For millions of drivers, auto insurance is a non-negotiable expense—a legal requirement in most places and a vital financial safety net against the uncertainties of the road. Yet, the cost of this essential protection can be a significant drain on personal finances, leading many to perpetually search for the elusive “cheap auto insurance.” The truth, however, is that there isn’t a single insurer universally hailed as the cheapest. Instead, affordability is a highly individualized metric, influenced by a complex web of factors unique to each driver, vehicle, and location.

Navigating the labyrinthine world of auto insurance can feel overwhelming, with countless providers vying for your business, each promising competitive rates. The quest for savings requires more than just a quick online search; it demands a strategic approach, a clear understanding of what drives premiums, and a willingness to explore all available avenues for cost reduction. This article will delve into the critical elements that shape your insurance costs, uncover proven strategies for reducing your premiums, and equip you with the knowledge to consistently find the most affordable coverage tailored to your specific needs, all within the crucial realm of personal finance and prudent money management.

The Core Factors Driving Auto Insurance Premiums

Understanding what dictates your auto insurance premium is the first step toward effectively managing and reducing this significant expense. Insurers meticulously assess risk, and your premium reflects their calculation of how likely you are to file a claim and how costly that claim might be. These factors fall into several key categories, painting a comprehensive picture of your individual risk profile.

Personal Profile: Age, Driving Record, and Location

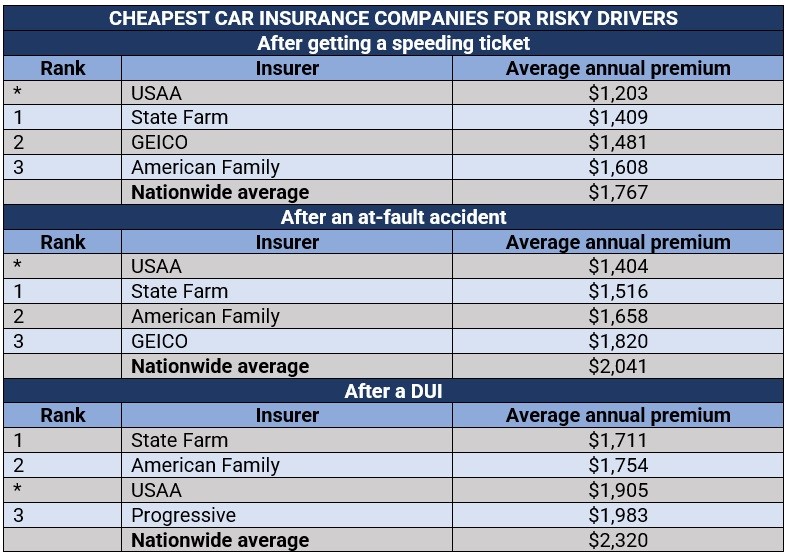

Your personal characteristics play an enormous role in determining your insurance rates. Younger, less experienced drivers, particularly those under 25, typically face higher premiums due to statistical evidence suggesting a greater likelihood of accidents. Conversely, mature drivers with a clean record often enjoy lower rates. Your driving history is paramount; a spotless record free of accidents, tickets, or serious violations (like DUIs) is your strongest asset for securing lower costs. Conversely, even minor infractions can significantly elevate your premiums for years. Finally, where you live matters. Urban areas with higher traffic density, crime rates, and greater incidence of accidents often translate to higher premiums than quieter, rural locales. Even within the same city, specific zip codes can have vastly different rates based on local claim statistics.

Vehicle Characteristics: Make, Model, and Safety Features

The car you drive is another major component of your premium calculation. High-performance sports cars, luxury vehicles, and models frequently targeted by thieves often come with higher insurance costs due due to their higher repair costs, greater potential for speed-related accidents, or increased theft risk. On the other hand, vehicles with excellent safety ratings, advanced safety features (like automatic emergency braking, lane-keeping assist, or anti-theft devices), and a lower likelihood of severe damage in a collision can lead to significant savings. Electric vehicles and hybrids sometimes qualify for eco-friendly discounts, while older, less valuable cars might allow you to opt for less comprehensive coverage, further reducing costs.

Coverage Choices and Deductibles

Perhaps the most direct control you have over your premium is the type and amount of coverage you choose, along with your deductible. Most states require a minimum level of liability insurance, which covers damages you cause to others. However, opting for higher liability limits, along with collision (for damage to your car in an accident) and comprehensive (for non-collision damage like theft, vandalism, or natural disasters) coverage, will increase your premium. Personal injury protection (PIP) or medical payments coverage, uninsured/underinsured motorist coverage, and roadside assistance are additional options that add to the total cost. Your deductible—the amount you pay out-of-pocket before your insurance kicks in—is inversely related to your premium. A higher deductible typically means a lower premium, as you’re assuming more of the initial financial risk.

