In the intricate world of personal finance and investing, few concepts hold as much transformative power as compounded interest. Often referred to as the “eighth wonder of the world” by Albert Einstein, it is the engine that drives exponential wealth creation over time. Far from being a mere accounting principle, understanding and harnessing compounded interest is fundamental to anyone aspiring to build financial security, achieve long-term investment goals, and truly comprehend the dynamics of both growth and debt.

At its most basic, compounded interest is the interest earned not only on the initial principal but also on the accumulated interest from previous periods. Unlike simple interest, which is calculated solely on the original principal amount, compounding allows your money to grow at an accelerating rate. It creates a snowball effect, where each period’s earnings become part of the principal for the next period, generating even more interest. This seemingly subtle difference is, in fact, the bedrock upon which significant financial fortunes are built and, conversely, where debt can become overwhelmingly burdensome. Grasping its mechanics is not just theoretical; it’s a critical step toward making informed financial decisions that shape your future.

The Core Mechanics of Compounding

To truly appreciate the power of compounded interest, one must first understand its underlying mechanisms and how it fundamentally differs from its simpler counterpart. It’s in these foundational principles that the true magic of wealth accumulation begins to unfold.

Simple vs. Compound Interest: A Fundamental Distinction

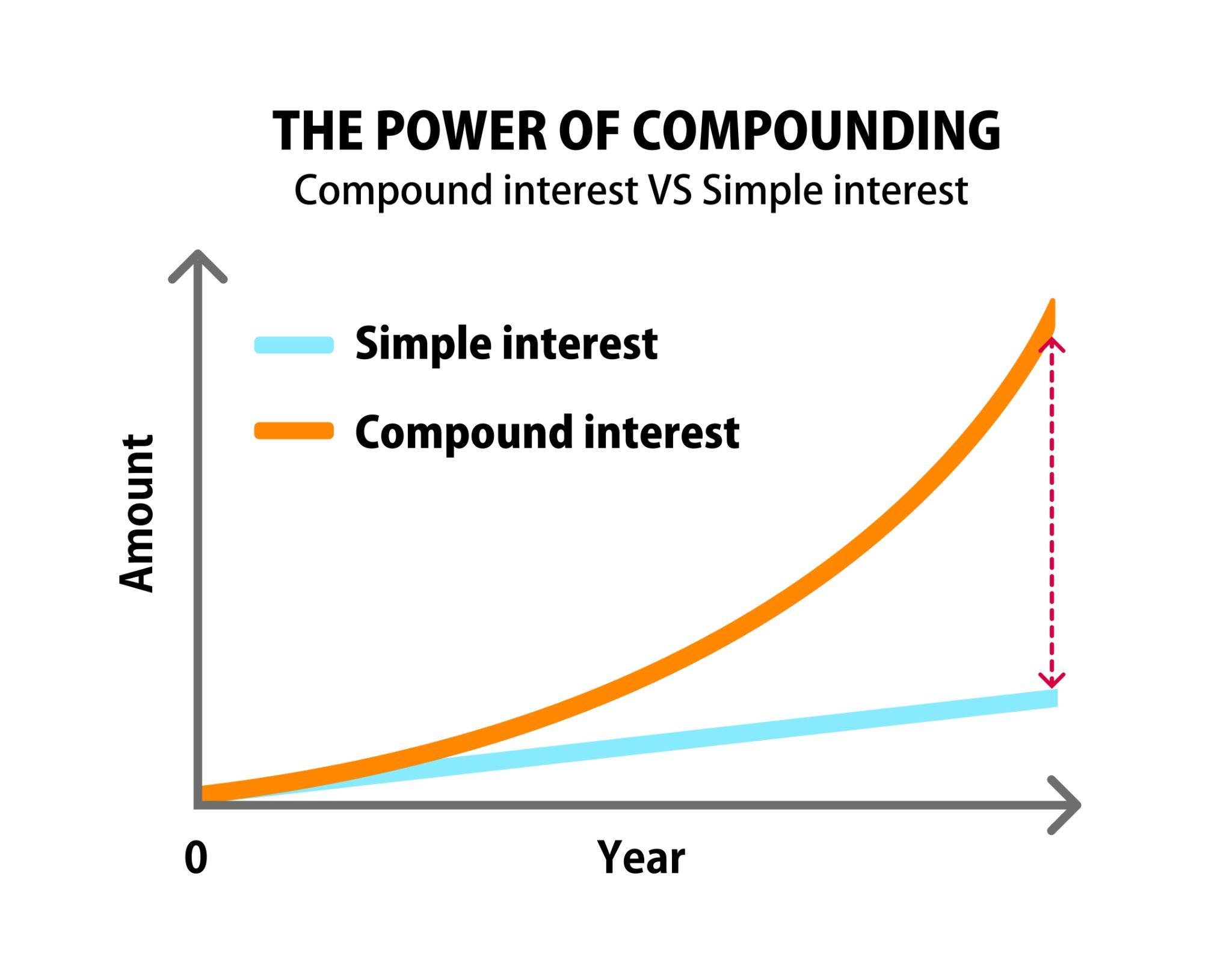

Imagine you invest $1,000 at an annual interest rate of 5%.

With simple interest, after one year, you would earn $50 ($1,000 * 0.05). After two years, you would earn another $50, bringing your total interest to $100 and your principal to $1,100. Each year, the interest calculation always refers back to the original $1,000.

