Navigating the intricacies of bank fees can often feel like deciphering a complex code, and among the most common, and often frustrating, charges are overdraft fees. For account holders with Chase, understanding the specific costs associated with overdrawing your account is crucial for maintaining sound financial health. An overdraft occurs when you spend more money than you have available in your checking account, leading the bank to cover the transaction, but usually at a cost. While this service can prevent a transaction from being declined, the accompanying fees can quickly add up, turning a small miscalculation into a significant financial burden.

This comprehensive guide will delve into Chase’s overdraft policies, detailing the standard fees, the various ways an overdraft can occur, and crucially, how you can protect yourself from incurring these charges. By gaining a clear understanding of Chase’s system, you can implement proactive strategies to manage your money more effectively, avoid unnecessary fees, and ensure your financial journey remains on track.

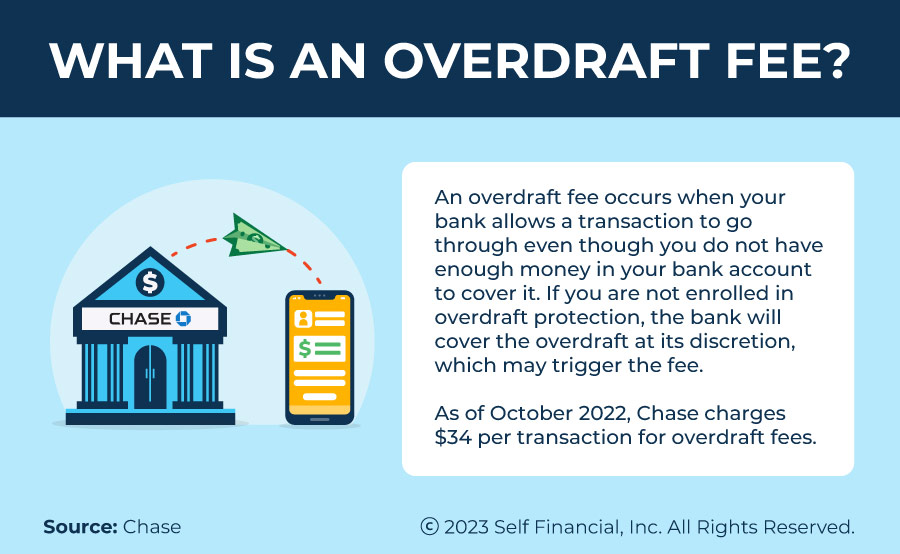

Understanding Chase’s Overdraft Policy and Fees

Chase, like most major financial institutions, has a structured policy regarding overdrafts, designed to cover transactions when your account balance falls below zero. However, this convenience comes with a specific price tag that every account holder should be aware of.

The Standard Overdraft Fee at Chase

As of the latest information, Chase charges a standard overdraft fee of $34 per item. This means that each transaction that causes your account to become overdrawn, or that is processed while your account is already negative, could incur this fee. It’s vital to note that this isn’t a one-time daily charge; rather, it applies per transaction. This distinction is critical, as multiple small transactions processed while your account is in the red can quickly multiply the fees you owe. For instance, if you make three separate purchases that each overdraw your account, you could be charged $102 in fees ($34 x 3) in a single day.

Overdraft Limits and Daily Caps

While Chase charges per item, there is a limit to how many overdraft fees you can incur in a single day. Typically, Chase caps the total number of overdraft fees at a maximum of three (3) per business day. This means that regardless of how many transactions push your account into overdraft territory after the first three, you generally won’t be charged more than $102 for those fees on that particular day. However, it’s important to remember that this cap only applies to the overdraft fees, not necessarily to the negative balance itself, which you will still be responsible for repaying. Furthermore, the bank reserves the right to decline transactions that would overdraw your account beyond a certain threshold, even if you are opted into overdraft services.

What Triggers an Overdraft?