Financial Health: Credit Score and Payment History

While it might seem unrelated, your credit score, or more accurately, your “credit-based insurance score,” is a significant factor in many states. Insurers use these scores as a predictor of future claim likelihood, with data suggesting a correlation between a higher credit score and a lower probability of filing claims. A strong credit history signals financial responsibility, which insurers often interpret as a lower risk. Similarly, your payment history with previous insurers can influence your rates; a history of late payments or policy cancellations can lead to higher premiums or even difficulty securing coverage. Maintaining a healthy credit score and a consistent payment record is therefore a crucial, yet often overlooked, aspect of managing your auto insurance costs.

Proven Strategies for Finding Affordable Auto Insurance

Armed with an understanding of what influences your premiums, you can now proactively implement strategies to lower your costs. The search for cheap auto insurance is less about finding a single “best” company and more about optimizing your profile and making informed choices.

Embrace Comparison Shopping: Your Most Potent Weapon

The single most effective strategy for finding affordable auto insurance is to shop around and compare quotes from multiple providers. Prices for identical coverage can vary by hundreds, if not thousands, of dollars between different insurers because each company has its own proprietary risk assessment models, pricing strategies, and target customer demographics. Do not make the mistake of renewing with your current provider out of habit without first seeing what competitors offer. Utilize online comparison tools, which allow you to get multiple quotes by entering your information just once. Alternatively, work with an independent insurance agent who can shop various carriers on your behalf. Make sure you are comparing apples to apples—identical coverage limits, deductibles, and endorsements—to get an accurate picture. Repeat this process at least once a year, or whenever you experience a significant life event.

Leverage Discounts: Don’t Leave Money on the Table

Insurance companies offer a wide array of discounts, and often, customers don’t even realize they qualify for them. Always ask your agent or review your policy details for every possible discount. Common discounts include:

- Multi-Policy/Bundling Discount: Combining your auto insurance with home, renters, or life insurance from the same provider can lead to substantial savings on both policies.

- Safe Driver Discount: For drivers with a clean record over a specified period (e.g., 3-5 years).

- Good Student Discount: Available to high school and college students who maintain a certain GPA.

- Low Mileage Discount: For those who drive less than a certain number of miles annually.

- Anti-Theft Device Discount: For vehicles equipped with approved alarm systems or tracking devices.

- Defensive Driving Course Discount: Completing an approved defensive driving course can sometimes earn you a discount and may even help remove points from your record.

- Loyalty Discount: Some insurers reward long-term customers.

- Professional/Alumni Association Discount: Many insurers partner with various organizations, offering special rates to members.

- Payment Discounts: For paying in full, setting up automatic payments, or receiving paperless statements.

It’s critical to ask about all available discounts and ensure they are applied to your policy. A few minutes of inquiry could save you a significant amount.

Optimize Your Coverage and Deductibles

While it’s tempting to cut coverage to the bare minimum to save money, this can be a financially risky move. Instead, review your policy annually to ensure your coverage aligns with your current needs and assets. If you have an older car with a low market value, the cost of collision and comprehensive coverage might outweigh the potential payout if the car is totaled. In such cases, you might consider dropping these coverages.

Regarding deductibles, strategically increasing yours can significantly lower your premiums. If you can comfortably afford to pay a higher deductible (e.g., $1,000 instead of $500) out of pocket in the event of a claim, you’ll see a noticeable reduction in your annual premium. Just ensure you have the funds readily available in an emergency fund to cover that higher deductible if an accident occurs. This is a classic financial trade-off: assume more immediate risk to reduce ongoing expenses.

Improve Your Driver Profile and Credit Score

Investing in yourself can directly translate to lower insurance costs. Maintaining a clean driving record by avoiding accidents and traffic violations is paramount. Every ticket or at-fault accident can impact your rates for several years. For new drivers, or those looking to refresh their skills, completing an accredited defensive driving course can not only lead to discounts but also make you a safer driver overall, reducing the likelihood of future claims.

As previously mentioned, your credit-based insurance score is influential in most states. Regularly monitoring your credit report, disputing errors, and practicing sound financial habits—paying bills on time, managing debt responsibly, avoiding excessive new credit applications—can gradually improve your credit score. A higher credit score often signals lower risk to insurers, translating directly into more favorable insurance rates over time. This synergy between general financial health and insurance costs underscores the holistic nature of personal finance.

Beyond the Basics: Advanced Tactics for Maximum Savings

For those committed to squeezing every possible saving out of their auto insurance, several more advanced tactics can yield substantial benefits. These strategies often involve embracing new technologies or making larger lifestyle and financial adjustments.

