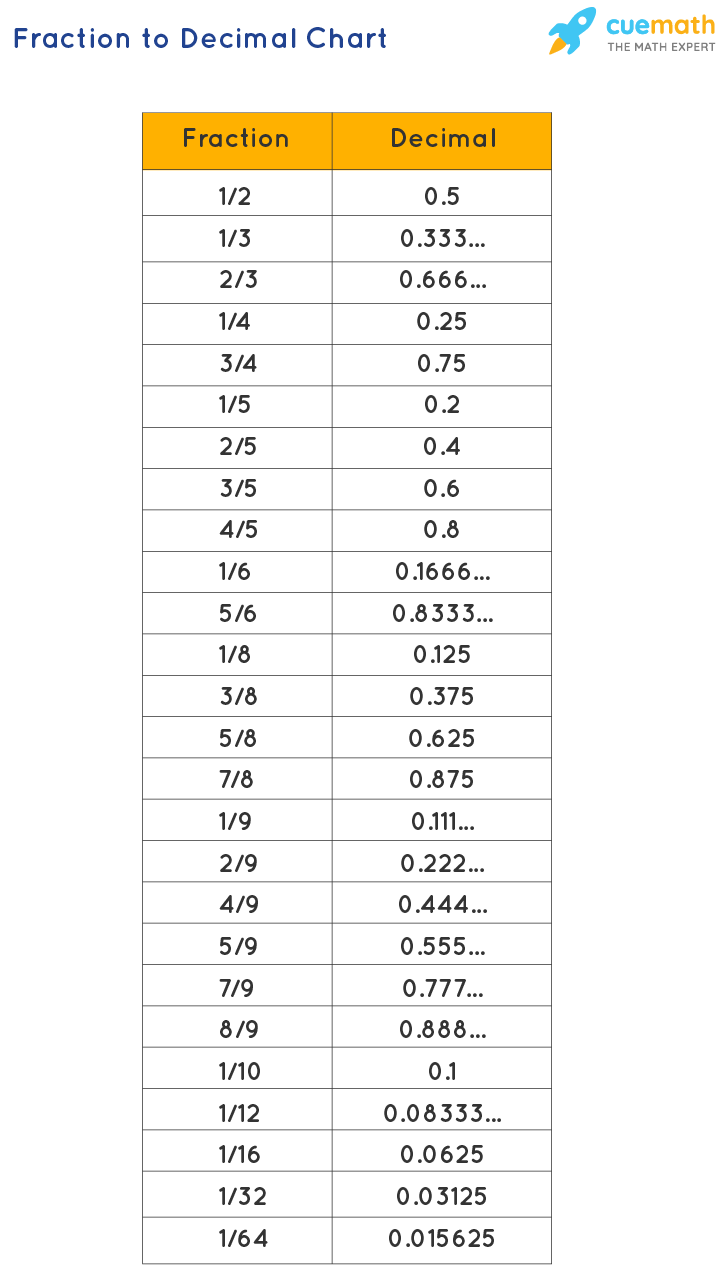

At first glance, the question “what is 1/12 as a decimal” seems like a rudimentary math problem, a relic from grade school arithmetic. It’s a simple division: 1 divided by 12 equals 0.08333… (with the 3 repeating infinitely). However, to dismiss this fundamental conversion as trivial would be a significant oversight, especially when it comes to personal finance, investing, and business management. In the intricate world of money, understanding fractions and their decimal equivalents isn’t just about passing a math test; it’s a foundational skill that empowers individuals and businesses to make informed decisions, accurately track financial performance, and strategically plan for the future.

From budgeting household expenses and calculating monthly loan payments to understanding investment returns and analyzing business performance metrics, the ability to effortlessly navigate between fractions, decimals, and percentages is indispensable. This article delves into the profound financial significance of seemingly simple mathematical conversions, using the example of 1/12 to illustrate how a solid grasp of these basics underpins virtually every aspect of sound financial management.

The Foundation: Understanding Fractions and Decimals in Finance

Financial literacy often begins with a firm grasp of fundamental mathematical concepts. Fractions, decimals, and percentages are the ABCs of financial calculations, serving as different ways to represent parts of a whole. In the financial realm, where precision can mean the difference between profit and loss, understanding these interconnections is paramount.

Basic Conversion: From Fraction to Decimal

The conversion of 1/12 to a decimal is straightforward division. When you divide 1 by 12, the result is 0.083333… This is a repeating decimal, meaning the ‘3’ continues indefinitely. In most financial applications, however, you’ll encounter a need to round this number to a practical number of decimal places. For currency, this often means two decimal places (e.g., $0.08), though for interest rates or more precise calculations, four or more decimal places (e.g., 0.0833) are common to minimize rounding errors over time.

