The question, “How much for retirement?” is perhaps one of the most significant and anxiety-inducing inquiries for individuals across all age groups. It’s a question that doesn’t have a simple, universally applicable answer, but rather a deeply personal one shaped by aspirations, current circumstances, and future unknowns. Far from a mere numerical calculation, determining your retirement nest egg involves a comprehensive understanding of your desired lifestyle, potential income sources, the relentless march of inflation, and the ever-present specter of healthcare costs. This article will delve into the intricacies of projecting your retirement needs, explore common guidelines, and equip you with a framework to build your personalized roadmap to financial independence.

The Elusive “Magic Number”: Why It’s Not One-Size-Fits-All

The quest for a single, definitive “retirement number” is often misguided. What constitutes a comfortable or even luxurious retirement for one person might feel restrictive to another. Your individual retirement target is a dynamic figure, influenced by a multitude of personal and economic factors. Understanding these variables is the first critical step in demystifying the “how much” question.

Lifestyle Expectations and Desires

At the heart of your retirement calculation lies your vision for those golden years. Do you dream of extensive international travel, pursuing expensive hobbies, or perhaps relocating to a high-cost-of-living area? Or do you envision a simpler life, enjoying local community activities and spending more time with family? Your desired lifestyle directly dictates your projected annual expenses. Those who wish to maintain or even elevate their pre-retirement living standards will naturally require a significantly larger nest egg than those content with a more modest existence. Consider housing (will your mortgage be paid off?), transportation, entertainment, dining out, and leisure activities. A detailed assessment of these categories in your imagined retirement life is paramount.

Longevity and Healthcare Costs

People are living longer, healthier lives, which is excellent news, but it also means your retirement savings need to stretch further. The average retirement duration can easily extend to 20, 30, or even more years. Compounding this extended timeline are the soaring costs of healthcare. Even with Medicare, out-of-pocket expenses for premiums, deductibles, co-pays, and services not covered can be substantial. Long-term care, for instance, is a significant financial burden that many fail to adequately plan for. Ignoring potential healthcare costs is one of the biggest pitfalls in retirement planning and can rapidly deplete even a substantial savings account. Factor in an escalating budget for medical expenses as part of your annual projections.

Inflation: The Silent Eroder of Purchasing Power

Inflation is the quiet antagonist of long-term financial planning. What $100 buys today will likely require $150 or more in 20-30 years. A retirement income that seems adequate now will gradually lose its purchasing power over time. If you retire with $1 million today, and inflation averages 3% annually, in 20 years, that $1 million will have the purchasing power of approximately $550,000. It’s crucial to account for inflation in your calculations, either by assuming a higher rate of return on investments or by projecting your future expenses in inflation-adjusted dollars. A common approach is to assume your investments need to grow faster than the rate of inflation to maintain or increase your real wealth.

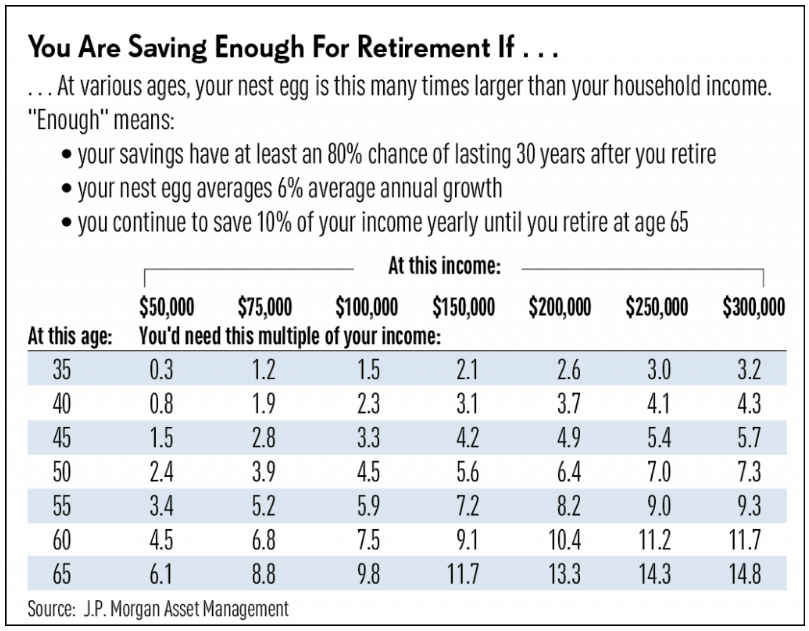

Common Rules of Thumb and Starting Points

While a personalized approach is ideal, several widely accepted rules of thumb can provide a useful starting point and a quick reality check for your retirement planning. These guidelines offer a broad framework that can be adapted to your unique situation.

