In the ever-evolving landscape of personal finance, managing bank accounts effectively is a fundamental skill. Sometimes, this management involves the decision to close an account, a process that can seem daunting but is entirely manageable with the right information. Whether you’re consolidating your financial portfolio, switching to a new banking institution, or simply no longer need a particular account, understanding “how to close a Citibank account” is crucial for a smooth and stress-free transition. This guide will delve into the motivations behind such a decision, outline the essential preparatory steps, detail the various methods of closure, highlight potential pitfalls, and advise on post-closure actions, all within the strict confines of the Money niche.

Why Consider Closing Your Citibank Account?

The decision to close a bank account is rarely arbitrary. It often stems from a thoughtful evaluation of one’s financial situation and banking needs. Recognizing the underlying reasons can help solidify your decision and ensure you proceed with confidence.

Changing Financial Needs and Priorities

As life progresses, so do our financial requirements. A checking account that perfectly suited your needs in college might be less ideal when you’re managing a family budget or a growing investment portfolio. Similarly, a savings account opened for a specific goal might no longer be necessary once that goal is met. Citibank, like other large financial institutions, offers a broad spectrum of products. However, if your current accounts no longer align with your financial priorities – perhaps you need more robust budgeting tools, different interest rates, or specific investment integration – then closure becomes a logical consideration.

Seeking Better Banking Alternatives

The financial market is highly competitive, with traditional banks, online-only banks, and credit unions vying for customers. It’s common for individuals to discover new financial products or services that offer better terms, lower fees, higher interest rates, or more convenient digital tools. If you’ve found an alternative that better suits your lifestyle, offers superior customer service, or provides greater financial benefit, transitioning away from your current Citibank account can be a smart money move. This often involves comparing fees, ATM access, mobile banking capabilities, and customer support responsiveness.

Consolidating Accounts for Simplicity

Many individuals accumulate multiple bank accounts over time, often for different purposes or from various life stages. While having several accounts can offer diversification, it can also lead to fragmentation and make overall financial management more complex. Consolidating your accounts into a single, comprehensive banking relationship can simplify budgeting, streamline bill payments, and provide a clearer overview of your financial standing. Closing redundant or underutilized Citibank accounts is a key step in this consolidation process, freeing up mental space and reducing administrative overhead.

Dissatisfaction with Services or Fees

Customer experience plays a significant role in banking relationships. If you’ve experienced persistent issues with Citibank’s customer service, encountered unexpected or rising fees, or found the digital banking interface cumbersome, these frustrations can be powerful motivators for closure. While switching banks takes effort, the long-term benefit of a more positive and efficient banking experience can outweigh the initial inconvenience, ultimately contributing to better personal finance management.

Pre-Closure Checklist: Essential Steps Before You Begin

Before initiating the formal closure process, a series of preparatory steps are crucial to prevent complications, ensure a smooth transition, and safeguard your financial well-being. This pre-closure checklist is your roadmap to a hassle-free exit.

Transferring Funds and Settling Debts

The absolute first step is to ensure that your Citibank account balance is either zero or at a minimal level, sufficient only to cover any impending fees or small outstanding transactions. Transfer any remaining funds to your new bank account or another designated account. Simultaneously, confirm that all debts associated with the account, such as an overdraft or a line of credit, are fully settled. Closing an account with an outstanding balance can lead to complications, including collection efforts and negative impacts on your credit score, especially if it’s a credit product.

Updating Automatic Payments and Direct Deposits

Modern financial life is built on automation. Many individuals have direct deposits for their paychecks or government benefits, and numerous automatic payments for bills like utilities, rent, mortgages, and subscriptions, linked to their primary checking accounts. Before closing your Citibank account, meticulously identify and update all these recurring transactions. Notify your employer, benefit providers, and all billers of your new account details. Failing to do so can result in missed payments, late fees, disruptions to services, and delayed income. Create a comprehensive list and systematically work through each one.

Downloading and Archiving Account Statements

Even after an account is closed, you may need access to past statements for tax purposes, audits, or personal financial record-keeping. Citibank typically allows customers to access past statements through online banking for a limited period after closure. However, it’s a best practice to download and securely archive at least the last 5-7 years of statements (or more, depending on your jurisdiction’s requirements) before the account is formally closed. This ensures you retain critical financial history irrespective of the bank’s data retention policies for closed accounts.