With compounded interest, the calculation changes. After the first year, you still earn $50, making your total $1,050. However, in the second year, the 5% interest is applied not to the original $1,000, but to the new total of $1,050. This means you earn $52.50 ($1,050 * 0.05), bringing your total to $1,102.50. While the difference initially seems small, over decades, this additional $2.50 (and the accumulating interest on that interest) can translate into hundreds of thousands, if not millions, of dollars. This is the essence of compounding: interest earning interest.

The “Interest on Interest” Principle

This principle is the beating heart of compounded growth. Each time interest is calculated and added to the principal, that new, larger sum becomes the base for the next interest calculation. This iterative process creates an accelerating curve of growth. It means your money isn’t just working for you; it’s also making its earnings work for you. This exponential effect is why starting early and letting your investments grow undisturbed for extended periods is paramount. The longer the money compounds, the more pronounced the “interest on interest” effect becomes.

Key Variables Influencing Compounding Growth

Several factors dictate the speed and magnitude of compounded growth:

- Principal (P): The initial amount of money invested or saved. A larger principal will naturally lead to larger interest earnings.

- Interest Rate (r): The percentage at which your money grows each period. Even small differences in rates can lead to significant disparities over the long term. A higher rate means faster growth.

- Time (t): The duration over which the money is allowed to compound. This is arguably the most critical variable, as the exponential nature of compounding truly takes hold over decades, not years.

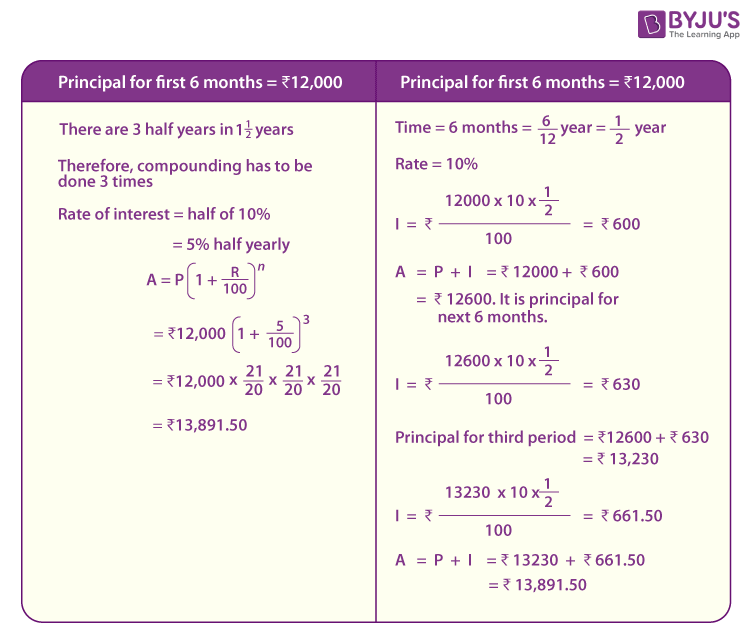

- Compounding Frequency (n): How often the interest is calculated and added to the principal (e.g., annually, semi-annually, quarterly, monthly, daily). The more frequent the compounding, the faster the money grows, assuming the same annual interest rate. For instance, an investment compounding daily will grow slightly faster than one compounding annually, even if both have a 5% annual percentage rate (APR).

