For millions of Americans, Social Security represents a cornerstone of their retirement security, offering a reliable stream of income that can significantly impact financial well-being in later life. Yet, understanding how your individual benefit amount is calculated can feel like navigating a complex maze. It’s not a one-size-fits-all figure; rather, it’s a highly personalized sum determined by a confluence of factors, primarily your earnings history and the age at which you choose to claim. Demystifying this process is crucial for effective retirement planning, enabling you to make informed decisions that could optimize your financial future. This article aims to break down the intricacies of Social Security benefit calculations, providing clarity on the key variables and practical steps you can take to ascertain your estimated benefit.

Understanding the Pillars of Your Social Security Benefit

At its core, your Social Security benefit is an earned entitlement, directly tied to your lifetime contributions to the system through payroll taxes. However, simply knowing you’ve paid in isn’t enough; the specific amount you receive hinges on several critical components.

Your Earnings History: The Foundation

The bedrock of your Social Security benefit is your earnings record. The Social Security Administration (SSA) meticulously tracks your taxable earnings throughout your working life. When it comes time to calculate your retirement benefit, the SSA focuses on your 35 highest-earning years. It’s important to note that these earnings are “indexed” to account for changes in average wages over time. This indexing process ensures that earlier earnings reflect their relative value compared to more recent ones, preventing inflation from unfairly diminishing their impact. For instance, an income earned in the 1980s is adjusted upwards to compare fairly with an income earned today. If you have fewer than 35 years of earnings, the missing years will be recorded as zeros, which can significantly lower your average and, consequently, your benefit amount. This underscores the importance of consistent employment and adequate earnings throughout your career.

Age at Claiming: A Crucial Decision

Perhaps the most impactful decision you’ll make regarding your Social Security benefit is when to start receiving it. The SSA establishes a Full Retirement Age (FRA), which is the age at which you are entitled to 100% of your primary insurance amount (PIA). For individuals born in 1960 or later, the FRA is 67. For those born between 1943 and 1959, the FRA gradually increases from 66 to 67.

You have the flexibility to claim benefits as early as age 62, but doing so will result in a permanent reduction of your monthly payment. This reduction can be substantial, decreasing your benefit by as much as 30% if you claim at 62 instead of your FRA. Conversely, delaying your claim past your FRA—up to age 70—can lead to significantly higher monthly payments. For each year you delay past your FRA, your benefit amount increases by a certain percentage, known as delayed retirement credits, typically accumulating to an 8% increase per year, up to age 70. This means delaying from age 67 to 70 could boost your monthly payment by 24%. The choice of when to claim requires careful consideration of your financial needs, health, life expectancy, and other retirement income sources.

Social Security Credits: Eligibility Requirements

Before any benefit calculation can even begin, you must first be eligible to receive Social Security retirement benefits. Eligibility is determined by earning “credits” through your work. In 2024, you earn one credit for every $1,730 in earnings, up to a maximum of four credits per year. To qualify for retirement benefits, you generally need 40 credits, which translates to 10 years of working and earning at least the minimum amount each year. Once you’ve earned 40 credits, you are “fully insured” and eligible to receive benefits based on your earnings record.

Deconstructing the Benefit Calculation Process

While the concept of earnings history and claiming age is straightforward, the actual mathematical process the SSA uses to arrive at your benefit amount involves a few more steps.

Average Indexed Monthly Earnings (AIME) in Detail

After identifying your 35 highest-earning years and indexing those earnings, the SSA sums these indexed earnings and divides the total by the number of months in 35 years (420 months). This calculation yields your Average Indexed Monthly Earnings (AIME). The AIME is a crucial figure, as it represents your average monthly earnings over your career, adjusted for historical wage growth. It’s the primary input for determining your basic benefit amount.

Primary Insurance Amount (PIA): Your Baseline Benefit

The AIME is then used to calculate your Primary Insurance Amount (PIA). Your PIA is the monthly benefit you would receive if you started claiming benefits exactly at your Full Retirement Age. The PIA calculation is progressive, meaning lower-income earners receive a higher percentage of their average indexed monthly earnings than higher-income earners. This progressivity is achieved through a “bend point” formula. The formula applies different percentages to different segments of your AIME. For example, in 2024, the formula for someone turning 62 in 2024 is:

- 90% of the first $1,174 of AIME, plus

- 32% of AIME between $1,174 and $7,078, plus

- 15% of AIME over $7,078.

These “bend points” are indexed annually, just like earnings, to keep pace with wage growth. The result of this calculation is your monthly PIA, the starting point for any further adjustments based on when you claim your benefits.