Redeeming Rewards Points and Unused Services

If your Citibank account is linked to a rewards program (e.g., credit card points, debit card rewards, or special savings bonuses), ensure you redeem all accumulated points or benefits before closing the account. Often, rewards points are forfeited upon account closure. Similarly, if you’re paying for any optional services linked to the account, such as identity theft protection or specific insurance products, cancel them separately if you no longer need them or transfer them to another provider.

Notifying Joint Account Holders (if applicable)

For joint accounts, open communication with all account holders is paramount. All parties must agree to the closure. Depending on Citibank’s specific policy, all joint account holders may need to provide consent or signatures for the closure to proceed. Ensure everyone involved is aware of the decision, understands the implications, and participates in the preparatory steps.

The Step-by-Step Process for Closing Your Citibank Account

Once your preparatory steps are complete, you’re ready to initiate the formal account closure with Citibank. There are several avenues available, each with its own nuances.

Understanding Citibank’s Closure Policies

Before you contact Citibank, it’s beneficial to briefly review their general policies regarding account closure. These can often be found in the account agreement or on their official website. Key aspects to look for include:

- Minimum balance requirements: Some accounts may require a zero balance to close, while others might allow a small positive balance to be transferred out during the process.

- Fees: Check if there are any early closure fees, especially for accounts opened recently, or if any outstanding fees need to be settled.

- Required documentation: What identification or information might they ask for to verify your identity?

Method 1: Closing via Online Banking (Limited Availability)

For some basic savings or checking accounts, Citibank might offer an option to initiate closure through their online banking portal or mobile app. This is often the most convenient method. Look for options like “Account Services,” “Manage Accounts,” or “Close Account” within your dashboard. If available, follow the prompts carefully. Be prepared to confirm your identity and the reason for closure. It’s crucial to ensure your balance is zero before attempting an online closure. Note that not all account types (e.g., investment accounts, complex credit lines) can be closed this way.

Method 2: Contacting Customer Service by Phone

Calling Citibank’s customer service is a widely available and often effective method for closing accounts.

- Prepare your information: Have your account number(s), personal identification (like your Social Security Number or date of birth), and possibly your online banking login details ready.

- Call the dedicated line: Use the customer service number typically found on the back of your debit card, credit card, or on Citibank’s official website.

- Explain your intent: Clearly state that you wish to close a specific account.

- Follow instructions: The representative will guide you through the process, which may involve identity verification, confirming your balance, and potentially asking for the reason for closure (though you are not obliged to provide one beyond “personal reasons”).

- Request confirmation: Always ask for a confirmation number or for a written confirmation to be sent to you via mail or email, documenting the closure request.

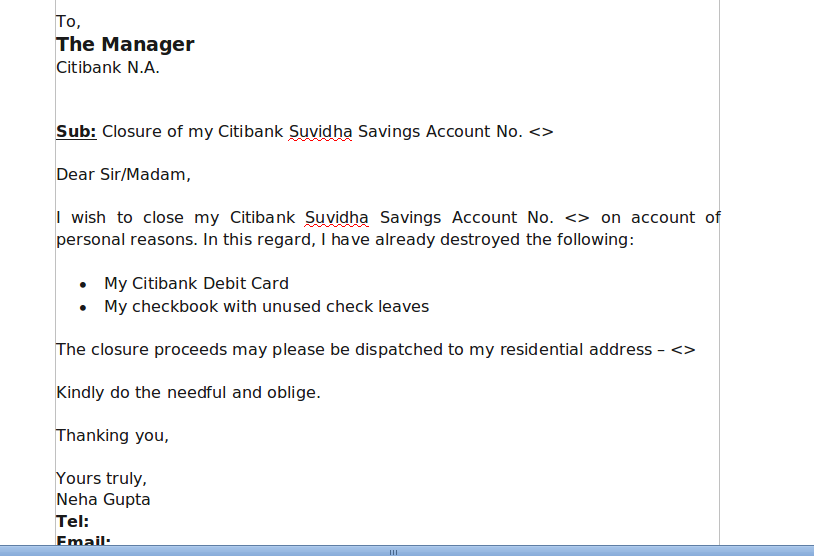

Method 3: Visiting a Citibank Branch In-Person

For those who prefer face-to-face interaction or have more complex accounts (e.g., joint accounts requiring multiple signatures), visiting a Citibank branch can be the best option.

- Bring necessary documents: Carry valid government-issued photo identification (e.g., driver’s license, passport) and your account details. For joint accounts, all account holders should ideally be present with their IDs.

- Speak with a representative: A branch employee can assist you directly with the closure paperwork.