This simple act of conversion—taking a fraction and turning it into a decimal—is the bedrock upon which more complex financial analyses are built. It translates abstract proportions into quantifiable figures that are universally understood and easily manipulated by financial tools.

Why Decimals Dominate Financial Calculations

While fractions are intuitive for conceptualizing parts of a whole (like “one-twelfth”), decimals are the lingua franca of financial computation. There are several compelling reasons for this dominance:

- Ease of Computation: Decimals are far simpler to work with in calculators, spreadsheets, and financial software. Adding, subtracting, multiplying, and dividing decimals is more straightforward and less prone to manual error than performing the same operations with fractions, especially when dealing with uncommon denominators.

- Standardization: Financial statements, interest rates, tax rates, and investment returns are almost universally expressed in decimals or percentages (which are decimals multiplied by 100). This standardization allows for clear, unambiguous communication and comparison of financial data across different institutions, markets, and time periods.

- Precision and Scalability: Decimals allow for greater precision when needed. While fractions can represent any rational number, decimals provide a more flexible framework for expressing very small or very large proportions and are easily scaled up or down in calculations without losing clarity.

- Direct Conversion to Percentages: Decimals convert directly into percentages, a format frequently used to communicate rates, growth, and change. For example, 0.0833 is 8.33%, a form commonly seen in annual percentage rates (APRs), discounts, or stock returns. This seamless conversion makes financial reporting and analysis much more accessible.

Practical Applications of 1/12 (and Similar Concepts) in Personal Finance

The seemingly simple conversion of 1/12 to a decimal takes on significant practical weight when applied to personal financial management. It’s a concept that directly impacts how individuals budget, save, invest, and manage debt.

Budgeting and Monthly Allocations

One of the most common applications of 1/12 in personal finance is in budgeting. Many financial commitments, such as salaries, insurance premiums, property taxes, or subscription services, are quoted annually but paid or received monthly. To effectively manage cash flow and create a realistic budget, these annual figures must be broken down into their monthly equivalents.

- Annual to Monthly Expense Conversion: If your annual car insurance premium is $1,200, dividing it by 12 (or multiplying by 1/12, or 0.0833) immediately tells you that you need to budget $100 per month for this expense. Similarly, if your property taxes are $3,000 annually, setting aside $250 each month (1/12 of $3,000) prevents a large, unexpected bill.

- Savings Goals: The “1/12 rule” can also apply to saving. If you have an annual savings goal of $6,000, aiming to save $500 each month (1/12 of $6,000) makes the larger goal manageable and achievable. This structured approach is a cornerstone of effective financial planning.

- Income Distribution: For individuals who receive bonuses or irregular income annually, understanding how to effectively distribute a portion of that lump sum across the subsequent 12 months can stabilize their monthly finances.

Understanding Interest Rates and Returns

The world of lending and investing heavily relies on interest rate calculations, where the concept of 1/12 (or similar fractional breakdowns) is critical.

- Annual Percentage Rate (APR) to Monthly Interest: Loans like mortgages, car loans, and credit cards typically quote an Annual Percentage Rate (APR). To calculate your monthly interest payment, you often need to convert the annual rate to a monthly rate. A simple, though sometimes inaccurate for compounding interest, way to estimate this is to divide the APR by 12. For instance, a credit card with an 18% APR might charge approximately 1.5% interest per month (18% / 12). While actual compounding calculations are more complex, this initial division provides a valuable estimate.

- Investment Returns: Similarly, understanding monthly investment returns requires converting annual figures. If a mutual fund reports an average annual return, investors often want to project what that translates to on a monthly basis. This helps in comparing investments or tracking progress toward monthly financial goals.

Investment Portfolios and Diversification

In investment management, fractions and decimals are crucial for portfolio allocation and understanding fractional ownership.

- Asset Allocation: Investors decide to allocate specific portions of their portfolio to different asset classes (e.g., 60% stocks, 30% bonds, 10% cash). While these are typically expressed as percentages, they originate from fractional concepts. You might decide to dedicate 1/12 of your new investment capital to a specific emerging market fund each month as part of a dollar-cost averaging strategy.

- Fractional Shares: The rise of commission-free trading and micro-investing platforms has made fractional share ownership accessible. Instead of buying a whole share of a high-priced stock, you can invest a specific dollar amount, owning a fraction of a share (e.g., 0.0833 of a share if your investment happens to perfectly align with 1/12 of the share price). This allows for greater diversification and accessibility for smaller investors.

Business Finance: Beyond Simple Division

While the principles remain the same, the application of fractions and decimals in business finance scales up in complexity and impact. Businesses rely on these mathematical tools for everything from financial reporting and performance analysis to strategic planning and tax compliance.

Financial Ratios and Performance Metrics

Financial ratios are the backbone of business analysis, providing insights into a company’s liquidity, profitability, solvency, and efficiency. These ratios are almost always expressed as decimals or percentages.

