Deciding to cancel a credit card is a significant financial decision that should be approached with careful consideration. While it might seem like a straightforward task, understanding the financial implications and following the correct procedures is crucial to protect your credit score and ensure a smooth transition. For Capital One cardholders, the process involves a few key steps and a thorough awareness of how it impacts your broader personal finance strategy. This guide will walk you through the financial rationale, the detailed steps, and the critical considerations when closing a Capital One credit card, ensuring you make an informed decision for your financial well-being.

Why Consider Cancelling Your Credit Card? (Financial Rationale)

The decision to cancel a credit card often stems from a desire to improve one’s financial health, simplify personal finance management, or react to changing financial circumstances. Understanding the underlying financial reasons can help affirm if cancellation is indeed the right move for you.

Eliminating Unnecessary Debt Potential

For many, an open credit line represents a temptation to spend, potentially leading to accumulating debt. If you find yourself struggling with impulse purchases or have a history of carrying high balances, closing a card can be a proactive step to remove this temptation. It’s a way of setting boundaries for your future spending habits and reducing the psychological burden of available credit that you might not need. This is particularly relevant for those committed to a debt-reduction strategy, as fewer cards mean fewer opportunities to fall back into old habits.

Reducing Annual Fees

Some Capital One credit cards, especially premium travel or rewards cards, come with annual fees that can range from modest to substantial. If you’re no longer utilizing the card’s benefits to offset these fees, or if your spending habits have changed, retaining such a card becomes a financial drain. Cancelling a card with an annual fee that you no longer find valuable is a direct way to cut unnecessary recurring expenses, thereby freeing up funds that can be allocated to savings, investments, or debt repayment. Always review the fee structure and the value you derive before committing to a cancellation.

Simplifying Your Financial Portfolio

Managing multiple credit cards can be cumbersome, leading to missed payments, overlooked fees, or a general lack of clarity about your overall financial standing. Consolidating your financial accounts by cancelling unused or rarely used cards can significantly simplify your personal finance management. A streamlined portfolio means fewer statements to review, fewer payment due dates to remember, and a clearer picture of your total available credit and outstanding balances. This simplification can reduce financial stress and help you maintain better oversight of your money.

Strategic Debt Management

In some cases, cancelling a credit card can be a tactical move within a broader debt management plan. If you are consolidating high-interest debt onto a single lower-interest loan or card, closing the original high-interest accounts can prevent you from racking up new debt on those lines. This approach ensures that your efforts to become debt-free are not undermined by the continued availability of credit, reinforcing your commitment to financial discipline. However, it’s crucial to understand the credit score implications before proceeding, as discussed in the next section.

The Financial Implications of Credit Card Cancellation

While there are valid reasons to cancel a credit card, it’s vital to be aware of the potential repercussions, particularly concerning your credit score and overall financial flexibility. A comprehensive understanding of these implications will enable you to make a decision that supports your long-term financial health.

Impact on Credit Score (Credit Utilization Ratio)

One of the most significant impacts of closing a credit card is on your credit utilization ratio. This ratio compares your total credit card balances to your total available credit limit. When you close a card, you reduce your total available credit. If your balances remain the same, your utilization ratio will increase, which can negatively affect your credit score. Lenders view a high utilization ratio as a sign of financial risk. To mitigate this, consider paying down existing balances on your other cards before closing one, thereby lowering your overall reported debt relative to your remaining available credit.

Impact on Credit History Length

The length of your credit history, or the average age of your accounts, is another factor influencing your credit score. Closing an older credit card can shorten your overall credit history, especially if it was one of your oldest accounts. A longer credit history generally demonstrates a consistent track record of responsible borrowing, which is favorable to lenders. If the Capital One card you’re considering cancelling is your oldest account, weigh the benefit of cancellation against the potential negative impact on your credit history length. Sometimes, keeping an old, unused card open (even just for small, infrequent purchases) might be a better strategy to maintain that history.

Loss of Rewards and Benefits

Before cancelling, meticulously check if you have any outstanding rewards points, cash back, or other benefits associated with your Capital One card. Most credit card issuers, including Capital One, will forfeit any unredeemed rewards once the account is closed. This could represent a tangible financial loss. Ensure you redeem all available points or cash back well in advance of the cancellation process. Similarly, if your card offers perks like travel insurance, extended warranties, or concierge services, confirm you won’t need these services in the near future, as they will cease upon account closure.

Contingency Planning and Emergency Funds

A credit card can sometimes serve as a financial safety net for emergencies, particularly if you have a low-interest rate or a substantial credit limit. While relying solely on credit for emergencies is not ideal, removing this option without an adequate cash emergency fund in place could leave you vulnerable. Before cancelling, ensure you have a robust emergency savings account that can cover unexpected expenses, usually three to six months’ worth of living expenses. This ensures that you maintain financial resilience without relying on debt.

