For residents of the five boroughs, the convenience of owning a vehicle often comes with a significant financial trade-off. New York City is consistently ranked as one of the most expensive places in the United States to insure a car. Between the dense traffic of Manhattan, the narrow residential streets of Brooklyn, and the complex “no-fault” insurance laws of New York State, drivers face a unique set of fiscal challenges. Understanding how much car insurance costs in NYC—and more importantly, why it costs that much—is essential for any vehicle owner looking to optimize their personal finances and protect their assets.

Understanding the NYC Insurance Premium Landscape

The cost of car insurance in New York City is not a monolith; it varies significantly based on borough, coverage limits, and state mandates. On average, NYC drivers pay anywhere from $2,500 to over $5,000 per year for full coverage, which is substantially higher than the national average. This disparity is driven by the sheer density of the city, where the statistical probability of a fender bender or a theft is significantly higher than in suburban or rural environments.

Why NYC Costs More Than the National Average

The primary driver of high premiums in NYC is risk. Insurance companies are essentially risk-assessment entities. In a city where millions of people share limited road space, the frequency of claims is heightened. Additionally, New York City has a high cost of living, which translates to higher labor rates at auto repair shops and higher medical costs for injury claims. When an insurer calculates a premium for a Queens or Bronx resident, they are factoring in the increased likelihood of a claim and the elevated cost of settling that claim.

Minimum Coverage vs. Full Coverage in New York State

New York is a “no-fault” state, which means that regardless of who caused an accident, your own insurance provider pays for your medical treatments and lost wages through Personal Injury Protection (PIP). The state requires a minimum amount of liability coverage: $25,000 for bodily injury to one person, $50,000 for bodily injury to all persons, and $10,000 for property damage.

However, for most NYC drivers, carrying only the state minimum is a risky financial move. Given the high value of luxury vehicles often found on city streets, a $10,000 property damage limit can be exhausted in seconds. “Full coverage,” which includes collision and comprehensive insurance, is usually recommended to protect the vehicle owner’s investment, though it adds a substantial layer to the annual premium.

The No-Fault System and Its Impact on Your Wallet

The No-Fault system was designed to reduce litigation and speed up payments for medical bills. While it streamlines the recovery process for minor injuries, it often leads to higher base premiums. Drivers in NYC must pay for PIP coverage, and because the city sees a high volume of fraudulent medical claims, insurers pass those costs onto the consumer. Navigating this requires a clear understanding of your health insurance policy, as some drivers can coordinate benefits to avoid paying for redundant medical coverage.

Key Factors Influencing Your Personal Quotes

While geography sets the baseline for NYC insurance rates, individual financial and behavioral factors determine the final number on your bill. From a personal finance perspective, your car insurance premium is one of the few “fixed” costs that you actually have some control over by improving your profile as a borrower and driver.