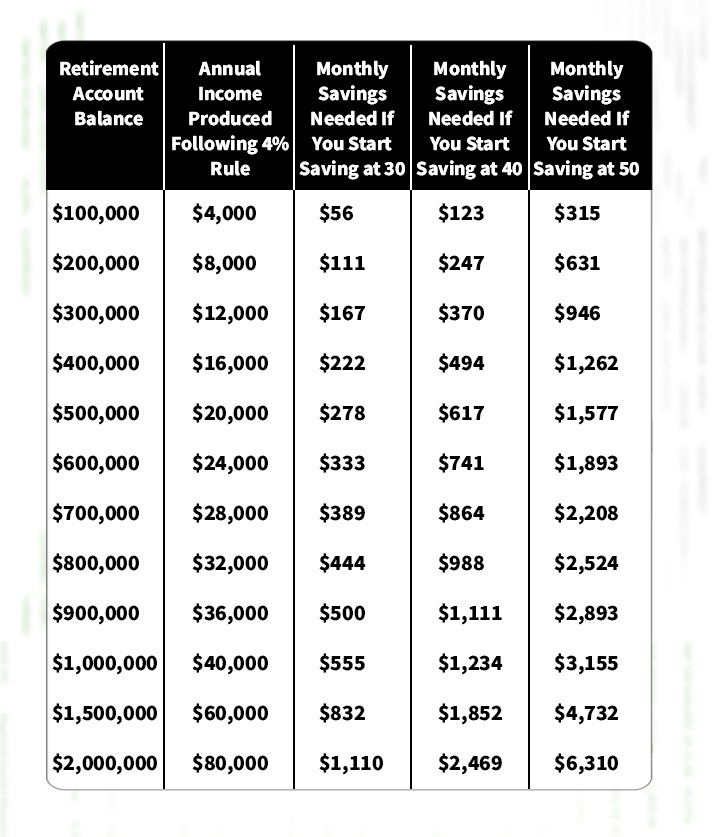

The 4% Rule: A Popular Guideline

The “4% Rule” suggests that retirees can safely withdraw 4% of their initial retirement portfolio balance each year, adjusted for inflation in subsequent years, without running out of money for at least 30 years. For example, if you have a $1,000,000 portfolio, you could withdraw $40,000 in your first year of retirement. This rule implies that to generate an annual income of $X, you would need $X / 0.04 (or 25 times $X) saved. So, if you aim for $80,000 per year, you’d need $2 million saved. While popular, the 4% rule originated from specific market conditions and asset allocations, and its applicability in today’s lower-return environment is often debated. It serves as a good estimation, but not a guarantee.

The 70-80% Income Replacement Ratio

Another frequently cited benchmark is the “70-80% income replacement ratio.” This rule posits that you’ll need to replace approximately 70-80% of your pre-retirement annual income to maintain your lifestyle in retirement. The rationale is that certain expenses, such as commuting costs, work-related clothing, and payroll taxes, diminish or disappear in retirement, while others, like healthcare, might increase. If you earn $100,000 annually before retirement, you would aim to have enough income to generate $70,000 – $80,000 per year in retirement. This simplifies the planning process by tying your retirement needs directly to your current income, assuming a relatively consistent lifestyle.

