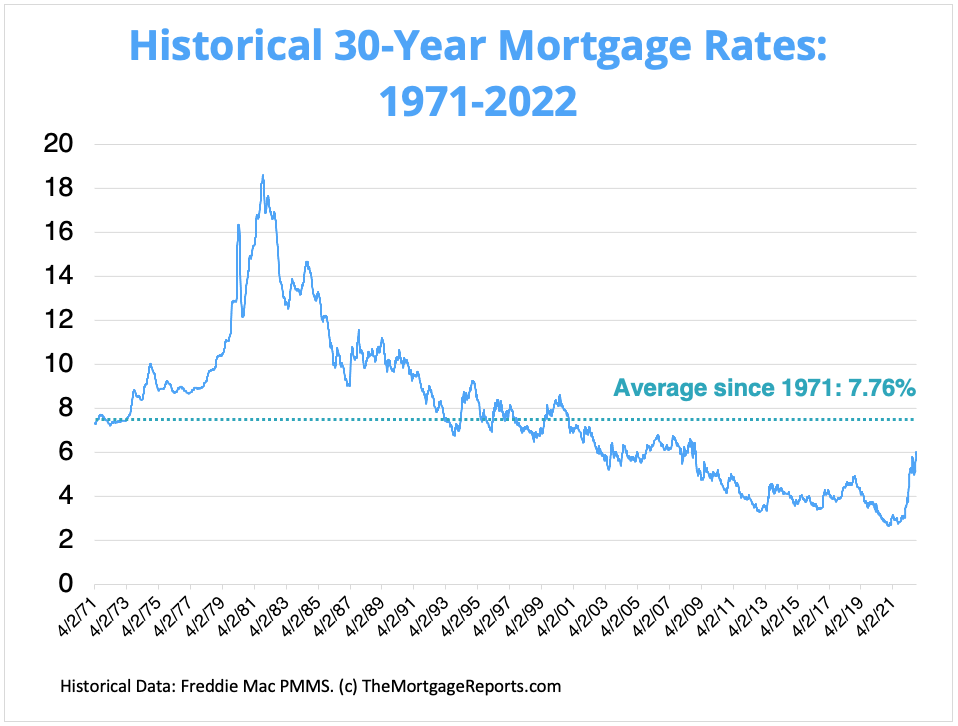

In the complex ecosystem of global finance, few numbers hold as much weight for the average consumer as the 30-year mortgage rate. It is the pulse of the housing market, a primary indicator of economic health, and the most significant factor in determining the long-term affordability of homeownership. For most individuals, a home is the largest investment they will ever make, and the interest rate attached to that purchase dictates their financial flexibility for decades. Understanding what this rate is, how it is calculated, and what forces drive its movement is essential for anyone looking to navigate the modern financial landscape.

The Economic Mechanics Behind the 30-Year Mortgage Rate

The 30-year mortgage rate is the interest rate charged by lenders on a loan used to purchase property, with the principal and interest paid back over a fixed three-decade term. While it might seem like a static number set by a local bank, the reality is far more dynamic. This rate is a reflection of the broader bond market, investor appetite for risk, and the overarching monetary policy of the country.

The Connection to the 10-Year Treasury Yield

A common misconception is that mortgage rates are tied directly to the Federal Funds Rate. In reality, the most accurate “north star” for the 30-year fixed-rate mortgage is the yield on the 10-year U.S. Treasury note. Investors treat mortgage-backed securities (MBS)—which are bundles of home loans sold on the secondary market—as alternatives to Treasury bonds.

Because the average 30-year mortgage is often paid off or refinanced within ten years, investors look for a yield that provides a “spread” over the risk-free return of government debt. When Treasury yields rise due to economic growth or inflation fears, mortgage rates almost always follow suit to remain competitive for investors.

The Role of Mortgage-Backed Securities (MBS)

When a bank issues you a mortgage, they rarely keep that debt on their books for 30 years. Instead, they sell the loan to entities like Fannie Mae or Freddie Mac, which package thousands of loans into Mortgage-Backed Securities. These are then sold to global investors, pension funds, and insurance companies. The “rate” you see on the news is essentially the price these investors demand in exchange for providing the liquidity that allows banks to keep lending. If investors perceive higher risk in the economy, they demand higher yields, which pushes mortgage rates upward.

Why the 30-Year Fixed-Rate Mortgage is the Industry Standard

While other countries often rely on adjustable-rate mortgages or shorter 5-year fixed terms that must be renewed, the 30-year fixed-rate mortgage remains the “gold standard” in the United States. Its popularity stems from its unique blend of consumer protection and long-term financial predictability.