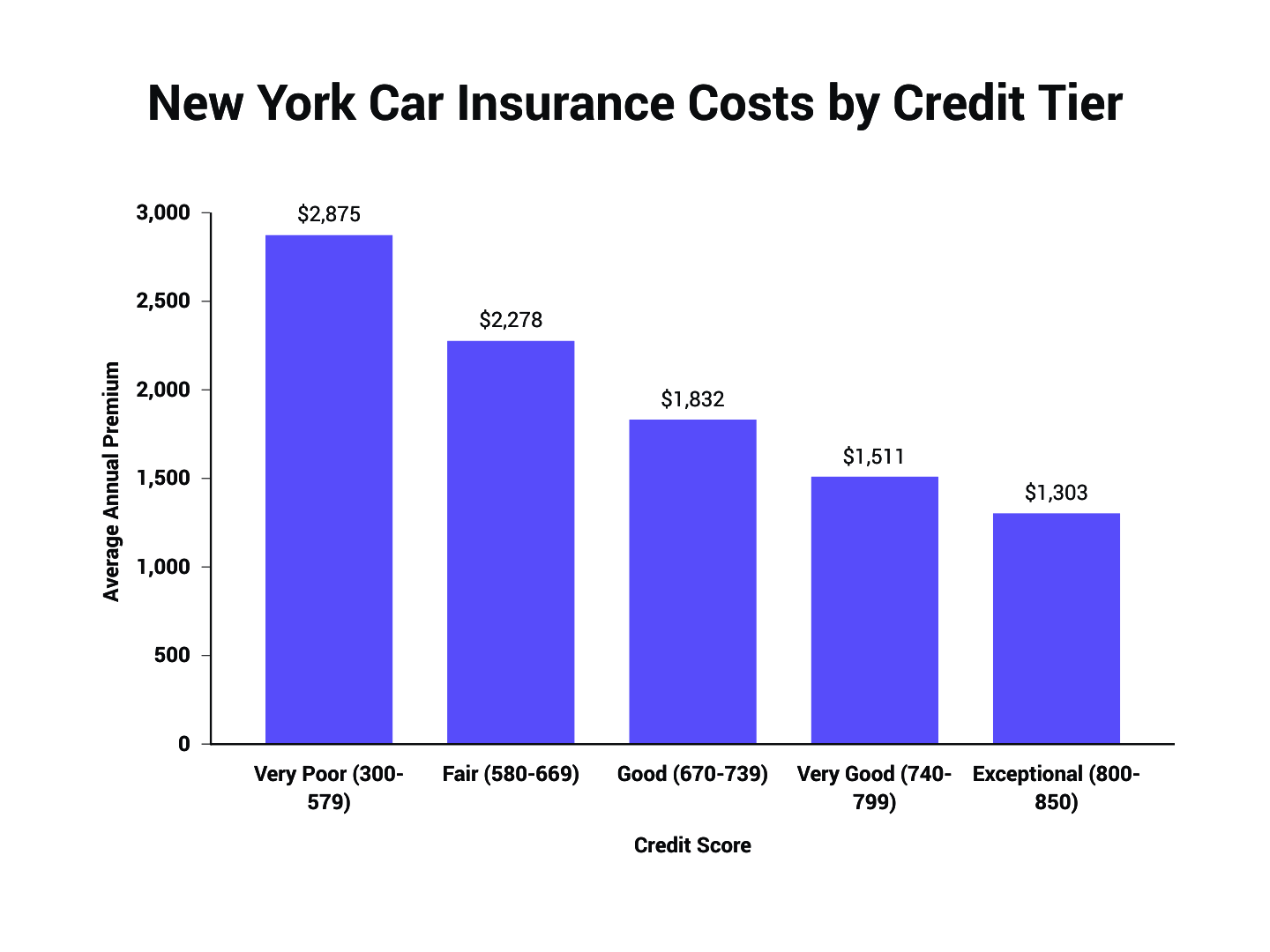

The Impact of Credit-Based Insurance Scores

In New York, insurers are permitted to use your credit history as a factor in determining your premium. From a financial management standpoint, this creates a direct link between your fiscal health and your driving costs. Statistical data suggests that individuals who manage their credit responsibly are less likely to file insurance claims. Consequently, a driver with an “excellent” credit score might pay thousands less over a five-year period than a driver with “poor” credit, even if both have identical driving records. Improving your credit score is, therefore, one of the most effective long-term strategies for lowering insurance costs.

Neighborhood Nuances: Brooklyn vs. Manhattan

Even within the city limits, premiums fluctuate wildly by zip code. A driver moving from a quiet neighborhood in Staten Island to a busy street in Bushwick, Brooklyn, might see their premium jump by 30% or more. This is due to localized data regarding localized crime rates (theft and vandalism) and traffic patterns. Manhattan often sees high rates due to the sheer volume of commercial traffic, while certain parts of the Bronx and Brooklyn are flagged for higher rates of uninsured motorists, which increases the cost of “Uninsured Motorist” coverage for everyone else in the area.

Vehicle Selection and Financial Depreciation

The type of car you drive in NYC significantly impacts your premium. A high-performance sports car or a luxury SUV is not only more expensive to repair but is also a more frequent target for theft. Furthermore, the financial concept of depreciation should play a role in your insurance choices. If you are driving an older vehicle with low market value, paying for collision and comprehensive coverage may no longer make sense, as the annual premium could eventually exceed the actual cash value of the car.

Strategies for Reducing Your Annual Premium

Managing the cost of car insurance requires a proactive approach to personal finance. It is not a “set it and forget it” expense. By utilizing specific financial strategies, NYC drivers can mitigate the “city tax” associated with their premiums.

Maximizing Discounts and Defensive Driving Courses

One of the most straightforward ways to save money is the New York State Point and Insurance Reduction Program (PIRP). By completing an approved defensive driving course, drivers are eligible for a mandatory 10% reduction in the base rate of their automobile and motorcycle liability and collision insurance premiums for three years. Additionally, many insurers offer discounts for “green” vehicles, vehicles equipped with anti-theft devices, or for students who maintain a high GPA.

