For most individuals, a home is the most significant purchase they will ever make. However, the sticker price of a property is only one part of the financial equation. The true cost of homeownership is dictated by housing interest rates. In the realm of personal finance, understanding these rates is not merely an academic exercise; it is a critical skill for wealth preservation and strategic investment.

Housing interest rates, or mortgage rates, represent the cost of borrowing money from a lender to purchase real estate. Expressed as a percentage, this rate determines your monthly payment and the total amount of interest you will pay over the life of the loan. Because mortgage terms often span 15 to 30 years, even a fractional difference in an interest rate can result in a variance of tens of thousands—or even hundreds of thousands—of dollars.

The Fundamental Mechanics of Housing Interest Rates

To navigate the world of real estate finance, one must first understand the different structures these rates can take and the external forces that move them.

Fixed-Rate vs. Adjustable-Rate Mortgages

The most common distinction in the mortgage market is between fixed-rate and adjustable-rate mortgages (ARMs). A fixed-rate mortgage locks in an interest rate for the entire duration of the loan. This provides the borrower with predictability; your principal and interest payment remains identical from the first month to the 360th month. This is often the preferred choice for those seeking long-term stability in their personal budget.

Conversely, an Adjustable-Rate Mortgage (ARM) usually offers a lower “teaser” rate for an initial period (such as five or seven years), after which the rate fluctuates based on market indices. While ARMs can be beneficial if interest rates are expected to drop or if the borrower intends to sell the property quickly, they carry significant risk. If market rates climb, your monthly obligation could increase substantially, potentially straining your financial liquidity.

The Role of the Central Bank and Monetary Policy

While commercial banks set the rates offered to consumers, they do not do so in a vacuum. In the United States, the Federal Reserve plays a pivotal role. When the “Fed” adjusts the federal funds rate—the rate at which banks lend to each other overnight—it creates a domino effect. While the Fed does not directly set mortgage rates, mortgage lenders track the yield on the 10-year Treasury note. As the Fed tightens monetary policy to combat inflation, Treasury yields typically rise, leading to higher housing interest rates. Conversely, in a sluggish economy, the Fed may lower rates to encourage borrowing and stimulate the housing market.

Principal, Interest, and the Amortization Schedule

Every mortgage payment is divided into two primary components: principal (the original amount borrowed) and interest (the fee for borrowing). In the early years of a mortgage, the vast majority of your monthly payment goes toward interest. This process is known as amortization. As the loan matures, the ratio shifts, and a larger portion of the payment is applied to the principal. Understanding this “front-loaded” interest structure is vital for homeowners who are considering selling their property within the first few years of ownership, as they may find they have built very little equity despite years of payments.

Determinants of Your Personal Mortgage Rate

Not every borrower is offered the same interest rate. Lenders assess risk through a variety of lenses, and your financial profile directly influences the “premium” you pay.

Credit Scores and Financial Reliability

Your credit score is perhaps the most influential factor in determining your specific housing interest rate. Lenders use scores from bureaus like Equifax, Experian, and TransUnion to gauge the likelihood that you will default on your loan. A borrower with a “prime” score (typically 740 or higher) will qualify for the lowest available rates. Someone with a “subprime” score may be charged a significantly higher rate to compensate the lender for the increased risk. Over a 30-year period, the difference between a 650 score and a 750 score can cost a homeowner a fortune in interest.

The Loan-to-Value (LTV) Ratio

The LTV ratio is a comparison between the amount of the loan and the appraised value of the property. For example, if you put down 20% on a $500,000 home, your loan is $400,000, resulting in an LTV of 80%. Generally, a lower LTV (meaning a larger down payment) results in a lower interest rate. Lenders view borrowers with more “skin in the game” as less likely to walk away from a property during a market downturn. Furthermore, if your LTV is higher than 80%, you are typically required to pay Private Mortgage Insurance (PMI), which adds to your monthly financial burden.

Debt-to-Income (DTI) and Employment History

Lenders also analyze your Debt-to-Income ratio, which measures your monthly debt obligations against your gross monthly income. A high DTI suggests that you may be overleveraged, prompting lenders to increase the interest rate or deny the loan altogether. Consistency in employment is another pillar of financial health; lenders prefer borrowers with a stable two-year history in the same field, as it provides confidence in the borrower’s continued ability to service the debt.

The Economic Ripple Effect: How Rates Shape the Housing Market

Housing interest rates do more than just affect individual bank accounts; they are the primary driver of the broader real estate economy.