- Obtain immediate confirmation: Closing an account in person often allows you to receive immediate written confirmation of the closure, which provides peace of mind. This is particularly useful if you need to take any remaining funds as a cashier’s check.

The Importance of Written Confirmation

Regardless of the method chosen, obtaining written confirmation of your account closure is non-negotiable. This document serves as proof that you officially requested and completed the closure. It should include the date of closure, the account number closed, and confirmation that the balance is zero. This record can be invaluable if any discrepancies or issues arise later, protecting you from potential fees or collection attempts for an account you believed was closed.

Understanding Potential Pitfalls and Best Practices

While closing a bank account is generally straightforward, certain pitfalls can lead to unexpected charges or administrative headaches. Awareness of these can save you time and money.

Avoiding Account Overdrafts and Negative Balances

A common pitfall is attempting to close an account with a pending debit or an existing negative balance. If an automated payment or a check clears after you’ve initiated closure or zeroed out the account, it can result in an overdraft. This might incur fees, delay the closure process, and require you to deposit funds to clear the negative balance before the account can be fully closed. It’s best practice to keep a small buffer in the account until you have received formal confirmation of closure.

Watch Out for Pending Transactions

Be meticulous about identifying and accounting for all pending transactions. Checks that haven’t cleared, debit card transactions that haven’t posted, or delayed ACH transfers can create issues. Give the account a few extra days, or even a week, after you believe all transactions have settled before initiating closure. This ‘cooling-off’ period can prevent unexpected post-closure complications.

Be Aware of Account Closure Fees

While many checking and savings accounts can be closed without a fee, some banks, including Citibank, may charge a fee if an account is closed shortly after it was opened (e.g., within 90 or 180 days). Review your account agreement or ask a representative if such a fee applies to your specific account. Budget for this if necessary to avoid surprises.

The Impact on Your Credit Score (for credit products)

If you are closing a credit card account with Citibank, it’s crucial to understand the potential impact on your credit score. Closing older credit accounts can sometimes reduce your overall available credit and shorten your average credit history, both of which can negatively affect your credit score, especially if you have few other credit lines. For checking and savings accounts, closure generally does not directly impact your credit score, as these are not credit products. However, if an account closes with an unpaid negative balance or an overdraft that goes to collections, that will negatively affect your credit.

Keeping Records of All Communications

Maintain a meticulous record of all interactions related to your account closure. This includes:

- Dates and times of phone calls.

- Names of representatives you spoke with.

- Confirmation numbers.

- Copies of any correspondence (emails, letters).

- Scans or photos of the written closure confirmation.

This documentation is your safety net, providing concrete evidence if any dispute arises regarding the closure.

Post-Closure Actions: Ensuring a Smooth Transition

Closing your Citibank account isn’t the final step; there are a few important actions to take afterward to ensure everything is settled and your financial life continues smoothly.

Verifying Account Closure

Even after receiving written confirmation, it’s a good idea to perform a final check. A week or two after the official closure date, you can attempt to log into your Citibank online banking portal (though access may be revoked). If you can no longer access it, or if it clearly indicates the account is closed, that’s a good sign. Alternatively, you can call customer service one last time to confirm verbally that the account is indeed closed with a zero balance.

Safely Disposing of Cards and Checks

Once the account is confirmed closed, cut up your Citibank debit cards, credit cards, and any unused checks. For cards, ensure you cut through the chip and the magnetic strip. This prevents unauthorized use and protects your identity. Do not simply throw them away intact.

Monitoring Your Credit Report

For a few months following the closure of any credit product (e.g., a Citibank credit card), keep an eye on your credit report. You can obtain a free copy annually from each of the three major credit bureaus (Equifax, Experian, TransUnion) via AnnualCreditReport.com. This allows you to verify that the account is correctly reported as “closed by consumer” and that no outstanding issues or incorrect information appear.

Communicating with Relevant Parties (Employers, Billers)

Although you would have updated direct deposits and automatic payments before closure, it’s a wise practice to follow up with key parties (like your employer or primary utility providers) after a week or two to confirm that your new banking details have been successfully updated in their systems. This proactive step helps prevent any missed payments or delayed deposits.

Closing a Citibank account, or any bank account, is a significant financial action. By understanding the motivations, meticulously preparing, following the correct procedures, being aware of potential pitfalls, and taking necessary post-closure steps, you can navigate this process with confidence and ensure a seamless transition to your new financial arrangements. Taking control of your banking relationships is a fundamental aspect of sound personal finance management.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.