The Role of Higher Deductibles in Cash Flow Management

In the world of personal finance, a deductible is a form of self-insurance. By choosing a higher deductible—moving from $500 to $1,000 or $2,000—you assume more risk in the event of an accident. In exchange, the insurance company lowers your monthly or annual premium. For NYC drivers with a healthy emergency fund, opting for a higher deductible can save hundreds of dollars annually. This is a strategic move: you are essentially betting on your own safe driving to keep that premium money in your high-yield savings account rather than giving it to the insurance company.

Bundling and Loyalty Programs

Most major carriers provide a “multi-policy” discount. If you rent an apartment or own a home in NYC, bundling your auto insurance with your renters or homeowners insurance can result in a 5% to 15% discount across both policies. However, a common financial mistake is staying loyal to a brand for too long without re-quoting. The “loyalty” discount is often smaller than the “new customer” incentive offered by a competitor.

Choosing the Right Provider for Your Financial Profile

Not all insurance companies view risk the same way. Some companies target high-net-worth individuals with specialized “white glove” service, while others use aggressive pricing to attract budget-conscious drivers.

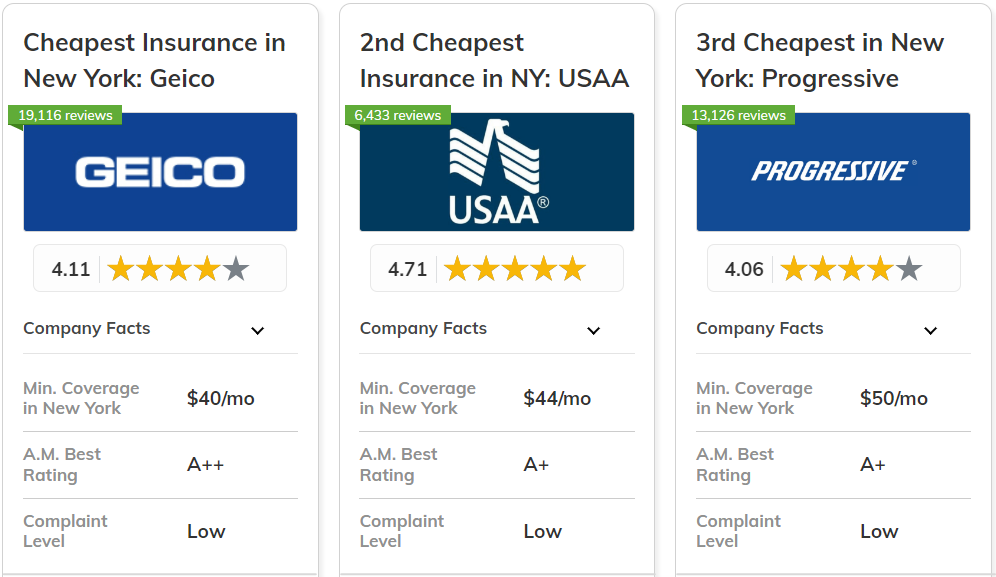

Comparing Regional Carriers vs. National Giants

National giants like Geico, State Farm, and Progressive have massive data sets and can often offer lower rates for drivers with “standard” profiles. However, regional carriers that specialize in the New York market may have a more nuanced understanding of NYC’s unique driving conditions and might offer more competitive rates for specific niches, such as ride-share drivers or owners of vintage cars. Comparing at least three quotes annually is a fundamental rule of financial literacy for car owners.

The Importance of Annual Reviews and Re-quoting

The insurance market is dynamic. Rates change based on the insurer’s recent loss ratios in your specific zip code. A company that was the cheapest for you last year might have increased its rates due to a surge in claims in your neighborhood. Conducting an annual financial audit of your recurring bills—starting with car insurance—ensures that you are not overpaying for coverage that could be obtained more cheaply elsewhere.

Utilizing Modern Financial Tools for Comparison

The rise of digital insurance marketplaces has made it easier than ever to compare costs. Instead of calling individual agents, drivers can use AI-driven tools to scan dozens of providers simultaneously. This transparency forces companies to be more competitive. When using these tools, ensure you are comparing “apples to apples”—the same liability limits, the same deductibles, and the same riders.

Conclusion: Balancing Protection and Cost

While “how much is car insurance in nyc” has no single answer, the financial reality is that it will likely be one of your largest annual expenses. By treating insurance as a flexible financial product rather than a fixed tax, you can take control of your costs. Through maintaining a high credit score, choosing your vehicle wisely, maximizing state-mandated discounts, and shopping around annually, you can ensure that you are protected against the chaos of NYC streets without compromising your long-term financial goals. In the end, the goal of car insurance is to protect your net worth; by managing its cost, you are simply protecting more of it.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.