Understanding how these variables interact is crucial for making strategic financial decisions, whether it’s choosing a savings account, evaluating investment opportunities, or managing debt.

The Power of Time: Unlocking Exponential Growth

While interest rates and principal amounts are important, it is the element of time that truly unleashes the full, awe-inspiring potential of compounded interest. Time is the multiplier that transforms steady contributions into substantial wealth.

Early Start: The Greatest Advantage

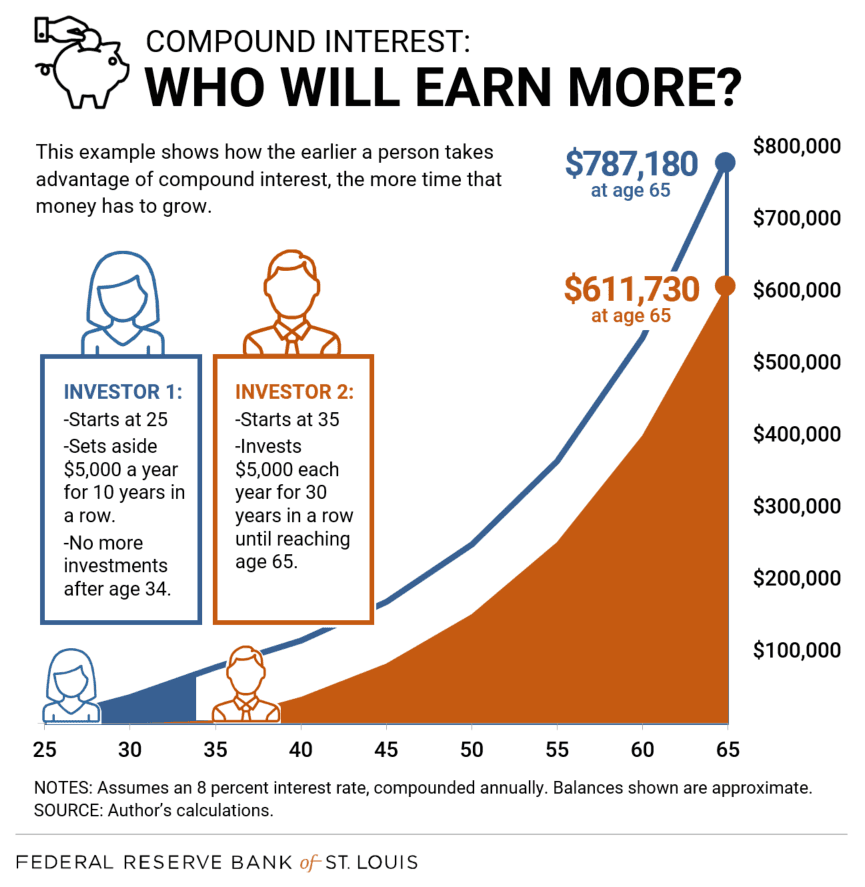

One of the most profound lessons in personal finance is the incredible advantage of starting to save and invest early. Because compounding works exponentially, the early years, even with smaller contributions, contribute disproportionately to future wealth. Imagine two individuals: Investor A starts at age 25, investing $200 per month for 10 years and then stops, letting their money grow until age 65. Investor B starts at age 35, investing $200 per month for 30 years, also until age 65. Assuming a modest 7% annual return, Investor A, who contributed for only 10 years, will likely have significantly more money at age 65 than Investor B, who contributed for three times as long but started later. This phenomenon vividly illustrates that time in the market is far more impactful than trying to time the market or simply contributing more later in life. The initial contributions have the longest runway to compound, making them incredibly powerful.

