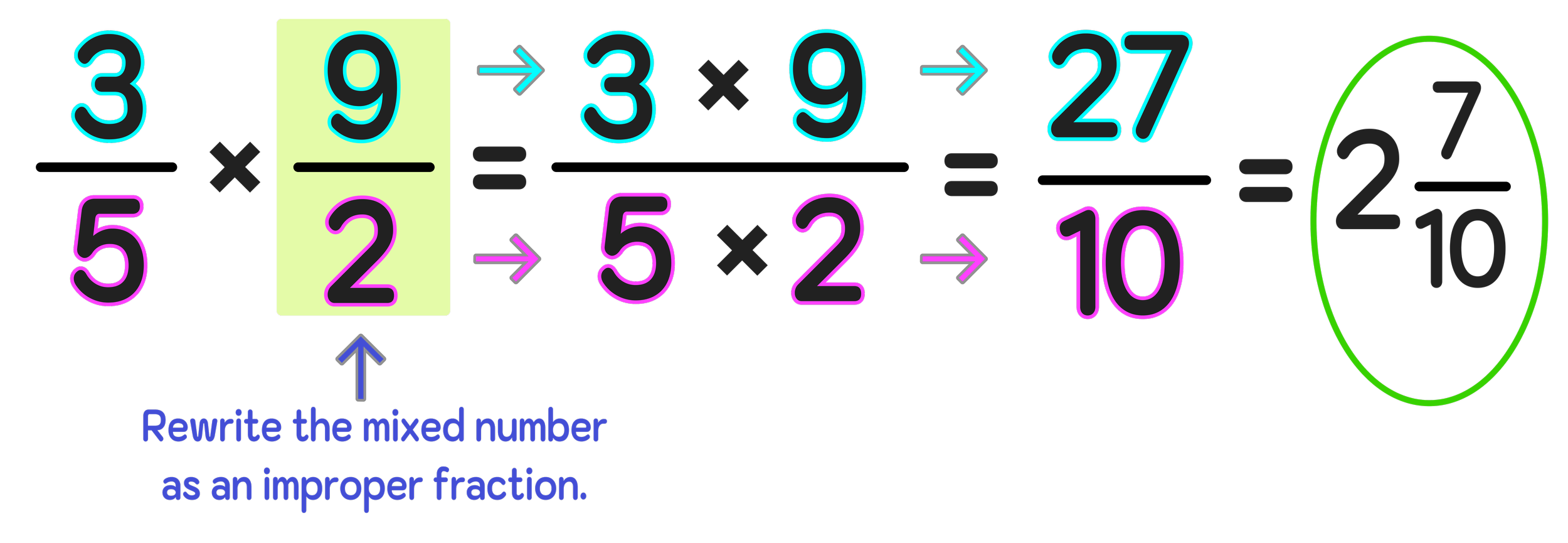

At first glance, the question “What is 2/3 of 3/5?” might appear to be a purely academic exercise, a relic from a primary school mathematics textbook. It’s a fundamental problem in fractions, a building block of arithmetic. The direct answer is straightforward: to find a fraction of a fraction, you multiply them. So, (2/3) * (3/5) = (23) / (35) = 6/15, which simplifies to 2/5.

However, to relegate this seemingly simple calculation to the realm of elementary math is to miss its profound relevance and practical application in the world of money and finance. Far from being a triviality, understanding how to work with fractions – and indeed, the underlying principles they represent – is an indispensable skill for navigating personal finance, making savvy investment decisions, managing business operations, and ultimately, building enduring wealth. In an era saturated with complex financial instruments and algorithmic trading, the foundational literacy that allows one to confidently answer “What is 2/3 of 3/5?” is often the very bedrock upon which sound financial decisions are made. This article delves into why mastering such basic fractional concepts is not just about getting the right answer on a test, but about empowering yourself with robust financial acumen.

The Ubiquity of Fractions in Personal Finance

Every individual, regardless of income level, engages with fractions daily, often without consciously realizing it. From budgeting to managing debt, fractional thinking underpins many critical personal finance decisions.

Budgeting and Income Allocation

One of the most immediate applications of fractions in personal finance is in budgeting. When you create a budget, you are essentially allocating portions of your total income towards different categories: savings, housing, food, transportation, debt repayment, and discretionary spending.