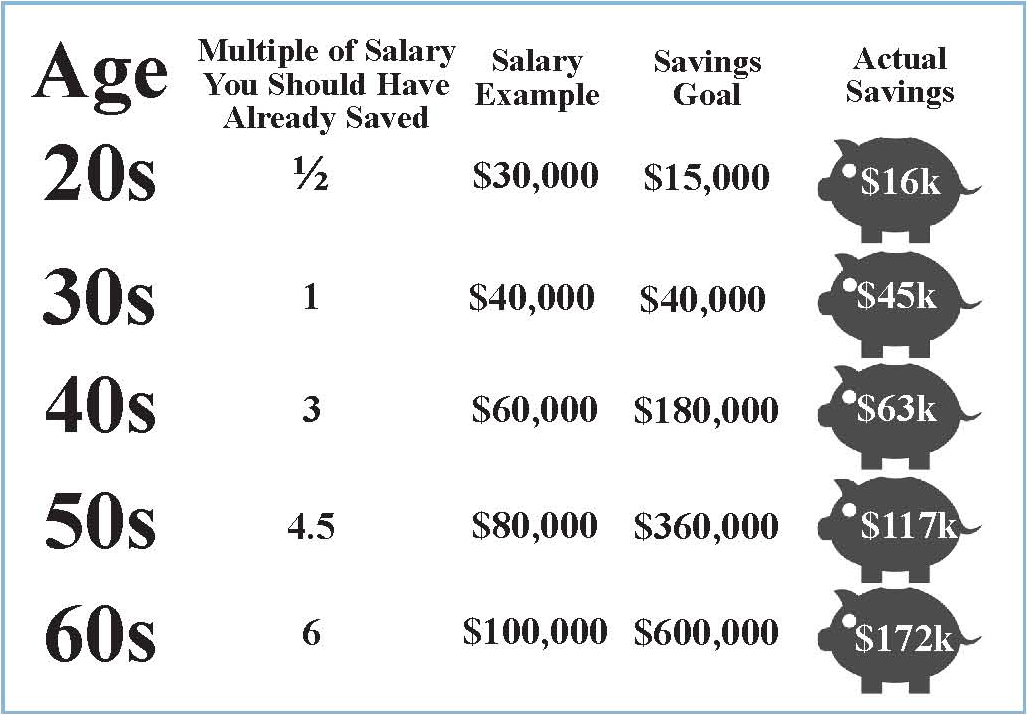

Multiples of Your Salary by Age

Financial advisors often recommend saving a certain multiple of your salary by specific ages to stay on track. While figures vary slightly, a common progression might look like this:

- Age 30: 1x your annual salary

- Age 40: 3x your annual salary

- Age 50: 6x your annual salary

- Age 60: 8x your annual salary

- Age 67 (Retirement): 10x your annual salary

These benchmarks are useful for gauging your progress. If you earn $100,000 at age 40 and have $300,000 saved, you’re generally on target according to this rule. If you’re behind, it signals a need to increase your savings rate.

Building Your Personalized Retirement Blueprint

While rules of thumb offer a general idea, a truly effective retirement plan requires a detailed, personalized blueprint. This involves a more rigorous analysis of your anticipated income and expenses.

Projecting Your Retirement Expenses

This is the most crucial and often overlooked step. Start by itemizing your current monthly expenses. Then, adjust them for what you anticipate in retirement.

- Decrease: Mortgage (if paid off), commuting, work-related expenses, dependent care, saving for retirement itself.

- Increase: Healthcare, travel, hobbies, entertainment, potentially new home maintenance costs (if you downsize or move to a larger property), discretionary spending on leisure.

- New Expenses: Long-term care insurance, higher utility bills (if home more often), new insurance needs.

Create a detailed budget that reflects your desired retirement lifestyle, listing everything from groceries and utilities to travel funds and unexpected repairs. This bottom-up approach provides a much more accurate picture than relying solely on income replacement ratios.

Estimating Future Income Streams

Your retirement income won’t solely come from your savings. Identify all potential sources:

- Social Security: Estimate your benefits. You can get an estimate from the Social Security Administration website. Remember that these benefits are typically not enough to live on their own.

- Pensions: If you’re fortunate enough to have a defined benefit pension plan from a previous employer, factor that in.

- Investment Income: This will be the primary source for most, derived from your 401(k), IRA, Roth IRA, brokerage accounts, etc.

- Part-Time Work: Many retirees choose to work part-time for enjoyment or to supplement their income.

- Other Assets: Rental income from properties, royalties, or other passive income sources.

Subtract your estimated annual income from these sources from your projected annual expenses. The remaining amount is the gap your personal savings will need to cover.

Accounting for Unexpected Costs and Contingencies

Life is unpredictable, and retirement is no exception. It’s wise to build a buffer for unexpected costs. This could include:

- Emergency Fund: A separate fund for sudden major home repairs, medical emergencies not fully covered by insurance, or other unforeseen expenses.