The Compounding Curve: Visualizing Growth

When plotted on a graph, the growth of an investment under compound interest doesn’t follow a straight line; it follows an upward-sloping curve that becomes increasingly steep over time. In the initial years, the growth appears modest, almost linear. Many individuals, seeing slow progress, become discouraged. However, as the principal and accumulated interest grow, the amount of interest earned in each subsequent period becomes larger, causing the curve to bend sharply upwards. This inflection point, where growth truly accelerates, often occurs later in the investment horizon. This “hockey stick” curve is the visual representation of exponential growth and underscores why patience is not just a virtue but a financial superpower when it comes to compounding.

Patience and Consistency: Cornerstones of Success

The greatest enemy of compounded interest is impatience. Many investors, looking for quick gains, withdraw their money or alter their strategies too frequently, disrupting the compounding process. Successful compounding requires a steadfast commitment to regular contributions and the discipline to let investments mature over extended periods, weathering market fluctuations without panic. Consistency, both in contributing funds and in maintaining an investment strategy, ensures that your money continually benefits from the interest-on-interest principle. Even small, consistent contributions made over decades can accumulate into substantial wealth, thanks to the unwavering force of compounding.

Practical Applications in Personal Finance

Compounded interest is not merely an abstract concept; it is the underlying mechanism for growth (and sometimes debt) across a myriad of financial products and strategies relevant to everyday personal finance and investing.

Investing: Stocks, Bonds, Mutual Funds, ETFs

At the heart of long-term investing across various asset classes lies compounding.

- Stocks: When you invest in dividend-paying stocks and choose to reinvest those dividends, you’re directly leveraging compounding. The dividends purchase more shares, which then generate even more dividends, creating a self-reinforcing growth loop. Even without dividends, the capital appreciation of stocks held over long periods is a form of compounding, as the growth builds on previous growth.

- Bonds: While often seen as less volatile, bonds also compound. If you hold a bond and reinvest its interest payments (coupons), those reinvested payments start earning interest themselves, leading to compounded returns.

- Mutual Funds & ETFs: These pooled investment vehicles inherently benefit from compounding. As the underlying assets (stocks, bonds, etc.) grow and generate income, that growth is reinvested within the fund, allowing your fund units to appreciate faster due to the compounding effect of the underlying investments.

Savings Accounts and Certificates of Deposit (CDs)

These traditional banking products are straightforward examples of compounding.

- Savings Accounts: Most high-yield savings accounts compound interest daily or monthly, and then credit it to your account. This means your balance grows, and then the next interest calculation is based on that slightly larger balance, illustrating compounding at its simplest.

- Certificates of Deposit (CDs): CDs offer a fixed interest rate for a specified term. While some pay out interest periodically, many allow interest to compound within the CD until maturity, meaning you earn interest on your interest for the duration of the term, maximizing your return.

Retirement Planning: 401(k)s and IRAs

Retirement accounts are perhaps the most compelling real-world applications of compounded interest.

- 401(k)s and IRAs: These tax-advantaged accounts are designed for long-term growth, often spanning 30-40 years. The contributions you make, combined with employer matches (in 401(k)s), are invested and grow completely tax-deferred (or tax-free in a Roth account). This allows the investments to compound undisturbed for decades, leading to substantial sums by retirement age. The tax benefits further amplify the compounding effect by preventing taxes from eroding growth each year.

Understanding the Debt Side: Credit Cards and Loans

While largely discussed as a wealth-building tool, compounded interest has a formidable negative side, particularly with debt.

- Credit Cards: The most insidious example. If you carry a balance on a credit card, interest is calculated on your outstanding principal and any unpaid interest from previous billing cycles. With high annual percentage rates (APRs) often exceeding 15-25%, compounded credit card interest can quickly spiral out of control, making it incredibly difficult to pay off debt.

- Loans (Mortgages, Student Loans): While structured differently, interest on loans also compounds. Mortgages, for instance, amortize over many years, meaning early payments largely go towards interest, which has compounded over time. Understanding how loan interest compounds is crucial for determining total cost and for strategizing accelerated repayment to save money.

Strategies to Maximize Compounding Returns

Understanding the mechanics of compounding is the first step; actively employing strategies to leverage its power is the next. By making conscious choices, individuals can significantly amplify their long-term financial growth.

Prioritize Early and Regular Contributions

As highlighted earlier, time is the ultimate multiplier for compounding. Starting to save and invest as early as possible, even with small amounts, provides your money the longest possible runway to grow exponentially. Furthermore, making regular contributions, ideally automatically, ensures consistent capital injection that continuously benefits from the compounding effect. This disciplined approach smooths out market fluctuations (through dollar-cost averaging) and steadily builds your principal base.