Adjustments for Early or Delayed Claiming

Once your PIA is established, it is then adjusted based on your claiming age.

- Early Claiming (Before FRA): If you claim benefits before your FRA, your PIA is reduced. The reduction is calculated on a monthly basis. For example, if your FRA is 67, and you claim at 62, your benefit will be reduced by 5/9 of 1% for each of the first 36 months, and then by 5/12 of 1% for each additional month. This can lead to a significant permanent reduction.

- Delayed Claiming (After FRA): If you delay claiming past your FRA, your PIA is increased by delayed retirement credits. These credits add to your benefit amount for each month you delay, up to age 70. The annual rate of increase varies based on your birth year, but for those born in 1943 or later, it’s 8% per year. These credits are a powerful incentive to delay if your financial situation allows, as they result in a substantially higher monthly payment for the rest of your life.

Beyond Your Individual Retirement Benefit: Other Considerations

Social Security offers more than just individual retirement benefits. Understanding these related provisions can further illuminate your overall financial picture.

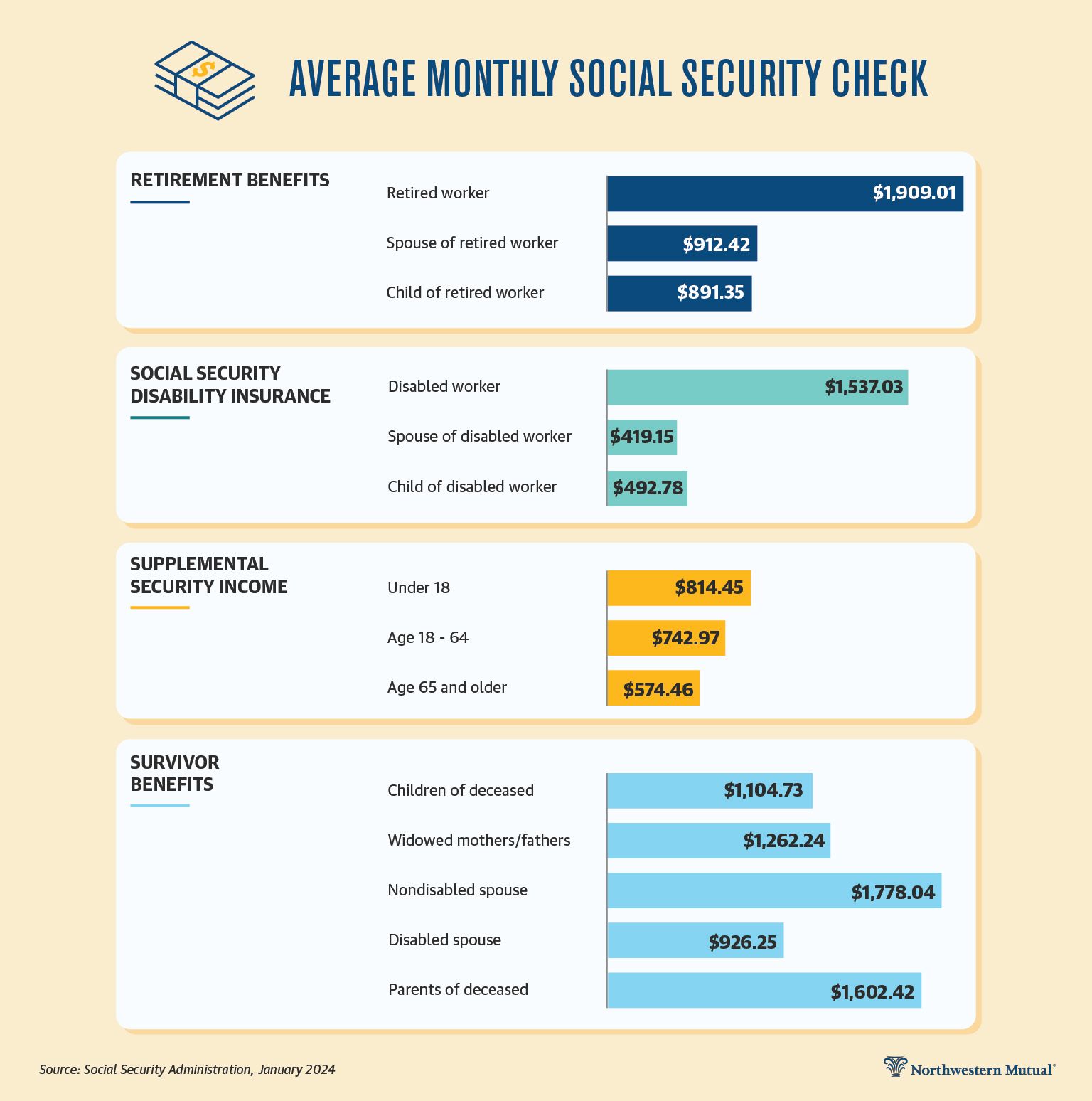

Spousal and Survivor Benefits

Social Security is a family-oriented program. If you are married, divorced (under certain conditions), or widowed, you may be eligible for benefits based on your spouse’s or ex-spouse’s earnings record, even if your own earnings record is limited.