Understanding how an overdraft occurs is the first step in preventing them. Several types of transactions can lead to an overdraft:

- Debit Card Purchases: Using your debit card for everyday purchases at stores, restaurants, or online is a common trigger.

- ATM Withdrawals: Taking out cash from an ATM when your balance is insufficient.

- Checks: Writing a check for an amount greater than your available funds.

- ACH Transactions: Automated Clearing House payments, which include direct debits for recurring bills like utilities, gym memberships, or subscription services.

- Online Bill Pay: Payments scheduled through Chase’s online bill pay service.

It’s important to differentiate between your “available balance” and your “current balance.” Your current balance reflects all settled transactions, while your available balance accounts for pending transactions and holds. It’s your available balance that Chase uses to determine if a transaction will cause an overdraft.

The Difference Between Overdrafts and Returned Items

Sometimes, instead of covering an overdraft, Chase might simply return a transaction unpaid. This often happens with checks or ACH payments. If a check bounces or an ACH payment is returned, the recipient doesn’t get their money, and you might incur a “returned item fee” from Chase, which is typically the same as an overdraft fee ($34). Additionally, the payee (the person or company you were trying to pay) might also charge you a fee for the returned item. It’s crucial to understand that even if Chase doesn’t cover the transaction, you might still face charges from both your bank and the intended recipient, compounding the financial pain.

Chase’s Overdraft Protection and Related Services

Recognizing the financial strain overdrafts can cause, Chase offers several services designed to help customers manage their accounts and potentially avoid fees. These services range from automatic transfers to specific programs that provide a grace period.

Linking to a Savings Account or Line of Credit

One of the most effective and often least expensive ways to prevent overdraft fees is to set up overdraft protection. Chase allows you to link your checking account to another Chase account, such as a savings account, or to a Chase credit card or personal line of credit.

- Savings Account Link: If your checking account runs low, funds are automatically transferred from your linked savings account to cover the transaction. While there’s typically no fee from Chase for these transfers, it does deplete your savings, and if you have frequent transfers, it might be a sign of deeper budgeting issues.

- Line of Credit/Credit Card Link: Funds can be drawn from a pre-approved line of credit or your linked credit card to cover overdrafts. While this prevents an overdraft fee, you will typically incur interest charges on the amount borrowed from your line of credit or credit card, and these funds must be repaid. This option essentially turns an overdraft into a loan, which can be beneficial but requires disciplined repayment to avoid accumulating interest debt.

Chase Overdraft Assist℠

Chase Overdraft Assist℠ is a specific program designed to help eligible customers avoid overdraft fees under certain conditions. This service automatically waives the overdraft fee if:

- Your account is overdrawn by $50 or less at the end of the business day.

- You bring your account balance to a positive status by the end of the next business day.

This provides a valuable grace period and a buffer for minor shortfalls. It’s not a free pass for continuous overdrafts, but a helpful safety net for small, unexpected discrepancies. To be eligible, customers must generally be opted into Chase’s Debit Card Overdraft Service and meet specific account criteria, such as maintaining a positive balance for a certain period. Understanding the rules and leveraging this service responsibly can save customers significant money.

Debit Card Overdraft Service (Opt-In)

When you open a checking account with Chase, you are typically given a choice regarding “Debit Card Overdraft Service.” This is an opt-in service, meaning you must specifically agree to it.

- Opted In: If you choose to opt-in, Chase may authorize and pay debit card transactions and ATM withdrawals even if you don’t have enough money in your account. If they do, you will likely be charged the standard $34 overdraft fee for each transaction. The benefit is that your card won’t be declined at the point of sale, which can be convenient.

- Opted Out: If you opt-out (or do nothing), Chase will generally decline debit card transactions and ATM withdrawals if you don’t have sufficient funds. This means you avoid the overdraft fee for these specific types of transactions, but your card might be declined, which can be embarrassing or inconvenient. However, it forces you to live within your means for debit card spending. It’s important to remember that opting out only applies to debit card and ATM transactions; other types of transactions like checks or ACH payments can still overdraw your account and incur fees.