Seek Higher Interest Rates (Wisely)

While the principal and time are crucial, the interest rate significantly impacts the speed of growth. A difference of even 1-2% in annual return can lead to tens, or even hundreds, of thousands of dollars more over a few decades.

- For Savings: Look for high-yield savings accounts, money market accounts, or CDs that offer competitive rates.

- For Investments: Carefully select investment vehicles (stocks, bonds, mutual funds) that align with your risk tolerance and have a track record of reasonable returns. However, chasing extremely high, unrealistic returns often comes with disproportionately high risk. The key is to seek the highest sustainable rates of return that fit your financial plan.

Reinvesting Returns

One of the most direct ways to turbocharge compounding is to consistently reinvest any earnings.

- Dividends: If you own dividend-paying stocks or mutual funds, opt for dividend reinvestment plans (DRIPs), which automatically use your dividends to buy more shares.

- Interest: In savings accounts or CDs, allow the interest to remain in the account so it can earn interest itself in subsequent periods.

- Capital Gains: When you sell an investment for a profit, consider reinvesting those gains into new opportunities rather than spending them. Every dollar reinvested becomes a new seed for future compounding.

Minimizing Fees and Taxes

Fees and taxes are silent erosions of your compounded growth. Each dollar lost to fees or taxes is a dollar that cannot compound for you.

- Fees: Be mindful of management fees in mutual funds, expense ratios in ETFs, transaction fees in brokerage accounts, and any administrative charges on retirement accounts. Even seemingly small annual fees (e.g., 1% of assets) can significantly diminish your total returns over decades. Prioritize low-cost index funds and ETFs where appropriate.

- Taxes: Utilize tax-advantaged accounts like 401(k)s, IRAs (Traditional or Roth), and HSAs. These accounts allow your investments to grow tax-deferred or tax-free, meaning the full sum can compound without annual deductions for capital gains or income tax until withdrawal (or ever, in the case of Roth accounts). This significantly enhances the effective compounding rate.

The Psychology and Philosophy of Compounding

Beyond the mathematical formulas and practical strategies, compounded interest also offers profound lessons in patience, discipline, and a long-term perspective—qualities that extend beyond finance into many aspects of life.

The Magic of the Long Run

Compounding thrives on the long run. It’s an affirmation of the adage that “slow and steady wins the race.” In a world often obsessed with instant gratification and quick returns, compounding forces us to embrace a marathon mindset. It teaches us that significant results often emerge not from single, dramatic events, but from the consistent application of sound principles over extended periods. This perspective shift, from short-term gains to long-term wealth building, is a cornerstone of financial wisdom.

Avoiding Behavioral Pitfalls (Impatience, Market Timing)

The exponential nature of compounding means that early returns can seem underwhelming, which often leads to impatience. Investors might get discouraged and pull out their money, or chase after speculative investments promising unrealistic immediate returns, thereby forfeiting the true power of long-term compounding. Similarly, trying to “time the market”—buying low and selling high consistently—is notoriously difficult and often leads to missing key growth periods that are crucial for compounding. The most successful approach for leveraging compounding is typically a consistent, diversified investment strategy held for many years, resisting the urge to react to every market fluctuation.

Compounding as a Wealth-Building Mindset

Ultimately, understanding compounded interest is about more than just numbers; it’s about adopting a specific mindset towards wealth. It’s the recognition that every financial decision, big or small, has implications for future growth or debt accumulation. It’s about prioritizing delayed gratification for greater future reward, making consistent efforts, and trusting in the power of time. This mindset encourages frugality, disciplined saving, strategic investing, and responsible debt management, all of which are critical for achieving long-term financial freedom.

In conclusion, compounded interest is not just a financial calculation; it is a fundamental principle governing the growth of wealth. By understanding its mechanics, leveraging the power of time, applying effective strategies, and adopting a long-term, disciplined mindset, individuals can truly unlock its extraordinary potential to build substantial financial security and achieve their most ambitious financial aspirations. It is indeed a wonder, accessible to all who choose to understand and embrace its power.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.