Preparing for Cancellation: A Financial Checklist

Before you pick up the phone to contact Capital One, a series of preparatory steps can save you headaches and help preserve your financial standing. This checklist ensures you’ve considered all angles.

Pay Off Your Balance Entirely

This is the most critical step. You cannot cancel a credit card with an outstanding balance. Ensure that your Capital One account balance is exactly $0.00. Pay off the full amount and then wait for the payment to clear and be reflected on your account. It’s also wise to check for any pending transactions or automatic payments that might post after you’ve made your final payment.

Redeem All Rewards and Benefits

As mentioned, any unredeemed points, cash back, or travel miles will typically be forfeited upon cancellation. Log into your Capital One account online or call their customer service to redeem every last bit of your rewards. This ensures you don’t leave any money or value on the table.

Update Recurring Payments

Many people link their credit cards to automatic payments for subscriptions (e.g., streaming services, gym memberships), utility bills, or online purchases. Before closing your card, go through all your recurring payments and update them with a different credit card or bank account. Forgetting this step can lead to missed payments, service interruptions, and potentially late fees on those services.

Review Credit Report

It’s a good practice to obtain a copy of your credit report from one of the three major credit bureaus (Experian, Equifax, TransUnion) before and after cancelling your card. This allows you to verify that the card is indeed reported as closed and to monitor for any unexpected changes to your credit score. You are entitled to a free credit report from each bureau once a year via AnnualCreditReport.com.

Step-by-Step Guide to Cancelling Your Capital One Card (Practical Financial Action)

Once you’ve completed your preparatory steps, you’re ready to initiate the cancellation process. Following these steps will ensure a smooth and documented closure of your account.

Contacting Capital One

The most common and effective method to cancel a Capital One credit card is by phone.

- Phone: Call the customer service number located on the back of your card or on Capital One’s official website. Be prepared for retention specialists who may try to offer incentives to keep your account open. Stick to your decision if you are firm on cancellation.

- Online Chat/Secure Message (Less Common for Cancellation): While Capital One offers online support, cancellation typically requires a phone conversation for identity verification and final processing.

- Mail (Least Recommended): You could send a written request, but this is slow and offers less immediate confirmation. If you choose this, send it via certified mail with a return receipt requested.

What to Say and Ask

When you speak with a Capital One representative, be clear and direct:

- State that you wish to close your credit card account.

- Confirm that your balance is $0.00 and ask the representative to verify this.

- Inquire about any residual interest that might post to the account after your final payment. Ensure this is accounted for.

- Ask if there are any outstanding fees or charges you need to be aware of.

- Request a written confirmation of the account closure to be mailed to you.

- Note the date and time of your call, the representative’s name or ID, and a confirmation number if provided.

Documenting the Process

Thorough documentation is your best defense against future disputes or misunderstandings.

- Keep Call Logs: Record the date, time, and name of the representative you spoke with.

- Save Confirmation Numbers: If the representative provides one, save it.