Strategies to Avoid Chase Overdraft Fees

Proactive money management is the most effective defense against overdraft fees. By implementing a few key strategies, you can significantly reduce your risk of encountering these charges.

Monitor Your Account Balance Regularly

The easiest way to prevent an overdraft is to always know how much money you have. Utilize Chase’s robust online banking platform and mobile app to check your balance frequently. Pending transactions, direct deposits, and upcoming bill payments can all impact your available balance, and staying informed allows you to anticipate shortfalls. Set a routine to check your account daily or every other day.

Set Up Low Balance Alerts

Chase offers customizable alerts that can notify you when your account balance falls below a certain threshold you define. This is an invaluable tool for preventing overdrafts. You can receive these alerts via text, email, or push notifications through the mobile app. Setting an alert at, for example, $100 or $50 can give you enough warning to transfer funds or adjust your spending before an overdraft occurs.

Utilize Budgeting Tools and Apps

Beyond just checking your balance, a comprehensive budget is essential. Use budgeting apps (like Mint, YNAB, or Chase’s own financial planning tools if available) or even a simple spreadsheet to track your income and expenses. Categorize your spending, identify areas where you can cut back, and allocate funds for upcoming bills. A clear picture of your cash flow minimizes surprises and ensures you always have enough for essential payments.

Build an Emergency Fund

One of the most robust defenses against overdrafts is a healthy emergency fund. This dedicated savings account should hold at least three to six months’ worth of living expenses. In the event of an unexpected expense, a job loss, or a temporary income disruption, your emergency fund can act as a buffer, preventing you from needing to dip into your checking account below zero. It’s the ultimate financial safety net that guards against many financial misfortunes, including overdrafts.

Review and Reconcile Your Transactions

Make it a habit to regularly reconcile your account statements with your own records. This involves comparing all transactions that have cleared your account against your receipts or spending log. This process helps catch errors, identify forgotten subscriptions, and ensures you’re aware of all pending transactions that haven’t yet posted, giving you an accurate picture of your true available funds.

What to Do If You Incur an Overdraft Fee

Despite your best efforts, an overdraft can sometimes happen. If you find yourself facing a Chase overdraft fee, don’t panic. There are steps you can take.

Contact Chase Immediately

The most important step is to call Chase customer service as soon as you realize you’ve been charged a fee. Explain your situation politely and calmly. Banks, including Chase, sometimes offer a “courtesy waiver” for overdraft fees, especially if it’s your first time, you have a good banking history, or if you can quickly deposit funds to cover the negative balance. While they are not obligated to waive the fee, a polite request can often be successful. Be prepared to explain how you plan to prevent future overdrafts.

Understand the Repayment Timeline

If your account is overdrawn, you are typically required to bring it back to a positive balance as quickly as possible. Chase will usually provide a specific timeframe (e.g., by the end of the next business day) within which you must deposit funds to clear the negative balance. Failing to do so can lead to continued account issues, including the possibility of additional fees (though capped for a single day), suspension of overdraft services, or even account closure. Swift action is key to mitigating further problems.

Review Your Overdraft Protection Settings

After an overdraft event, take the opportunity to review your current overdraft protection settings.

- Are you opted into debit card overdraft service? If you frequently get overdrafts from debit card use, perhaps opting out would be a better choice, forcing your card to decline rather than incur a fee.

- Do you have a linked savings account or line of credit for protection? If not, consider setting one up.

- Are your low balance alerts configured correctly? Adjust the threshold if necessary to give you more warning.

This experience can be a valuable learning opportunity to refine your financial safeguards.

In conclusion, while Chase overdraft fees can be an unwelcome surprise, they are largely avoidable with careful planning and proactive account management. By understanding Chase’s fee structure, utilizing their overdraft protection services, and adopting disciplined budgeting habits, you can protect your finances and keep your money working for you, not against you. Stay informed, stay vigilant, and take control of your banking experience.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.