- Inflation Spikes: While you factor in average inflation, there could be periods of higher-than-expected inflation that erode your purchasing power faster.

- Market Downturns: Your investment portfolio will experience fluctuations. A significant downturn early in retirement could seriously impact your long-term sustainability (this is where the safe withdrawal rate becomes critical).

- Family Needs: You might need to assist adult children or elderly parents.

Consider allocating a portion of your projected savings to a contingency fund or designing your withdrawal strategy with a conservative buffer.

Key Pillars of a Robust Retirement Portfolio

Accumulating the necessary funds requires a strategic approach to saving and investing. It’s not just about how much you save, but also where and how you save it.

Leveraging Tax-Advantaged Accounts (401k, IRA, HSA)

These accounts are designed to encourage retirement savings by offering significant tax benefits.

- 401(k) / 403(b): Offered through employers, these allow pre-tax contributions to grow tax-deferred. Many employers offer matching contributions, which is essentially free money and should always be maximized.

- Traditional IRA: Allows pre-tax contributions to grow tax-deferred. Withdrawals in retirement are taxed as ordinary income.

- Roth IRA / Roth 401(k): Contributions are made with after-tax dollars, but qualified withdrawals in retirement are entirely tax-free. This offers incredible flexibility, especially if you anticipate being in a higher tax bracket in retirement.

- Health Savings Account (HSA): If you have a high-deductible health plan, an HSA offers a “triple tax advantage”: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. It can also function as an additional retirement savings vehicle after age 65, where withdrawals for non-medical expenses are taxed like a traditional IRA.

Diversification and Asset Allocation Strategies

Don’t put all your eggs in one basket. Diversification across different asset classes (stocks, bonds, real estate, cash equivalents) is crucial to manage risk and optimize returns. Your asset allocation should generally align with your age and risk tolerance. Younger investors with a longer time horizon can typically afford to take on more risk (e.g., higher stock allocation), while those closer to retirement usually shift towards a more conservative portfolio with a higher allocation to bonds and cash to preserve capital. Rebalance your portfolio periodically to maintain your desired allocation.

The Power of Compound Interest: Starting Early

The single most powerful tool in your retirement arsenal is compound interest. The earlier you start saving, the less you have to save overall, thanks to the exponential growth of your investments over time. Even small, consistent contributions made early can snowball into substantial sums. Delaying your savings by just a few years can dramatically increase the amount you need to save monthly to catch up. Time truly is your greatest asset when it comes to retirement planning.

Actionable Steps Towards Financial Freedom

The question of “how much for retirement” can feel overwhelming, but breaking it down into manageable steps makes the journey achievable.

1. Define Your Vision

Spend time truly visualizing your ideal retirement. Don’t just think about numbers; consider experiences, feelings, and daily routines. This qualitative exercise will give you the motivation and clarity needed to power your quantitative planning.

2. Calculate Your Gap

Armed with your projected expenses and estimated income streams, calculate the exact annual shortfall your savings will need to cover. Then, use the 4% rule (or a more conservative 3% or 3.5% withdrawal rate) to determine your target nest egg. For instance, if you need $60,000 annually from savings, and you plan for a 4% withdrawal rate, you’ll need $1,500,000 ($60,000 / 0.04).

3. Automate Your Savings

Make saving non-negotiable by setting up automatic transfers from your checking account to your retirement accounts with every paycheck. “Pay yourself first” ensures your savings grow consistently without you having to actively think about it each month. Increase your contributions whenever you get a raise.

4. Seek Professional Guidance

Consider consulting a qualified financial advisor. They can help you create a personalized plan, optimize your investment strategy, navigate complex tax laws, and provide guidance on estate planning and risk management. A good advisor acts as a coach, keeping you accountable and adjusting your plan as life changes.

5. Review and Adapt Regularly

Your retirement plan isn’t a static document. Life changes – salaries increase, expenses shift, market conditions evolve, and your goals may even change. Review your plan annually, or whenever a major life event occurs (marriage, divorce, new child, job change), and make necessary adjustments to stay on track.

Ultimately, “how much for retirement” isn’t a single number to be feared, but a dynamic goal to be understood, planned for, and actively pursued. By taking a thoughtful, proactive approach, you can transform this daunting question into a clear, actionable path towards a secure and fulfilling future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.