Supply, Demand, and Home Pricing

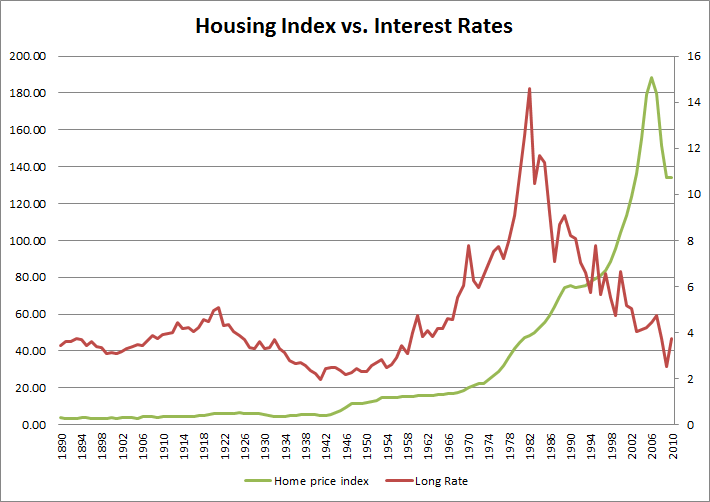

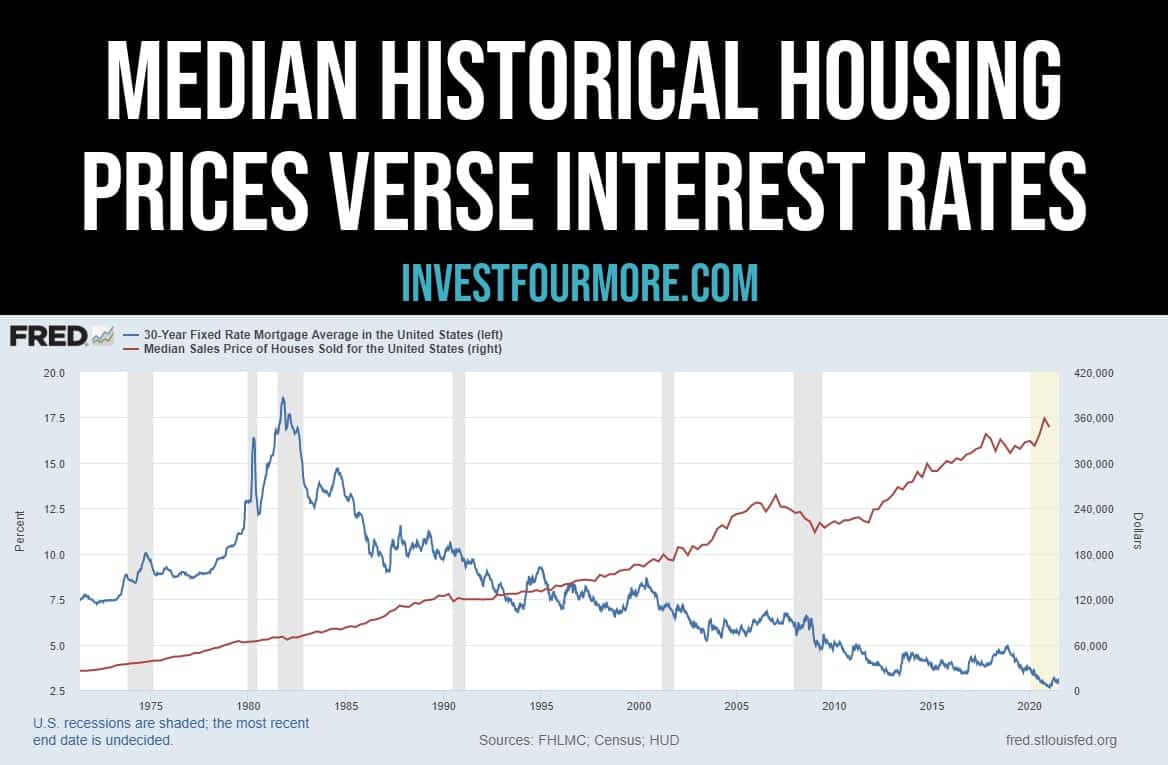

There is a general inverse relationship between interest rates and home prices. When rates are low, borrowing is cheap, which increases the purchasing power of buyers. This surge in demand often drives home prices upward. Conversely, when rates rise, the “cost of admission” for a home increases. Buyers who could previously afford a $400,000 home may find that at higher rates, their budget is restricted to $325,000. This cooling of demand often leads to a stagnation or decrease in property values, creating a “buyer’s market.”