Stability and Inflation Protection

The primary advantage of a 30-year fixed rate is the certainty it provides. Regardless of whether inflation skyrockets or the economy enters a recession, the homeowner’s monthly principal and interest payment remains identical from the first month to the 360th month. In an inflationary environment, this becomes a powerful wealth-building tool. As the cost of living and wages rise over time, the “real” value of that fixed mortgage payment actually decreases, allowing the homeowner to pay back the debt with “cheaper” dollars.

The Trade-off Between Monthly Cash Flow and Total Interest

The 30-year term is designed to maximize affordability. By stretching the repayment of the principal over 360 months, the monthly payment is significantly lower than that of a 15-year or 20-year mortgage. This allows families to qualify for more expensive homes or retain more of their monthly income for other investments. However, the price of this lower monthly payment is a much higher total interest cost over the life of the loan. In many interest rate environments, a borrower might end up paying more in total interest than the original purchase price of the home itself.

Factors That Influence Your Specific Mortgage Rate

While the “national average” 30-year mortgage rate is what makes headlines, the rate an individual borrower receives is highly personalized. Lenders use a process called “risk-based pricing” to determine how much interest to charge based on the likelihood of default.

Credit Scores and Financial Reliability

The most significant lever a borrower can pull to affect their rate is their FICO score. Lenders view the credit score as a window into the borrower’s financial discipline. A borrower with a score above 760 will typically receive the lowest available rates, while someone with a score in the 620s might face a rate that is 1% to 1.5% higher. Over 30 years, even a 1% difference in the interest rate can result in tens of thousands of dollars in extra payments.

The Impact of Down Payments and Loan-to-Value (LTV)

The amount of “skin in the game” a borrower has also dictates the rate. The Loan-to-Value (LTV) ratio measures the amount of the loan against the appraised value of the home. A 20% down payment (resulting in an 80% LTV) is generally the threshold for the best pricing. If a borrower puts down less, the lender perceives higher risk. Not only might the interest rate be higher, but the borrower will often be required to pay Private Mortgage Insurance (PMI), further increasing the effective cost of the debt.

Navigating Volatility in the Current Financial Market

The 30-year mortgage rate is notoriously sensitive to economic shifts. In recent years, we have seen historic lows followed by rapid ascents, driven by shifting fiscal policies and global events. Navigating this volatility requires a strategic approach to timing and financial planning.

Inflation and the Federal Reserve’s Mandate

Inflation is the natural enemy of fixed-income investors. Because a 30-year mortgage pays back a fixed amount of interest, high inflation erodes the value of those future payments. Consequently, when the Federal Reserve raises interest rates to combat inflation, mortgage rates tend to climb. Understanding the Federal Reserve’s “dot plot” and their stance on the Consumer Price Index (CPI) can give prospective homebuyers a preview of where mortgage rates might head in the coming quarters.

The Strategy of Rate Locks and Points

When a borrower finds a rate they are comfortable with during the home-buying process, they have the option to “lock” that rate for a specific period, usually 30 to 60 days. This protects them from market swings while the loan is being processed. Additionally, many borrowers choose to “buy down” their rate using discount points. One “point” typically costs 1% of the loan amount and reduces the interest rate by a predetermined margin (usually 0.25%). For those planning to stay in their home for many years, paying points upfront can be a savvy financial move that lowers the total cost of the loan over time.

Long-Term Financial Planning and the Mortgage Rate

Beyond the initial purchase, the 30-year mortgage rate remains a central pillar of an individual’s financial strategy. It affects everything from retirement planning to the ability to tap into home equity for future needs.

The Math of Amortization

Understanding the 30-year rate requires an understanding of the amortization schedule. In the early years of the loan, the vast majority of each monthly payment goes toward interest, with very little applied to the principal. As the years progress, the ratio shifts. For a homeowner, this means that equity is built slowly at first. Higher interest rates exacerbate this effect, making the “break-even” point for selling a home further away in the future.

Strategic Refinancing Opportunities

The 30-year mortgage is not necessarily a 30-year commitment. One of the most powerful financial maneuvers available to homeowners is the “rate-and-term refinance.” If market rates drop significantly below the rate a borrower is currently paying—typically by 0.5% to 1%—it may make sense to take out a new loan to pay off the old one. This can lower monthly obligations or shorten the loan term, potentially saving the borrower a fortune in interest. However, one must always calculate the “closing costs” of the new loan against the monthly savings to ensure the move is mathematically sound.

Conclusion: The Anchor of Personal Finance

The 30-year mortgage rate is far more than a statistic; it is the price of the American dream and a fundamental building block of personal wealth. It bridges the gap between the macroeconomics of the bond market and the microeconomics of a household budget. By understanding the forces that move this rate—from Treasury yields to credit scores—and the long-term implications of the 30-year term, consumers can make informed decisions that secure their financial future. Whether the rate is at a historic low or a cyclical high, the principles of leverage, amortization, and risk management remain constant. In the world of money, there is perhaps no single number more worthy of close study than the 30-year mortgage rate.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.