For instance, a common budgeting rule is the “50/30/20 rule,” where 50% of your income goes to needs, 30% to wants, and 20% to savings and debt repayment. These percentages are, in essence, fractions (1/2, 3/10, 1/5). But what if your financial plan is more granular?

Consider a scenario where you’ve decided to dedicate a specific portion of your income to investments. If you allocate 2/3 of your disposable income to savings, and then decide that 3/5 of that specific savings portion should be directed into a long-term investment fund, you are literally performing the calculation “2/3 of 3/5” to determine the final fraction of your disposable income going into that fund. The result, 2/5, means 40% of your disposable income is earmarked for that investment. Without this fractional understanding, accurately tracking and adhering to such a detailed budget becomes challenging, leading to potential overspending or under-saving.

Debt Management and Interest Calculations

Debt, particularly consumer debt, often involves complex interest calculations that are easier to grasp with a solid understanding of fractions and percentages. When you pay off a credit card bill, a portion goes to the principal, and a portion goes to interest. The interest rate itself is a fraction (e.g., 18% APR is 18/100).

Understanding minimum payments and their impact requires fractional thinking. A minimum payment might cover only a small fraction of the total balance, predominantly interest, leaving the principal largely untouched. If you decide to pay an additional 2/3 of your minimum payment, and the minimum payment itself represents 3/5 of the interest accrued, knowing how to calculate 2/3 of 3/5 helps you understand how much extra you’re really paying towards reducing the interest burden or accelerating principal repayment. This clarity empowers you to strategize debt reduction more effectively, avoiding the trap of perpetual interest payments.

Savings Goals and Milestones

Achieving significant savings goals, whether for a down payment on a house, retirement, or a child’s education, often involves breaking down the large goal into smaller, manageable fractions. You might aim to save 1/4 of the total cost in the first year, 1/3 of the remainder in the second, and so on. Each step involves calculating a fraction of a remaining fraction. If your goal requires saving a total of $100,000, and you’ve already accumulated 3/5 of it, you then need to calculate what 2/3 of the remaining 2/5 of the goal is to set your next savings target. These incremental calculations provide motivation and a clear roadmap, turning an intimidating large sum into achievable financial milestones.

Investment Strategies and Portfolio Management

The world of investing is deeply steeped in fractional calculations. From asset allocation to understanding returns, fractions are the language of portfolio construction and performance analysis.

Asset Allocation and Diversification

Asset allocation is perhaps the most critical decision an investor makes. It involves distributing investment funds among different asset classes, such as stocks, bonds, real estate, and commodities, to optimize risk and return. This is fundamentally a fractional exercise. A common recommendation might be to allocate 60% (3/5) to stocks and 40% (2/5) to bonds. But what if you further diversify within these categories?

For instance, you might decide that within your 3/5 stock allocation, 2/3 should be invested in growth stocks, and the remaining 1/3 in value stocks. Here, the “2/3 of 3/5” calculation directly tells you that 2/5 (or 40%) of your total portfolio is in growth stocks. This precision is vital for managing exposure, aligning investments with risk tolerance, and ensuring adequate diversification. Without this foundational understanding, investors risk misallocating capital, leading to unintended concentrations or insufficient diversification.

Understanding Returns, Yields, and Performance

Investment returns are frequently expressed as percentages, which are just fractions out of 100. A stock that returned 15% means it grew by 15/100 of its initial value. Similarly, dividend yields, bond yields, and expense ratios of funds are all fractional representations. When comparing two investment options, one offering a certain yield on 2/3 of your capital and another offering a different yield on the remaining 3/5 of that particular portion, understanding how these fractions combine is crucial for calculating your overall blended return. Compound interest, often hailed as the “eighth wonder of the world,” relies heavily on fractional growth over time, where each period’s earnings become part of the principal for the next period’s calculation. A lack of fractional fluency can lead to a misunderstanding of how returns accumulate, especially over long investment horizons.

Real Estate and Fractional Ownership

In modern investment landscapes, fractional ownership has become an increasingly popular model, particularly in real estate, art, and even high-value collectibles. This allows multiple investors to own a portion of an asset, making expensive investments more accessible. If you own 2/3 of a property, and then decide to sell 3/5 of your share to another investor, the question “2/3 of 3/5” directly determines the new fractional ownership structure and the value of the transaction. This understanding is critical for calculating equity, distributing rental income, and managing buy-sell agreements within these structures.