- Spousal Benefits: A spouse can claim up to 50% of their partner’s PIA if they claim at their own FRA. If they claim early, their spousal benefit will also be reduced. A key rule is that the primary earner must have already filed for their benefits for the spouse to claim on their record.

- Survivor Benefits: If your spouse passes away, you (as a widow or widower) may be eligible for survivor benefits, which can be up to 100% of your deceased spouse’s benefit amount if you claim at your FRA. Dependent children may also qualify for benefits. These provisions are critical safety nets for families.

Cost-of-Living Adjustments (COLAs)

To help maintain the purchasing power of benefits against inflation, Social Security benefits are typically subject to annual Cost-of-Living Adjustments (COLAs). These adjustments are usually announced in the fall and are based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If the CPI-W increases, your Social Security benefit will generally increase the following year. While not guaranteed every year, COLAs are a vital feature that helps retirees keep pace with rising costs of living.

Taxation of Social Security Benefits

It’s a common misconception that Social Security benefits are entirely tax-free. For many beneficiaries, a portion of their benefits may be subject to federal income tax, depending on their “provisional income.” Provisional income includes your adjusted gross income, tax-exempt interest, and one-half of your Social Security benefits. If your provisional income exceeds certain thresholds, up to 50% or even 85% of your benefits may be taxable. State taxation of benefits also varies, with some states taxing them and others not. It’s wise to consult with a tax professional to understand your specific tax obligations.

How to Find Your Social Security Benefit Estimate

Given the complexity, how can you find your personal benefit estimate without performing intricate calculations yourself? Fortunately, the SSA provides convenient tools.

Creating Your My Social Security Account

The most efficient and accurate way to get personalized information is to create a secure My Social Security account online at ssa.gov. This free service allows you to:

- View your complete earnings record, year by year, and check for accuracy.

- Get personalized estimates of your future retirement benefits at different claiming ages (e.g., age 62, your FRA, and age 70).

- See estimates for disability and survivor benefits.

- Manage your benefits if you are already receiving them.

Having an online account is highly recommended for everyone, regardless of age, as it serves as a critical financial planning tool and helps prevent identity theft.

Understanding Your Social Security Statement

If you prefer a physical document or haven’t set up an online account, the SSA used to mail annual statements to all workers. While this practice has largely shifted to digital access, you can still request a copy of your Social Security Statement. This statement provides a detailed summary of your earnings history and estimated future benefits under various scenarios. It’s crucial to review your earnings history carefully on the statement (or in your online account) to ensure all your past earnings are correctly recorded. Any discrepancies should be reported to the SSA promptly, as errors could negatively impact your future benefits.

Making Informed Decisions About Your Social Security

Your Social Security benefit is more than just a number; it’s a vital component of your broader retirement strategy. Understanding its potential value empowers you to make smarter financial choices.

Integrating Social Security into Your Retirement Plan

Think of Social Security as one leg of a multi-legged stool that supports your retirement. It provides a foundational layer of income, but it’s rarely sufficient to cover all retirement expenses for most people. Therefore, it’s essential to integrate your estimated Social Security benefits with other sources of retirement income, such as 401(k)s, IRAs, pensions, and personal savings. Analyzing how much Social Security will provide helps you determine how much more you need to save and invest to achieve your desired retirement lifestyle. Strategic claiming decisions for Social Security should be made in conjunction with your overall financial plan.

Seeking Professional Guidance

Given the numerous variables and the potential long-term impact of your claiming decision, consulting with a qualified financial advisor can be invaluable. A professional can help you analyze your specific situation, including your health, longevity expectations, other assets, and family circumstances, to model different claiming scenarios. They can provide personalized advice on when to start benefits, how to integrate them with your other investments, and strategies for minimizing taxes. The SSA itself can also provide assistance and clarity on benefit rules and regulations.

Understanding “What is my Social Security benefit amount?” is a critical step towards securing a comfortable and stable retirement. By familiarizing yourself with the calculation methods, exploring your personalized estimates through the SSA, and integrating this knowledge into your comprehensive financial plan, you can make confident decisions that pave the way for a more prosperous future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.