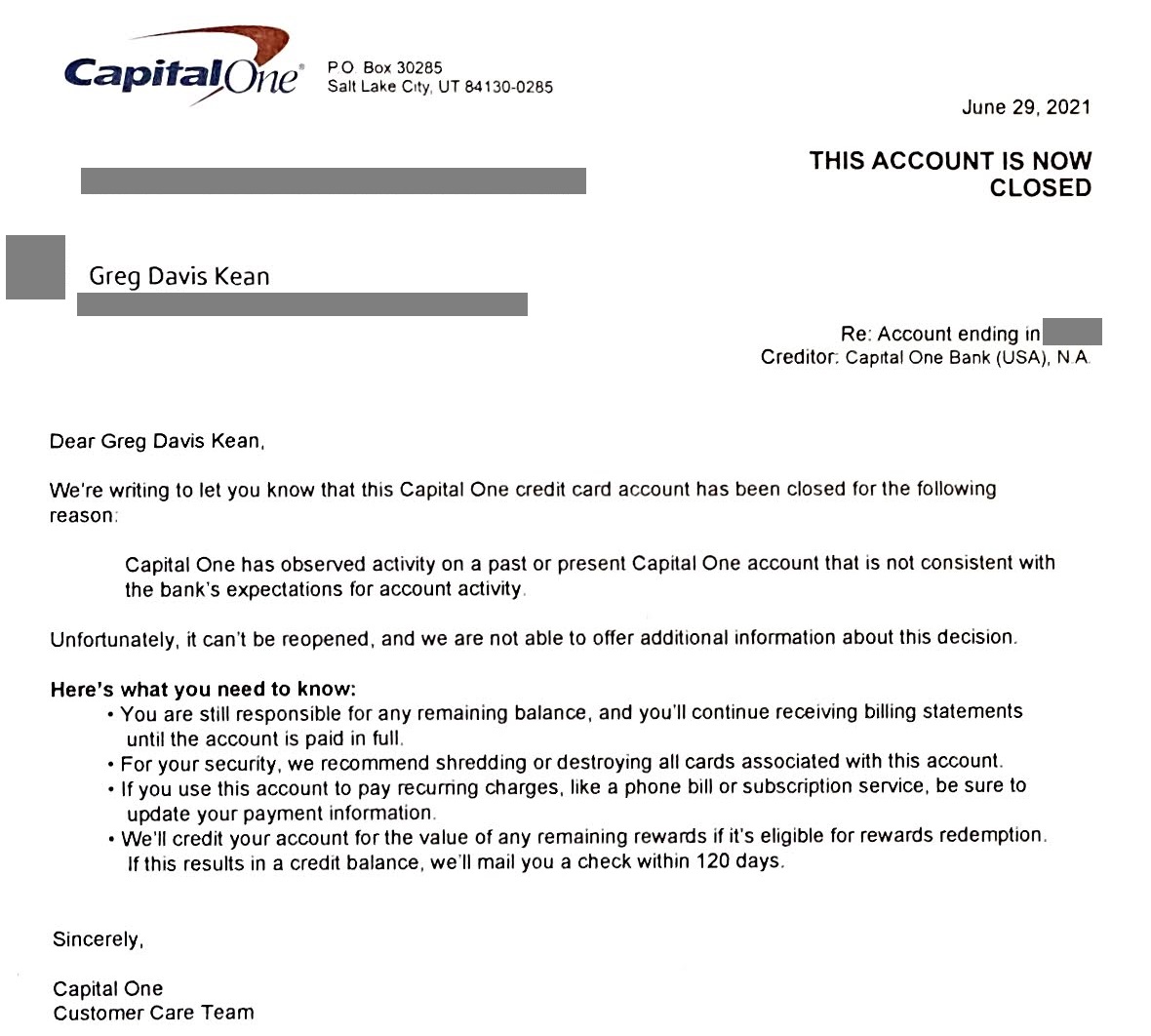

- Retain Written Confirmation: Once you receive the letter confirming account closure, keep it with your financial records. This serves as official proof that the account was closed at your request.

- Check Your Credit Report (Again): After a billing cycle or two, check your credit report to ensure the card is reported as “closed by grantor” (meaning by you) and that your utilization and credit history are correctly reflected.

What to Do with the Physical Card

Once the account is officially closed and you have confirmation, physically destroy the card. Cut through the magnetic stripe, chip, and account number multiple times to render it unusable and prevent fraudulent activity. Do not simply throw it away intact.

Alternatives to Cancellation: Financial Optimization Strategies

Before committing to cancellation, it’s worth exploring alternatives that might serve your financial goals better, especially if preserving your credit history or avoiding a credit score dip is a priority. These strategies focus on optimizing your existing financial tools.

Downgrading to a No-Annual-Fee Card

If your primary reason for cancelling is to avoid an annual fee, ask Capital One if you can product change or downgrade your card to one of their no-annual-fee options. This allows you to keep the account open, preserving your credit history and available credit, but without incurring recurring costs. This is often an ideal solution for older cards that contribute significantly to your average age of accounts.

Balance Transfers and Debt Consolidation

If you’re looking to eliminate debt, a balance transfer to a card with a 0% introductory APR could be a more effective strategy than outright cancellation, especially if you plan to pay off the transferred balance within the promotional period. Similarly, exploring debt consolidation loans can simplify payments and potentially reduce interest, allowing you to manage debt more strategically before considering card closures.

Strategically Using the Card

If the card is old and contributes positively to your credit history, consider keeping it open and using it for a small, recurring expense that you pay off immediately each month (e.g., a streaming service, a small utility bill). This keeps the account active and positively reporting to credit bureaus without incurring debt or annual fees (if it’s a no-fee card). This strategy maintains your available credit and credit history length, both beneficial for your credit score.

Negotiating with Capital One

Before cancelling, especially if you have a good payment history, try negotiating with Capital One. You might be able to secure a lower interest rate, a waiver of an annual fee, or a better rewards structure if they believe it will retain you as a customer. This can transform a card you were considering closing into a more beneficial financial tool.

Cancelling a Capital One credit card is a financial act with consequences that extend beyond merely cutting up a piece of plastic. By understanding the financial rationale, preparing thoroughly, executing the cancellation precisely, and exploring alternatives, you can ensure that your decision aligns with your broader financial goals and contributes positively to your overall financial health. Always prioritize a strategic approach to managing your credit and debt.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.