments. This is the preferred choice in a low-interest-rate environment.

An Adjustable-Rate Mortgage (ARM) usually offers a lower initial “teaser” rate for a set period (e.g., 5 or 7 years), after which the rate adjusts based on market indices. ARMs can be strategic for buyers who plan to sell or refinance before the initial period ends, but they carry the risk of significantly higher payments in the future.

Selecting the Right Financial Partner

Where you get your loan matters as much as the loan itself. You have three primary options:

- Retail Banks: Often offer convenience if you already have an established relationship, but their lending criteria can be rigid.

- Credit Unions: Member-owned institutions that often provide lower interest rates and more personalized service.

- Mortgage Brokers: Professionals who shop your profile across multiple lenders to find the best deal. This can be particularly helpful for borrowers with unique financial situations.

3. The Mortgage Application and Approval Process

Once your finances are in order and you have selected a loan type, the formal process begins. This stage requires organizational discipline and transparency.

The Power of Pre-Approval

A pre-qualification is a simple estimate of what you might be able to borrow, but a pre-approval is a conditional commitment from a lender. To get pre-approved, you must submit your tax returns, W-2s, bank statements, and pay stubs for a thorough review. In a competitive real estate market, a pre-approval letter is essential; it signals to sellers that you are a serious, vetted buyer with the financial backing to close the deal.

The Underwriting Phase

After you find a home and your offer is accepted, the loan moves into “underwriting.” This is the stage where the lender’s underwriter scrutinizes every detail of your financial life and the property itself.

During this time, the lender will order an appraisal to ensure the home’s value matches the purchase price. They will also perform a “title search” to ensure there are no liens or legal disputes regarding the property. It is vital during this phase to avoid any major financial changes—do not change jobs, do not open new credit cards, and do not make large, unexplained deposits into your bank accounts, as these can trigger a re-evaluation of your file.

Understanding Private Mortgage Insurance (PMI)

If you put down less than 20% on a conventional loan, you will likely be required to pay Private Mortgage Insurance. PMI protects the lender in case you default on the loan. While it increases your monthly payment, it is not a permanent fixture. Once your home equity reaches 20% through mortgage payments or market appreciation, you can typically request to have the PMI removed, effectively lowering your monthly overhead.

4. Finalizing the Loan and Closing with Confidence

The final stretch of the home loan process involves significant paperwork and the official transfer of funds. Understanding the final requirements ensures you don’t stumble at the finish line.

Locking in Your Interest Rate

Interest rates change daily based on bond market activity and Federal Reserve policy. Once you have a signed purchase agreement, you can “lock” your interest rate. This protects you from rate hikes while your loan is being processed. Be sure to check the duration of the lock; if the closing process takes longer than expected, you may need to pay an extension fee to keep that rate.

Reviewing the Closing Disclosure (CD)

At least three business days before you close, your lender is legally required to provide a Closing Disclosure. This document outlines the final terms of your loan, including the exact interest rate, monthly payment, and the total “cash to close” required. Compare this document carefully against the “Loan Estimate” you received earlier in the process. If there are significant discrepancies in fees, ask for a detailed explanation immediately.

The Closing Day

On closing day, you will sign a mountain of legal documents, including the Deed of Trust and the Promissory Note. You will provide the funds for your down payment and closing costs, usually via a wire transfer or cashier’s check. Once the lender funds the loan and the county records the deed, the process is complete.

Conclusion

Getting a loan for a house is a marathon, not a sprint. It demands a proactive approach to credit management, a strategic choice of mortgage products, and a disciplined approach to the application process. By strengthening your financial profile and understanding the mechanics of the lending industry, you transition from being a mere applicant to a sophisticated borrower.

While the process may seem daunting, the reward is the acquisition of a tangible asset that serves as both a sanctuary and a cornerstone of your long-term financial portfolio. Approach the journey with patience and professional diligence, and the path to homeownership will become significantly clearer.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.