- Monthly Performance vs. Annual Targets: Companies set annual revenue, profit, and expense targets. Regularly comparing monthly performance to 1/12 of the annual target helps management assess progress, identify variances, and make timely adjustments. For example, if a company aims for $1.2 million in annual revenue, it needs to generate $100,000 each month (1/12 of $1.2 million) to stay on track.

- Working Capital Management: Understanding the flow of funds over a 12-month cycle, often broken down into monthly segments, is crucial for managing working capital. This involves analyzing current assets and liabilities, and predicting needs for short-term financing based on monthly operational cycles.

Cost Allocation and Revenue Recognition

Businesses often incur costs or earn revenue that needs to be spread out over time, rather than recognized all at once. This is where amortization, depreciation, and subscription revenue models heavily rely on fractional and decimal concepts.

- Depreciation and Amortization: Assets like machinery or software have a useful life beyond one year. Businesses allocate their cost over this useful life. For example, a piece of equipment costing $12,000 with a 10-year useful life might be depreciated by $100 per month ($12,000 / 120 months = $100), or $1,200 annually (1/10 of $12,000). This systematic allocation (often monthly) impacts a company’s reported profit and tax liability.

- Subscription Revenue: A software company selling an annual subscription for $1,200 cannot recognize all $1,200 as revenue upfront. Instead, it recognizes $100 per month (1/12 of the total) over the 12-month subscription period. This ensures that revenue is matched to the period in which the service is provided, adhering to accounting principles.

Tax Planning and Compliance

Businesses face numerous tax obligations, many of which involve monthly or quarterly calculations based on annual projections.

- Estimated Tax Payments: Many businesses are required to pay estimated taxes throughout the year, often on a monthly or quarterly basis, to avoid penalties. These payments are typically calculated as a fraction (e.g., 1/12 or 1/4) of the anticipated annual tax liability.

- Sales Tax and VAT Returns: Depending on jurisdiction, businesses collect sales tax or Value Added Tax (VAT) and remit it to the authorities monthly or quarterly. Accurate tracking and calculation of these amounts, often involving percentages, is critical for compliance.

The Role of Financial Tools and Avoiding Common Pitfalls

While understanding the underlying math is crucial, modern financial management heavily relies on digital tools. Knowing how these tools work and being aware of potential pitfalls can significantly enhance financial accuracy.

Leveraging Spreadsheets and Financial Software

Spreadsheets (like Excel or Google Sheets) and specialized financial software are indispensable for handling complex financial calculations. They automate conversions and allow for sophisticated modeling.

- Automated Calculations: These tools can instantly convert 1/12 to 0.083333… and perform subsequent calculations with high precision. They streamline budgeting, forecasting, and scenario planning.

- Data Analysis: Financial software can analyze trends, build reports, and visualize data, making it easier to interpret complex financial information. However, the accuracy of the output depends entirely on the accuracy of the input and the user’s understanding of the underlying principles. You must understand why you are dividing by 12, even if the software does the division for you.

The Importance of Precision and Rounding

One of the most common pitfalls in financial calculations is improper rounding.

- When to Use More Decimal Places: For calculations involving interest rates, particularly over long periods (like a 30-year mortgage), using more decimal places (e.g., 0.083333 instead of 0.08) can significantly impact the final sum. Small rounding differences, when compounded, can lead to substantial discrepancies.

- When to Round to Two Decimal Places: For final currency amounts, rounding to two decimal places (e.g., $8.33) is standard. The key is to perform all intermediate calculations with maximum precision and only round the final result for presentation.

Beyond 1/12: Developing Broader Financial Literacy

The example of 1/12 serves as a gateway to broader financial literacy. Mastery of such basic conversions builds confidence and lays the groundwork for understanding more advanced financial concepts.

- Compound Interest: Understanding how decimals and percentages work is essential for grasping the power of compound interest, both in saving and in debt.

- Inflation: The eroding power of inflation is often expressed in percentages, and understanding how these numbers translate to actual purchasing power requires a good grasp of decimal math.

- Present and Future Value: Financial planning often involves calculating the present value of future cash flows or the future value of current investments, all of which rely heavily on percentages and decimal conversions.

In conclusion, the simple mathematical question “what is 1/12 as a decimal” unlocks a critical door to financial empowerment. While the answer itself (0.0833…) is straightforward, its implications for personal and business finance are far-reaching. From the daily mechanics of budgeting and expense tracking to the strategic nuances of investment management and corporate financial planning, a solid understanding of fractions, decimals, and their interrelationships is not merely academic—it is a cornerstone of sound financial decision-making and a prerequisite for achieving lasting financial success. Embracing these fundamental mathematical concepts is the first step toward gaining clarity, control, and confidence in your financial journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.