Business Finance and Entrepreneurship

For entrepreneurs and business owners, fractions are not just useful; they are indispensable for making informed operational, financial, and strategic decisions.

Profit Sharing and Equity Distribution

In partnerships or startups, how profits are shared or equity is distributed among founders and early employees is a common and often sensitive area. These agreements are almost always expressed in fractional or percentage terms. If a business partnership dictates that Partner A receives 2/3 of the net profits, and Partner B receives the remaining 1/3, but then Partner A has an agreement with a key consultant to give them 3/5 of their own share (i.e., Partner A’s 2/3 share) as a performance bonus, knowing that 2/3 of 3/5 equals 2/5 of the total net profits going to the consultant is vital for accurate accounting and maintaining transparent relationships. Miscalculations here can lead to legal disputes and significant financial loss.

Calculating Margins, Discounts, and Ratios

Businesses constantly calculate profit margins (gross profit / revenue), operating margins (operating income / revenue), and discount percentages (discount amount / original price). All are fractional expressions critical for assessing financial health and pricing strategies.

If a product normally sells for a certain price, but you offer a 2/3 discount, and then a customer applies a further 3/5 coupon on top of the discounted price, knowing the sequential fractional reduction is crucial for determining your actual revenue. For example, if a product is $100, a 2/3 discount means you pay $100 * (1 – 2/3) = $100 * (1/3) = $33.33. If a 3/5 coupon is applied to this discounted price, the final price is $33.33 * (1 – 3/5) = $33.33 * (2/5) = $13.33. Understanding “fraction of a fraction” prevents pricing errors that can erode profitability.

Financial Ratios and Performance Metrics

Financial analysts and business managers rely heavily on financial ratios to gauge a company’s performance, liquidity, solvency, and efficiency. Ratios such as current ratio (current assets / current liabilities), debt-to-equity ratio (total debt / shareholder equity), and return on equity (net income / shareholder equity) are all fractional representations. Interpreting these ratios requires an intuitive grasp of how fractions work. A company’s inventory turnover rate, for example, might indicate that 2/3 of its stock is sold within a quarter, and of that, 3/5 generates a specific profit margin. These insights drive operational improvements and strategic planning.

Avoiding Common Financial Pitfalls

The seemingly simple act of understanding “2/3 of 3/5” serves as a foundational defense against common financial misconceptions and errors.

Misinterpreting Percentages and Proportions

One of the most frequent financial missteps stems from a misunderstanding of how percentages and fractions combine or compound. Many people fall prey to promotions like “an additional 20% off the sale price,” not realizing that the “additional 20%” is calculated on the already reduced price, not the original. This is a classic “fraction of a fraction” scenario. Misinterpreting these proportions can lead consumers to believe they are getting a better deal than they are, or investors to miscalculate their true returns or losses. The clarity provided by fractional thinking helps to cut through marketing jargon and understand the real financial implications.

The Cost of Financial Illiteracy

At its core, the inability to confidently answer “What is 2/3 of 3/5?” when it applies to a real-world financial scenario is a symptom of financial illiteracy. This illiteracy has tangible costs. Individuals might miss out on optimal savings rates, incur unnecessary interest charges, make suboptimal investment choices, or even fall victim to predatory lending practices simply because they cannot accurately calculate proportions, percentages, and fractional impacts. A strong command of basic mathematical concepts, particularly fractions, empowers individuals to critically evaluate financial products, terms, and conditions, leading to more informed and advantageous decisions. It’s the difference between blindly accepting terms and understanding them deeply enough to negotiate or seek better alternatives.

Conclusion

The question “What is 2/3 of 3/5?” yields the simple answer of 2/5. However, the true value of this seemingly basic mathematical problem lies not just in the numerical solution, but in its profound implications for financial literacy and decision-making. From managing personal budgets and allocating investment portfolios to understanding complex business financials and avoiding costly pitfalls, a solid grasp of fractions is an indispensable tool.

In a world where financial decisions can have long-lasting consequences, the ability to confidently navigate percentages, proportions, and fractional relationships empowers individuals to take control of their financial destiny. It underscores the vital truth that robust financial health isn’t built on complex algorithms or insider knowledge, but on a strong foundation of fundamental mathematical understanding. Embrace the power of fractions, and you embrace a clearer, more confident path to financial mastery.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.