The “Lock-In” Effect on Inventory

High interest rates can lead to a phenomenon known as the “lock-in” effect. This occurs when existing homeowners, who secured very low rates (perhaps 3% or lower) during previous years, are reluctant to sell their homes. Moving would require them to take on a new mortgage at a much higher current rate (perhaps 7%). This reluctance to move reduces the supply of existing homes for sale, which can paradoxically keep home prices high even when demand has cooled. For the personal finance strategist, this makes timing the market a complex challenge.

Inflation and Real Interest Rates

When discussing housing interest rates, one must consider inflation. The “nominal” interest rate is the number the bank gives you. The “real” interest rate is the nominal rate minus the inflation rate. If you have a 5% mortgage but inflation is running at 6%, the “real” cost of your debt is actually negative. In such an environment, debt can act as a hedge against inflation, as you are paying back the bank with dollars that are worth less than when you originally borrowed them.

Financial Strategies for Managing Interest Rate Risk

Smart money management involves not just accepting the rates offered, but actively working to optimize your position.

The Math of Refinancing

Refinancing is the process of replacing an existing mortgage with a new one, typically to take advantage of lower interest rates. However, refinancing is not free; it involves closing costs that can range from 2% to 5% of the loan amount. To determine if a refinance is financially sound, you must calculate the “break-even point”—the number of months it will take for the monthly savings to cover the cost of the new loan. If you plan to stay in the home longer than the break-even period, refinancing is a powerful tool for increasing your monthly cash flow.

Buying Down the Rate with Discount Points

At the time of purchase, many lenders offer the option to “buy down” the interest rate using discount points. One point typically costs 1% of the total loan amount and reduces the interest rate by a predetermined margin (often 0.25%). This is essentially an upfront interest payment. From a personal finance perspective, this is an investment. If you intend to keep the loan for many years, paying for points can save you significant money over the long term. If you plan to sell or refinance within a few years, the upfront cost may not be recovered.

Strategic Overpayment and Recasting

If you have a high housing interest rate, one of the most effective “investments” you can make is paying down your principal faster. By making extra payments toward the principal, you reduce the balance upon which interest is calculated. Some homeowners also utilize “mortgage recasting.” This involves making a large lump-sum payment toward the principal; the lender then recalculates the remaining monthly payments based on the new, lower balance. Unlike refinancing, recasting usually carries a very low fee and does not change the interest rate, but it significantly improves monthly cash flow.

The Long-Term Impact on Wealth Accumulation

Ultimately, housing interest rates are a primary determinant of a household’s net worth over time.

Equity Building vs. Interest Expense

Every dollar paid in interest is a dollar that does not contribute to your net worth. In the early stages of a high-interest mortgage, wealth accumulation is slow. By securing a lower rate, a larger portion of each payment builds equity—the portion of the home you actually own. Over 30 years, the difference between a 4% and a 7% interest rate on a $300,000 loan is over $200,000 in interest. That is $200,000 that could have been invested in a diversified portfolio or used for retirement.

Opportunity Cost of Capital

In personal finance, decisions must always be weighed against the “opportunity cost.” If you have extra cash, should you use it to pay down a 3% mortgage or invest it in the stock market where historical returns average 7–10%? When housing interest rates are low, it often makes more financial sense to carry the debt and invest surplus capital elsewhere. However, when mortgage rates rise toward 7% or 8%, the “guaranteed return” of paying down that debt becomes much more attractive compared to the volatility of the equity markets.

Tax Implications and Deductions

In many jurisdictions, the interest paid on a primary residence is tax-deductible up to certain limits. This effectively lowers the “after-tax” cost of the interest rate. For high-income earners in high-tax brackets, the mortgage interest deduction can significantly mitigate the impact of a higher rate. However, as standard deductions rise, fewer homeowners find it beneficial to itemize these deductions, making the headline interest rate even more critical to their bottom line.

In conclusion, housing interest rates are far more than a simple percentage on a loan application. They are a complex synthesis of global economics, central bank policy, and personal financial health. By understanding how these rates are calculated, how they influence the broader market, and how to strategically manage them, individuals can transform homeownership from a mere expense into a cornerstone of long-term financial prosperity.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.