Explore Telematics and Usage-Based Insurance

Telematics, or usage-based insurance (UBI), is a growing trend that allows insurers to collect data on your actual driving habits through a device plugged into your car’s diagnostic port or via a smartphone app. This data typically tracks factors such as mileage, speed, braking habits, time of day you drive, and even cornering. If you’re a safe, low-mileage driver, a UBI program can offer significant discounts—sometimes up to 30% or more. Companies like Progressive (Snapshot), Allstate (Drivewise), and State Farm (Drive Safe & Save) are prominent examples. While some drivers might be wary of data privacy concerns, for many, the potential for personalized savings based on actual driving behavior makes it an attractive option for reducing costs.

Bundling Policies for Comprehensive Savings

While mentioned as a discount, bundling warrants a deeper dive as a strategic financial move. Beyond just auto and home, consider bundling other types of insurance if offered by the same carrier, such as boat, RV, motorcycle, or even umbrella policies. The discounts for bundling multiple lines of insurance can be incredibly lucrative, often ranging from 10% to 25% across all policies. This strategy not only simplifies your insurance management by consolidating policies with a single provider but also entrenches you as a more valuable customer, potentially opening doors to additional benefits or preferred treatment in the future. Always calculate the total cost of bundled policies versus separate policies from different carriers to ensure the savings are genuine.

Consider Your Vehicle Choice Wisely

While not always feasible for everyone, the type of car you purchase has long-term implications for your insurance costs. Before buying a new or used vehicle, it’s prudent financial planning to get insurance quotes for a few models you’re considering. You might be surprised by the significant differences in premiums even between similar vehicles. Factors like the vehicle’s safety ratings, its statistical likelihood of being stolen, the cost of parts and repairs, and its engine size all contribute to insurance pricing. Opting for a car with a solid safety record, good theft deterrents, and readily available, inexpensive parts can translate to lower insurance premiums throughout your ownership. This forward-thinking approach integrates insurance costs into your overall vehicle budget, preventing sticker shock down the road.

When and How to Re-evaluate Your Policy

Finding cheap auto insurance isn’t a one-time event; it’s an ongoing process. Your life changes, market rates fluctuate, and new discounts emerge. Regular review and proactive adjustments are key to continuous savings.

Annual Reviews and Life Event Triggers

Make it a habit to review your auto insurance policy at least once a year, ideally a few weeks before its renewal date. This gives you ample time to shop around and compare rates without feeling rushed. Even if your rates haven’t changed drastically, another insurer might now offer a better deal. Furthermore, certain life events should immediately trigger a policy review, as they can significantly impact your rates or coverage needs:

- Buying a new car: Always get quotes before you finalize the purchase.

- Moving to a new address: Even within the same city, your zip code can change your rates.

- Getting married or divorced: Marital status is a rating factor.

- Adding or removing a driver: Especially when a teen driver gets their license or an adult child moves out.

- Changing jobs or retiring: This might impact your annual mileage or car usage.

- Improving your credit score: Inform your insurer if you believe your credit health has significantly improved.

- Paying off your car loan: You might be able to drop comprehensive and collision coverage, depending on the car’s value.

Each of these events presents an opportunity to adjust your coverage and potentially find new savings.

Working with Agents vs. Direct Insurers

When seeking quotes, you have two primary avenues: working with an insurance agent or going directly to insurers.

- Independent Agents: These agents work with multiple insurance companies and can provide quotes from several providers at once, often offering personalized advice and helping you identify specific discounts. They can be particularly useful for those with complex insurance needs or those who prefer a human touch. Their services are typically free to you, as they earn commission from the insurers.

- Captive Agents: These agents work exclusively for one insurance company (e.g., State Farm, Allstate). They have deep knowledge of their company’s products and discounts but can only offer policies from that single provider.

- Direct Insurers: Many companies, like GEICO or Progressive, allow you to get quotes and purchase policies directly online or over the phone. This can be convenient and efficient, often giving you direct access to online-only discounts.

There’s no single “best” method; it often depends on your preference for human interaction versus self-service, and the complexity of your situation. For comprehensive results, consider using a combination of methods—get a few direct online quotes and then consult with an independent agent to see if they can beat or match those offers.

Conclusion

The quest for cheap auto insurance is a continuous journey of informed decision-making and proactive management, deeply intertwined with your overall financial well-being. There is no one-size-fits-all answer to “who has cheap auto insurance” because the “cheapest” policy is the one that offers you the right amount of coverage for the lowest premium, tailored specifically to your unique circumstances.

By understanding the factors that influence your premiums, diligently comparing quotes, leveraging every available discount, and strategically optimizing your coverage and deductibles, you can significantly reduce this essential household expense. Furthermore, by maintaining a clean driving record and fostering good financial health, you’re investing in a future of more affordable insurance. Make it a habit to review your policy annually and adapt it as your life changes. With a strategic approach, you can confidently navigate the auto insurance market, ensuring you have robust protection without overpaying, ultimately bolstering your personal finances.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.